Market Overview:

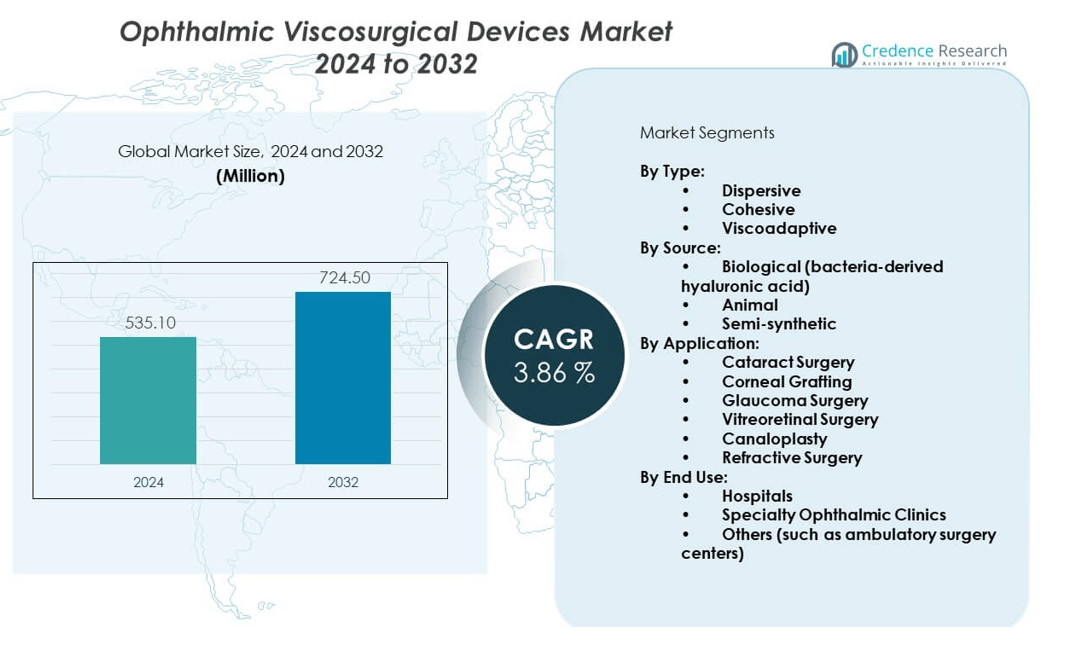

The ophthalmic viscosurgical devices market is projected to grow from USD 535.1 million in 2024 to USD 724.5 million by 2032, registering a CAGR of 3.86% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ophthalmic Viscosurgical Devices Market Size 2024 |

USD 535.1 million |

| Ophthalmic Viscosurgical Devices Market, CAGR |

3.86% |

| Ophthalmic Viscosurgical Devices Market Size 2032 |

USD 724.5 million |

Growth in the ophthalmic viscosurgical devices market is primarily driven by the rising prevalence of cataracts, glaucoma, and other age-related eye disorders. Increasing adoption of premium intraocular lenses, coupled with a higher volume of cataract surgeries, supports demand for these devices. Aging populations, improved access to eye care, and growing awareness about vision health further encourage adoption. Technological innovations in viscoelastic formulations, alongside increasing surgical success rates, continue to strengthen physician and patient confidence, boosting market growth.

Regionally, North America dominates the ophthalmic viscosurgical devices market due to advanced healthcare infrastructure, high cataract surgery volumes, and rapid adoption of innovative surgical solutions. Europe follows closely, supported by strong ophthalmic research and increasing government initiatives in eye health. The Asia-Pacific region is emerging as the fastest-growing market, driven by a large aging population, rising healthcare investments, and growing surgical capacity in countries such as India and China. Meanwhile, Latin America and the Middle East & Africa show steady growth, fueled by improving access to ophthalmic care and expanding healthcare infrastructure.

Market Insights:

- The ophthalmic viscosurgical devices market was valued at USD 535.1 million in 2024 and is projected to reach USD 724.5 million by 2032, expanding at a CAGR of 86% during the forecast period.

- Rising prevalence of cataracts, glaucoma, and other vision-related disorders continues to drive strong demand for these devices.

- Increasing adoption of minimally invasive ophthalmic surgeries supports higher utilization of advanced viscoelastic formulations.

- High product costs and reimbursement limitations in certain regions act as key restraints for market growth.

- Regulatory challenges and strict approval requirements for new devices add to the market barriers.

- North America leads the market due to advanced healthcare infrastructure and high surgical volumes.

- Asia-Pacific is emerging as the fastest-growing region, fueled by a large aging population, expanding healthcare access, and government-led cataract treatment programs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Burden of Age-Related Eye Disorders Fueling the Demand for Advanced Surgical Solutions:

The ophthalmic viscosurgical devices market is expanding due to the increasing prevalence of cataracts, glaucoma, and other age-related eye conditions. Cataracts remain one of the leading causes of blindness, creating high surgical demand worldwide. An aging global population significantly contributes to this growing patient pool, driving adoption of surgical interventions. Surgeons rely on these devices to maintain anterior chamber stability and protect delicate tissues during procedures. Rising healthcare awareness and patient preference for vision-restoring treatments support market growth. Government initiatives promoting early diagnosis and affordable surgical access further strengthen adoption. The increasing emphasis on reducing blindness rates positions ophthalmic viscosurgical devices as essential tools. It is benefiting from continuous demand in both developed and emerging healthcare markets.

- For instance, Alcon’s ARGOS Biometer and SMARTCataract DX digital planning solutions have optimized workflow efficiencies for cataract surgeries, improving precision and patient outcomes particularly in aging populations.

Technological Advancements in Ophthalmic Surgery Supporting Market Expansion:

Advances in ophthalmic surgical techniques and technologies are a key driver of the ophthalmic viscosurgical devices market. Modern formulations now provide improved viscoelastic properties, enhancing surgical precision and safety. Surgeons benefit from products that offer greater transparency, better retention, and smoother tissue manipulation. The integration of minimally invasive techniques also boosts reliance on these devices during complex eye procedures. Rising investments in research and development encourage product innovations that meet diverse clinical needs. Surgeons increasingly prefer advanced solutions that reduce post-operative complications and accelerate recovery times. The demand for premium intraocular lens implants creates further dependence on these devices. It continues to expand as manufacturers deliver products that meet evolving clinical expectations.

- For example, Alcon’s DisCoVisc OVD offers a unique viscodispersive formulation that provides full space maintenance during intraocular lens insertion, vastly improving procedural handling and endothelial protection.

Growing Surgical Volumes Due to Expanding Access to Ophthalmic Care:

The ophthalmic viscosurgical devices market benefits from increasing global surgical volumes, driven by expanding access to eye care facilities. Cataract surgeries are the most frequently performed ophthalmic procedures, accounting for millions of cases annually. Expanding healthcare infrastructure in emerging economies supports greater access to surgical interventions. Government healthcare schemes offering free or subsidized eye surgeries create strong demand. Rising awareness of treatable blindness encourages more patients to seek timely interventions. The availability of skilled ophthalmic surgeons in developing regions further drives growth. Partnerships between governments and non-governmental organizations enhance surgical outreach programs globally. It continues to grow as the number of procedures rises across both urban and rural settings.

Rising Patient Preference for Minimally Invasive Ophthalmic Procedures:

The ophthalmic viscosurgical devices market is propelled by patient preference for minimally invasive surgical approaches. Patients increasingly demand safer, quicker, and less painful procedures with shorter recovery times. Ophthalmic viscosurgical devices enable surgeons to meet these expectations by reducing intraoperative risks. The shift towards advanced phacoemulsification and femtosecond laser-assisted surgeries boosts product usage. Higher success rates in complex surgical cases strengthen surgeon confidence in these devices. Patients also benefit from better post-operative vision outcomes, encouraging adoption. Demand for high-quality surgical care continues to rise in both developed and emerging regions. It remains essential as healthcare systems embrace efficiency-driven surgical techniques.

Market Trends:

Increasing Use of Combination Surgical Techniques Enhancing Device Utility:

The ophthalmic viscosurgical devices market is witnessing growing adoption of combination surgical techniques. Surgeons are increasingly combining cataract and glaucoma procedures to reduce patient burden. These multi-procedure approaches expand the role of viscoelastic devices in complex surgeries. The versatility of products enables surgeons to perform intricate steps with improved safety. This trend reflects a broader push toward patient-centered surgical care. Demand for advanced formulations that can serve multiple surgical requirements is rising. Healthcare providers favor integrated approaches that reduce costs and improve recovery outcomes. It continues to evolve as surgeons adopt multi-functional applications for enhanced surgical efficiency.

- For instance, Alcon’s DuoVisc combines cohesive and dispersive properties into a single device, facilitating safer and more efficient multi-step surgeries by optimizing both tissue protection and chamber maintenance.

Rising Adoption of Premium Ophthalmic Devices in Advanced Healthcare Systems:

The ophthalmic viscosurgical devices market is experiencing growth in premium product adoption within developed economies. Surgeons in regions like North America and Europe prefer advanced formulations with superior performance. Premium devices offer longer retention, lower inflammatory response, and better surgical outcomes. Patients in these regions also show higher willingness to opt for premium procedures. Insurance coverage and supportive reimbursement structures encourage greater adoption of advanced products. The trend highlights a growing divide between high-end and cost-sensitive markets. Healthcare systems increasingly prioritize innovation and patient outcomes over cost considerations. It expands as premium solutions gain traction among technologically advanced ophthalmic practices.

- For instance, Alcon’s premium products such as the NGENUITY 1.5 3D Visualization System have enhanced surgical precision and visualization, gaining significant preference in high-end ophthalmic centers.

Integration of Digital Platforms and AI in Ophthalmic Surgery Enhancing Precision:

The ophthalmic viscosurgical devices market is influenced by the integration of digital tools in ophthalmology. Surgeons increasingly utilize AI-based platforms to plan and monitor surgical steps. Real-time imaging technologies guide viscoelastic injection and chamber stability maintenance. These technologies reduce risks and enhance accuracy during delicate procedures. Companies are investing in smart surgical ecosystems that combine devices with AI-driven insights. Patients benefit from improved safety and reduced surgical variability. Digital transformation in ophthalmic care continues to accelerate, creating new opportunities for device adoption. It adapts to the changing landscape where technology and precision-based care dominate surgical practice.

Sustainable Manufacturing Practices Gaining Momentum in Ophthalmic Device Production:

The ophthalmic viscosurgical devices market is aligning with sustainability-focused manufacturing. Companies are adopting eco-friendly processes and minimizing resource-intensive production methods. Regulatory pressures on medical device sustainability encourage greener innovation. Manufacturers explore biodegradable packaging and reduced carbon footprints for ophthalmic products. Hospitals and clinics increasingly consider sustainability in procurement decisions. The shift reflects broader environmental responsibility across healthcare industries. Patient awareness of sustainability initiatives also influences purchasing preferences. It is steadily transitioning toward more environmentally conscious production and distribution models.

Market Challenges Analysis:

Regulatory and Pricing Pressures Creating Constraints for Market Expansion:

The ophthalmic viscosurgical devices market faces strong challenges from regulatory and pricing pressures. Medical device regulations are becoming stricter across leading healthcare economies, increasing approval timelines. Compliance with global quality standards raises operational costs for manufacturers. Pricing pressures from governments and insurance providers limit profit margins. In emerging markets, affordability remains a major barrier for patients seeking premium devices. Competitive pricing among manufacturers intensifies cost-related challenges. Reimbursement gaps in several countries reduce adoption of advanced formulations. The imbalance between innovation investment and cost control creates tension in the market. It continues to confront obstacles from strict regulatory oversight and pricing limitations.

Supply Chain Disruptions and Unequal Global Access Restricting Market Growth:

The ophthalmic viscosurgical devices market also struggles with supply chain vulnerabilities and uneven distribution. Global disruptions affect the steady availability of raw materials and finished products. Smaller manufacturers face difficulty maintaining consistent supply levels. Healthcare facilities in rural and low-income regions experience limited access to advanced devices. The uneven distribution of ophthalmic specialists worsens this disparity. Manufacturers find it challenging to balance supply between developed and emerging regions. Pandemic-related impacts further highlighted fragility within global supply chains. It continues to face setbacks where unequal access and disruptions hinder consistent global growth.

Market Opportunities:

Expanding Role of Ophthalmic Surgery in Emerging Economies Creating Strong Growth Potential:

The ophthalmic viscosurgical devices market holds strong opportunities in emerging economies with growing healthcare investments. Countries like India, China, and Brazil are expanding surgical infrastructure at a rapid pace. Government health programs are supporting large-scale cataract surgery initiatives. Rising middle-class populations are increasingly willing to spend on vision-restoring treatments. Local manufacturing initiatives provide cost-effective solutions for price-sensitive markets. International collaborations are bringing advanced products to new regions. It is well-positioned to benefit from improving accessibility and affordability in emerging healthcare systems.

Innovation in Product Design and Customization Enhancing Market Reach:

The ophthalmic viscosurgical devices market is set to gain from innovation in customized formulations. Manufacturers are developing products that cater to specific surgical preferences and patient needs. Customized viscoelastic properties enhance outcomes in complex or high-risk cases. Innovation in delivery systems ensures precise application and reduced surgical variability. Surgeons show greater interest in devices that combine safety, efficiency, and versatility. Opportunities lie in developing patient-specific solutions that align with advanced surgical techniques. It is expected to expand further as innovation drives greater market penetration.

Market Segmentation Analysis:

By Type

The ophthalmic viscosurgical devices market is segmented into dispersive, cohesive, and viscoadaptive products. Dispersive devices dominate due to their superior ability to coat and protect delicate ocular tissues during surgery. Cohesive variants are preferred for easy removal and effective chamber maintenance, while viscoadaptive devices are gaining traction for offering both dispersive and cohesive properties in one formulation. It continues to benefit from innovation in formulations that improve surgical outcomes and enhance surgeon preference.

- For example, Alcon’s DisCoVisc® OVD uniquely combines cohesive and dispersive properties within a single syringe, offering endothelial protection and space maintenance advantages during surgery.

By Source

The ophthalmic viscosurgical devices market is categorized into biological, animal-derived, and semi-synthetic products. Biological products, particularly those derived from bacteria-based hyaluronic acid, hold a leading share owing to high safety profiles and reduced risk of contamination. Animal-derived solutions maintain relevance but face growing scrutiny due to biocompatibility concerns and ethical issues. Semi-synthetic formulations are expected to expand with their consistent quality and scalable production. It is witnessing strong movement toward biocompatible and sustainable raw material sources.

- For instance, Alcon’s use of biologically sourced sodium hyaluronate derived from bacterial fermentation aligns with their commitment to high purity and safety standards in OVD production.

By Application

The ophthalmic viscosurgical devices market covers cataract surgery, corneal grafting, glaucoma surgery, vitreoretinal surgery, canaloplasty, and refractive surgery. Cataract surgery represents the dominant segment, driven by its high global surgical volumes and reliance on viscoelastic devices for chamber stability. Glaucoma and vitreoretinal surgeries are expanding applications, supported by increasing disease prevalence. Corneal grafting and refractive surgeries also create specialized demand for tailored viscoelastic solutions. It remains central to modern ophthalmic procedures that require precision and safety.

By End Use

The ophthalmic viscosurgical devices market is divided into hospitals, specialty ophthalmic clinics, and others including ambulatory surgery centers. Hospitals lead due to advanced infrastructure, availability of skilled surgeons, and high surgical throughput. Specialty clinics contribute significantly by offering personalized care and advanced ophthalmic treatments. Ambulatory surgery centers are growing rapidly due to patient demand for efficient and cost-effective procedures. It continues to expand across all settings as access to ophthalmic surgery broadens globally.

Segmentation:

By Type:

- Dispersive

- Cohesive

- Viscoadaptive

By Source:

- Biological (bacteria-derived hyaluronic acid)

- Animal

- Semi-synthetic

By Application:

- Cataract Surgery

- Corneal Grafting

- Glaucoma Surgery

- Vitreoretinal Surgery

- Canaloplasty

- Refractive Surgery

By End Use:

- Hospitals

- Specialty Ophthalmic Clinics

- Others (such as ambulatory surgery centers)

By Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

North America holds the largest share of the ophthalmic viscosurgical devices market, accounting for over 35% of global revenue. The region benefits from advanced healthcare infrastructure, high surgical volumes, and strong adoption of innovative ophthalmic solutions. Cataract surgeries are widely performed across the United States and Canada, with favorable reimbursement frameworks supporting patient access. The presence of leading manufacturers and research-driven innovation further strengthens the region’s leadership. Rising awareness of eye health and growing demand for premium intraocular procedures drive consistent adoption. It continues to maintain dominance through established surgical practices and continuous technological advancements.

Europe

Europe represents the second-largest market, contributing around 30% of the ophthalmic viscosurgical devices market. The region is characterized by widespread access to ophthalmic care and a growing elderly population that requires surgical interventions. Government-backed programs for cataract treatment and supportive reimbursement policies strengthen device adoption. Countries such as Germany, France, and the United Kingdom lead in surgical volumes, supported by strong clinical infrastructure. The emphasis on innovation and precision-driven ophthalmic solutions further drives market penetration. It remains well-positioned in Europe due to the availability of skilled professionals and growing focus on quality eye care.

Asia-Pacific

Asia-Pacific is the fastest-growing region, holding nearly 25% of the ophthalmic viscosurgical devices market. Rapid population aging in China, India, and Japan drives strong demand for cataract and glaucoma surgeries. Expanding healthcare access, government-led blindness prevention programs, and improving affordability encourage widespread adoption. Local manufacturing initiatives provide cost-effective solutions that appeal to price-sensitive markets. The growing middle-class population and rising awareness of advanced treatments create additional growth opportunities. It is expected to increase its global share significantly as surgical capacity expands across the region.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Player Analysis:

Competitive Analysis:

The ophthalmic viscosurgical devices market is highly competitive, with major players focusing on innovation, product quality, and global expansion. Leading companies such as Alcon, Johnson & Johnson Vision Care, Bausch + Lomb, and Carl Zeiss Meditec dominate with strong brand recognition and diversified portfolios. Mid-tier firms and regional manufacturers are gaining traction by offering cost-effective solutions for emerging economies. Partnerships, acquisitions, and continuous R&D investment remain key competitive strategies. It is shaped by intense competition, strong clinical demand, and the constant pursuit of better surgical outcomes.

Recent Developments:

- In April 2023, Bausch + Lomb announced the U.S. launch of StableVisc, a cohesive ophthalmic viscosurgical device (OVD), along with the TotalVisc Viscoelastic System. These innovations provide eye surgeons new dual-action protection options during cataract surgery, with StableVisc helping maintain space in the anterior chamber and TotalVisc offering combined mechanical and chemical protection. Both products contain sodium hyaluronate and sorbitol, enhancing protection and free radical scavenging capabilities.

- In April 2025, Johnson & Johnson Vision Care presented data supporting the next-generation Tecnis Odyssey intraocular lens (IOL) at the American Society of Cataract and Refractive Surgery (ASCRS). The Tecnis Odyssey IOL is recognized as the fastest growing presbyopia-correcting IOL in the U.S., offering superior image contrast, wide vision range, and reduced dysphotopsias, affirming its position as a leading advanced surgical solution.

- In August 2025, Rayner launched the RayOne Galaxy and RayOne Galaxy Toric intraocular lenses in Brazil, introducing the world’s first spiral IOL designed with artificial intelligence. This AI-designed lens provides a continuous full range of vision with zero light loss and minimizes dysphotopsia. The launch marks a significant advancement in premium lens replacement technology.

- In December 2024, HOYA Surgical Optics launched VisuPro advanced focus spectacle lenses targeted at young presbyopes. These lenses use Binocular Harmonization Technology to optimize near vision and reduce eye strain from digital device usage, addressing early presbyopia needs with comfortable and sharp focus throughout the day.

Report Coverage:

The research report offers an in-depth analysis based on type/product type, source, application, and end use. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising cataract and glaucoma prevalence will sustain strong demand.

- Emerging economies will offer new growth opportunities.

- Premium viscoelastic products will see increased adoption in advanced markets.

- Digital tools and AI will enhance surgical precision and efficiency.

- Local manufacturing in Asia-Pacific will improve accessibility.

- Hospitals will remain the primary end-use setting for adoption.

- Regulatory frameworks will influence product development strategies.

- Sustainability in production will gain greater focus.

- Consolidation among global leaders will reshape competition.

- Innovation in viscoadaptive formulations will expand clinical applications.