Market Overview

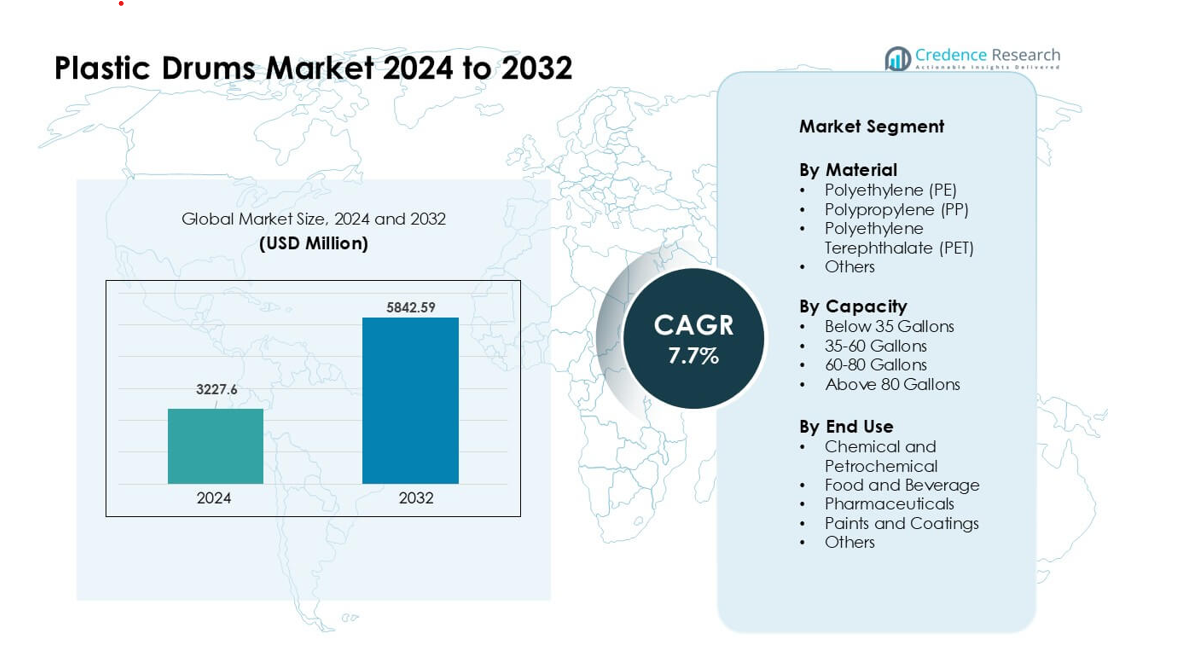

Plastic Drums Market was valued at USD 3227.6 million in 2024 and is anticipated to reach USD 5842.59 million by 2032, growing at a CAGR of 7.7 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Plastic Drums Market Size 2024 |

USD 3227.6 million |

| Plastic Drums Market, CAGR |

7.7% |

| Plastic Drums Market Size 2032 |

USD 5842.59 million |

The Plastic Drums Market is shaped by major players such as Greif, Mauser Packaging Solutions, Schütz GmbH & Co. KGaA, Time Technoplast Ltd., CurTec, Eagle Manufacturing, Cospak, C.L. Smith, The Cary Company, and U.S. COEXCELL INC. These companies compete through advanced HDPE drum designs, UN-certified safety standards, and expanding reconditioning networks that support circular packaging. Asia Pacific remained the leading region in 2024 with about 42% share, driven by strong chemical, pharmaceutical, and food-processing output. High manufacturing activity and rising export volumes kept the region at the forefront of global demand.

Market Insights

- The Plastic Drums Market reached USD 6 million in 2024 and is projected to grow at a CAGR of 7.7% through 2032.

- Strong demand from chemical and petrochemical industries drives adoption, with this segment holding about 54% share due to the need for safe, corrosion-resistant bulk packaging.

- Trends include rising use of reconditioned drums, growth in large-capacity formats, and higher adoption of recycled-content HDPE to meet sustainability goals across global supply chains.

- Competition remains strong among Greif, Mauser Packaging Solutions, Schütz, Time Technoplast, and others, with manufacturers focusing on UN-certified designs, automation, and circular packaging systems; raw material price swings act as a key restraint.

- Asia Pacific leads the market with nearly 42% share, supported by rapid industrial expansion, followed by North America at 28% and Europe at 26%, reflecting strong usage across chemicals, food, pharmaceuticals, and coatings applications.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Material

Polyethylene (PE) held the dominant position in 2024 with nearly 62% share due to strong durability, corrosion resistance, and safe handling of hazardous liquids. Manufacturers preferred PE because the material supports light weight, long service life, and wide chemical compatibility. PP and PET gained steady demand in sectors needing higher heat resistance or better transparency. Growth in global chemical trade and tighter safety rules pushed industries to adopt PE-based drums for bulk storage and transport. Rising recycling rates and higher use of HDPE also strengthened PE leadership across major markets.

- For instance, Time Technoplast Ltd a major industrial‑packaging manufacturer produces HM‑HDPE drums in the 200–250 litre range via automated blow‑moulding processes, ensuring mechanical strength and chemical resistance even for aggressive solvents.

By Capacity

Drums above 80 gallons led the segment in 2024 with about 48% share because large industries favored high-volume packaging for lower handling costs. Chemical, petrochemical, and paint producers used these drums to streamline bulk movement and reduce repeat shipments. Demand for 35–60-gallon units stayed stable in food and pharma due to easier manual handling. Growth in global trade and rising hazardous goods transport supported the need for bigger drums. Higher use in ports, warehouses, and long-haul logistics kept the above-80-gallon category in a strong position.

- For instance, many industrial‑drum suppliers in India offer 210‑litre (≈ 55 gallon) drums e.g., a 210 L drum from JSK Plast has a diameter of about 600 mm and a height of about 915 mm, and weighs around 7.8 to 8.5 kg, making it suitable for bulk chemical storage and transport.

By End Use

Chemical and petrochemical applications dominated in 2024 with nearly 54% share as this sector required robust containers for acids, solvents, and specialty chemicals. Industries relied on plastic drums for leak prevention, corrosion resistance, and compliance with global transport standards. Food and beverage demand grew due to rising use of hygienic, food-grade drums, while pharmaceuticals adopted drums for sensitive ingredient handling. Paints and coatings expanded use during construction growth cycles. Strong chemical production output across Asia and steady exports drove the dominant performance of the chemical and petrochemical segment.

Key Growth Drivers

Rising Demand from Chemical and Petrochemical Industries

Chemical and petrochemical producers drove strong demand for plastic drums because these containers offer high durability, safe chemical handling, and compliance with global transport rules. Many companies expanded bulk exports, which increased the need for lightweight, corrosion-resistant drums that reduce leakage risks. Growth in specialty chemicals and higher handling standards also supported wider adoption of high-density polyethylene drums. Large drum formats helped reduce logistics cost and improve warehouse efficiency. Strong output from Asia and rising global trade volumes continued to push steady procurement across major producers, making this driver a key force behind market expansion.

- For instance, a 210 L HDPE drum produced by a supplier such as Gayatri Polyplast meets UN‑approved specifications for hazardous goods transport, enabling safe handling of aggressive chemicals like solvents or caustics under international freight norms.

Growing Use in Food, Beverage, and Pharmaceutical Supply Chains

Food and drug industries adopted plastic drums to support hygienic storage, ingredient transport, and quality control standards. Many users shifted from metal to plastic because plastic drums resist contamination and support food-grade and pharma-grade compliance. Rising processed food demand, global cold-chain expansion, and higher export volumes strengthened drum usage across these sectors. Lightweight handling and lower cleaning effort also improved operational efficiency. Increasing investment in nutraceuticals and biopharma boosted the need for safe, inert packaging. Stricter hygiene rules across production centers kept plastic drums in strong demand across these supply chains.

- For instance, HDPE drums designed for food‑grade applications often comply with requirements for safe contact with consumables, making them suitable for storing ingredients such as syrups, edible oils or pharmaceutical intermediates without risk of leaching or contamination.

Shift Toward Reusable and Recyclable Packaging Solutions

Industries adopted reusable and recyclable drums to cut waste and meet sustainability goals. Companies preferred HDPE drums because they allow repeated use and easier recycling in closed-loop systems. Many global brands introduced circular packaging policies that pushed suppliers to expand recycled-content drum production. Reconditioning services also grew, reducing lifecycle cost and lowering environmental impact. Governments supported this shift by tightening waste rules and promoting eco-friendly industrial packaging. Rising adoption of green logistics and sustainability reporting strengthened this growth driver, making recyclable plastic drums a core part of long-term packaging strategies.

Key Trends & Opportunities

Expansion of Reconditioned and Refurbished Drum Markets

Reconditioned drums gained attention because they provide lower cost, safe performance, and reduced material waste. Many users in chemicals, paints, and agriculture adopted refurbished drums to control spending while meeting packaging safety rules. Drum reconditioning networks expanded across major ports and industrial hubs, which improved availability and turnaround time. Sustainability targets also encouraged companies to adopt refurbished options. Supported by stricter waste-reduction policies, this trend enhanced circular economy goals and opened new opportunities for service providers offering cleaning, testing, and certification.

- For instance, service providers now offer drum‑tracking, certification, and automated cleaning/inspection as part of reconditioning packages, helping companies meet compliance without buying new drums.

Growth of Large-Capacity Drums in Bulk Logistics

Large-capacity drums grew in use because they help lower handling costs and reduce shipping frequency. This trend expanded with rising export volumes of chemicals, coatings, and liquid ingredients. Logistics operators adopted bigger drums to optimize container loads and reduce warehouse space. Companies also developed stronger, impact-resistant designs for long-haul transport. Demand from ports, distribution hubs, and global freight corridors increased adoption of high-volume formats, creating new product development opportunities for manufacturers.

- For instance, in petrochemical, chemical, and lubricants sectors, reconditioning services processed and reissued millions of drums plastic and steel for reuse in bulk logistics, emphasizing the viability of large-capacity drums in repeated transport cycles.

Technological Upgrades in Drum Design and Safety Features

Manufacturers offered improved drum designs featuring stronger walls, anti-static properties, UN-certified safety standards, and improved handling grips. Adoption of smart labeling and tracking supported better supply-chain visibility. New molding technologies provided stronger resistance to pressure and impact. These improvements created opportunities across sensitive industries such as pharmaceuticals and hazardous chemical transport.

Key Challenges

Fluctuating Raw Material Prices

Plastic drum manufacturers faced cost pressure due to volatile petrochemical feedstock prices. Shifts in crude oil markets affected the pricing of polyethylene and polypropylene, making production planning harder for suppliers. Many producers struggled to balance margin control with customer price expectations. Sudden price spikes also reduced purchase volumes in price-sensitive sectors. This challenge forced manufacturers to adopt stronger procurement planning, long-term supply contracts, and improved recycling systems to stabilize input availability.

Rising Regulatory Compliance Requirements

Manufacturers faced tighter rules governing chemical transport, food-grade packaging, and waste handling. Compliance demanded investment in testing, certification, and upgraded manufacturing processes. Smaller drum makers found it hard to meet evolving global standards, which increased operational burden. Failure to comply risked shipment delays and penalties across international trade routes. Regulations also pushed companies to adjust product designs, adopt traceability systems, and enhance quality audits, raising overall cost and complexity for the sector.

Regional Analysis

North America

North America held about 28% share in 2024, driven by strong demand from chemical, pharmaceutical, and food-processing industries. Manufacturers preferred HDPE drums because they support safe handling, advanced compliance needs, and bulk distribution across long logistics routes. Growth in chemical exports from the U.S. Gulf Coast and rising demand for hygienic packaging strengthened regional usage. Expanding drum reconditioning networks also supported circular packaging goals. The region benefited from steady investment in manufacturing, well-regulated transport standards, and strong adoption of large-capacity drums across major distributors.

Europe

Europe accounted for nearly 26% share in 2024, supported by strict packaging safety rules and a strong focus on sustainability. Industries adopted recyclable and reconditioned drums to meet environmental targets and reduce waste. Chemical and coatings production across Germany, France, and the U.K. drove steady procurement of certified HDPE drums for hazardous material handling. Demand also grew in food and pharma due to stringent hygiene norms. Widespread use of bulk packaging formats and advanced recycling infrastructure kept Europe a stable market with rising preference for high-performance, compliant drum designs.

Asia Pacific

Asia Pacific led the global market in 2024 with around 42% share, supported by strong industrial growth and large-scale chemical, petrochemical, and food-processing output. Rapid expansion in manufacturing hubs across China, India, and Southeast Asia boosted drum consumption for bulk movement of chemicals, ingredients, and solvents. Companies preferred lightweight, durable HDPE drums to meet rising export loads and fast logistics cycles. Growing pharmaceutical production and higher agricultural chemical use strengthened demand. Increasing investment in industrial packaging, rising safety standards, and cost-effective production capacity kept the region the strongest global contributor.

Latin America

Latin America captured about 8% share in 2024, driven by steady growth in chemical, agrochemical, and food-related industries. Brazil and Mexico remained the major consumers, using plastic drums for bulk transport of solvents, fertilizers, and food ingredients. Local producers adopted HDPE drums due to their cost efficiency and resistance to corrosion in varied climates. Rising industrialization and expanding export activity supported demand across ports and distribution hubs. Although cost-sensitive, the region saw growing interest in reusable drums and improved handling systems, supporting moderate but consistent market expansion.

Middle East & Africa

The Middle East & Africa region held nearly 6% share in 2024, supported by strong use in petrochemical, lubricants, and construction chemical sectors. High output from Gulf countries increased demand for durable drums suited for long-distance shipping and harsh climate conditions. Africa’s growing food and pharmaceutical industries also adopted plastic drums for safe ingredient handling and easier storage. Investment in industrial zones and port infrastructure boosted procurement. Although the region remains developing, rising trade flows, expanding chemical processing, and increasing safety standards contributed to steady adoption of plastic drums.

Market Segmentations:

By Material

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Others

By Capacity

- Below 35 Gallons

- 35-60 Gallons

- 60-80 Gallons

- Above 80 Gallons

By End Use

- Chemical and Petrochemical

- Food and Beverage

- Pharmaceuticals

- Paints and Coatings

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Plastic Drums Market features strong competition among leading manufacturers such as Greif, Mauser Packaging Solutions, Schütz GmbH & Co. KGaA, Time Technoplast, CurTec, Eagle Manufacturing, U.S. COEXCELL INC., Cospak, C.L. Smith, and The Cary Company. These companies focused on expanding product portfolios that include UN-certified drums, high-strength HDPE designs, and reconditioned options for circular use. Many players invested in automation, blow-molding upgrades, and lightweight structures to support cost-efficient bulk handling across chemicals, pharmaceuticals, and food industries. Partnerships with logistics firms and reconditioning service networks helped strengthen distribution. Sustainability goals pushed manufacturers to develop recycled-content drums and closed-loop recovery systems. Continuous focus on safety, compliance, and global reach kept competition active across regional and international markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Greif, Inc.

- CurTec

- The Cary Company

- Schütz GmbH & Co. KGaA

- S. COEXCELL INC.

- Time Technoplast Ltd.

- Mauser Packaging Solutions

- Eagle Manufacturing

- Cospak

- L. Smith

Recent Developments

- In August 2025, Schütz GmbH & Co. KGaA Announced further global expansion with a new U.S. production plant (Kenosha, Wisconsin) to manufacture IBCs and plastic drums for North American customers and showcased circular-economy solutions and new drum/jerrycan variants at FACHPACK 2025. These moves bolster Schütz’s capacity for food-certified and recycled-content drum products

- In July 2025, CurTec Became the target of a strategic investment/acquisition intended to accelerate growth and innovation (reported 23 Jul 2025); the company also published new sustainable product lines (ECO LITE drums with biobased content and lighter designs) and renewed sustainability credentials (EcoVadis recognition). These moves focus CurTec drum portfolio on lower-carbon and recycled-content options.

- In May 2025, The Cary Company Expanded U.S. reach by opening a new distribution center in Grand Prairie, Texas (May 9, 2025), strengthening logistics and availability for plastic drums and related bulk containers across the region; Cary continues to list a broad range of HDPE plastic drum SKUs and reconditioned drum services.

Report Coverage

The research report offers an in-depth analysis based on Material, Capacity, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Global demand will rise as chemical and pharmaceutical industries expand production capacity.

- Adoption of recycled-content HDPE drums will increase under stricter sustainability rules.

- Reconditioning and reuse programs will grow as companies shift toward circular packaging.

- Large-capacity drums will gain wider use to support bulk logistics efficiency.

- Manufacturers will invest more in automation to improve drum strength and reduce defects.

- Smart labeling and tracking technologies will enhance supply-chain visibility.

- Food and beverage processors will increase use of food-grade drums for safer ingredient handling.

- Emerging markets in Asia and Africa will drive new consumption through industrial growth.

- Regulations for hazardous material transport will push demand for UN-certified drum designs.

- Partnerships between drum makers and logistics firms will expand to support faster distribution.