Market Overview

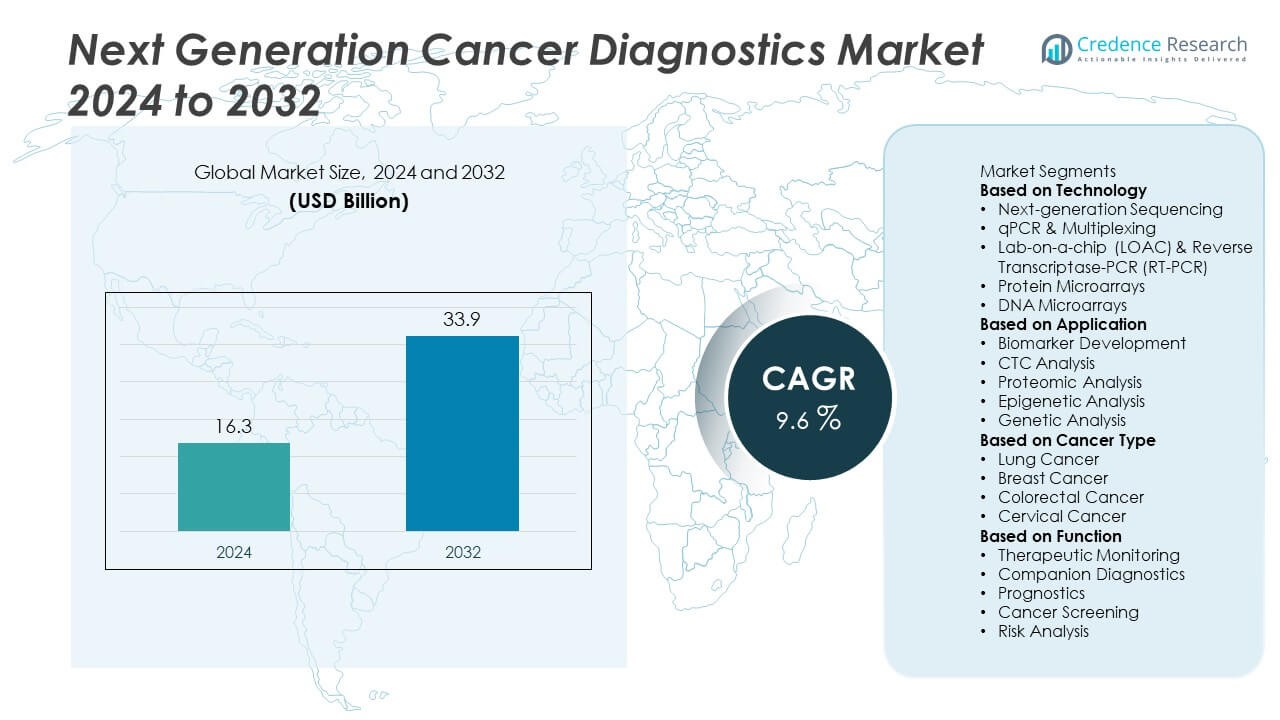

The Next Generation Cancer Diagnostics Market was valued at USD 16.3 billion in 2024 and is projected to reach USD 33.9 billion by 2032, growing at a CAGR of 9.6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Next Generation Cancer Diagnostics Market Size 2024 |

USD 16.3 Billion |

| Next Generation Cancer Diagnostics Market, CAGR |

9.6% |

| Next Generation Cancer Diagnostics Market Size 2032 |

USD 33.9 Billion |

The Next Generation Cancer Diagnostics Market grows through strong drivers and evolving trends that shape its progress. Rising demand for early detection, precision oncology, and personalized treatment fuels adoption of advanced diagnostic tools. It benefits from the rapid uptake of liquid biopsies and next-generation sequencing.

The Next Generation Cancer Diagnostics Market demonstrates strong geographical presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with each region contributing to growth through distinct strengths. North America leads adoption due to advanced healthcare infrastructure, extensive clinical research, and early integration of precision medicine. Europe emphasizes collaborative cancer research programs and government-backed initiatives that support early detection and biomarker-driven diagnostics. Asia-Pacific emerges as a high-growth hub, supported by rising cancer incidence, improving healthcare access, and strong government investment in genomic medicine. Latin America and the Middle East & Africa show gradual progress, driven by expanding awareness and infrastructure upgrades. Key players driving innovation and expanding global reach include Illumina, Inc., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, and QIAGEN. Their focus on advanced sequencing, liquid biopsy development, and AI integration reinforces competitiveness and strengthens the global diagnostics ecosystem.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Next Generation Cancer Diagnostics Market was valued at USD 16.3 billion in 2024 and is projected to reach USD 33.9 billion by 2032, growing at a CAGR of 9.6%.

- Rising demand for early cancer detection and precision medicine drives adoption of advanced diagnostic technologies across clinical and research settings.

- Increasing trends include the integration of liquid biopsies, next-generation sequencing, and AI-based digital pathology, improving accuracy and reducing reliance on invasive procedures.

- Competitive dynamics remain strong, with key players such as Illumina, Thermo Fisher Scientific, F. Hoffmann-La Roche, and QIAGEN focusing on expanding genomic platforms, companion diagnostics, and multi-omics solutions.

- High costs of advanced diagnostic tools, limited reimbursement policies, and regulatory complexities act as restraints, slowing widespread adoption in low-resource regions.

- North America leads the market due to robust infrastructure, clinical trials, and strong investment in molecular diagnostics, while Europe follows with collaborative research programs and emphasis on early detection.

- Asia-Pacific emerges as a high-growth hub with rising cancer prevalence, growing healthcare investments, and supportive government initiatives, while Latin America and the Middle East & Africa show steady but slower adoption driven by awareness campaigns and infrastructure expansion.

Market Drivers

Rising Emphasis on Early Detection and Personalized Medicine

The Next Generation Cancer Diagnostics Market gains momentum from the rising focus on early disease detection and precision medicine. Healthcare providers prioritize tests that identify cancer at treatable stages. It supports improved survival rates and reduces long-term treatment costs. Growing demand for personalized therapies drives adoption of molecular diagnostics, liquid biopsies, and companion testing. Physicians increasingly rely on genetic and genomic insights to design tailored treatment plans. The shift toward precision oncology ensures steady expansion of advanced diagnostic platforms.

- For instance, Illumina’s TruSight Oncology 500 (TSO 500) assays, which have been adopted by laboratories worldwide since 2018, can enable the profiling of 523 cancer-relevant DNA genes in a single test. In addition to DNA variants, the tissue-based TSO 500 assays can also profile RNA fusions and other biomarkers within the same workflow.

Increasing Adoption of Liquid Biopsies and Non-Invasive Technologies

The Next Generation Cancer Diagnostics Market benefits from strong interest in liquid biopsy solutions and other non-invasive methods. Patients and clinicians favor procedures that reduce surgical risks and provide faster results. It offers real-time insights into tumor progression through circulating tumor DNA and other biomarkers. The convenience and safety of liquid biopsies make them a preferred choice across oncology practices. Growing validation of clinical utility strengthens confidence among healthcare providers. Expanding research in this field supports a broader range of applications.

- For instance, in 2024, Guardant Health’s reports show they processed approximately 206,700 clinical and 40,500 biopharma liquid biopsy tests, demonstrating growing adoption for both routine patient care and clinical trials. The original figure only accounted for clinical tests, omitting those for biopharma customers.

Integration of Artificial Intelligence and Genomic Sequencing Advancements

The Next Generation Cancer Diagnostics Market advances with the integration of artificial intelligence and next-generation sequencing tools. AI algorithms enhance accuracy in detecting cancer markers and predicting treatment response. It supports the analysis of large genomic datasets with greater efficiency. Progress in sequencing technologies reduces costs and accelerates adoption across clinical laboratories. Hospitals and research centers increasingly apply AI-based platforms for diagnostic decision-making. These developments strengthen clinical outcomes and foster wider use of advanced diagnostics.

Expanding Government Support and Rising Research Investments

The Next Generation Cancer Diagnostics Market benefits from expanding government funding and institutional research initiatives. Policymakers support innovation in diagnostics to address the growing cancer burden. It drives clinical trials and accelerates approval of advanced testing solutions. Public health programs promote access to molecular testing and screening tools. Investments from global research bodies encourage collaborations between diagnostic companies and academic centers. Strengthened policy frameworks and financial incentives improve adoption rates in both developed and emerging markets.

Market Trends

Growing Use of Multi-Omics Approaches in Cancer Diagnostics

The Next Generation Cancer Diagnostics Market progresses with the integration of multi-omics technologies, including genomics, proteomics, and metabolomics. Researchers combine these datasets to achieve a more comprehensive understanding of cancer biology. It enhances the precision of diagnostic tools and supports accurate treatment planning. Multi-omics platforms help uncover hidden biomarkers and provide a holistic view of disease progression. Pharmaceutical companies adopt such methods to guide drug development and clinical trials. These approaches create opportunities for more personalized and effective cancer care.

- For instance, QIAGEN’s QIAseq kits have historically processed more than four million next-generation sequencing (NGS) samples for a variety of applications, including cancer research.

Rising Adoption of Point-of-Care Diagnostic Solutions

The Next Generation Cancer Diagnostics Market shows strong growth in point-of-care testing solutions. Patients and clinicians demand rapid, accurate, and portable diagnostic platforms for faster decision-making. It reduces the reliance on centralized laboratories and broadens access to advanced testing in remote areas. Portable devices support continuous monitoring of patients and facilitate timely adjustments in therapy. Healthcare systems adopt these solutions to improve efficiency and reduce diagnostic delays. The expansion of point-of-care tools reflects a shift toward decentralized cancer diagnostics.

- For instance, Abbott’s The ID NOW is a rapid, instrument-based diagnostic platform for detecting infectious diseases caused by various pathogens, including COVID-19, Influenza A & B, Strep A, and RSV.

Expansion of Digital Pathology and Artificial Intelligence Applications

The Next Generation Cancer Diagnostics Market benefits from the expansion of digital pathology platforms supported by artificial intelligence. AI-enabled systems improve diagnostic accuracy by automating image analysis and detecting subtle cellular changes. It allows pathologists to process large volumes of slides with improved speed and consistency. Hospitals invest in AI-assisted tools to strengthen clinical decision-making and optimize workflows. These solutions also enable remote consultations and collaborative reviews among specialists. Digital pathology adoption creates scalable and efficient diagnostic ecosystems.

Increasing Focus on Liquid Biopsy Applications Beyond Oncology

The Next Generation Cancer Diagnostics Market experiences a shift as liquid biopsy technology extends into broader clinical applications. While oncology remains the primary focus, liquid biopsies gain attention in monitoring organ transplant health and prenatal testing. It expands the utility of circulating biomarkers across multiple disease areas. Companies invest heavily in research to validate new applications and strengthen market presence. Broader acceptance of liquid biopsy improves clinical confidence and accelerates adoption in diverse medical fields. This trend enhances the long-term growth prospects of diagnostic technologies.

Market Challenges Analysis

High Costs and Limited Accessibility of Advanced Diagnostic Technologies

The Next Generation Cancer Diagnostics Market faces challenges due to the high cost of advanced testing platforms. Many healthcare systems struggle to afford genomic sequencing, liquid biopsies, and AI-enabled tools. It creates disparities in access between developed and emerging economies. Patients in low-resource regions face delays or lack of access to cutting-edge diagnostics. Limited reimbursement policies further restrict adoption and discourage hospitals from investing in these technologies. The cost barrier slows down the pace of global adoption and limits widespread clinical integration.

Regulatory Complexities and Data Management Constraints

The Next Generation Cancer Diagnostics Market also encounters challenges linked to regulatory hurdles and data management. Obtaining approvals for new diagnostic methods requires extensive validation and long timelines. It delays the introduction of innovative solutions into clinical practice. Large-scale use of genomic and multi-omics testing generates massive datasets that demand secure storage and advanced analysis systems. Hospitals face issues related to data privacy, integration, and interoperability across platforms. These constraints hinder the efficiency of diagnostic workflows and limit the scalability of advanced technologies.

Market Opportunities

Expansion into Emerging Healthcare Markets and Untapped Regions

The Next Generation Cancer Diagnostics Market presents strong opportunities in emerging economies with rising cancer prevalence and improving healthcare infrastructure. Countries in Asia-Pacific, Latin America, and parts of Africa are increasing investments in advanced diagnostics. It creates pathways for diagnostic companies to expand their footprint and form local partnerships. Growing awareness of early detection and government-driven screening programs support faster adoption. Lower-cost testing solutions tailored for resource-limited settings can unlock significant patient reach. Companies that address affordability and accessibility will capture long-term growth potential in these untapped regions.

Advancements in Companion Diagnostics and Precision Oncology Integration

The Next Generation Cancer Diagnostics Market also benefits from opportunities in companion diagnostics that support personalized medicine. Pharmaceutical firms actively collaborate with diagnostic providers to align targeted therapies with specific biomarkers. It enhances treatment effectiveness and improves patient outcomes across oncology care. Expanding adoption of precision oncology creates demand for genomic profiling and multi-omics platforms. Research institutions and biotech companies are investing in collaborative studies to validate new biomarkers. Wider acceptance of companion diagnostics will strengthen integration of diagnostics into therapeutic pathways and drive new revenue streams for industry leaders.

Market Segmentation Analysis:

By Technology

The Next Generation Cancer Diagnostics Market is segmented into next-generation sequencing, polymerase chain reaction, liquid biopsy, immunoassays, and others. Next-generation sequencing leads the segment due to its ability to provide comprehensive genomic data and support precision oncology. It enables rapid identification of genetic mutations and tumor-specific markers, improving personalized treatment planning. Liquid biopsy is gaining momentum as a non-invasive alternative for monitoring disease progression and treatment response. Immunoassays maintain steady demand due to their role in detecting protein biomarkers with high sensitivity. Together, these technologies offer diverse diagnostic capabilities that strengthen clinical decision-making.

- For instance, in 2023, Thermo Fisher introduced new innovative products, including an electron-beam-based solution for semiconductors and an ultrapure water purification system for laboratories.

By Application

The Next Generation Cancer Diagnostics Market finds application in screening, diagnostics, prognosis, therapy selection, and monitoring. Screening remains vital as healthcare systems push for early cancer detection to improve survival outcomes. It helps in identifying high-risk populations and reducing late-stage diagnoses. Diagnostics and prognosis functions play a central role in confirming cancer presence and predicting disease progression. Therapy selection is growing in importance, as clinicians rely on biomarker-driven tests to choose effective treatments. Monitoring applications support ongoing patient management by assessing therapeutic response and detecting recurrence. Expanding use across these applications enhances the clinical value of advanced diagnostic platforms.

- For instance, in 2024, Roche’s Diagnostics Division delivered 30 billion tests globally. Roche’s Diagnostics Division has a broad portfolio covering different disease areas like oncology, infectious diseases, and women’s health. The company is a major player in companion diagnostics (CDx), which are tests used to determine if a patient will benefit from a specific targeted drug.

By Cancer Type

The Next Generation Cancer Diagnostics Market covers breast cancer, lung cancer, colorectal cancer, prostate cancer, and other types. Breast cancer dominates the segment due to high global prevalence and widespread screening programs. It benefits from strong adoption of molecular tests that improve early detection and guide treatment strategies. Lung cancer diagnostics are expanding as demand for non-invasive liquid biopsies rises, offering faster results for critical cases. Colorectal cancer screening programs continue to strengthen adoption of advanced assays across developed regions. Prostate cancer and other rare cancers also drive demand for genomic profiling and biomarker-based tests. The growing use of tailored diagnostics across multiple cancer types supports the broader adoption of advanced technologies.

Segments:

Based on Technology

- Next-generation Sequencing

- qPCR & Multiplexing

- Lab-on-a-chip (LOAC) & Reverse Transcriptase-PCR (RT-PCR)

- Protein Microarrays

- DNA Microarrays

Based on Application

- Biomarker Development

- CTC Analysis

- Proteomic Analysis

- Epigenetic Analysis

- Genetic Analysis

Based on Cancer Type

- Lung Cancer

- Breast Cancer

- Colorectal Cancer

- Cervical Cancer

Based on Function

- Therapeutic Monitoring

- Companion Diagnostics

- Prognostics

- Cancer Screening

- Risk Analysis

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounted for the largest market share of around 38% in the Next Generation Cancer Diagnostics Market in 2024. The region benefits from advanced healthcare infrastructure, high adoption of innovative diagnostic technologies, and strong presence of leading biotechnology and pharmaceutical companies. It shows consistent growth supported by favorable reimbursement frameworks and large-scale government initiatives promoting precision medicine. The United States dominates regional demand with its extensive clinical trials, integration of genomic sequencing in oncology, and strong pipeline of biomarker-based companion diagnostics. Canada also contributes significantly through cancer prevention programs and adoption of molecular testing across public health institutions. It maintains leadership due to early adoption of next-generation sequencing, liquid biopsies, and AI-powered diagnostic platforms.

Europe

Europe represented a market share of nearly 27% in the Next Generation Cancer Diagnostics Market in 2024. The region benefits from strong policy support, active investments in cancer research, and collaborative programs across academic and healthcare institutions. Countries such as Germany, the United Kingdom, and France lead adoption through national cancer strategies that emphasize early detection and precision diagnostics. It has witnessed growing penetration of digital pathology and AI-assisted tools to support more accurate diagnostics. Rising demand for liquid biopsy technologies strengthens the role of molecular testing in clinical settings. The European Union’s focus on cross-border collaborations and data sharing also accelerates development of standardized diagnostic frameworks.

Asia-Pacific

Asia-Pacific captured approximately 23% market share in the Next Generation Cancer Diagnostics Market in 2024. Rapidly increasing cancer prevalence, expanding healthcare infrastructure, and rising investments in biotechnology support growth across the region. China dominates adoption with strong government-driven initiatives in genomics and growing collaborations with multinational diagnostic providers. Japan continues to strengthen its role with high adoption of liquid biopsy and sequencing technologies in cancer care. India shows strong potential driven by increasing cancer awareness and expanding healthcare access. It demonstrates high growth potential due to untapped patient populations and expanding affordability of molecular diagnostics. Rising investments from global companies position the region as a key growth hub.

Latin America

Latin America held a market share of close to 7% in the Next Generation Cancer Diagnostics Market in 2024. Brazil and Mexico lead the region with investments in cancer research programs and adoption of early detection tools. It experiences steady demand growth as governments expand access to public health services and screening initiatives. However, high costs and limited reimbursement policies continue to slow adoption rates across many countries. Diagnostic companies are targeting the region with lower-cost testing platforms and strategic collaborations with local healthcare providers. Growing cancer awareness campaigns and partnerships with global research bodies strengthen opportunities for expanded adoption.

Middle East & Africa

The Middle East & Africa accounted for nearly 5% market share in the Next Generation Cancer Diagnostics Market in 2024. The region shows gradual adoption, supported by growing investments in advanced healthcare infrastructure in countries like the United Arab Emirates and Saudi Arabia. South Africa leads adoption across Sub-Saharan Africa, with a growing emphasis on cancer awareness and screening programs. It faces barriers from limited healthcare access and high costs of advanced diagnostic tools. International collaborations and government-led initiatives are working to improve access to molecular diagnostics. Rising private-sector participation further drives slow but steady adoption across the region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- GE HealthCare

- QIAGEN

- Novartis AG

- Thermo Fisher Scientific Inc.

- Abbott

- Illumina, Inc.

- Hoffmann-La Roche Ltd

- Agilent Technologies, Inc. (Dako)

- Janssen Pharmaceuticals, Inc.

- Koninklijke Philips N.V.

Competitive Analysis

The competitive landscape of the Next Generation Cancer Diagnostics Market is shaped by leading players including Illumina, Inc., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, QIAGEN, Abbott, Agilent Technologies, Inc. (Dako), Janssen Pharmaceuticals, Inc., Novartis AG, Koninklijke Philips N.V., and GE HealthCare. These companies focus on innovation, strategic collaborations, and expansion of advanced diagnostic platforms to strengthen their market position. They invest heavily in next-generation sequencing, liquid biopsy technologies, and biomarker-driven companion diagnostics to meet the rising demand for precision oncology. Many players are advancing artificial intelligence integration and multi-omics approaches to improve accuracy and scalability of cancer diagnostics. Strong pipelines of molecular assays, partnerships with pharmaceutical firms for therapy-linked diagnostics, and expansion into emerging markets remain central strategies. Mergers, acquisitions, and research alliances also play a key role in broadening technology portfolios and enhancing global reach. The competitive environment remains dynamic, with continuous technological advancements driving strong differentiation among market leaders.

Recent Developments

- In June 2025, GE HealthCare introduced AI-driven molecular imaging innovations, enhancing visualization to aid therapy.

- In May 2025, the GE HealthCare highlighted its oncology workflow tools, including Omni Legend and MIM software, to support better patient outcomes.

- In May 2025, Novartis emphasized a reimagining of cancer care through radioligand therapy (RLT)—a targeted precision nuclear medicine approach.

- In January 2025, the Thermo Fisher Scientific Inc. partnered with UK Biobank to support the world’s largest human proteomics study via its Olink Explore platform.

Report Coverage

The research report offers an in-depth analysis based on Technology, Application, Cancer Type, Function and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Precision medicine will drive broader adoption of genomics-based diagnostics in clinical settings.

- Expansion of liquid biopsy use will support earlier detection and improve treatment monitoring.

- AI integration in pathology and imaging will sharpen diagnostic accuracy and reduce analysis time.

- Multi-omics tools will help uncover complex biomarker patterns and personalize cancer care.

- Decentralized point-of-care testing will extend access to advanced diagnostics in remote areas.

- Companion diagnostics will grow in importance, aligning more treatments with specific biomarkers.

- Regulatory frameworks will increasingly favor innovation through faster approvals and pilot programs.

- Emerging economies will fuel market growth by expanding cancer screening programs and lab infrastructure.

- Collaborative partnerships between diagnostics firms and biopharma will accelerate test development.

- Data sharing platforms and cloud analytics will streamline diagnostic workflows and improve interoperability.