CHAPTER NO. 1 : GENESIS OF THE MARKET

1.1 Market Prelude – Introduction & Scope

1.2 The Big Picture – Objectives & Vision

1.3 Strategic Edge – Unique Value Proposition

1.4 Stakeholder Compass – Key Beneficiaries

CHAPTER NO. 2 : EXECUTIVE LENS

2.1 Pulse of the Industry – Market Snapshot

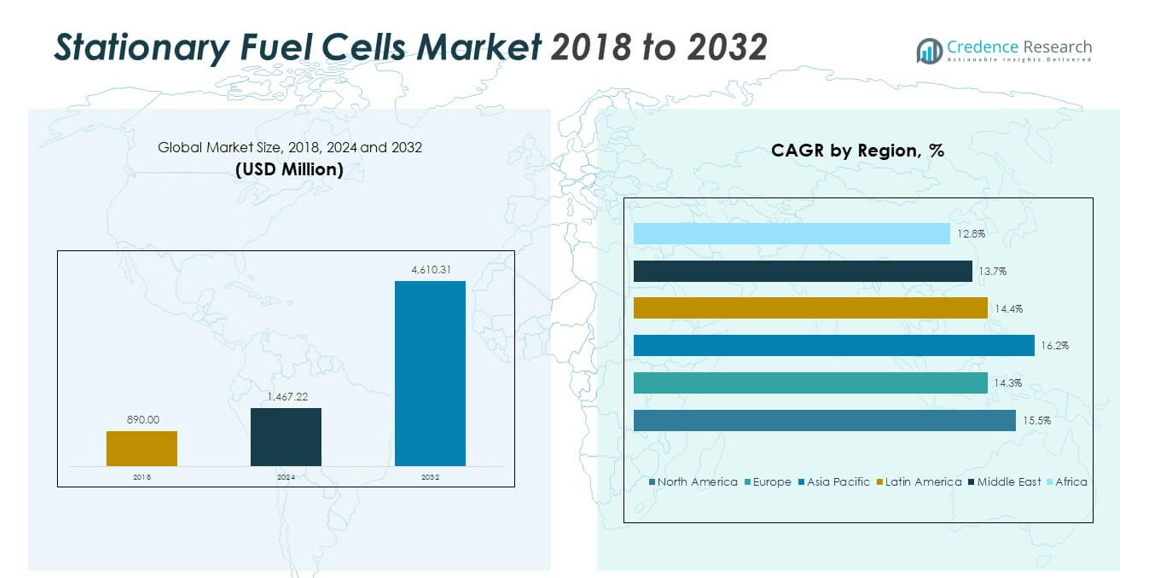

2.2 Growth Arc – Revenue Projections (USD Million)

2.3. Premium Insights – Based on Primary Interviews

CHAPTER NO. 3 : STATIONARY FUEL CELLS MARKET FORCES & INDUSTRY PULSE

3.1 Foundations of Change – Market Overview

3.2 Catalysts of Expansion – Key Market Drivers

3.2.1 Momentum Boosters – Growth Triggers

3.2.2 Innovation Fuel – Disruptive Technologies

3.3 Headwinds & Crosswinds – Market Restraints

3.3.1 Regulatory Tides – Compliance Challenges

3.3.2 Economic Frictions – Inflationary Pressures

3.4 Untapped Horizons – Growth Potential & Opportunities

3.5 Strategic Navigation – Industry Frameworks

3.5.1 Market Equilibrium – Porter’s Five Forces

3.5.2 Ecosystem Dynamics – Value Chain Analysis

3.5.3 Macro Forces – PESTEL Breakdown

3.6 Price Trend Analysis

3.6.1 Regional Price Trend

3.6.2 Price Trend by product

CHAPTER NO. 4 : KEY INVESTMENT EPICENTER

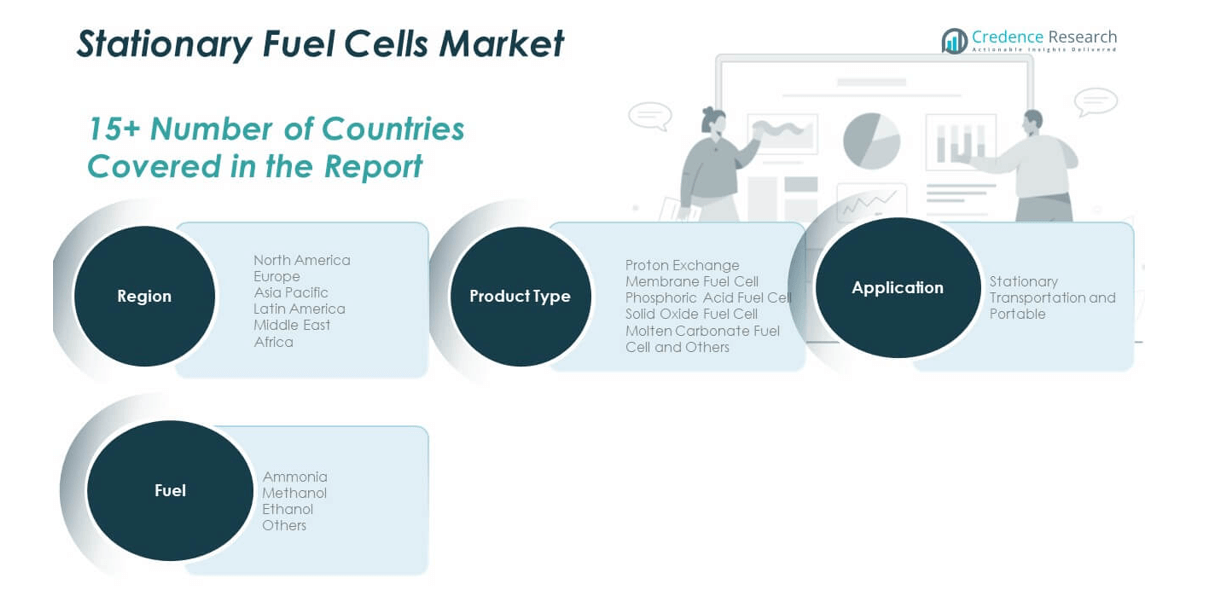

4.1 Regional Goldmines – High-Growth Geographies

4.2 Product Frontiers – Lucrative Product Categories

4.3 Application Sweet Spots – Emerging Demand Segments

CHAPTER NO. 5: REVENUE TRAJECTORY & WEALTH MAPPING

5.1 Momentum Metrics – Forecast & Growth Curves

5.2 Regional Revenue Footprint – Market Share Insights

5.3 Segmental Wealth Flow – Type & Application Revenue

CHAPTER NO. 6 : TRADE & COMMERCE ANALYSIS

6.1. Import Analysis by Region

6.1.1. Global Stationary Fuel Cells Market Import Revenue By Region

6.2. Export Analysis by Region

6.2.1. Global Stationary Fuel Cells Market Export Revenue By Region

CHAPTER NO. 7 : COMPETITION ANALYSIS

7.1. Company Market Share Analysis

7.1.1. Global Stationary Fuel Cells Market: Company Market Share

7.2. Global Stationary Fuel Cells Market Company Revenue Market Share

7.3. Strategic Developments

7.3.1. Acquisitions & Mergers

7.3.2. New Product Launch

7.3.3. Regional Expansion

7.4. Competitive Dashboard

7.5. Company Assessment Metrics, 2024

CHAPTER NO. 8 : STATIONARY FUEL CELLS MARKET – BY TYPE SEGMENT ANALYSIS

8.1. Stationary Fuel Cells Market Overview by Type Segment

8.1.1. Stationary Fuel Cells Market Revenue Share By Type

8.2. Proton Exchange Membrane Fuel Cell

8.3 Phosphoric Acid Fuel Cell

8.4. Solid Oxide Fuel Cell

8.5. Molten Carbonate Fuel Cell

8.6. Others

CHAPTER NO. 9 : STATIONARY FUEL CELLS MARKET – BY APPLICATION SEGMENT ANALYSIS

9.1. Stationary Fuel Cells Market Overview by Application Segment

9.1.1. Stationary Fuel Cells Market Revenue Share By Application

9.2. Stationary

9.3. Transportation and Portable

CHAPTER NO. 10 : STATIONARY FUEL CELLS MARKET – BY FUEL SEGMENT ANALYSIS

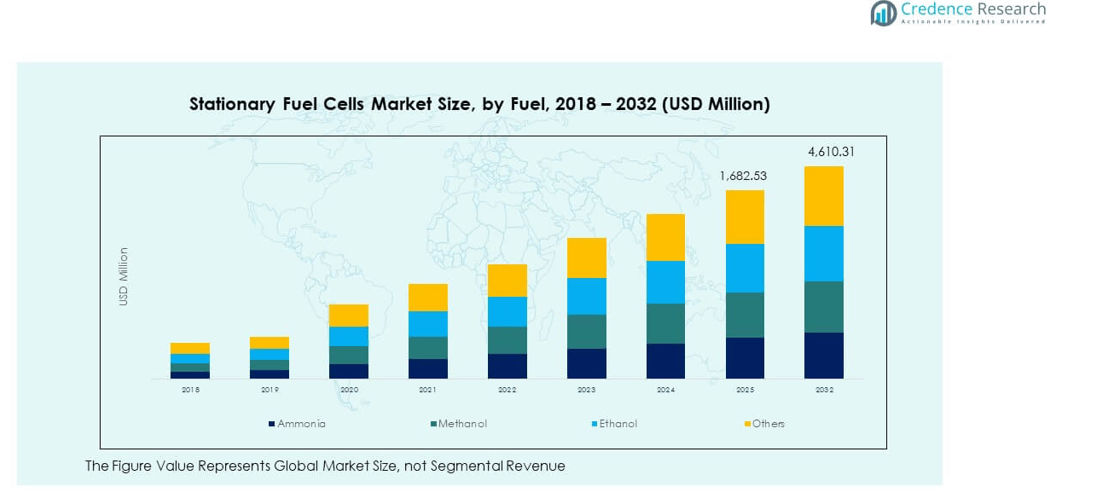

10.1. Stationary Fuel Cells Market Overview by Fuel Segment

10.1.1. Stationary Fuel Cells Market Revenue Share By Fuel

10.2. Ammonia

10.3. Methanol

10.4. Ethanol

10.5. Others

CHAPTER NO. 11 : STATIONARY FUEL CELLS MARKET – REGIONAL ANALYSIS

11.1. Stationary Fuel Cells Market Overview by Region Segment

11.1.1. Global Stationary Fuel Cells Market Revenue Share By Region

11.1.3. Regions

11.1.4. Global Stationary Fuel Cells Market Revenue By Region

.1.6. Type

11.1.7. Global Stationary Fuel Cells Market Revenue By Type

11.1.9. Application

11.1.10. Global Stationary Fuel Cells Market Revenue By Application

11.1.12. Fuel

11.1.13. Global Stationary Fuel Cells Market Revenue By Fuel

CHAPTER NO. 12 : NORTH AMERICA STATIONARY FUEL CELLS MARKET – COUNTRY ANALYSIS

12.1. North America Stationary Fuel Cells Market Overview by Country Segment

12.1.1. North America Stationary Fuel Cells Market Revenue Share By Region

12.2. North America

12.2.1. North America Stationary Fuel Cells Market Revenue By Country

12.2.2. Type

12.2.3. North America Stationary Fuel Cells Market Revenue By Type

12.2.4. Application

12.2.5. North America Stationary Fuel Cells Market Revenue By Application

2.2.6. Fuel

12.2.7. North America Stationary Fuel Cells Market Revenue By Fuel

2.3. U.S.

12.4. Canada

12.5. Mexico

CHAPTER NO. 13 : EUROPE STATIONARY FUEL CELLS MARKET – COUNTRY ANALYSIS

13.1. Europe Stationary Fuel Cells Market Overview by Country Segment

13.1.1. Europe Stationary Fuel Cells Market Revenue Share By Region

13.2. Europe

13.2.1. Europe Stationary Fuel Cells Market Revenue By Country

13.2.2. Type

13.2.3. Europe Stationary Fuel Cells Market Revenue By Type

13.2.4. Application

13.2.5. Europe Stationary Fuel Cells Market Revenue By Application

13.2.6. Fuel

13.2.7. Europe Stationary Fuel Cells Market Revenue By Fuel

13.3. UK

13.4. France

13.5. Germany

13.6. Italy

13.7. Spain

13.8. Russia

13.9. Rest of Europe

CHAPTER NO. 14 : ASIA PACIFIC STATIONARY FUEL CELLS MARKET – COUNTRY ANALYSIS

14.1. Asia Pacific Stationary Fuel Cells Market Overview by Country Segment

14.1.1. Asia Pacific Stationary Fuel Cells Market Revenue Share By Region

14.2. Asia Pacific

14.2.1. Asia Pacific Stationary Fuel Cells Market Revenue By Country

14.2.2. Type

14.2.3. Asia Pacific Stationary Fuel Cells Market Revenue By Type

14.2.4. Application

14.2.5. Asia Pacific Stationary Fuel Cells Market Revenue By Application

14.2.5. Fuel

14.2.7. Asia Pacific Stationary Fuel Cells Market Revenue By Fuel

14.3. China

14.4. Japan

14.5. South Korea

14.6. India

14.7. Australia

14.8. Southeast Asia

14.9. Rest of Asia Pacific

CHAPTER NO. 15 : LATIN AMERICA STATIONARY FUEL CELLS MARKET – COUNTRY ANALYSIS

15.1. Latin America Stationary Fuel Cells Market Overview by Country Segment

15.1.1. Latin America Stationary Fuel Cells Market Revenue Share By Region

15.2. Latin America

15.2.1. Latin America Stationary Fuel Cells Market Revenue By Country

15.2.2. Type

15.2.3. Latin America Stationary Fuel Cells Market Revenue By Type

15.2.4. Application

15.2.5. Latin America Stationary Fuel Cells Market Revenue By Application

15.2.6. Fuel

15.2.7. Latin America Stationary Fuel Cells Market Revenue By Fuel

15.3. Brazil

15.4. Argentina

15.5. Rest of Latin America

CHAPTER NO. 16 : MIDDLE EAST STATIONARY FUEL CELLS MARKET – COUNTRY ANALYSIS

16.1. Middle East Stationary Fuel Cells Market Overview by Country Segment

16.1.1. Middle East Stationary Fuel Cells Market Revenue Share By Region

16.2. Middle East

16.2.1. Middle East Stationary Fuel Cells Market Revenue By Country

16.2.2. Type

16.2.3. Middle East Stationary Fuel Cells Market Revenue By Type

16.2.4. Application

16.2.5. Middle East Stationary Fuel Cells Market Revenue By Application

16.2.6. Fuel

16.2.7. Middle East Stationary Fuel Cells Market Revenue By Fuel

16.3. GCC Countries

16.4. Israel

16.5. Turkey

16.6. Rest of Middle East

CHAPTER NO. 17 : AFRICA STATIONARY FUEL CELLS MARKET – COUNTRY ANALYSIS

17.1. Africa Stationary Fuel Cells Market Overview by Country Segment

17.1.1. Africa Stationary Fuel Cells Market Revenue Share By Region

17.2. Africa

17.2.1. Africa Stationary Fuel Cells Market Revenue By Country

17.2.2. Type

17.2.3. Africa Stationary Fuel Cells Market Revenue By Type

17.2.4. Application

17.2.5. Africa Stationary Fuel Cells Market Revenue By Application

17.2.6. Fuel

17.2.7. Africa Stationary Fuel Cells Market Revenue By Fuel

17.3. South Africa

17.4. Egypt

17.5. Rest of Africa

CHAPTER NO. 18 : COMPANY PROFILES

18.1. Horizon Fuel Cell Technologies (Singapore)

18.1.1. Company Overview

18.1.2. Product Portfolio

18.1.3. Financial Overview

18.1.4. Recent Developments

18.1.5. Growth Strategy

18.1.6. SWOT Analysis

18.2. Mitsubishi Heavy Industries (Japan)

18.3. ElringKlinger (Germany)

18.4. Hydrogenics (Canada)

18.5. SOLIDpower Italia (Italy)

18.6. Ceres Power (UK)

18.7. Ballard Power Systems (Canada)

18.8. AVL (Austria)

18.9. Bosch (Germany)

18.10. Pragma Industries (France)

18.11. W. L. Gore & Associates (US)

18.12. Nedstack Fuel Cell Technology (Netherlands)

18.13. Proton Motor Fuel Cell GmbH (Germany)

18.14. Bloom Energy (US)

18.15. ITM Power (UK)

18.16. Plug Power (US)

18.17. Nuvera Fuel Cells, LLC (US)