Palladium Chloride Market Overview:

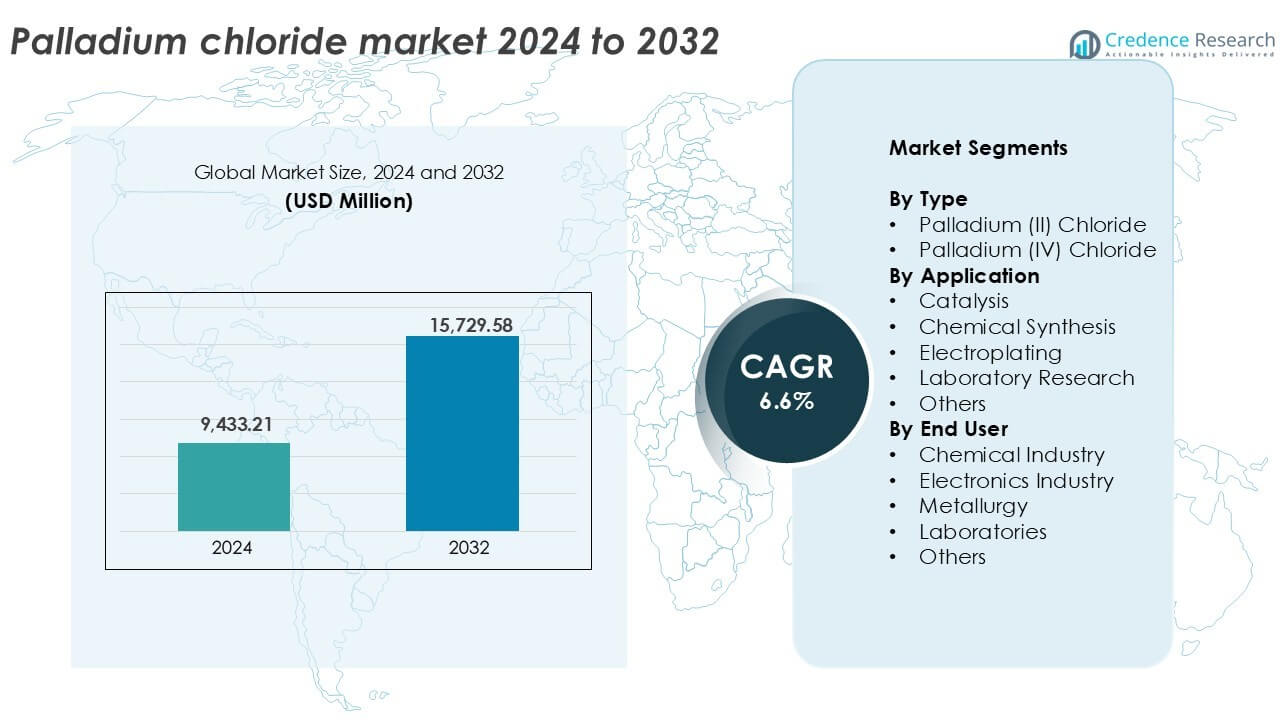

The Palladium Chloride market size was valued at USD 9,433.21 million in 2024 and is anticipated to reach USD 15,729.58 million by 2032, growing at a CAGR of 6.6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Palladium Chloride Market Size 2024 |

USD 9,433.21 million |

| Palladium Chloride Market, CAGR |

6.6% |

| Palladium Chloride Market Size 2032 |

USD 15,729.58 million |

Palladium Chloride Market Insights

- Demand rises due to strong use in catalysis for pharmaceuticals, fine chemicals and advanced synthesis processes. Palladium (II) chloride dominates by type, holding over 70% share, driven by high reactivity and wide industrial acceptance.

- Growing electronics manufacturing supports trends in electroplating, especially for connectors and circuit boards. Research-led adoption of palladium-based catalysts and nanomaterials creates new opportunities across laboratories and specialty chemicals.

- Competition remains moderately consolidated, led by global precious metal and chemical companies focusing on purity, recycling and supply security. High raw material costs and palladium price volatility act as key restraints.

- Asia-Pacific leads with 34% market share, supported by electronics and chemical production. North America holds 28%, Europe 24%, while Latin America and the Middle East and Africa together account for the remaining share, driven by emerging industrial growth.

Palladium Chloride Market Segmentation Analysis

By type

Palladium (II) chloride dominated the market with over 72% share in 2024. Its widespread use in homogeneous and heterogeneous catalytic processes drives this leadership. The compound’s high solubility and reactivity make it a preferred precursor in organometallic chemistry. Industries favor palladium (II) chloride for its role in cross-coupling reactions and efficient carbon-carbon bond formation. Palladium (IV) chloride holds a smaller share due to limited industrial adoption. Its usage remains confined to niche oxidation reactions and academic research applications, offering moderate growth potential in specialized synthesis.

- Johnson Matthey supplies palladium (II) chloride for homogeneous catalysis applications. The compound is used as a precursor in Suzuki and Heck coupling reactions.

By application

Catalysis emerged as the dominant application segment, accounting for nearly 48% of market share in 2024. Demand stems from its role in hydrogenation, dehydrogenation and carbon-carbon coupling reactions. Palladium chloride acts as a highly efficient catalyst, especially in petrochemical and fine chemical synthesis. Chemical synthesis followed as the second-largest segment, driven by rising use in preparing complex organic molecules. Electroplating applications continue to grow in electronics manufacturing, while laboratory research and other segments contribute marginally, supported by academic and small-scale industrial studies.

- BASF uses palladium-based catalysts in fine chemical production. Palladium chloride-derived catalysts enable selective hydrogenation processes. BASF operates more than 230 production sites globally.

By end user

The chemical industry led the end-user segment with a 41% market share in 2024, driven by large-scale use of palladium chloride in catalytic reactions and complex compound manufacturing. Electronics followed closely, fueled by rising demand for high-performance coatings and circuit plating. Metallurgy benefits from palladium’s corrosion resistance and conductivity, especially in refining and alloy processing. Laboratories represent a growing user base due to expanded R&D in material sciences and catalysis. Other end users include automotive and pharmaceuticals, where palladium compounds are being explored for advanced catalytic and synthesis applications.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key growth drivers

Rising demand for catalysts in fine chemical and pharmaceutical synthesis

Palladium chloride plays a central role in catalysis, especially in pharmaceutical and fine chemical production. Its efficiency in facilitating carbon-carbon and carbon-heteroatom bond formation makes it indispensable for processes like Suzuki, Heck and Sonogashira coupling reactions. The pharmaceutical sector increasingly relies on these palladium-based catalysts to produce active pharmaceutical ingredients with high selectivity and yield. As global drug development expands, particularly for oncology and central nervous system therapies, the need for precise and scalable synthesis routes strengthens. Fine chemical manufacturers also leverage palladium chloride for custom and bulk molecule development. The drive toward green chemistry and process optimization further increases its relevance, as palladium-based systems offer lower energy consumption and reduced waste.

- Johnson Matthey supplies palladium chloride used in Suzuki and Heck coupling reactions. The compound serves as a precursor for palladium acetate and supported catalysts.

Expansion of electronics manufacturing and electroplating applications

Palladium chloride serves as a critical material in electronic component manufacturing, particularly in electroplating for connectors, semiconductors and printed circuit boards. As demand for miniaturized, high-performance electronics grows, manufacturers require advanced plating solutions that provide corrosion resistance, excellent conductivity and reliable bonding. Palladium chloride offers consistent deposition and thin-layer control, making it ideal for smartphones, automotive electronics and data storage devices. The global expansion of 5G infrastructure and proliferation of Internet of Things devices further strengthen this need. Emerging economies in Asia-Pacific, including China, South Korea and India, are ramping up electronics production, generating sustained demand.

- Umicore supplies palladium-based electroplating chemicals for electronics. Its palladium chloride solutions enable controlled thin-layer deposition on connectors.

Government-led initiatives in green chemistry and precious metal recovery

Sustainability efforts have intensified focus on recyclable catalysts and eco-friendly chemical processes. Palladium chloride, as a homogeneous and recyclable catalyst, aligns well with green chemistry principles promoted by regulatory bodies and international organizations. Governments and research institutions are increasingly funding clean synthesis technologies and circular economy models that favor catalyst recovery and reuse. Palladium’s high value and reusability make it an attractive investment for firms seeking reduced environmental impact and cost-effective operations. Europe and North America have implemented policies encouraging recycling of platinum-group metals, spurring innovations in metal recovery technologies.

Key trends and opportunities

Advancements in palladium-based nanocatalysts

Nanotechnology is creating new frontiers in catalysis, and palladium chloride is central to this innovation. Researchers are developing palladium-based nanocatalysts that offer higher surface area, enhanced reactivity and improved selectivity in complex reactions. These nanocatalysts reduce palladium usage while boosting performance, making them cost-effective and environmentally favorable. The trend is gaining attention in pharmaceutical, petrochemical and energy sectors where high-efficiency catalysis is vital. Nanocatalysts also support emerging areas like biomass conversion and hydrogenation under mild conditions. As sustainability and resource efficiency become core strategies, nanotechnology offers a clear pathway for extending palladium chloride’s utility into next-generation catalysts, sensors and energy storage systems.

- Johnson Matthey developed palladium nanocatalysts with particle sizes below five nanometers for fine chemical synthesis. These catalysts deliver higher turnover frequency compared to conventional supported palladium systems.

Growing adoption in academic and industrial research applications

Academic institutions and R&D centers are increasingly adopting palladium chloride for complex molecule design, sensor development and reaction mechanism studies. Its predictable reactivity, stability and solubility make it ideal for advanced chemistry experiments and process innovations. Universities and research labs are expanding its role beyond traditional catalysis — exploring uses in organic photovoltaic materials, bioconjugation techniques and CO₂ reduction processes. Startups and chemical innovators are also tapping into palladium chloride’s potential to develop new ligands, chiral complexes and hybrid materials. These experimental pathways offer new commercial applications and enhance its value in specialty chemical synthesis.

Key challenges

Supply chain volatility and palladium price fluctuations

Palladium is a rare and expensive metal, with limited global production concentrated in a few regions such as Russia and South Africa. Market disruptions, geopolitical tensions or mine shutdowns in these areas can significantly affect supply and price stability. The high price volatility of palladium directly impacts the cost of palladium chloride, influencing profit margins for downstream users. Electronics, automotive and pharmaceutical sectors often struggle with budgeting due to unpredictable price swings. Speculative trading and fluctuating demand in other palladium-consuming sectors — such as catalytic converters — intensify market instability. While recycling helps reduce raw material dependency, it does not fully offset fresh demand.

Stringent handling and environmental regulations

Palladium chloride is a toxic and corrosive compound subject to strict handling, transportation and disposal regulations. Governments impose tight controls on hazardous material management to ensure worker safety and environmental protection. Compliance often requires significant investment in storage infrastructure, protective equipment and training. Companies must also manage waste disposal and emissions in accordance with local and international guidelines. These operational burdens can slow production timelines and increase overall manufacturing costs. Small-scale producers and research facilities may face particular difficulties meeting regulatory standards without affecting profitability.

Regional Analysis

North America

North America held a market share of approximately 28% in 2024, led by the United States. The region benefits from established pharmaceutical and chemical industries that drive high demand for palladium-based catalysts. Ongoing R&D in nanomaterials and a strong presence of specialty chemical manufacturers also support growth. Electroplating applications in electronics and defense sectors further boost consumption. Recycling regulations and sustainability programs encourage the reuse of palladium from industrial waste. Canada contributes through its expanding electronics and mining sectors.

Europe

Europe accounted for around 24% of the global palladium chloride market in 2024. Germany, the United Kingdom and France are major contributors due to strong chemical and pharmaceutical industries. The European Union’s commitment to green chemistry and metal recovery systems enhances regional demand. Government incentives and academic funding support innovation in catalysis and nano-formulations. The region’s strict environmental regulations push companies to adopt palladium-based solutions aligned with sustainability targets. Europe’s balanced approach between research and manufacturing drives consistent market performance.

Asia-Pacific

Asia-Pacific dominated the palladium chloride market with over 34% share in 2024, driven by rapid industrialization and robust electronics manufacturing in China, Japan, South Korea and India. The region’s expanding semiconductor and printed circuit board sectors fuel high-volume demand for electroplating applications. The pharmaceutical industry in India and China increasingly uses palladium catalysts in synthesis. Government investments in clean energy and chemical process efficiency further support growth. Rising academic research output and startup activity enhance laboratory and specialty chemical consumption.

Latin America

Latin America captured around 6% of the global palladium chloride market in 2024, with Brazil and Mexico leading regional consumption. Growth is supported by the development of local chemical industries and increasing demand for specialty materials. Expanding electronics assembly and automotive sectors contribute to electroplating usage. Although the market remains relatively small, government initiatives to attract chemical and electronics investments present growth potential. Limited domestic production capacity and reliance on imports affect cost competitiveness and supply consistency.

Middle East and Africa

The Middle East and Africa held a modest market share of 4% in 2024. The UAE and Saudi Arabia are investing in chemical parks and industrial R&D to diversify their economies beyond oil. These initiatives support catalyst and plating applications in specialty manufacturing. South Africa’s mining and metallurgy sectors offer steady demand for palladium derivatives. Limited local production and weaker regulatory infrastructure for advanced chemicals restrain faster growth. Strategic collaborations with international firms could unlock new opportunities in this underpenetrated region.

Palladium Chloride Market Segmentations:

By Type

- Palladium (II) Chloride

- Palladium (IV) Chloride

By Application

- Catalysis

- Chemical Synthesis

- Electroplating

- Laboratory Research

- Others

By End User

- Chemical Industry

- Electronics Industry

- Metallurgy

- Laboratories

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the palladium chloride market features a mix of global chemical manufacturers, precious metal refiners and specialized catalyst producers. Key players include Umicore, BASF SE, Tanaka Holdings, Johnson Matthey Plc, Heraeus Holding and Anglo American Platinum. These companies leverage vertically integrated operations covering raw material sourcing, refining and compound formulation. Firms such as Metalor, Alfa Aesar and Sigma-Aldrich Corp. cater to research and specialty segments with high-purity grades. Strategic priorities include expanding production capacity, enhancing recycling capabilities and developing advanced palladium-based catalysts. Collaborative R&D, particularly in nanocatalysts and sustainable recovery technologies, shapes future competitiveness. The market remains moderately consolidated, with top players holding significant shares due to established infrastructure and global customer bases. Regional firms like Vineeth Precious Catalysts and Gelest target niche demand with localized solutions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key player analysis

- Umicore

- BASF SE

- Tanaka Holdings Co. Ltd.

- Johnson Matthey Chemicals

- Goodfellow Cambridge Limited

- Metalor

- Sigma-Aldrich Corp.

- Vineeth Precious Catalysts Pvt. Ltd.

- Heraeus Holding

- Alfa Aesar

- Johnson Matthey Plc

- Anglo American Platinum

- American Elements

- Gelest Inc.

Recent developments

- In 2022, TANAKA Kikinzoku Kogyo contributed to the DMC No. 1 Investment Limited Partnership venture capital fund to support the establishment of a medical venture ecosystem in Japan. The investment aligns with the goal of advancing technology within Japan’s medical and healthcare sector.

- In 2022, BASF and Heraeus collaborated to establish a joint venture in China focused on advanced precious metal recycling for high-tech industries. The initiative promotes a circular economy by recycling spent catalysts containing precious metals, contributing to sustainable resource management.

Report coverage

The research report offers an in-depth analysis based on type, application, end user and geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams and key applications. The report also includes insights into the competitive environment, SWOT analysis, current market trends, and primary drivers and constraints. It examines market dynamics, regulatory scenarios and technological advancements shaping the industry, and provides strategic recommendations for new entrants and established companies.

Future outlook

- Demand for palladium chloride will grow with rising use in pharmaceutical and fine chemical synthesis.

- Advanced catalyst development will continue to drive innovation in industrial and academic applications.

- Nanotechnology will enhance the efficiency and performance of palladium-based catalysts.

- Electroplating demand will increase with expansion in electronics and semiconductor manufacturing.

- Recycling technologies will become more important to reduce dependence on primary palladium sources.

- Asia-Pacific will remain the largest and fastest-growing region due to industrial output and R&D investment.

- Market players will focus on purity, consistent supply and sustainable production processes.

- Price volatility of palladium will drive interest in alternative catalysts and cost-control measures.

- Government support for green chemistry and precious metal recovery will open new growth channels.

- The competitive landscape will see deeper collaboration between refiners, chemical firms and technology innovators.