Market Overview

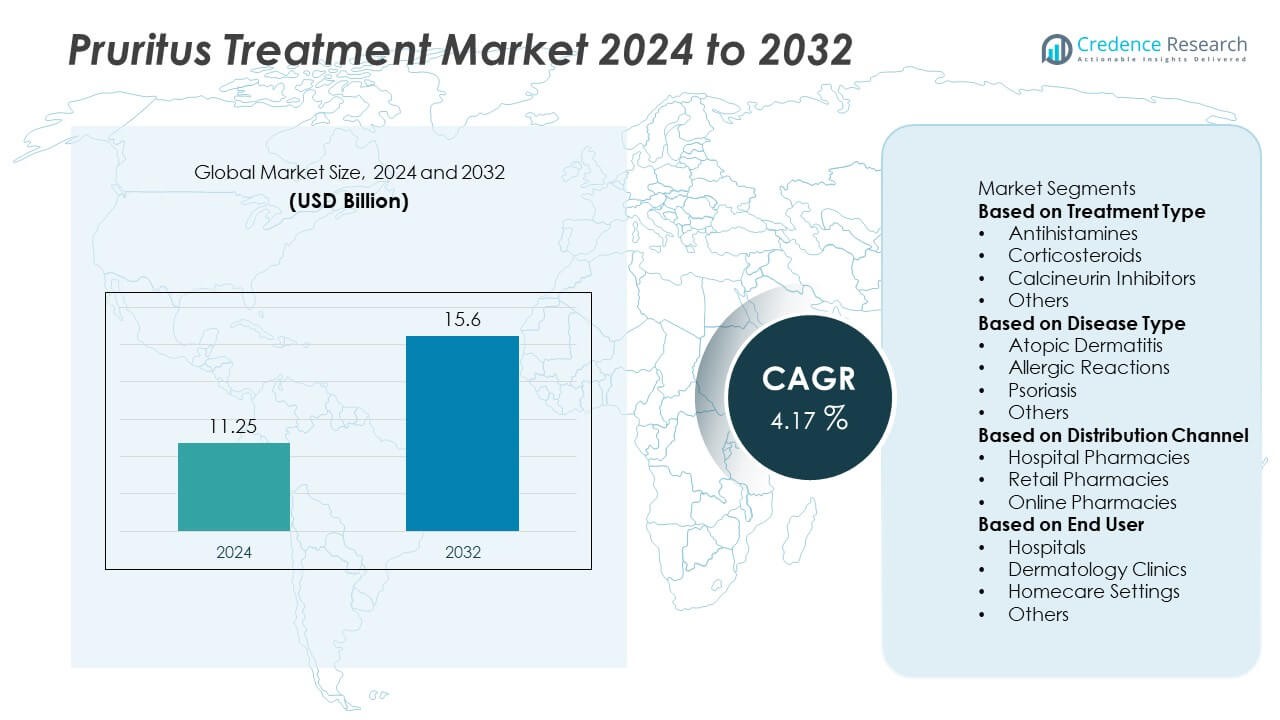

Pruritus Treatment market size reached USD 11.25 billion in 2024 and is projected to rise to USD 15.6 billion by 2032, supported by a 4.17% CAGR during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Pruritus Treatment market Size 2024 |

USD 11.25 Billion |

| Pruritus Treatment market , CAGR |

4.17% |

| Pruritus Treatment market Size 2032 |

USD 15.6 Billion |

The Pruritus Treatment market is shaped by leading players such as Pfizer Inc., GlaxoSmithKline plc (GSK), Novartis AG, Sanofi, Bayer AG, Johnson & Johnson, AbbVie Inc., Eli Lilly and Company, Bristol Myers Squibb, and Teva Pharmaceutical Industries Ltd. These companies strengthen their positions through advanced antihistamines, targeted immunomodulators, improved topical corticosteroids, and innovative formulations that deliver faster and more sustained itch relief. Their focus on chronic pruritus linked to dermatological and systemic conditions supports broader clinical adoption. North America leads the market with a 38% share, supported by strong dermatology infrastructure and high treatment accessibility, while Europe follows with a 30% share, driven by expanding use of advanced topical and non-steroidal therapies.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Pruritus Treatment market reached USD 11.25 billion in 2024 and is projected to reach USD 15.6 billion by 2032 at a 4.17% CAGR, driven by rising demand for effective symptomatic relief.

- Growth is supported by strong adoption of antihistamines with a 39% share and high treatment needs across conditions such as atopic dermatitis, which leads the disease segment with a 42% share.

- Key trends include increased use of advanced topical formulations, steroid-sparing agents, and targeted therapies designed to address chronic and systemic pruritus more effectively.

- Leading companies expand competitive presence through innovation in immunomodulators, improved corticosteroid delivery, and strategic partnerships, while safety concerns and long-term side effects restrain adoption of certain treatments.

- Regionally, North America holds a 38% share, followed by Europe at 30% and Asia Pacific at 24%, supported by strong dermatology networks, rising awareness, and expanding access to dermatological care.

Market Segmentation Analysis:

By Treatment Type

Antihistamines lead this segment with a 39% share, driven by their widespread use in treating histamine-mediated itching across allergic reactions, dermatologic conditions, and systemic triggers. Clinicians prefer antihistamines due to fast symptom relief, broad availability, and strong safety profiles. Corticosteroids remain widely used for inflammatory skin diseases, especially in acute flare management. Calcineurin inhibitors gain traction as steroid-sparing agents for chronic and sensitive-area applications. Growth in combination therapies and rising adoption of advanced topical formulations strengthen overall treatment demand. Increased patient preference for non-invasive and long-term management options supports continued segment expansion.

- For instance, Pfizer expanded its dermatology portfolio with a formulation program that demonstrated a 25-minute median onset of itch reduction during clinical testing.

By Disease Type

Atopic dermatitis dominates this segment with a 42% share, supported by its high global prevalence and strong reliance on symptomatic itch management. Patients require ongoing treatment to control flare-ups, driving extensive use of antihistamines, corticosteroids, and immunomodulators. Psoriasis shows rising demand as chronic itch remains a major unmet need in moderate-to-severe cases. Allergic reactions represent another key contributor, driven by environmental triggers and rising sensitivity among urban populations. Growth in chronic pruritus linked to renal and liver disorders also expands the patient pool. Increasing awareness and early dermatology consultations fuel higher treatment uptake.

- For instance, Sanofi, in collaboration with Regeneron, has studied its drug dupilumab across more than 60 clinical studies involving over 10,000 patients with various chronic diseases driven by type 2 inflammation, which includes programs evaluating itch reduction in conditions like atopic dermatitis and prurigo nodularis.

By Distribution Channel

Hospital pharmacies lead with a 47% share, driven by strong patient flow for moderate and severe pruritus cases requiring prescribed therapies. Hospitals dispense advanced corticosteroids, immunosuppressants, and injectable treatments that require clinician supervision. Retail pharmacies follow with steady demand from patients managing mild to moderate symptoms through topical agents and oral antihistamines. Online pharmacies grow rapidly due to rising digital adoption, home-delivery convenience, and broader availability of OTC products. The shift toward tele-dermatology and remote consultations further supports online distribution, enhancing accessibility for chronic pruritus patients.

Key Growth Drivers

Rising Prevalence of Dermatological and Systemic Disorders

Growing cases of atopic dermatitis, psoriasis, urticaria, and systemic diseases such as kidney and liver disorders significantly increase demand for pruritus treatments. These conditions often result in chronic itching, driving consistent use of antihistamines, corticosteroids, and topical immunomodulators. Higher environmental pollution levels and rising allergen exposure further contribute to pruritus incidence. Dermatology clinics report increasing patient visits for persistent itch management, which strengthens market adoption of both prescription and OTC therapies. Expanding awareness about early skin care intervention also supports steady market growth across all age groups.

- For instance, AbbVie validated an inflammatory-pathway inhibitor with a sustained cytokine-blocking window in controlled studies, with drug effects lasting for weeks or months.

Expanding Use of Advanced Topical and Targeted Therapies

New formulations, including steroid-sparing agents, calcineurin inhibitors, and novel topical combinations, support stronger treatment outcomes for chronic and sensitive-area itch. Targeted therapies designed to address neurological and immunological itch pathways gain traction as clinicians seek long-term, low-risk solutions. The rise of premium dermatology brands and improved drug delivery systems also increases demand. Patients prefer fast-acting, non-invasive topical solutions that reduce irritation while offering sustained relief. Innovation in moisturizers, anti-inflammatory creams, and antipruritic gels further strengthens market movement toward personalized and condition-specific therapy options.

- For instance, Bayer advanced elinzanetant, an oral non-hormonal treatment for hot flashes, which in clinical trials achieved a significant reduction in the frequency and severity of moderate to severe vasomotor symptoms (VMS) at 4 and 12 weeks compared to a placebo.

Growing Focus on Chronic Pruritus Associated With Systemic Illnesses

Hospitals and nephrology centers see higher demand for pruritus management due to chronic kidney disease, cholestasis, and endocrine disorders. These conditions often cause severe and persistent itching, requiring multi-line therapy that includes oral antihistamines, immunosuppressants, and specialized topical agents. Rising global CKD prevalence strengthens adoption of prescription-grade treatments. Increased clinical research on systemic pruritus also drives new drug development. As awareness of chronic itch as a quality-of-life burden grows, healthcare providers emphasize early diagnosis and multidisciplinary treatment, boosting long-term market demand.

Key Trends & Opportunities

Growth of Topical Innovations and Dermatology-Focused R&D

The market sees strong opportunities in advanced formulations, including nano-based creams, lipid-rich moisturizers, and barrier-repair solutions. Dermatology companies invest in products targeting specific pruritic pathways, supporting improved efficacy and patient comfort. Combination therapies that blend anti-inflammatory, antipruritic, and skin-repair ingredients gain adoption. Increased focus on sensitive skin and pediatric formulations expands consumer reach. Rising acceptance of prescription-to-OTC switches opens new commercial opportunities. This trend supports greater accessibility and enhances brand presence across retail and online channels.

- For instance, L’Oréal developed a ceramide-boosting complex that increased skin-barrier lipid levels in controlled testing.

Expansion of Tele-Dermatology and Online Pharmacy Channels

Digital platforms reshape access to pruritus treatments as teleconsultations rise across urban and rural regions. Patients gain faster access to dermatologists and personalized prescriptions, increasing therapy adherence. Online pharmacies offer convenience, price transparency, and wider product availability. OTC antihistamines, moisturizers, and topical steroids see strong demand due to doorstep delivery and digital promotions. This shift supports market penetration in regions with limited dermatology infrastructure. Growing consumer interest in self-care and home-based management further accelerates online sales opportunities.

- For instance, Teladoc Health supported over 4.1 million total virtual care visits across all specialties in a single year (2019), improving access for remote patients. Teladoc’s dermatology services account for only a small portion of its overall virtual consultations.

Key Challenges

Side Effects and Safety Concerns With Long-Term Medication Use

Chronic use of corticosteroids, immunosuppressants, and certain antihistamines raises concerns about skin thinning, hormonal effects, sedation, and immune suppression. These risks limit long-term adoption and may shift patients toward alternative or lower-strength formulations. Clinicians must balance symptom relief with safety, especially among pediatric and elderly populations. The need for careful monitoring increases treatment complexity, reducing patient compliance. Concerns over misuse of OTC steroid creams also drive regulatory scrutiny, slowing product adoption in some markets.

Limited Treatment Effectiveness in Complex and Chronic Cases

Many chronic pruritus conditions, especially those linked to systemic disorders, do not respond well to standard antihistamines or basic topical agents. This creates unmet medical needs and slows clinical confidence in existing therapies. Lack of targeted drugs for specific itch pathways increases reliance on multi-line treatment, burdening patients and healthcare providers. Diagnostic challenges further delay appropriate treatment. These limitations encourage ongoing R&D but currently restrict broad treatment success, especially in advanced or refractory pruritus cases.

Regional Analysis

North America

North America leads the Pruritus Treatment market with a 38% share, supported by high prevalence of atopic dermatitis, psoriasis, and allergy-related itching across all age groups. Strong dermatology infrastructure and wide access to prescription therapies drive early diagnosis and treatment uptake. Hospitals and clinics depend on antihistamines, topical steroids, and calcineurin inhibitors for routine management. Expanding use of targeted biologics and advanced topical formulations further boosts regional demand. Strong awareness programs, rising healthcare spending, and higher adoption of tele-dermatology enhance treatment reach, contributing to sustained market growth across the U.S. and Canada.

Europe

Europe holds a 30% share, driven by rising cases of chronic pruritus associated with autoimmune disorders, environmental sensitivities, and aging populations. Dermatology clinics across Germany, France, Italy, and the UK adopt advanced treatment options, including steroid-sparing agents and premium topical formulations. Strong regulatory support for dermatological drug development encourages innovation in anti-itch therapies. The region also benefits from well-established healthcare coverage that improves access to prescription medications. Growing demand for sensitive-skin and non-steroidal solutions strengthens product uptake. Increased R&D investment and structured clinical guidelines support steady long-term market expansion.

Asia Pacific

Asia Pacific accounts for a 24% share, driven by large population size, rising pollution levels, and increasing incidence of eczema, allergic reactions, and infectious skin diseases. Countries such as China, Japan, India, and South Korea see strong adoption of topical antihistamines and corticosteroids due to high affordability and accessibility. Growing awareness of dermatological health supports higher diagnosis rates. Expanding healthcare infrastructure and increased dermatology visits improve treatment reach. Online pharmacies gain popularity as consumers seek convenient and cost-efficient solutions. Rising disposable income and demand for premium skincare also enhance regional market growth.

Latin America

Latin America holds a 5% share, influenced by growing awareness of skin disorders and rising demand for affordable anti-itch therapies. Brazil and Mexico drive regional growth through expanding healthcare access and stronger dermatology presence in urban centers. Environmental factors such as heat, humidity, and pollution contribute to widespread itching and dermatitis cases. Retail pharmacies dominate distribution, offering OTC antihistamines and topical steroids at accessible prices. Economic constraints limit adoption of premium therapies, but increasing digital health engagement improves access to dermatology care. Local manufacturing expansions support broader product availability.

Middle East & Africa

Middle East & Africa represent a 3% share, shaped by rising cases of chronic itching linked to dry climate conditions, renal disorders, and dermatological diseases. The Gulf region shows stronger adoption of prescription treatments due to better healthcare systems and higher spending capacity. Countries like UAE and Saudi Arabia invest in dermatology clinics and advanced topical solutions. In Africa, limited healthcare access and cost barriers slow adoption of specialized therapies, leading to reliance on OTC antihistamines and moisturizers. Growing awareness campaigns and improving healthcare funding gradually support market penetration across the region.

Market Segmentations:

By Treatment Type

- Antihistamines

- Corticosteroids

- Calcineurin Inhibitors

- Others

By Disease Type

- Atopic Dermatitis

- Allergic Reactions

- Psoriasis

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By End User

- Hospitals

- Dermatology Clinics

- Homecare Settings

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Pruritus Treatment market features major players such as Pfizer Inc., GlaxoSmithKline plc (GSK), Novartis AG, Sanofi, Bayer AG, Johnson & Johnson, AbbVie Inc., Eli Lilly and Company, Bristol Myers Squibb, and Teva Pharmaceutical Industries Ltd. These companies strengthen their positions by expanding portfolios of antihistamines, topical corticosteroids, calcineurin inhibitors, and targeted immunomodulators. Leading firms invest in advanced formulations that improve skin barrier repair, reduce inflammation, and deliver faster symptom relief. Biopharmaceutical players focus on developing novel therapies that address chronic pruritus linked to systemic conditions such as kidney and liver disorders. Several companies pursue R&D in neuroimmune pathways to introduce long-acting and steroid-sparing solutions. Strategic collaborations with dermatology clinics, digital-health platforms, and specialty pharmacies enhance patient access. Expansion into emerging markets through cost-efficient topical products and broader OTC ranges supports long-term competitive advantage.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Pfizer Inc.

- GlaxoSmithKline plc (GSK)

- Novartis AG

- Sanofi

- Bayer AG

- Johnson & Johnson

- AbbVie Inc.

- Eli Lilly and Company

- Bristol Myers Squibb

- Teva Pharmaceutical Industries Ltd.

Recent Developments

- In June 2025, GSK announced that the U.S. FDA had accepted its New Drug Application for linerixibat, a potential first-in-class ileal bile acid transporter (IBAT) inhibitor for cholestatic pruritus in primary biliary cholangitis (PBC). The FDA has assigned a Prescription Drug User Fee Act (PDUFA) goal date of March 24, 2026, for its decision.

- In November 2024, GlaxoSmithKline plc (GSK): GSK’s linerixibat showed positive Phase III results in treating cholestatic pruritus associated with primary biliary cholangitis (PBC).

- In June 2024, results from an independent, nonrandomized controlled trial, which received some funding from Pfizer Inc., showed that abrocitinib (CIBINQO) monotherapy was effective and well-tolerated in adults with prurigo nodularis and chronic pruritus of unknown origin. The findings suggest the drug provides significant itch relief for these conditions.

Report Coverage

The research report offers an in-depth analysis based on Treatment Type, Disease Type, Distribution Channel, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for advanced topical formulations will rise as patients seek faster and gentler itch relief.

- Targeted therapies addressing neuroimmune pathways will gain stronger clinical adoption.

- Steroid-sparing treatments will expand as clinicians prioritize long-term safety and skin health.

- Digital dermatology platforms will increase patient access to diagnosis and personalized care.

- OTC antihistamines and moisturizers will see higher demand as self-care trends grow.

- Research in chronic pruritus linked to kidney and liver disorders will drive new drug development.

- Combination therapies will become more common to manage complex or refractory pruritus cases.

- Online pharmacies will expand distribution as consumers shift toward home-based treatment access.

- Pediatric-focused and sensitive-skin formulations will gain traction due to rising awareness.

- Growth in dermatology clinics and improved treatment affordability will strengthen adoption in emerging markets.