Self-Service Technologies Market Overview:

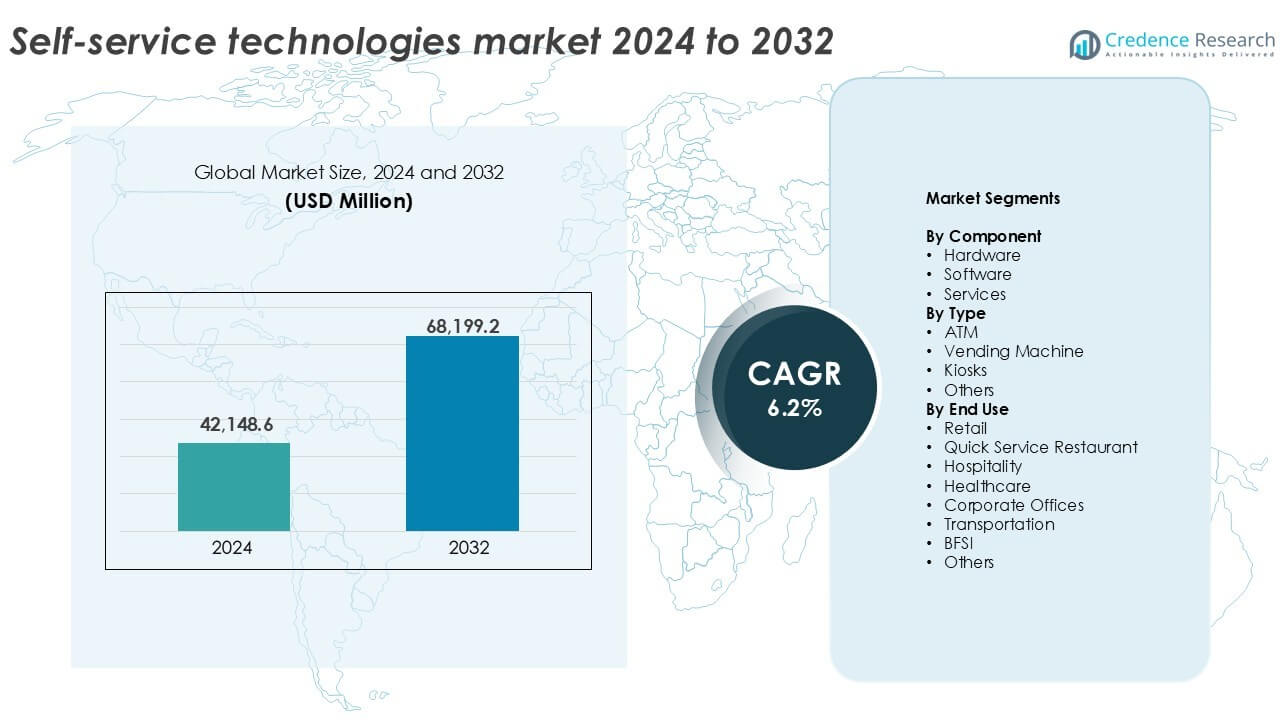

The self-service technologies market size was valued at USD 42,148.6 million in 2024 and is anticipated to reach USD 68,199.2 million by 2032, at a CAGR of 6.2% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Self-Service Technologies Market Size 2024 |

USD 42,148.6 million |

| Self-Service Technologies Market, CAGR |

6.2% |

| Self-Service Technologies Market Size 2032 |

USD 68,199.2 million |

Self-Service Technologies Market Insights

- Rising demand for contactless services across retail, BFSI, and healthcare sectors drives rapid technology adoption.

- Trends such as AI-enabled kiosks, biometric ATMs, and smart vending machines enhance user experience and support real-time data integration.

- NCR Corporation, Diebold Nixdorf, Ingenico Group, and KIOSK Information Systems lead the market with diverse portfolios and strong global presence.

- North America holds the highest regional share at 35%, followed by Europe at 27% and Asia Pacific at 22%. Hardware remains the dominant component with over 55% share, while ATMs lead the type segment with more than 40% share.

Self-Service Technologies Market Segmentation Analysis:

By Component

Hardware dominates the self-service technologies market by component, accounting for over 55% of the market share in 2024. Strong demand for interactive kiosks, ATMs, and vending systems drives hardware sales across sectors. Organizations continue to invest in durable and scalable machines to ensure 24/7 service access. The shift toward touchless interfaces, biometric authentication, and smart dispensing units reinforces hardware upgrades. Hardware demand also rises with deployments in transportation hubs and retail chains. Continuous innovation in physical interfaces ensures user convenience, security, and operational efficiency, making hardware the most preferred component across deployments.

- For instance, Diebold Nixdorf supplies ATM hardware, such as the DN Series, with the capability to integrate biometric solutions, including fingerprint scanners, as optional modules for banks to deploy based on their needs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Type

ATMs represent the largest type segment in the self-service technologies market, capturing more than 40% share in 2024. Their wide usage in banking and public cash access points supports this dominance. ATM networks remain critical in both developed and emerging regions for financial inclusion. Innovations such as cardless withdrawals, facial recognition, and deposit-enabled machines increase utility. Kiosks follow closely, gaining traction in retail, hospitality, and healthcare through self-check-in, information access, and product ordering. Vending machines also expand into non-traditional offerings such as electronics and medicines, supporting the overall type segment growth.

- For instance, NCR-enabled ATMs support QR-based withdrawals used by major banks across Asia and North America. Kiosks expand rapidly beyond banking.

By End Use

The retail sector leads the market by end use, accounting for around 30% of the total market share in 2024. Retailers increasingly deploy self-checkout kiosks, smart vending systems, and digital signage to streamline operations and reduce wait times. Rising customer preference for convenience, speed, and personalized service supports wide adoption. Quick service restaurants (QSRs) follow as a key adopter, integrating self-ordering kiosks and mobile-connected solutions to improve order accuracy and upselling. Healthcare and transportation sectors also show strong growth due to patient check-in kiosks and ticketing systems, highlighting rising use across diverse industries.

Key Growth Drivers

Rising Demand for Contactless and Automated Services

Consumer demand for touch-free and efficient service options has surged, particularly after the COVID-19 pandemic. Businesses across retail, QSR, banking, and healthcare sectors now prioritize self-service technologies to reduce human interaction and improve speed. ATMs, vending machines, and kiosks with features like QR scanning, voice commands, and facial recognition are gaining rapid adoption. This shift addresses hygiene concerns and enhances convenience. Enterprises also benefit from operational cost reductions, minimized staffing needs, and consistent service quality. Contactless solutions also support 24/7 availability, especially in transportation and hospitality sectors. As digital-first customer behavior grows, organizations continue to invest in scalable, low-touch infrastructure, fueling long-term demand.

- For instance, Fuji Electric confirmed that over 80% of its vending machines installed in Japan support contactless payments.

Technological Advancements in Hardware and Software Integration

Advances in embedded systems, AI, IoT, and biometric authentication continue to enhance self-service technologies. Hardware units now come equipped with smart sensors, secure modules, and cloud connectivity. Software platforms offer real-time analytics, remote management, and AI-powered personalization. These integrations improve user experience, uptime, and data-driven decision-making. For instance, smart kiosks can adjust content based on customer demographics or behavior. Retailers use integrated systems for cross-selling, dynamic pricing, and loyalty program engagement. In BFSI and healthcare, enhanced software ensures compliance, fraud prevention, and data security. These developments attract enterprises aiming for automation, personalization, and improved customer engagement, thus accelerating market growth.

- For instance, Zebra Technologies deploys kiosks with embedded sensors and edge computing, supporting real-time inventory tracking across thousands of retail locations.

Cost Optimization and Operational Efficiency for Businesses

Self-service technologies offer businesses measurable cost benefits by automating repetitive customer-facing tasks. Retailers cut checkout times and reduce labor costs with self-checkout kiosks. Banks lower branch staffing needs by expanding ATM services. In QSRs, self-ordering kiosks help improve speed and reduce order errors. Maintenance is simplified through modular hardware and remote diagnostics. Businesses also gain real-time insights into usage patterns, inventory levels, and customer preferences. These efficiencies enhance service speed, reduce downtime, and improve ROI. The flexibility of deployment from compact kiosks to large-scale vending networks also enables businesses of all sizes to adopt self-service models, making them a key enabler of sustainable growth.

Key Trends & Opportunities

Integration of AI and Personalization Features

Artificial intelligence is transforming how self-service systems interact with users. AI-powered kiosks and vending machines use image recognition, voice interaction, and behavioral analytics to deliver tailored responses. In retail, machines can suggest products based on past purchases or demographics. In banking, AI enables fraud detection and smart navigation of services. Machine learning algorithms improve the adaptability of software, making interactions more intuitive. Personalized engagement increases customer satisfaction and loyalty. Businesses also leverage these tools for targeted promotions and data-driven insights. As AI becomes more affordable and accessible, its deeper integration into self-service platforms presents strong growth potential across verticals.

- For instance, NCR Voyix deploys AI-enabled retail kiosks using computer vision to recognize items and reduce checkout time to under 20 seconds per transaction in live retail pilots.

Expanding Use in Healthcare and Public Sector Services

The healthcare industry increasingly deploys self-service kiosks for patient check-ins, appointment scheduling, and health information access. These reduce administrative burden and enhance patient flow management. Hospitals use vending-style units to dispense medical products and supplies. Public sector services such as ID issuance, license renewals, and ticketing also benefit from kiosk-based automation. The shift supports higher service availability, shorter queues, and better allocation of manpower. In developing countries, government programs are leveraging these technologies to expand rural access to services. The growing digitalization of citizen services and healthcare delivery creates strong long-term opportunities for self-service solutions.

Key Challenges

High Initial Investment and Maintenance Costs

Despite long-term savings, the upfront cost of installing self-service machines—particularly advanced models with biometric or AI features—remains a barrier for many small to mid-sized enterprises. Costs include hardware purchase, software integration, network setup, training, and compliance. Additionally, machines in high-traffic areas face wear and tear, requiring frequent servicing or replacement of parts. Downtime from technical failures can lead to customer dissatisfaction and revenue loss. Businesses also bear the cost of periodic software upgrades and cybersecurity compliance. These factors can delay adoption in budget-sensitive sectors or in emerging markets with lower digital infrastructure readiness.

Security and Data Privacy Concerns

As self-service systems collect and process sensitive user data, including payment details and personal identifiers, they become potential targets for cyberattacks. A breach can expose customer data and damage brand trust. End-users are increasingly concerned about how their information is stored and used. Regulations such as GDPR and HIPAA demand strict data protection protocols, adding complexity to system design. For developers and operators, ensuring encryption, access control, and compliance increases costs and operational burdens. Failure to implement strong security measures can result in fines, reputational loss, and service disruptions, making cybersecurity a persistent challenge in this market.

Regional Analysis

North America

North America leads the self-service technologies market, holding over 35% of the global market share in 2024. High consumer preference for convenience and widespread adoption in retail, BFSI, and QSR sectors support dominance. The United States drives innovation with AI-enabled kiosks and cardless ATMs. Businesses invest heavily in automation to enhance customer experience and reduce labor costs. Strong digital infrastructure and early technology adoption further fuel growth. In Canada, rising deployment of healthcare kiosks and smart vending solutions continues to expand usage. The region’s focus on seamless, contactless services keeps demand consistently high across all sectors.

Europe

Europe holds around 27% of the global market share, driven by mature banking systems and strict regulatory compliance. Countries such as the UK, Germany, and France witness broad deployment of self-service terminals in transport, hospitality, and retail. Advanced contactless payment infrastructure and consumer openness to automation support growth. Retailers use kiosks to enable multilingual service and personalized offers. The healthcare sector adopts check-in kiosks for managing patient flows. Eco-friendly hardware adoption and energy-efficient machines align with sustainability mandates. Europe’s structured digital ecosystem and strong public-private tech collaborations continue to promote long-term market expansion.

Asia Pacific

Asia Pacific accounts for approximately 22% of the self-service technologies market in 2024 and is the fastest-growing region. Rising urbanization, increasing digital payment adoption, and expanding middle-class consumer base support growth. China and Japan lead in kiosk and vending machine deployment, while India sees rapid ATM and retail automation expansion. E-commerce growth drives demand for smart parcel lockers and self-pickup systems. Governments in Southeast Asia invest in smart city projects integrating public kiosks. Cost-effective hardware manufacturing in the region also aids local adoption. Regional enterprises adopt self-service solutions to reduce operational costs and reach underserved areas.

Latin America

Latin America holds nearly 8% of the global market share, with Brazil and Mexico leading regional demand. The retail and BFSI sectors drive adoption of self-service kiosks, ATMs, and vending machines to improve service accessibility. Growing interest in automation stems from labor cost challenges and the need to serve high-footfall areas efficiently. Mobile and digital banking services stimulate ATM modernization. Healthcare and public transport sectors show early signs of self-service integration. However, fragmented infrastructure and limited funding in rural areas slow adoption. Despite these constraints, rising digital literacy and mobile penetration create long-term market potential.

Middle East & Africa (MEA)

The MEA region captures about 6% of the global market share, with the UAE, Saudi Arabia, and South Africa driving demand. Smart city initiatives and digital transformation programs accelerate the deployment of kiosks and vending systems across public and commercial sectors. The BFSI sector invests in next-gen ATMs to enhance financial inclusion. Airports and hospitality hubs adopt interactive kiosks to streamline visitor services. Retailers implement self-checkout systems to improve operational efficiency. However, infrastructure gaps and high import costs of advanced hardware pose challenges in several African countries. Despite these, the region is showing steady adoption momentum.

Self-Service Technologies Market Segmentations:

By Component

- Hardware

- Software

- Services

By Type

- ATM

- Vending Machine

- Kiosks

- Others

By End Use

- Retail

- Quick Service Restaurant

- Hospitality

- Healthcare

- Corporate Offices

- Transportation

- BFSI

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The self-service technologies market features a competitive landscape marked by innovation, strategic partnerships, and product diversification. Leading players such as NCR Corporation, Diebold Nixdorf, Ingenico Group, and Elo Touch Solutions maintain strong market presence through robust hardware offerings and integrated software platforms. Companies focus on enhancing user experience with AI-powered interfaces, biometric authentication, and remote management tools. KIOSK Information Systems, Meridian Kiosks, and Olea Kiosks cater to niche demands with custom kiosk designs across sectors like retail, transportation, and healthcare. Emerging players such as Avanti Markets and Embross drive innovation in vending and check-in solutions, respectively. Strategic mergers, investments in R&D, and global expansion efforts shape competitive positioning. Vendors also emphasize compliance with data security and accessibility standards. As businesses prioritize automation, vendors compete on reliability, uptime, and service support, while addressing vertical-specific needs. The market remains moderately fragmented, with regional players competing alongside global giants for specialized deployments and long-term contracts.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In 2025, Diebold Nixdorf partnered with LOC Software, enabling LOC’s ThriVersA software to run natively on Diebold Nixdorf’s self-checkout and kiosk systems aimed at simplifying deployment and improving flexibility for retailers.

- In August 2025, Zebra acquired Elo Touch Solutions to expand its footprint in customer-facing self-service kiosks, POS terminals, and interactive touchscreen solutions across retail, hospitality, QSR, healthcare and industrial markets.

- In May 2025, Diebold Nixdorf launched a new retail-technology production line in North Canton, Ohio to build self-service kiosks and checkout systems for grocery, general merchandise, QSR (quick service restaurant), and convenience retailers in the U.S.

- In May 2023, Applova Inc., a Silicon Valley-based technology company announced a partnership with Samsung to launch a Self-service kiosk for restaurants. These kiosk offers contactless ordering and payment, helping restaurants streamline operations, increase sales, and boost profits.

Report Coverage

The research report offers an in-depth analysis based on Component, Type, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Businesses will increase investment in self-service kiosks to reduce labor costs and improve efficiency.

- AI and machine learning will enhance personalization and decision-making in kiosks and ATMs.

- Contactless technologies such as QR codes and facial recognition will become standard features.

- Healthcare and government sectors will expand deployment of self-check-in and information kiosks.

- Integration with cloud platforms will enable real-time monitoring and remote system updates.

- Retailers will adopt smart vending and self-checkout systems to optimize customer service.

- Voice-enabled interfaces will improve accessibility and ease of use for diverse users.

- Energy-efficient and modular hardware designs will gain traction across global markets.

- Emerging economies will see increased adoption driven by digital inclusion initiatives.

- Data privacy and cybersecurity will remain key priorities for vendors and end-users.