Market Overview

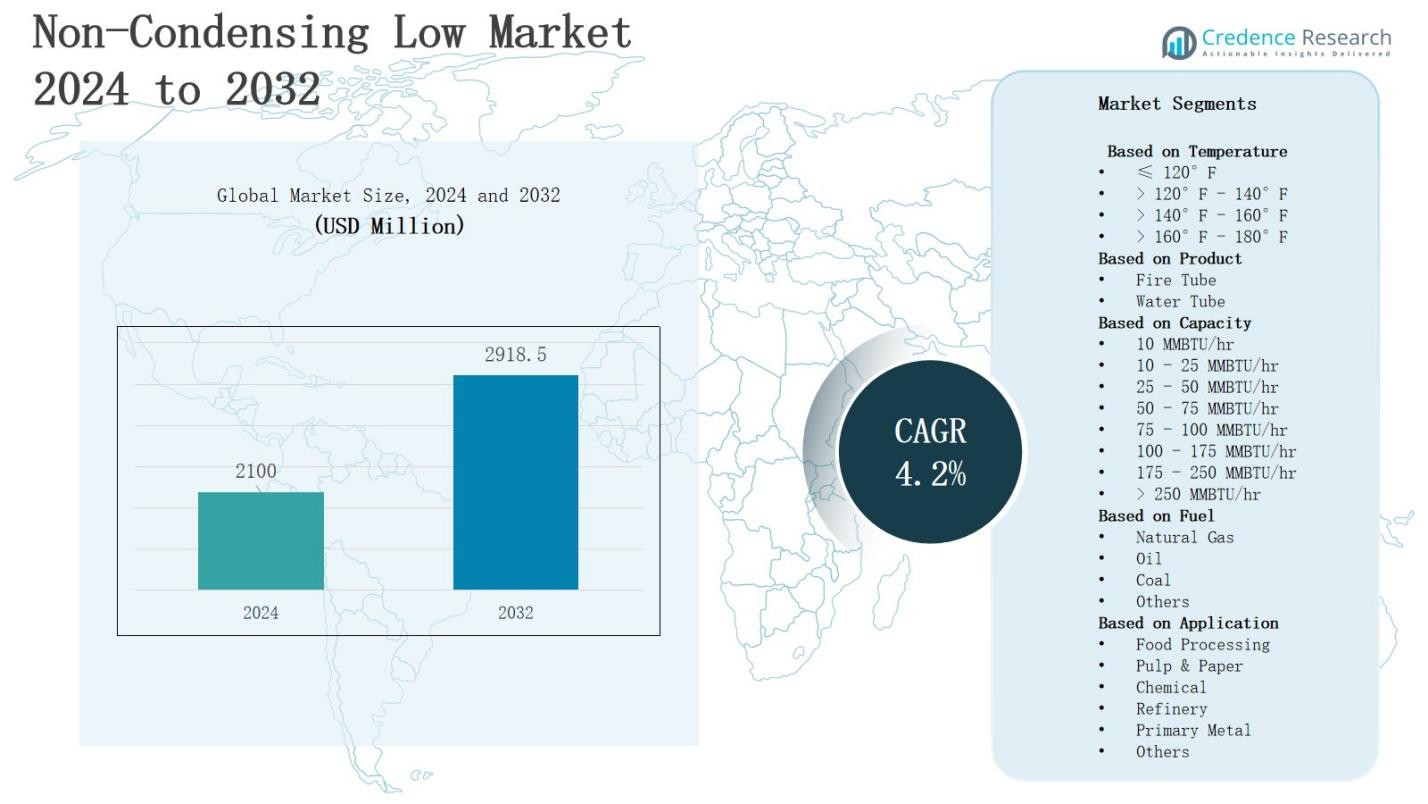

The Non-Condensing Low Temperature Industrial Boiler market is projected to grow from USD 2100 million in 2024 to USD 2918.5 million by 2032, registering a CAGR of 4.2% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Non-Condensing Low Temperature Industrial Boiler Market Size 2024 |

USD 2100 Million |

| Non-Condensing Low Temperature Industrial Boiler Market, CAGR |

4.2% |

| Non-Condensing Low Temperature Industrial Boiler Market Size 2032 |

USD 2918.5 Million |

The non-condensing low temperature industrial boiler market is driven by rising demand for cost-effective heating solutions, strict energy efficiency standards, and growing adoption in industrial facilities requiring reliable low-temperature operations. Increasing industrialization across emerging economies and the need for durable, low-maintenance systems further accelerate market growth. Trends include technological advancements aimed at improving efficiency, integration with smart monitoring systems, and the shift toward eco-friendly fuel options to meet sustainability goals. Expanding applications in food processing, chemicals, and manufacturing industries continue to shape market development, while modernization of aging infrastructure presents significant opportunities for long-term adoption.

The non condensing low temperature industrial boiler market shows diverse geographical dynamics, with Asia-Pacific holding the largest share, followed by North America and Europe, while Latin America and the Middle East & Africa present steady growth opportunities. It benefits from industrial expansion in emerging economies and modernization in developed markets. Key players shaping the competitive landscape include Babcock Wanson, Bosch Industriekessel, Cleaver-Brooks, Cochran, Ferroli, Fulton, Hurst Boiler & Welding, IHI, Maxima Boilers, Miura America, Parker Boiler, and Precision Boilers, all focusing on efficiency and compliance-driven solutions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The non condensing low temperature industrial boiler market will grow from USD 2100 million in 2024 to USD 2918.5 million by 2032, registering a CAGR of 4.2%.

- The >160°F – 180°F temperature segment leads with 35% share, driven by stable heating demand in chemicals, textiles, and food processing industries requiring medium-to-high heat operations.

- Fire tube boilers dominate with 60% share due to cost-effectiveness, easy maintenance, and suitability for small to medium-sized enterprises, while water tube boilers remain limited to higher-capacity industrial use.

- The 10 – 25 MMBTU/hr capacity range holds 28% share, supported by adoption in food, textile, and pharmaceutical industries seeking affordable, efficient heating with balanced operational costs.

- Asia-Pacific leads with 30% share, followed by North America at 32% and Europe at 27%, while Latin America and the Middle East & Africa account for 6% and 5% respectively.

Market Drivers

Rising Demand for Cost-Effective Heating Solutions

The non condensing low temperature industrial boiler market benefits from rising adoption due to cost-effectiveness and reliability in industrial heating applications. Industries seek durable systems that minimize operational expenses while providing consistent performance in low-temperature processes. Its appeal lies in simple design, lower installation costs, and reduced maintenance needs compared to advanced condensing units. Manufacturing facilities, food processing plants, and textile industries increasingly prefer such systems for stable output, further supporting steady demand across global industrial applications.

- For instance, Viessmann’s Vitomax LW boilers offer high efficiency with over 95.5% thermal efficiency and can operate on up to 100% hydrogen, reducing emissions and cutting operational expenses in chemical and food processing industries.

Stringent Energy Efficiency and Emission Regulations

Regulatory pressure is a major driver in the non condensing low temperature industrial boiler market, with governments enforcing stricter efficiency and emission standards. It encourages industries to replace outdated systems with modern low-temperature models capable of meeting compliance requirements. These boilers consume less fuel while maintaining consistent heating output, aligning with energy conservation goals. Environmental concerns regarding industrial emissions also accelerate adoption, as companies prioritize solutions that balance performance with regulatory demands across diverse sectors.

- For instance, Bosch Industriekessel GmbH reported that its UL-S boiler systems with integrated economizers reduce fuel consumption by up to 7%, directly addressing Germany’s tightened energy efficiency regulations under the Energy Efficiency Act of 2024.

Growing Industrialization and Infrastructure Expansion

Rapid industrial growth in emerging economies significantly fuels the non condensing low temperature industrial boiler market. Expanding infrastructure in manufacturing, chemicals, and processing industries creates strong demand for affordable and efficient heating systems. It addresses the operational needs of medium-scale facilities requiring reliable heat supply without high investment costs. Infrastructure modernization projects also highlight opportunities for replacement and retrofitting, allowing industries to adopt boilers that combine traditional reliability with improved efficiency and compliance features.

Technological Integration and Modernization Opportunities

The non condensing low temperature industrial boiler market benefits from steady technological integration aimed at enhancing durability and efficiency. Manufacturers are incorporating smart monitoring, control systems, and improved material designs to optimize performance and extend lifecycle. It provides users with real-time operational data, reducing downtime and enhancing productivity. Aging boiler infrastructure across developed regions also creates replacement opportunities. Industries are increasingly investing in modern low-temperature systems that meet both operational and regulatory expectations effectively.

Market Trends

Adoption of Smart Monitoring and Control Systems

The non condensing low temperature industrial boiler market is witnessing a strong trend toward integration of smart monitoring technologies. Digital sensors and automated controls allow operators to track efficiency, temperature, and emissions in real time. It reduces operational risks, improves safety, and enhances predictive maintenance strategies. Industries are investing in intelligent systems to minimize downtime and extend equipment life. This trend aligns with broader industrial digitalization, offering end users cost savings and higher productivity.

- For instance, Cleaver-Brooks, a leading U.S. boiler manufacturer, introduced Prometha, an IoT-based platform that provides real-time analytics and alerts via web and mobile apps, helping operators optimize boiler efficiency and prevent downtime.

Shift Toward Eco-Friendly Fuel Alternatives

Sustainability initiatives are reshaping the non condensing low temperature industrial boiler market as industries explore eco-friendly fuel options. Companies are adopting boilers designed for biofuels, natural gas, and hybrid systems to reduce environmental impact. It aligns with global efforts to curb carbon emissions and comply with stricter policies. Growing preference for clean energy alternatives drives demand across sectors such as food processing, chemicals, and textiles. This transition enhances energy efficiency and supports long-term market resilience.

- For instance, Miura’s modular water tube boilers are recognized for their fuel efficiency and lower emissions, providing rapid steam production while cutting down NOx and CO2 emissions.

Replacement of Aging Boiler Infrastructure

Modernization is a prominent trend in the non condensing low temperature industrial boiler market, with many industries replacing aging systems. Older units often fail to meet current efficiency and emission standards, leading to higher operational costs. It encourages investment in newer models that deliver better fuel efficiency and compliance with regulations. Replacement demand is particularly strong in developed regions with established industrial bases. This trend supports steady growth while ensuring reliability and operational continuity.

Increasing Applications Across Diverse Industrial Sectors

The non condensing low temperature industrial boiler market is expanding due to growing applications across varied industries. Manufacturing, pharmaceuticals, food processing, and chemicals are adopting these systems for reliable low-temperature operations. It provides consistent heating essential for processes requiring controlled thermal conditions. Rising industrialization in Asia-Pacific and Latin America fuels adoption in small to medium-scale facilities. This trend highlights the market’s versatility and adaptability, reinforcing its importance in industrial development and operational sustainability.

Market Challenges Analysis

Regulatory Pressure and Rising Efficiency Standards

The non condensing low temperature industrial boiler market faces significant challenges from tightening environmental regulations and energy efficiency standards. Governments worldwide are pushing industries to adopt sustainable technologies, often favoring condensing units with higher efficiency. It places pressure on manufacturers to redesign products or risk losing competitiveness. Non-condensing boilers, while cost-effective, often struggle to meet evolving efficiency benchmarks. This situation limits their acceptance in advanced markets and forces companies to invest heavily in research and development.

High Competition from Advanced Boiler Technologies

The non condensing low temperature industrial boiler market is challenged by growing competition from advanced alternatives such as condensing and hybrid boilers. These systems offer better energy savings, longer life cycles, and improved compliance with environmental policies. It creates difficulties for non-condensing models to sustain demand, particularly in regions prioritizing green technology adoption. End users are increasingly evaluating long-term operational costs, which often favor advanced solutions. This challenge limits the market’s growth potential and requires strategic positioning.

Market Opportunities

Expansion in Emerging Industrial Economies

The non condensing low temperature industrial boiler market holds strong opportunities in rapidly industrializing regions such as Asia-Pacific, Latin America, and the Middle East. Rising investments in manufacturing, food processing, textiles, and chemical industries are driving demand for affordable and reliable heating systems. It provides a cost-effective solution for small and medium enterprises seeking efficiency without high capital expenditure. Infrastructure growth, supported by government initiatives, creates a favorable environment for adoption. Expanding energy access in rural and semi-urban areas further strengthens the opportunity.

Modernization and Retrofit Demand Across Developed Regions

The non condensing low temperature industrial boiler market also benefits from modernization opportunities in mature economies with aging infrastructure. Industries in North America and Europe are increasingly investing in retrofitting existing systems to meet compliance requirements while maintaining operational continuity. It allows companies to upgrade with advanced materials, monitoring tools, and efficient designs without full replacement costs. Rising focus on lifecycle extension and maintenance efficiency encourages upgrades. This trend supports growth while enabling industries to balance performance with regulatory expectations.

Market Segmentation Analysis:

By Temperature

In the non condensing low temperature industrial boiler market, the >160°F – 180°F segment dominates with over 35% share. This range supports critical applications in industries such as chemicals, food processing, and textiles that require stable medium-to-high heat for production processes. Its popularity stems from balanced efficiency, operational reliability, and wide suitability across diverse facilities. Demand is further supported by replacement of outdated units and regulatory compliance needs, making this segment the leading contributor to market revenues.

- For instance, Miura America has deployed multiple units in textile facilities in the U.S., where stable 170°F hot water is required for fabric dyeing and finishing, ensuring process reliability and quality.

By Product

The fire tube segment leads the non condensing low temperature industrial boiler market with nearly 60% share. Fire tube boilers are cost-effective, easier to maintain, and widely adopted by small and medium-sized enterprises requiring steady output. Their simple design and durability make them preferable for facilities seeking lower installation and operational costs. Water tube models, though efficient at higher capacities, account for a smaller share due to higher upfront investment and maintenance needs.

- For instance, Cleaver-Brooks’ CBEX Firetube model features high efficiency and simplified cleaning access, making it a popular choice in institutional settings like hospitals that run on consistent heating demand.

By Capacity

The 10 – 25 MMBTU/hr capacity range holds the largest share at around 28% of the non condensing low temperature industrial boiler market. This category is well-suited for mid-sized industries such as food, textiles, and pharmaceuticals that demand consistent heating without large-scale fuel consumption. It provides a balance between efficiency and affordability, supporting strong adoption. Higher-capacity ranges above 100 MMBTU/hr serve heavy industries but remain limited in share due to fewer installations, while smaller units under 10 MMBTU/hr cater mainly to niche applications.

Segments:

Based on Temperature

- ≤ 120°F

- > 120°F – 140°F

- > 140°F – 160°F

- > 160°F – 180°F

Based on Product

Based on Capacity

- 10 MMBTU/hr

- 10 – 25 MMBTU/hr

- 25 – 50 MMBTU/hr

- 50 – 75 MMBTU/hr

- 75 – 100 MMBTU/hr

- 100 – 175 MMBTU/hr

- 175 – 250 MMBTU/hr

- > 250 MMBTU/hr

Based on Fuel

- Natural Gas

- Oil

- Coal

- Others

Based on Application

- Food Processing

- Pulp & Paper

- Chemical

- Refinery

- Primary Metal

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America accounts for 32% share of the non condensing low temperature industrial boiler market, driven by strong demand from food processing, chemicals, and manufacturing industries. The region benefits from advanced industrial infrastructure and the replacement of outdated systems with modern low-temperature boilers. It also faces regulatory pressure, encouraging the adoption of efficient and compliant equipment. The United States leads regional demand due to its large-scale industrial base. Canada follows, supported by investments in energy-efficient industrial systems and modernization projects.

Europe

Europe holds 27% share of the non condensing low temperature industrial boiler market, supported by strong manufacturing sectors and strict energy regulations. Countries such as Germany, France, and the UK are leading adopters due to mature industrial bases and infrastructure modernization. It benefits from industries prioritizing cost-effective and reliable solutions while managing compliance with environmental standards. The focus on reducing emissions while maintaining operational efficiency sustains steady demand. Retrofitting opportunities further strengthen the region’s market position.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing region with 30% share of the non condensing low temperature industrial boiler market. Rapid industrialization in China, India, and Southeast Asia fuels growth, supported by expanding food processing, textile, and chemical industries. It benefits from infrastructure development, rising energy access, and cost-sensitive demand for efficient systems. Local manufacturers play a vital role in meeting domestic needs, offering competitive pricing. Growing government support for industrial expansion continues to make Asia-Pacific a key driver of global market revenues.

Latin America

Latin America contributes 6% share of the non condensing low temperature industrial boiler market, led by Brazil and Mexico. Growth is supported by the expansion of food and beverage, textiles, and manufacturing industries. It appeals to medium-sized enterprises looking for cost-effective boilers with reliable performance. Economic growth and rising industrial investments foster gradual adoption. The region’s increasing integration into global trade also boosts demand for modernized systems. Replacement opportunities remain steady, particularly in established industrial hubs.

Middle East & Africa

The Middle East & Africa hold 5% share of the non condensing low temperature industrial boiler market, with demand concentrated in GCC nations and South Africa. Rising investments in chemicals, food processing, and energy-intensive sectors support adoption. It is also influenced by infrastructure expansion and government-backed industrialization programs. Industries in the region prefer durable and affordable systems that suit medium-scale applications. Growing diversification initiatives in oil-dependent economies strengthen demand, particularly across emerging non-oil industrial projects.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Parker Boiler

- Fulton

- IHI

- Cleaver-Brooks

- Maxima Boilers

- Babcock Wanson

- Precision Boilers

- Hurst Boiler & Welding

- Bosch Industriekessel

- Miura America

- Ferroli

- Cochran

Competitive Analysis

The non condensing low temperature industrial boiler market is characterized by intense competition among global and regional players focusing on cost-effective solutions, product reliability, and regulatory compliance. Key companies such as Babcock Wanson, Bosch Industriekessel, Cleaver-Brooks, Cochran, Ferroli, Fulton, Hurst Boiler & Welding, IHI, Maxima Boilers, Miura America, Parker Boiler, and Precision Boilers compete by expanding product portfolios, enhancing efficiency, and offering aftersales support. It benefits from companies investing in modernization, smart monitoring systems, and environmentally sustainable technologies to meet shifting customer expectations. Market players prioritize strategic partnerships, distribution expansion, and capacity optimization to strengthen their position across established and emerging regions. Continuous innovation, combined with a focus on durability and operational simplicity, drives competitive advantage, while replacement demand in developed markets and rapid industrialization in Asia-Pacific further intensify rivalry.

Recent Developments

- In May 2024, Lochinvar, a leading boiler manufacturer, launched the LECTRUS Light Commercial Electric Boiler, supporting electrification and decarbonization trends in the boiler industry.

- In May 2025, Burnham Holdings divested Thermo Pride and Norwood Manufacturing to R.W. Beckett Corporation, strengthening Beckett’s portfolio in the heating solutions market.

- In 2025, Cleaver-Brooks introduced its LVR electric hydronic boiler, designed to deliver zero onsite emissions and improved energy efficiency for industrial and commercial applications.

- In September 2024, Babcock Wanson introduced its LV-Pack industrial electric vertical boiler, a low-voltage unit capable of supplying steam at pressures up to 18 barg, delivering over 99% energy efficiency while eliminating CO2 and NOx emissions to comply with European energy optimization standards.

Report Coverage

The research report offers an in-depth analysis based on Temperature, Product, Capacity, , Fuel, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will rise in emerging economies due to expanding industrialization and infrastructure modernization projects.

- Replacement of outdated boiler systems will create strong opportunities in North America and Europe.

- Integration of smart monitoring systems will enhance efficiency, safety, and predictive maintenance capabilities.

- Adoption of eco-friendly fuel alternatives will support sustainability goals and regulatory compliance requirements globally.

- Food processing and chemical industries will remain key end users driving consistent long-term market demand.

- Fire tube boilers will maintain dominance due to cost-effectiveness and ease of operation.

- Mid-range capacity boilers will see strong adoption from medium enterprises needing affordable and reliable heating.

- Local manufacturing expansion in Asia-Pacific will strengthen supply chains and improve competitive market positioning.

- Technological improvements in material durability will extend lifecycle and reduce operational downtime in industries.

- Strategic partnerships and acquisitions among key players will boost innovation and expand global distribution networks.