Market Overview:

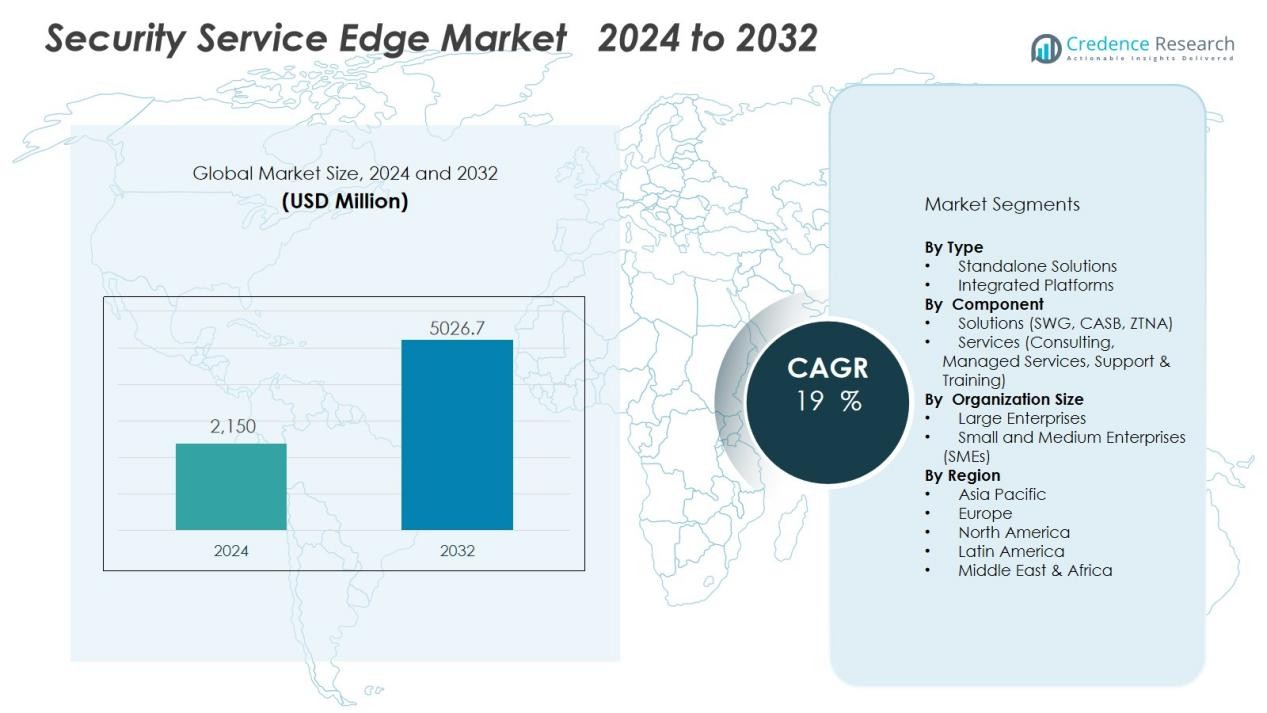

The security service edge market size was valued at USD 2,150 million in 2024 and is anticipated to reach USD 5026.7 million by 2032, at a CAGR of 19% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Security Service Edge Market Size 2024 |

USD 2,150 Million |

| Security Service Edge Market, CAGR |

19 % |

| Security Service Edge Market Size 2032 |

USD 5026.7 Million |

Market growth is driven by several factors, including heightened cyber threats, regulatory compliance requirements, and demand for scalable cloud-based security. Enterprises seek cost efficiency, simplified management, and enhanced protection for distributed workforces and multi-cloud environments. Vendors are increasingly offering advanced features like AI-powered threat detection, data loss prevention, and identity-based security policies. These capabilities are fueling rapid adoption across sectors such as BFSI, IT & telecom, government, and healthcare.

Regionally, North America dominates the security service edge market due to mature IT infrastructure, strong cloud adoption, and leading security vendors. Europe follows closely, with demand driven by GDPR compliance and digital innovation initiatives. Asia-Pacific is expected to witness the fastest growth, supported by large-scale digital transformation in China, India, and Southeast Asia. Meanwhile, Latin America and the Middle East & Africa are emerging markets, where growing connectivity and cyber risks are encouraging investment in SSE platforms.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The security service edge market was valued at USD 2,150 million in 2024 and is forecasted to reach USD 5,026.7 million by 2032 at a CAGR of 19%.

- Rising cyber threats such as ransomware, phishing, and insider attacks are accelerating the adoption of SSE platforms.

- Enterprises are rapidly shifting toward zero trust architectures to ensure continuous authentication of users and devices.

- Cloud adoption and digital transformation initiatives are driving demand for secure access to SaaS, IaaS, and multi-cloud environments.

- Regulatory frameworks like GDPR and HIPAA are compelling businesses to invest in SSE solutions to maintain compliance and protect sensitive data.

- North America leads with over 35% market share in 2024, supported by strong vendor presence and advanced IT infrastructure, while Asia-Pacific records the fastest growth through large-scale digital transformation.

- High implementation costs and integration challenges with legacy systems remain key barriers, but growing demand from SMEs and emerging markets is creating significant opportunities.

Market Drivers:

Rising Cybersecurity Threats and Need for Zero Trust Architectures:

The security service edge market is driven by the growing volume and sophistication of cyber threats. Enterprises face risks from ransomware, phishing, insider attacks, and advanced persistent threats. It enables organizations to adopt zero trust principles, ensuring every user and device is authenticated continuously. This model reduces risks associated with remote work and hybrid IT environments.

- For instance, Google implemented its BeyondCorp zero trust security framework, which authenticates over 100 million devices and users daily across its global workforce, significantly enhancing protection against unauthorized access.

Accelerated Cloud Adoption and Digital Transformation Across Enterprises:

Rapid migration to cloud-based infrastructure fuels demand for SSE solutions. Businesses require security frameworks that extend beyond traditional on-premises networks. The security service edge market supports secure access to SaaS applications, IaaS, and multi-cloud platforms. It ensures protection against data breaches while maintaining seamless user experience. This alignment with digital transformation initiatives is expanding adoption across industries.

Regulatory Compliance and Data Protection Requirements Driving Investment:

Global regulations on data privacy and cybersecurity compliance significantly impact enterprise security strategies. Companies must comply with frameworks such as GDPR, HIPAA, and regional data protection laws. The security service edge market helps organizations enforce unified policies, monitor data movement, and safeguard sensitive information. It offers centralized control that reduces compliance complexity and mitigates financial penalties. Rising regulatory oversight continues to drive investments in these solutions.

- For instance, Microsoft Defender for Endpoint protected more than 300 million devices globally in 2024, helping organizations enforce data security policies consistently.

Demand for Simplified Security Management and Operational Efficiency:

Managing fragmented security tools increases complexity, costs, and vulnerabilities for enterprises. The security service edge market consolidates functions like secure web gateway, CASB, and ZTNA into a unified solution. It allows IT teams to streamline management, reduce overhead, and improve visibility. Centralized dashboards enhance threat response times and policy enforcement. This integration strengthens both operational efficiency and security effectiveness across distributed networks.

Market Trends:

Integration of Artificial Intelligence and Machine Learning in Security Frameworks:

The security service edge market is witnessing strong adoption of artificial intelligence and machine learning to improve detection and response capabilities. AI-driven threat analytics allow faster identification of anomalies across distributed networks. Machine learning models continuously refine detection accuracy, reducing false positives and improving policy enforcement. It enhances predictive capabilities, enabling organizations to anticipate emerging risks and prevent breaches proactively. Vendors are embedding AI into core functions such as data loss prevention, secure web gateways, and zero trust access. This integration strengthens resilience against evolving cyberattacks while ensuring efficiency in large-scale cloud environments.

- For example, CrowdStrike’s Falcon platform uses ML to process over 1 trillion security events per week, enabling highly accurate detection with minimized false alerts.

Growing Shift Toward Unified and Cloud-Native Security Platforms:

The shift from fragmented point solutions to consolidated, cloud-native security is shaping the future of enterprise protection. The security service edge market supports this transition by offering integrated platforms that combine secure web gateways, CASB, and ZTNA. It reduces operational complexity and ensures seamless scalability across multi-cloud and hybrid infrastructures. Businesses value unified architectures that deliver consistent policy enforcement and simplified management. Adoption of cloud-native SSE is accelerating with the rise of remote workforces and global connectivity demands. Vendors are differentiating through flexible deployment models and partnerships with cloud service providers. This trend highlights the growing preference for centralized, adaptable, and cost-efficient security solutions.

- For instance, Palo Alto Networks’ Prisma Access secures more than 400 million SSL connections daily across global points of presence.

Market Challenges Analysis:

Complex Integration with Existing IT and Security Infrastructure:

The security service edge market faces challenges in integrating with legacy systems and diverse IT environments. Many enterprises rely on traditional firewalls, VPNs, and point solutions that complicate deployment of SSE platforms. It often requires significant reconfiguration of network architecture and alignment with existing identity management systems. Businesses must invest in migration strategies that minimize downtime and avoid operational disruptions. Limited interoperability between vendors also slows adoption. These factors make integration a critical barrier for organizations transitioning to SSE frameworks.

High Implementation Costs and Shortage of Skilled Professionals:

Cost remains a major obstacle for enterprises evaluating SSE adoption, particularly in small and medium businesses. The security service edge market demands substantial investments in advanced cloud-native technologies, vendor subscriptions, and workforce training. It creates financial pressure for companies with limited IT budgets. The shortage of cybersecurity professionals skilled in SSE deployment adds another layer of difficulty. Without adequate expertise, enterprises struggle to maximize platform efficiency and maintain compliance. Rising demand for specialized skills continues to drive competition for talent, delaying large-scale implementation.

Market Opportunities:

Expansion of Remote Work and Hybrid Enterprise Environments:

The security service edge market presents strong opportunities through the expansion of remote and hybrid work models. Organizations seek secure, seamless, and scalable access to cloud applications for globally distributed teams. It enables businesses to enforce zero trust policies, protect sensitive data, and ensure compliance across diverse endpoints. Growth in virtual collaboration tools and SaaS adoption further increases demand for unified SSE solutions. Vendors offering flexible, cloud-native platforms stand to gain competitive advantage. This trend creates long-term prospects for adoption across industries prioritizing workforce mobility.

Rising Demand from Emerging Economies and Small to Medium Enterprises:

The security service edge market also benefits from growing digital transformation in emerging economies. Rapid cloud adoption in Asia-Pacific, Latin America, and the Middle East fuels the need for advanced security frameworks. It provides an accessible pathway for small and medium enterprises to replace costly legacy systems. Demand for affordable, subscription-based solutions is creating opportunities for vendors to expand market presence. Government initiatives supporting cybersecurity modernization further enhance adoption in developing regions. This opens significant growth avenues for SSE providers targeting scalable, cost-efficient security solutions.

Market Segmentation Analysis:

By Type:

The security service edge market by type is divided into standalone solutions and integrated platforms. Standalone offerings focus on specific functions like secure web gateways or CASB. Integrated platforms combine multiple capabilities into a single framework, which attracts enterprises seeking simplicity and cost efficiency. It supports organizations with centralized policy enforcement and streamlined management. Demand for integrated solutions continues to rise as enterprises shift toward unified architectures that reduce complexity.

- For instance, Zscaler Secure Web Gateway processes 100 billion daily transactions through its Zero Trust Exchange cloud, inspecting every HTTP(S) request and response for 4,000 enterprise customers across 150 data centers.

By Component:

The market by component includes solutions and services. Solutions dominate with functions such as zero trust network access, secure web gateways, and cloud access security brokers. Services, including consulting, training, and managed security, are gaining traction as enterprises address skill shortages. It enables organizations to optimize adoption while ensuring compliance and operational efficiency. Managed services are expanding due to growing demand for continuous monitoring and proactive threat detection.

- For instance, Zscaler Private Access operates across 150 global data centers, ensuring consistent zero trust enforcement and seamless user-to-app connectivity in under one second per session.

By Organization Size:

The security service edge market by organization size includes large enterprises and small to medium enterprises (SMEs). Large enterprises lead adoption due to advanced IT infrastructure and higher security budgets. SMEs are emerging as a strong growth segment, driven by affordable subscription-based models and cloud-first strategies. It provides scalable protection for SMEs seeking to replace costly legacy systems. Demand across both segments highlights the market’s adaptability to diverse business needs.

Segmentations:

By Type:

- Standalone Solutions

- Integrated Platforms

By Component:

- Solutions (SWG, CASB, ZTNA)

- Services (Consulting, Managed Services, Support & Training)

By Organization Size:

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America:

North America holds the largest market share of the security service edge market, accounting for over 35% in 2024. The region benefits from advanced IT infrastructure, high cloud adoption, and strong presence of leading security vendors. It drives demand through strict data protection regulations and rapid digital transformation across sectors such as BFSI, healthcare, and government. Enterprises in the United States lead investments in SSE platforms due to rising cyberattacks targeting remote workforces. Canada also contributes with increased focus on compliance-driven security. This dominance is reinforced by continuous innovation and strategic partnerships from established technology providers.

Europe:

Europe captures a significant market share of 28% in 2024, driven by stringent data privacy regulations such as GDPR. The security service edge market in the region benefits from enterprises prioritizing regulatory compliance, secure data access, and hybrid work enablement. It is supported by investments in digital infrastructure and rising adoption of unified cloud security platforms. Germany, the United Kingdom, and France represent key contributors with strong enterprise demand. The market expands further as organizations streamline operations through centralized security frameworks. Regional focus on sustainability and secure digital ecosystems also strengthens growth potential.

Asia-Pacific:

Asia-Pacific accounts for a market share of 22% in 2024, with the fastest growth forecasted during the study period. The security service edge market in this region is driven by rapid digitalization, expanding cloud adoption, and rising cybersecurity threats. It gains momentum as small and large enterprises invest in scalable, cloud-native solutions. Countries such as China, India, Japan, and South Korea lead adoption through large-scale enterprise transformation initiatives. Strong government focus on cybersecurity modernization and data localization adds to regional momentum. The region’s expanding IT ecosystem and workforce mobility continue to fuel future opportunities.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Cisco Systems Inc

- VMware Inc

- Cloudflare Inc

- Fortinet Inc

- Zscaler Inc

- Palo Alto Networks Inc

- Cato Networks Ltd

- Forcepoint

- Versa Networks Inc

- Broadcom Corporation

- McAfee Corp

- Checkpoint Software Technologies Ltd

Competitive Analysis:

The security service edge market is highly competitive with strong participation from global technology leaders. Key players include Cisco Systems Inc, VMware Inc, Cloudflare Inc, Fortinet Inc, Zscaler Inc, Palo Alto Networks Inc, Cato Networks Ltd, Forcepoint, and Versa Networks Inc. It is characterized by continuous innovation, where vendors focus on integrating zero trust principles, AI-driven threat detection, and cloud-native capabilities into their platforms. Companies differentiate through scalability, unified policy enforcement, and simplified management of hybrid environments. Strategic partnerships with cloud service providers strengthen market positioning, while mergers and acquisitions expand solution portfolios. Vendors also compete on managed services, catering to enterprises lacking in-house expertise. Competitive intensity is expected to grow as enterprises prioritize unified security solutions that replace legacy systems and support evolving digital transformation needs.

Recent Developments:

- In May 2025, Cisco Systems revealed a new collaboration with the AI Infrastructure Partnership (AIP), joining major technology leaders to drive investment and innovation in AI-focused data centers and infrastructure.

- In December 2023, Broadcom finalized its $69 billion acquisition of VMware, integrating VMware’s products into Broadcom’s enterprise software group and starting a major transformation of offerings.

- In May 2024, Cloudflare expanded its partnership with CrowdStrike to connect platforms, enhance Zero Trust security, and enable AI-native Security Operations Centers for customers.

Report Coverage:

The research report offers an in-depth analysis based on Type, Component, Organization Size and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The security service edge market will evolve into a core component of enterprise cybersecurity strategies.

- It will continue to replace fragmented legacy systems with unified, cloud-native security platforms.

- Vendors will focus on embedding AI and machine learning to enhance predictive threat detection.

- Growing demand for zero trust architectures will reinforce adoption across large and mid-sized enterprises.

- Enterprises will prioritize SSE solutions that integrate seamlessly with multi-cloud and hybrid infrastructures.

- Rising adoption in emerging economies will create new opportunities for scalable and cost-efficient platforms.

- Governments and regulators will influence growth by enforcing stricter data protection and compliance standards.

- Partnerships between cloud providers and security vendors will expand integrated offerings and market reach.

- The shortage of skilled cybersecurity professionals will drive increased reliance on managed SSE services.

- Continuous innovation in identity-based security and adaptive policy enforcement will strengthen competitive differentiation.