Market Overview:

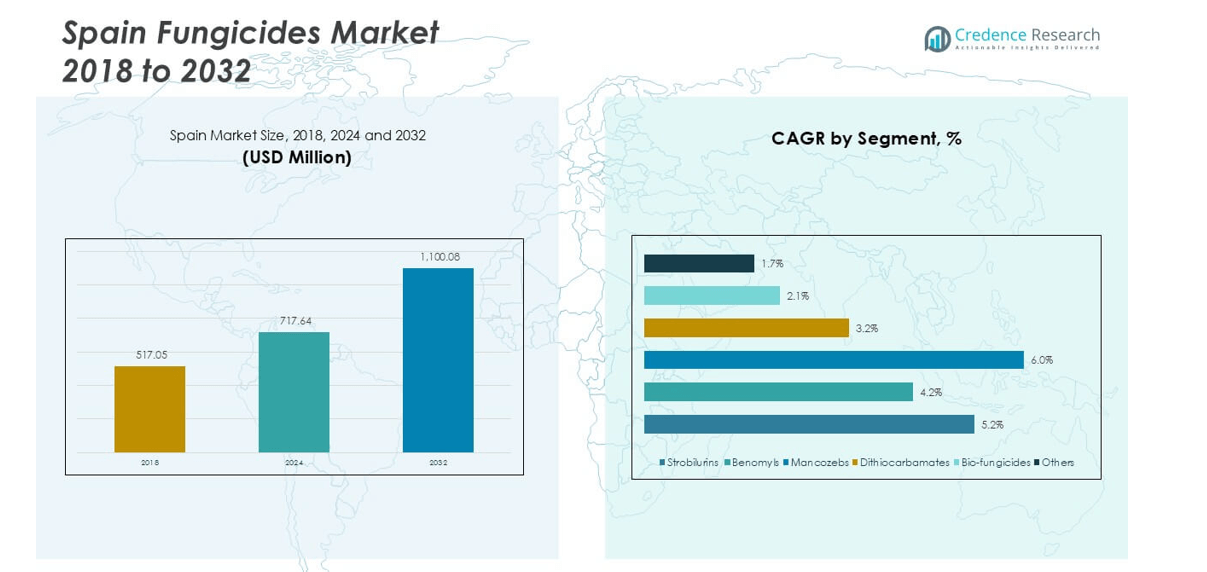

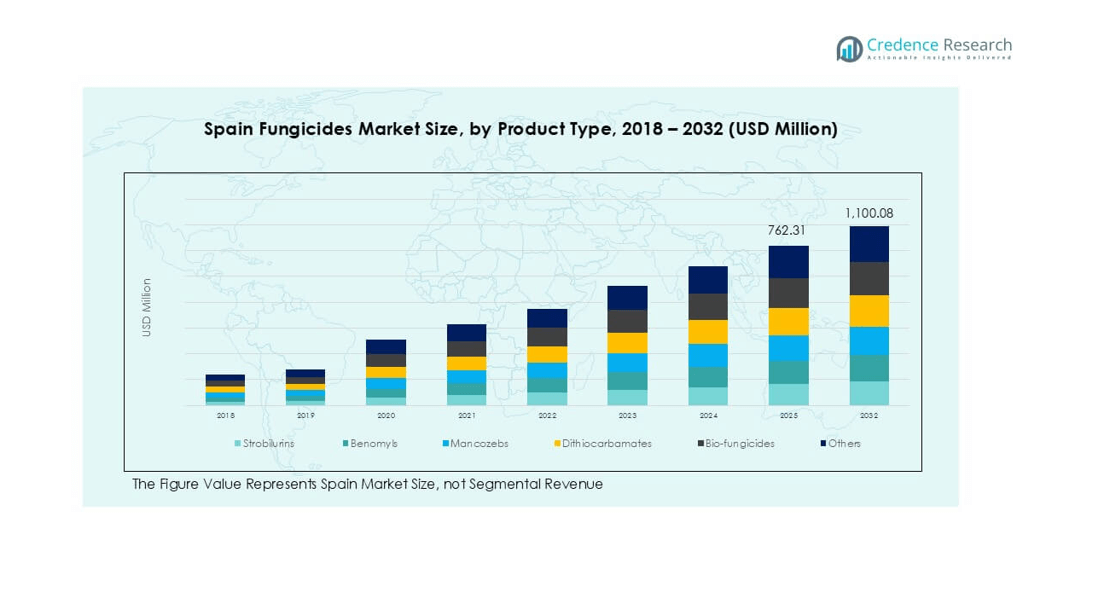

Spain Fungicides market size was valued at USD 517.05 million in 2018, grew to USD 717.64 million in 2024, and is anticipated to reach USD 1,100.08 million by 2032, at a CAGR of 5.38% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Spain Fungicides Market Size 2024 |

USD 717.64 million |

| Spain Fungicides Market, CAGR |

5.38% |

| Spain Fungicides Market Size 2032 |

USD 1,100.08 million |

The Spain fungicides market is led by major players such as Syngenta, Bayer CropScience, BASF SE, FMC Corporation, Dow AgroSciences, Adama, Nufarm, Sipcam Iberica, Atanor, and Indukern. These companies dominate through extensive product portfolios, innovation in bio-fungicides, and compliance with stringent EU regulations. Among regions, Southern Spain holds the largest share at 30%, driven by intensive fruit and vegetable cultivation for export markets. Northern Spain follows with 28%, supported by its strong viticulture sector, while Central Spain accounts for 24%, anchored by cereals and grains production. Eastern Spain contributes 18%, focusing on citrus, vegetables, and ornamentals. This regional distribution highlights the importance of horticulture and viticulture in shaping demand for fungicides across Spain.

Market Insights

- The Spain fungicides market was valued at USD 717.64 million in 2024 and is projected to reach USD 1,100.08 million by 2032, growing at a CAGR of 5.38%.

- Market growth is driven by expanding fruit and vegetable production, particularly tomatoes, peppers, citrus, and grapes, which face high fungal infection risks.

- A key trend is the rising adoption of bio-fungicides and sustainable solutions, supported by EU regulations encouraging low-residue products and integrated pest management practices.

- Competition involves global leaders like Syngenta, Bayer CropScience, BASF SE, and FMC, alongside regional players such as Sipcam Iberica and Indukern, focusing on tailored, cost-effective offerings.

- Regionally, Southern Spain dominates with 30% market share, followed by Northern Spain at 28%, Central Spain at 24%, and Eastern Spain at 18%. By product type, strobilurins lead the segment, while by application, fruits and vegetables hold the largest share due to high export demand.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

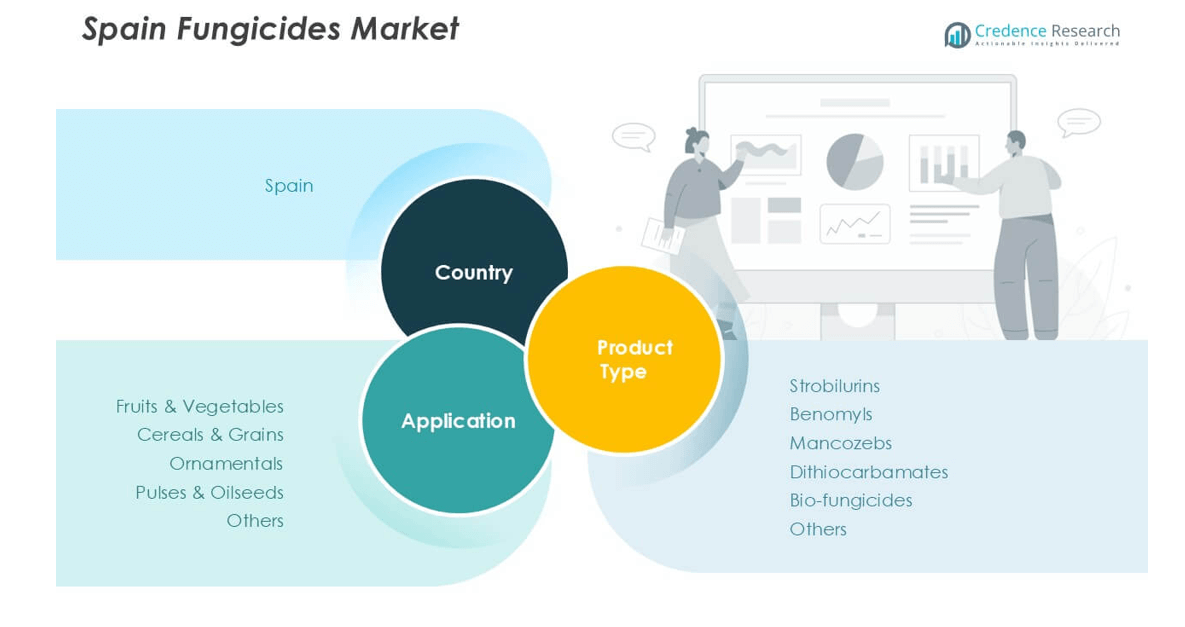

Market Segmentation Analysis:

By Product Type

The Spain fungicides market by product type is dominated by strobilurins, holding the largest share due to their broad-spectrum activity and effectiveness in controlling major fungal diseases across high-value crops. Their strong adoption stems from enhanced crop yield, resistance management benefits, and extended residual effect. Farmers prefer strobilurins in fruit and vegetable cultivation, which are vital segments in Spain’s agriculture. Demand is further supported by rising exports of horticultural produce and the need for sustainable crop protection solutions that maintain productivity under strict European Union residue regulations.

- For instance, Syngenta’s Amistar fungicide is a systemic, broad-spectrum fungicide used in Spanish agriculture to combat fungal diseases like early blight and powdery mildew in vegetables such as tomatoes and peppers.

By Application

Among applications, fruits and vegetables account for the largest market share, driven by Spain’s strong horticulture industry and its role as a leading exporter in Europe. High-value crops like tomatoes, peppers, citrus fruits, and grapes face persistent fungal threats, pushing farmers to rely on advanced fungicides for yield and quality assurance. The emphasis on export standards, coupled with rising domestic consumption, sustains demand for effective crop protection. Regulatory support for safer, low-residue solutions also accelerates adoption, ensuring fungicides remain central to protecting Spain’s fruit and vegetable sector.

- For instance, in 2022, Spanish apple orchards continued to address fungal diseases like apple scab and powdery mildew, which can affect export quality. Agrochemical products like ADAMA’s Custodia fungicide are known to treat these issues and are used in apple-growing regions, including Spain.

Market Overview

Expansion of Horticultural Production

Spain’s fungicides market benefits from the expansion of fruit and vegetable cultivation, which forms the backbone of its agricultural exports. Crops like grapes, citrus fruits, tomatoes, and peppers are highly vulnerable to fungal diseases, increasing the need for reliable protection solutions. Rising export demand within the European Union further accelerates adoption as farmers must ensure high-quality standards and consistent yields. This ongoing expansion drives significant demand for advanced fungicides that safeguard productivity and maintain Spain’s position as a key agricultural supplier.

- For instance, BASF, a major producer of crop protection products, offers Xemium-based fungicides in the Spanish market for use on cereals and horticultural crops. As part of its broader agricultural solutions, these products contribute to disease and resistance management, which are important aspects of crop productivity for Spanish farmers.

Adoption of Bio-Fungicides

The shift toward eco-friendly crop protection is a major growth driver in Spain. Farmers are adopting bio-fungicides to comply with strict EU regulations on chemical residues and environmental sustainability. These biological products are gaining traction in organic farming and integrated pest management systems, which are expanding across Spain’s agricultural landscape. Increasing consumer demand for safe, residue-free produce also supports adoption. This transition toward bio-based solutions enhances market opportunities, positioning bio-fungicides as a fast-growing sub-segment with long-term relevance in Spain’s fungicides industry.

- For instance, Certis Belchim introduced a bio-fungicide based on Aureobasidium pullulans in 2021, which was adopted across 8,000 hectares of Spanish vineyards to reduce reliance on synthetic fungicides.

Technological Advancements in Fungicide Formulations

Innovation in fungicide formulations, including improved active ingredients and resistance management solutions, drives market growth. Companies are focusing on multi-site action fungicides and advanced delivery systems to enhance efficacy while reducing application frequency. Such advancements support farmers in tackling resistant fungal strains, a growing concern in intensive agriculture. Modern formulations also align with sustainability goals, offering reduced environmental impact. The availability of these technologies in Spain helps farmers optimize crop protection strategies, reinforcing fungicides as essential inputs in both conventional and organic farming systems.

Key Trends and Opportunities

Rising Demand for Sustainable Crop Protection

A clear trend in Spain’s fungicides market is the growing demand for sustainable and low-residue solutions. Farmers face increasing regulatory pressure under EU policies to reduce chemical use and environmental impact. This creates strong opportunities for companies offering bio-fungicides, low-toxicity formulations, and integrated pest management systems. The focus on sustainability not only supports compliance but also strengthens Spain’s export competitiveness by aligning with international quality standards. This trend drives long-term opportunities for innovation in environmentally responsible fungicide products.

- For instance, Vivando SC, a BASF fungicide that uses the active ingredient metrafenone, is effective for controlling powdery mildew on crops like grapes and tomatoes. The product was introduced much earlier than 2022, with U.S. EPA approval for use on grapes dating back to at least December 2010.

Digital Farming and Precision Application

The integration of digital agriculture and precision spraying technologies is reshaping fungicide use in Spain. Farmers increasingly adopt data-driven tools such as sensors, drones, and GIS mapping to monitor crop health and apply fungicides more efficiently. These practices reduce wastage, minimize costs, and ensure targeted protection against fungal outbreaks. Precision application also aligns with sustainability objectives by lowering chemical footprints. The adoption of smart agriculture practices provides a strong growth opportunity for companies integrating digital tools with advanced fungicide offerings.

Key Challenges

Stringent EU Regulatory Framework

Spain’s fungicides market faces challenges from the European Union’s strict regulatory framework, which limits chemical residues and bans certain active ingredients. Compliance increases R&D costs and narrows the portfolio of chemical solutions available to farmers. While this encourages bio-fungicide adoption, it restricts flexibility in addressing fungal outbreaks, especially for high-value crops. Farmers often face higher costs in shifting to approved alternatives, while companies must continuously innovate to meet evolving regulatory standards. This dynamic remains a key challenge in sustaining growth.

Rising Fungal Resistance

The growing resistance of fungal pathogens to conventional fungicides poses a serious challenge in Spain. Intensive crop production and repeated application of single-mode action products accelerate resistance development, reducing effectiveness over time. Farmers face higher risks of crop losses and must invest in more complex resistance management strategies, which increase operational costs. The challenge of resistance underscores the urgent need for advanced formulations, rotational use of multiple fungicides, and adoption of integrated pest management to ensure long-term crop protection effectiveness.

Regional Analysis

Northern Spain

Northern Spain holds a 28% share of the fungicides market, driven by its strong vineyard and fruit-growing sectors. The region is renowned for grape cultivation, particularly in La Rioja and Navarra, where fungal diseases like powdery mildew and downy mildew pose significant threats. Farmers rely heavily on strobilurins and mancozebs to protect yield quality. Favorable climatic conditions for fungal proliferation increase fungicide demand throughout the year. Regulatory compliance and export-oriented viticulture further stimulate adoption of both chemical and bio-fungicides. Northern Spain remains a key consumer region, contributing steadily to the national fungicides market.

Central Spain

Central Spain accounts for 24% of the fungicides market, supported by large-scale cereal and grain cultivation across Castilla-La Mancha and Castilla y León. Fungal infections such as rusts and smuts are prevalent, necessitating extensive use of systemic fungicides. The dominance of cereals and pulses ensures strong demand for mancozebs and dithiocarbamates. Farmers are also adopting integrated pest management practices to meet sustainability goals, enhancing opportunities for bio-fungicides. Central Spain’s vast agricultural acreage and dependence on cereals for domestic consumption and exports sustain its important position in the national fungicide landscape.

Southern Spain

Southern Spain represents the 30% largest share of the fungicides market, reflecting its leadership in fruit and vegetable cultivation. Andalusia and Murcia are major production hubs for tomatoes, peppers, citrus fruits, and olives, all highly susceptible to fungal diseases. The region’s warm climate increases disease incidence, driving strong adoption of protective fungicides. Export commitments to European markets reinforce the need for high-quality, residue-compliant solutions. Both chemical fungicides and bio-fungicides see robust usage here, with rapid growth in sustainable formulations. Southern Spain’s agricultural diversity and export intensity secure its dominance within the national fungicides market.

Eastern Spain

Eastern Spain holds an 18% share of the fungicides market, anchored by high-value horticultural crops, particularly citrus, vegetables, and ornamentals grown in Valencia and Catalonia. The region’s mild Mediterranean climate fosters conditions favorable for fungal outbreaks, including molds and leaf spots. Growers depend on strobilurins, benomyls, and increasingly bio-fungicides to meet export requirements. Ornamental plant nurseries also drive niche demand for advanced formulations. Eastern Spain benefits from strong trade links to EU markets, where residue regulations encourage adoption of eco-friendly solutions. While smaller in scale compared to southern regions, it remains a key contributor to Spain’s fungicides market.

Market Segmentations:

By Product Type

- Strobilurins

- Benomyls

- Mancozebs

- Dithiocarbamates

- Bio-fungicides

- Others

By Application

- Fruits & Vegetables

- Cereals & Grains

- Ornamentals

- Pulses & Oilseeds

- Others

By Geography

- Northern Spain

- Central Spain

- Southern Spain

- Eastern Spain

Competitive Landscape

The competitive landscape of the Spain fungicides market is characterized by the presence of global leaders and strong regional players. Key companies include Syngenta, FMC Corporation, Dow AgroSciences, Adama, Bayer CropScience, Nufarm, BASF SE, Sipcam Iberica, Atanor, and Indukern. Multinational companies dominate through extensive product portfolios, advanced formulations, and investments in bio-fungicides to align with EU sustainability regulations. Local firms such as Sipcam Iberica and Indukern strengthen competition by offering region-specific solutions and cost-effective alternatives tailored to Spanish crops. Continuous innovation in resistance management, precision application technologies, and low-residue products shapes market dynamics. Strategic collaborations with distributors, expansion in organic solutions, and compliance with regulatory standards remain central to competitive strategies. Companies also prioritize R&D to develop multi-action fungicides and environmentally safe formulations, ensuring long-term growth. This blend of global expertise and regional specialization defines a highly competitive environment, where innovation and sustainability drive leadership in Spain’s fungicides market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Syngenta

- FMC Corporation

- Dow AgroSciences

- Adama

- Bayer CropScience

- Nufarm

- BASF SE

- Sipcam Iberica

- Atanor

- Indukern

Recent Developments

- In June 2024, BASF Agricultural Solutions announced the launch of Cevya, a new rice fungicide in China. This is the first isopropanol triazole fungicide approved for rice applications in two decades, designed to combat rice false smut and manage fungicide resistance. Cevya’s active ingredient, mefentrifluconazole, offers rice growers an innovative solution to enhance crop yields. BASF has conducted extensive field trials since 2020, collaborating with leading agricultural institutions to ensure its effectiveness and safety in disease management.

- In October 2023, “Bayer”, one of the well-known agriculture products companies based in the U.K., received approval from the Chemicals Regulation Division (CRD) for its new active substance to be used in fungicides. The new substance is isoflucypram, which will be used in its product called Vimoy.

- In August 2023, Bayer AG announced a significant investment of EUR 220 million in a new research and development facility at its Monheim site, marking its largest commitment to Crop Protection in Germany in 40 years. This state-of-the-art facility focuses on developing innovative fungicides and other chemicals that prioritize environmental and human safety.

- In September 2022, BASF, a well-known agriculture nutrition manufacturer, announced the launch of its all-new innovative fungicide product called Revylution, which received approval for use in New Zealand.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Spain fungicides market will continue steady growth supported by strong horticulture demand.

- Bio-fungicides will gain wider adoption due to EU sustainability regulations and organic farming expansion.

- Fruits and vegetables will remain the dominant application segment driving fungicide consumption.

- Strobilurins will maintain leadership in product type owing to broad-spectrum effectiveness.

- Resistance management strategies will push demand for multi-action and advanced formulations.

- Southern Spain will retain the largest regional share due to intensive fruit and vegetable production.

- Northern Spain will see stable demand growth led by the viticulture sector.

- Digital farming and precision spraying will optimize fungicide usage across all regions.

- Local companies will strengthen competitiveness with cost-effective and crop-specific solutions.

- Continuous R&D investment by global players will shape innovation in sustainable crop protection.