Ni Based Superalloys Market Overview:

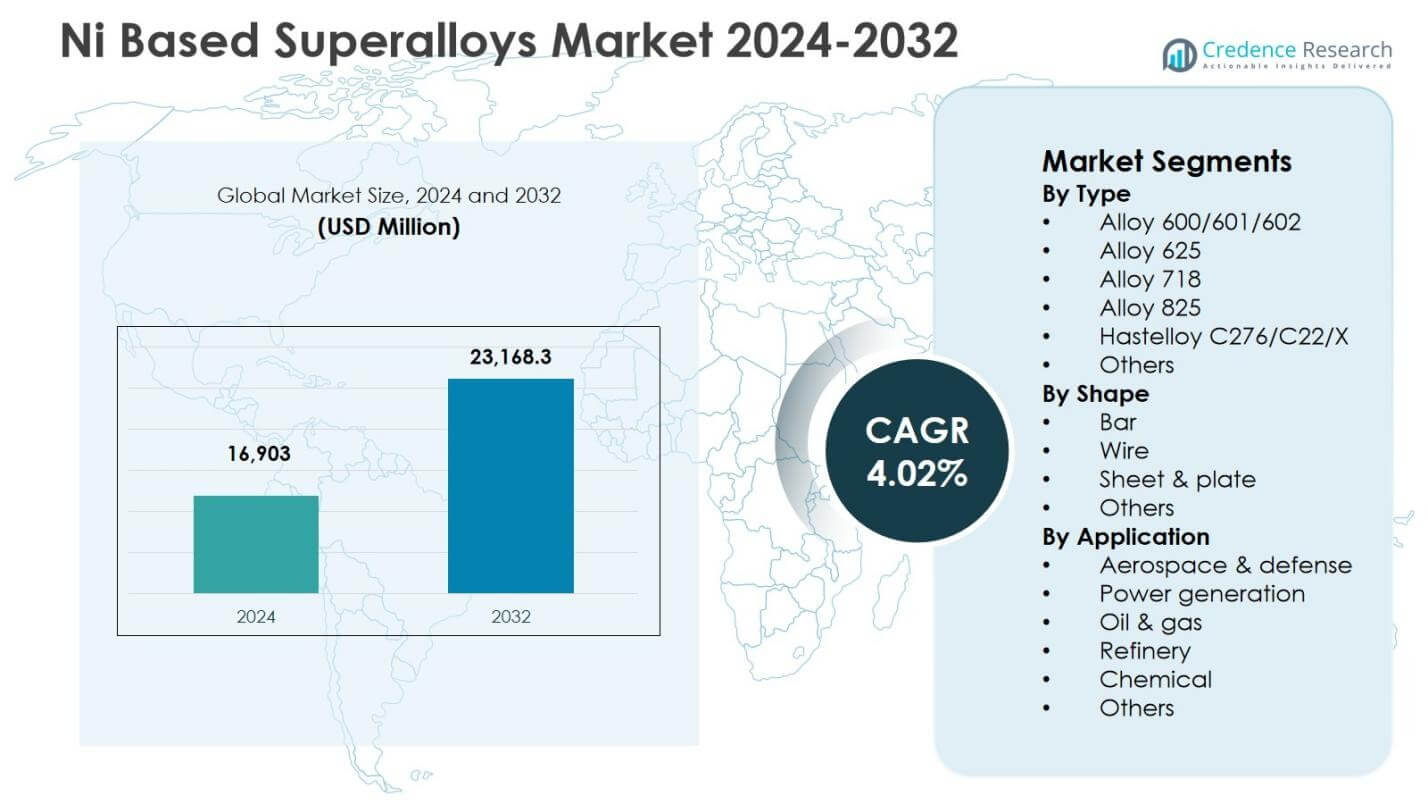

Ni Based Superalloys Market size was valued USD 16,903 Million in 2024 and is anticipated to reach USD 23,168.3 Million by 2032, at a CAGR of 4.02% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ni Based Superalloys Market Size 2024 |

USD 16,903 million |

| Ni Based Superalloys Market, CAGR |

4.02% |

| Ni Based Superalloys Market Size 2032 |

USD 23,168.3 million |

Ni Based Superalloys Market Insights

- The market is driven by rising demand from aerospace and defense engine manufacturing, turbine efficiency upgrades, and expanding use of high-temperature, corrosion-resistant materials in oil, gas, and chemical processing industries.

- Key market trends include increasing adoption of additive manufacturing for complex superalloy components, technological advancements in high-performance alloy grades, and growing investments in next-generation propulsion and hydrogen-ready turbine systems.

- Leading players strengthen market presence through material innovation, strategic supply partnerships, and capacity expansion initiatives, while the dominance of Alloy 718 with 34.2% share in 2024 reflects its widespread use in aerospace turbine and structural applications.

- Regional growth is led by North America with 32.6% share in 2024, followed by Europe with 27.4% and Asia-Pacific with 28.9%, supported by strong aerospace production, industrial manufacturing expansion, and power generation projects.

Ni Based Superalloys Market Segmentation Analysis:

By Type

The Ni Based Superalloys Market by type is led by Alloy 718, which accounted for 34.2% share in 2024, driven by its superior creep resistance, weldability, and high-temperature performance that make it the preferred material for turbine discs, compressor components, and aerospace fasteners. Demand is further supported by its widespread use in additive manufacturing and industrial gas turbines. Alloy 625 and Hastelloy C276/C22/X collectively gained traction in corrosion-intensive environments, while Alloy 600/601/602 and Alloy 825 remained relevant in refinery and chemical processing applications as end-user industries expanded capacity.

- For instance, Carpenter Technology and other aerospace suppliers specify Alloy 718 for turbine disks, compressor casings, and critical fasteners in modern jet engines because the alloy maintains strength and ductility at elevated temperatures while offering reliable weldability.

By Shape

In terms of shape, Sheet & Plate emerged as the dominant sub-segment with 41.7% share in 2024, owing to their extensive use in turbine casings, heat shields, combustor liners, and structural components across aerospace, power generation, and petrochemical sectors. The segment benefits from rising investments in turbine efficiency upgrades and large-format fabrication. Bars and wires together contributed a significant share due to their application in fasteners, shafts, and valve components, while other specialty forms gained adoption in precision-engineered components across niche industrial systems.

- For instance, Inconel 718 plates from Special Metals are employed in aerospace for turbine discs, blades, and combustion chambers, leveraging high-temperature strength up to 700°C and corrosion resistance.

By Application:

By application, Aerospace & Defense remained the leading sub-segment with 46.5% share in 2024, supported by increasing aircraft production, jet engine modernization, and defense fleet procurement programs that demand high-strength, oxidation-resistant alloys for turbines and exhaust systems. Growth is reinforced by stringent fuel-efficiency and emission-reduction targets that accelerate adoption of high-temperature superalloys. Power generation held a notable share driven by gas turbine expansions, while oil & gas, refinery, and chemical industries sustained demand for corrosion-resistant grades used in high-pressure processing, sour-gas handling, and critical plant infrastructure.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Expansion of Aerospace and Defense Manufacturing

The Ni Based Superalloys Market records strong growth due to accelerating aircraft production, modernization of jet engines, and rising investments in defense aviation programs. Manufacturers increasingly use high-temperature and fatigue-resistant alloys for turbine blades, combustor liners, and structural engine components to enhance durability and fuel efficiency. Stricter emission regulations and the shift toward lightweight propulsion platforms further strengthen demand. Replacement of aging fleets, higher MRO activity, and development of next-generation propulsion technologies continue to increase the consumption of Alloy 718 and related grades across global aerospace supply chains, reinforcing long-term market expansion.

- For instance, GE Aircraft Engines employs Alloy 718 extensively in critical rotating parts, airfoils, turbine disks, and supporting structures across its jet engines. Investment-cast Alloy 718 enables complex structures like the GE90 turbine rear frame, leveraging its weldability for cost-effective fabrication.

Increasing Adoption in Power Generation and Industrial Gas Turbines

Growing deployment of high-efficiency gas turbines significantly boosts the use of Ni based superalloys in power generation applications. These alloys enable turbines to operate at elevated firing temperatures while maintaining structural integrity, leading to improved thermal efficiency, extended service life, and reduced maintenance requirements. The transition toward combined-cycle plants, distributed power facilities, and cogeneration projects further fuels material demand. Refurbishment of aging turbine fleets and greater investment in reliability-centered maintenance programs strengthen adoption. Superior resistance to oxidation, corrosion, and thermal cycling positions these alloys as essential materials in advanced turbine manufacturing ecosystems worldwide.

- For instance, Mitsubishi Power utilizes similar materials in its JAC series gas turbines which have logged over 100,000 operating hours in commercial use to maintain oxidation and corrosion resistance under high thermal stress conditions.

Rising Use in Oil, Gas, Refining, and Chemical Processing

The Ni Based Superalloys Market benefits from increasing deployment in oil and gas, refinery, and chemical processing facilities due to exceptional corrosion resistance and stress-rupture strength. These alloys ensure safe operation in high-pressure, sour-gas, and high-temperature environments across reactors, valves, pipelines, and heat-exchanger systems. Growth in deep-water drilling, LNG value chains, hydrogen processing, and petrochemical plant expansions accelerates demand. Asset-life extension initiatives and reliability optimization programs encourage the use of premium-grade superalloys to minimize equipment failure risks and maintenance downtime, driving sustained consumption across critical industrial infrastructure applications.

Key Trends & Opportunities

Integration of Additive Manufacturing in Superalloy Component Production

Additive manufacturing represents a major advancement in the Ni Based Superalloys Market, enabling the production of complex, lightweight components with refined geometries and reduced material waste. Technologies such as laser powder bed fusion and directed energy deposition expand the applicability of Alloy 718, Alloy 625, and other grades in turbine, aerospace, and high-performance industrial parts. This trend supports rapid prototyping, design flexibility, and decentralized production capabilities, strengthening supply-chain resilience and reducing lead times. Collaboration between alloy manufacturers, 3D-printing system developers, and OEMs creates new opportunities for performance optimization, cost-efficient fabrication, and accelerated product innovation.

- For instance, InssTek and GOD Tech applied directed energy deposition with Inconel 625 to repair a power plant turbine blade (base CMSX-4) and vane (base MAR-M247).

Shift Toward High-Efficiency and Low-Emission Energy and Propulsion Systems

The global transition toward energy-efficient and low-emission technologies generates significant opportunities for Ni based superalloys in advanced turbine and propulsion platforms. Growing adoption of hydrogen-ready turbines, ultra-high-temperature aero-engines, and next-generation industrial processing systems increases demand for alloys capable of operating under extreme heat and oxidative stress. Advances in alloy chemistry, protective coatings, and manufacturing processes further enhance performance reliability and component durability. As industries invest in sustainable energy infrastructure and cleaner propulsion systems, Ni based superalloys play a pivotal enabling role in supporting technological progress and long-term decarbonization objectives.

- For instance, Siemens Energy’s SGT-800 hydrogen-ready gas turbine, capable of operating with up to 75% hydrogen in the fuel mix, relies on advanced Ni-based superalloys to maintain structural integrity at high combustion temperatures.

Key Challenges

High Material and Manufacturing Costs

A major challenge in the Ni Based Superalloys Market is the high cost associated with alloying elements, precision processing technologies, and specialized heat treatment and forging operations. Complex compositions, dependence on strategic metals, and stringent mechanical quality standards significantly increase production and machining expenses. These cost pressures limit adoption in price-sensitive applications and emerging markets, while fluctuations in raw-material pricing add procurement uncertainty. Manufacturers must focus on recycling efficiency, near-net-shape processing, and process optimization to improve cost competitiveness and expand the commercial scalability of advanced superalloy solutions.

Supply-Chain Constraints and Raw Material Availability Risks

The market faces ongoing challenges related to supply-chain fragility, limited availability of critical alloying inputs, and reliance on geographically concentrated mining and refining regions. Geopolitical disruptions, trade restrictions, and logistics delays increase lead times and affect delivery reliability for aerospace, power, and industrial manufacturers. Certification requirements and specialized batch production further complicate capacity expansion and inventory planning. These factors can disrupt component availability and production scheduling across critical industries. Strengthening supplier diversification, strategic sourcing partnerships, and long-term material security frameworks remains essential to ensuring stable supply continuity in the Ni Based Superalloys Market.

Regional Analysis

North America

North America held a leading position in the Ni Based Superalloys Market with 32.6% share in 2024, driven by strong aerospace engine manufacturing, defense modernization initiatives, and advanced turbine production programs in the U.S. and Canada. The region benefits from a well-established supply chain, high investments in additive manufacturing, and strong R&D activities supporting alloy innovation and performance enhancement. Growth in industrial gas turbines, refinery upgrades, and maintenance, repair, and overhaul (MRO) activities further strengthens demand. Expansion in space propulsion and next-generation jet engine platforms reinforces the strategic importance of high-temperature nickel-based materials across critical industries.

Europe

Europe accounted for 27.4% share in 2024, supported by the presence of major aerospace OEMs, turbine manufacturers, and chemical processing industries across Germany, France, the UK, and Italy. The region emphasizes fuel-efficient propulsion technologies, emission-reduction targets, and materials engineering advancements, which increase adoption of high-performance nickel superalloys. Strong demand from industrial gas turbines, refinery operations, and specialty engineering applications also contributes to market expansion. Investments in hydrogen-ready energy infrastructure and sustainable aviation technology development further stimulate consumption. Collaborative industrial research programs and strong metallurgical expertise enhance Europe’s competitive position in high-value superalloy production and application ecosystems.

Asia-Pacific

Asia-Pacific emerged as the fastest-growing regional market with 28.9% share in 2024, driven by rapid expansion in aerospace manufacturing, power generation capacity, and petrochemical and refining infrastructure across China, India, Japan, and South Korea. Rising aircraft fleet procurement, localization of engine component manufacturing, and strong investments in industrial gas turbine projects significantly boost demand. The region also benefits from large-scale chemical processing and LNG development activities requiring corrosion-resistant high-temperature alloys. Government-backed industrialization programs, technology transfer partnerships, and capacity additions in specialty alloy production strengthen Asia-Pacific’s role as a key manufacturing and consumption hub.

Latin America

Latin America represented 6.1% share in 2024, supported by increasing investments in oil and gas production, refinery upgrades, and industrial energy infrastructure across Brazil, Mexico, and Argentina. Rising adoption of Ni based superalloys in high-temperature processing equipment, gas turbine systems, and offshore drilling operations drives market demand. Growth in aerospace component assembly and maintenance facilities further contributes to consumption. Ongoing petrochemical expansions, reliability-focused plant modernization initiatives, and the development of LNG and deep-water exploration projects reinforce the need for corrosion- and heat-resistant alloys, strengthening the region’s long-term participation in the global superalloy value chain.

Middle East & Africa

The Middle East & Africa accounted for 5.0% share in 2024, driven by strong demand from oil and gas processing, petrochemical plants, and power generation projects across Saudi Arabia, the UAE, Qatar, and South Africa. High operating temperatures, sour-gas environments, and harsh processing conditions accelerate the use of Ni based superalloys in turbines, reactors, valves, and pipeline systems. Ongoing refinery expansions, gas-to-chemicals investments, and industrial diversification programs support market growth. Increasing adoption of advanced turbine technologies and reliability enhancement initiatives in critical energy infrastructure further strengthen the region’s demand for premium-grade, high-performance superalloy materials.

Ni Based Superalloys Market Segmentations:

By Type

- Alloy 600/601/602

- Alloy 625

- Alloy 718

- Alloy 825

- Hastelloy C276/C22/X

- Others

By Shape

- Bar

- Wire

- Sheet & plate

- Others

By Application

- Aerospace & defense

- Power generation

- Oil & gas

- Refinery

- Chemical

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Ni Based Superalloys Market is characterized by the presence of leading players such as General Electric Company, Pratt & Whitney, Rolls-Royce plc, Safran, ATI, Haynes International, Aubert & Duval, and United Technologies Corporation. These companies focus on advanced alloy development, precision manufacturing technologies, and long-term supply partnerships with aerospace, power generation, and industrial OEMs. The market remains highly innovation-driven, with strategic investments in additive manufacturing, high-temperature performance optimization, and corrosion-resistant alloy formulations to support next-generation turbine and propulsion platforms. Players strengthen competitiveness through vertical integration, capacity expansions, and collaborations with research institutions for metallurgical enhancement. In addition, suppliers emphasize quality certification, reliability assurance, and lifecycle service support to meet stringent industry performance standards. Growing application diversification across refinery, chemical processing, and energy infrastructure further encourages product portfolio expansion and customer-centric material engineering strategies across global markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Pratt & Whitney (U.S.)

- Aubert & Duval (France)

- Boeing (U.S.)

- Safran (France)

- ATI (U.S.)

- Rolls-Royce plc (UK)

- Global Atomic Corp. (U.S.)

- Haynes International (U.S.)

- United Technologies Corporation (U.S.)

- General Electric Company (U.S.)

Recent Developments

- In April 2025, QuesTek Innovations LLC developed and introduced a novel nickel-based superalloy for additive manufacturing tailored for extreme aerospace environments in collaboration with Stoke Space.

- In February 2025, MIDHANI launched three novel aerospace materials, including high-temperature nickel alloy billets, Alloy S152 forged bars, and Superni 41 plates, essential for jet engines, aircraft, and space technologies.

- In August 2025, EverMetal Holdings completed the acquisition of CAI Custom Alloys LLC, enhancing nickel-based superalloy scrap processing capacity and strengthening supply chain capabilities.

Report Coverage

The research report offers an in-depth analysis based on Type, Shape, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will witness sustained demand growth as aerospace engine production and fleet modernization initiatives continue worldwide.

- Manufacturers will increasingly adopt advanced alloy chemistries to enhance high-temperature strength, corrosion resistance, and fatigue performance.

- Additive manufacturing will play a larger role in producing complex superalloy components with improved efficiency and reduced material waste.

- Power generation applications will expand as high-efficiency gas turbines and hydrogen-ready systems gain wider deployment.

- Oil, gas, and petrochemical industries will increase the use of premium superalloys for reliability-critical, high-pressure operating environments.

- Material recycling, scrap recovery, and circular-economy practices will strengthen to address cost pressures and supply sustainability.

- Supply-chain partnerships between alloy producers, OEMs, and research institutions will intensify to accelerate innovation and qualification cycles.

- Emerging economies will expand local manufacturing capacity and specialty metallurgy capabilities to reduce import dependence.

- Regulatory focus on energy efficiency and emission reduction will reinforce investments in advanced turbine and propulsion technologies.

- Continuous R&D in coatings, processing techniques, and microstructure control will drive performance upgrades and long-term competitiveness in the market.