Steel Wire Market Overview:

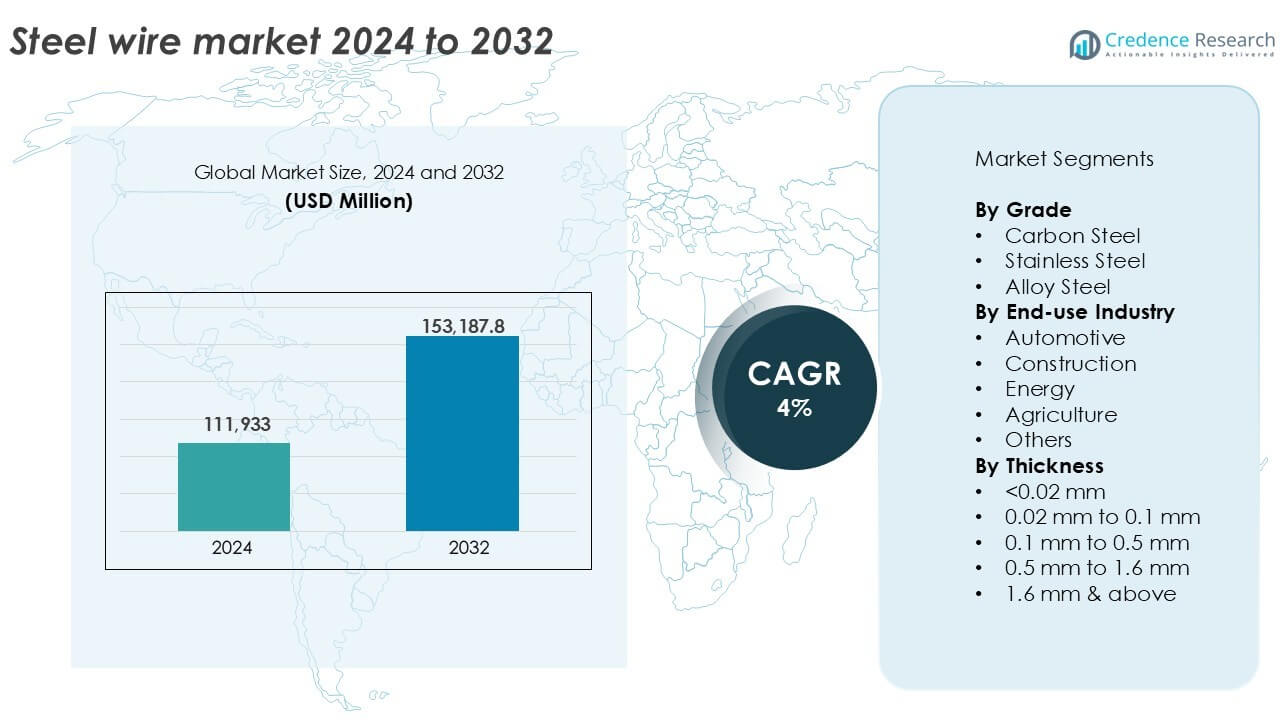

The steel wire market size was valued at USD 111,933 million in 2024 and is anticipated to reach USD 153,187.8 million by 2032, at a CAGR of 4% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Steel Wire Market Size 2024 |

USD 111,933 million |

| Steel Wire Market , CAGR |

4% |

| Steel Wire Market Size 2032 |

USD 153,187.8 million |

Steel Wire Market Insights

- Rising demand from automotive, construction, and energy sectors drives consistent steel wire consumption across industrial applications.

- Trends such as increased adoption of galvanized and coated steel wires, along with regional capacity expansion in Asia and Latin America, support market growth.

- Leading players like ArcelorMittal, Nippon Steel, and Bridon-Bekaert invest in product innovation and regional expansion to maintain competitive edge, while smaller players face challenges from raw material price volatility.

- Asia-Pacific dominates the market with over 45% share, followed by Europe at 22% and North America at 18%; by grade, carbon steel leads with over 50% market share, while 0.1 mm to 0.5 mm thickness wires account for the largest share among size segments due to wide industrial applications.

Market Segmentation Analysis:

By Grade

Carbon steel dominates the steel wire market by grade, accounting for over 50% of the total share in 2024. Its widespread use in construction, automotive, and general engineering is driven by high tensile strength, ductility, and cost-efficiency. Carbon steel wire finds applications in wire ropes, fencing, and fasteners. Stainless steel follows, favored for corrosion resistance in harsh environments such as marine and chemical processing. Alloy steel wire is used in niche applications requiring elevated heat or wear resistance, including aerospace and heavy machinery components, but holds a smaller market share due to higher costs.

- For instance, carbon steel wire is widely used in reinforced concrete and fencing applications globally, with the carbon steel segment holding over 60% of total market share in 2024.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By End-use Industry

The automotive industry leads the end-use segment, capturing more than 35% market share in 2024. Steel wire is essential in tire reinforcement, seat springs, clutch cables, and fasteners, driven by high vehicle production and aftermarket demand. Construction follows closely, using steel wire in concrete reinforcement, binding, and fencing. Energy sector applications include guy wires, grounding wire, and conductor core reinforcement. In agriculture, steel wire supports fencing, trellising, and machinery components. Other uses include packaging, industrial equipment, and household appliances, contributing to steady but smaller demand across miscellaneous sectors.

- For instance, global automotive manufacturing uses steel wire in tire bead reinforcement and springs across millions of vehicles annually, reflecting its core role in vehicle safety and durability.

By Thickness

Steel wire with a thickness range of 0.1 mm to 0.5 mm holds the largest market share, exceeding 30% in 2024. This segment caters to broad applications across automotive, electronics, and industrial machinery due to its balance of strength and flexibility. Wires under 0.02 mm serve precision industries like medical devices and microelectronics, while 0.02 mm to 0.1 mm wires are used in springs, mesh, and cables. The 0.5 mm to 1.6 mm range supports construction and fencing needs. Wires above 1.6 mm are used in heavy-duty applications, such as suspension bridges and crane cables.

Key Growth Drivers

Rising Demand from Automotive and Construction Industries

The steel wire market benefits significantly from the growing demand across automotive and construction sectors. In the automotive industry, steel wire is extensively used for tire reinforcement, seat springs, clutch cables, and fasteners. As global vehicle production increases, particularly in Asia-Pacific, steel wire consumption rises in parallel. Similarly, construction activities continue to expand due to rapid urbanization, infrastructure upgrades, and residential developments. Steel wire is widely used in binding, fencing, concrete reinforcement, and structural support. Emerging economies, including India, Vietnam, and Brazil, are witnessing strong construction growth supported by public and private investments. These trends sustain steady demand for medium-to-high strength wire grades and support the market’s long-term growth outlook.

- For instance, Bekaert supplied steel wire for approximately 750 to 800 million vehicle tires globally in 2023, supporting major OEM platforms.

Infrastructure Modernization and Power Grid Expansion

Ongoing upgrades to national infrastructure and power transmission networks continue to drive steel wire consumption. Governments are investing heavily in modernizing roads, bridges, railways, and utility grids, which demand large volumes of wire-based reinforcements, wire ropes, and conductors. In the power sector, steel-core aluminum conductors reinforced with steel wires are vital for overhead power lines. As renewable energy projects such as wind farms and solar parks expand, demand grows for tension cables and guy wires. Developed economies in North America and Europe are upgrading aging infrastructure, while Asian and African countries are rapidly building new networks. These initiatives ensure consistent demand for structural and utility-grade steel wires with high tensile properties.

- For instance, Prysmian Group, a global leader in the energy and telecom cable systems industry, employed more than 28,000 people worldwide in 2022 and reported record sales of over €16 billion driven by major high-voltage transmission projects like Germany’s SuedOstLink.

Growing Application in Industrial Equipment and Machinery

The expansion of industrial manufacturing and machinery sectors contributes to the increased demand for steel wire products. Steel wires are used in conveyor belts, fasteners, welding electrodes, springs, and wire meshes across machinery used in mining, textiles, packaging, and metalworking. Industrial automation and process efficiency improvements drive component miniaturization, which relies on precision steel wires. As global manufacturing hubs shift towards value-added production, the need for strong, flexible, and corrosion-resistant wire products rises. High-performance alloy and stainless steel wires gain traction in applications involving high temperatures, chemicals, or continuous mechanical stress. This industrial momentum plays a key role in boosting volume demand across diverse end-user categories.

Key Trends & Opportunities

Shift Toward High-Performance and Coated Steel Wires

A prominent trend in the steel wire market is the growing shift toward high-performance and coated steel wires. End-users increasingly demand wires with enhanced corrosion resistance, wear resistance, and longer life, especially in marine, construction, and infrastructure applications. Galvanized, zinc-aluminum alloy, epoxy-coated, and plastic-coated wires are gaining popularity due to their extended durability. This trend supports growth in value-added wire segments and promotes product differentiation among manufacturers. Coated steel wires are also favored in fencing, agriculture, and energy applications where environmental exposure is significant. Technological advances in surface treatment and wire drawing processes create new opportunities for innovation in customized wire grades that meet stricter quality standards.

- For instance, Bekaert operates a global network of advanced coating lines and sources approximately 2.5 to 2.8 million tonnes of steel wire rod annually for demanding applications, including energy transition, new mobility, and high-performance infrastructure.

Regional Expansion and Strategic Capacity Enhancements

Emerging markets in Southeast Asia, Latin America, and Africa present strong growth potential for steel wire producers. These regions are experiencing infrastructure development, construction booms, and rising automotive production. Global manufacturers are expanding operations or forming joint ventures in these regions to improve supply chain access and reduce transportation costs. Strategic capacity expansions, such as establishing new wire drawing plants or upgrading existing facilities, help meet localized demand and strengthen market presence. Regional government initiatives that support domestic steel production and infrastructure spending create favorable conditions for wire manufacturers. As localization becomes a strategic priority, companies that align production capabilities with regional demand trends stand to gain significantly.

Key Challenges

Volatility in Raw Material Prices

Fluctuations in the prices of raw materials such as steel billets, rods, and alloying elements pose a significant challenge for steel wire manufacturers. The global steel supply chain remains sensitive to changes in iron ore prices, energy costs, and trade dynamics. Disruptions caused by geopolitical tensions, environmental regulations, or supply shortages can lead to price spikes and reduced profit margins. Many manufacturers operate on fixed-term contracts, making it difficult to pass increased input costs to end-users. This price instability affects production planning, inventory control, and long-term investment decisions. Companies must implement strategic sourcing and maintain efficient cost structures to navigate raw material volatility.

Environmental Regulations and Emission Compliance

The steel wire industry faces increasing pressure to comply with environmental regulations targeting carbon emissions, energy use, and waste management. Steel production is energy-intensive, and downstream processes like wire drawing, coating, and annealing contribute to the carbon footprint. Regulatory bodies in Europe, North America, and China have implemented strict emission norms and sustainability reporting standards. Manufacturers must invest in cleaner production technologies, energy-efficient machinery, and closed-loop water systems to meet these standards. Smaller firms may struggle with the capital requirements of these upgrades. Compliance costs and certification efforts also strain operational budgets, especially in price-sensitive markets, limiting the agility of some market participants.

Regional Analysis

Asia-Pacific

Asia-Pacific dominates the global steel wire market with over 45% share in 2024, driven by strong demand from China, India, Japan, and Southeast Asia. Rapid urbanization, industrialization, and expanding automotive and construction sectors fuel consumption. China leads regional output with extensive manufacturing capabilities and domestic demand. India sees rising usage across infrastructure and agriculture. Governments in Indonesia, Vietnam, and the Philippines support construction and industrial growth, increasing wire demand. Regional steel producers benefit from competitive production costs and favorable trade terms. Ongoing investments in grid modernization, highways, and transport networks ensure sustained market expansion across Asia-Pacific economies.

Europe

Europe holds nearly 22% of the steel wire market in 2024, led by Germany, Italy, and France. The region’s advanced manufacturing base and strong automotive presence drive consistent wire demand. Steel wire is used in construction reinforcements, cable systems, and industrial machinery. Demand for stainless and alloy steel wires is high due to stringent quality and durability standards. The EU’s green energy goals support growth in wind energy applications, where tension cables and structural wires are vital. However, strict environmental regulations and energy cost fluctuations challenge producers. Investment in R&D and coated wire innovation enhances competitive positioning.

North America

North America accounts for around 18% of the steel wire market share in 2024, supported by stable construction, automotive, and energy sector demand. The U.S. leads regional consumption, with steel wire widely used in power infrastructure, roadways, and oil & gas equipment. Mexico and Canada contribute through automotive manufacturing and agriculture. Demand for galvanized and high-tensile wires remains strong. The region emphasizes infrastructure renewal, reinforcing wire usage across bridge and utility projects. Sustainability regulations and reshoring of manufacturing provide new opportunities for local suppliers. Advanced processing facilities and high product standards sustain competitive regional output.

Latin America

Latin America holds close to 8% share in the global steel wire market, driven by Brazil, Argentina, and Chile. The region shows steady demand across construction, mining, and agricultural sectors. Brazil dominates consumption with expanding infrastructure and industrial activity. Steel wire is used in fencing, rebar supports, and power line reinforcements. Growth in commercial construction and energy grid projects supports demand. However, political uncertainty and currency fluctuations affect investment cycles. Despite challenges, improving trade frameworks and regional production capacity upgrades open long-term growth opportunities. Domestic manufacturing expansion reduces import reliance and supports localized supply chain resilience.

Middle East & Africa (MEA)

The Middle East & Africa represent about 7% of the global steel wire market in 2024. GCC countries drive regional demand through infrastructure megaprojects, real estate, and energy developments. The UAE and Saudi Arabia lead consumption, using steel wire in high-rise buildings, utility grids, and industrial zones. In Africa, South Africa and Egypt support growth through mining, agriculture, and power sector expansion. Rising urbanization and population growth create long-term demand drivers. However, limited domestic steel production in several countries increases import dependency. Governments focus on diversifying economies and improving manufacturing bases to support steel wire demand in emerging sectors.

Steel Wire Market Segmentations:

By Grade

- Carbon Steel

- Stainless Steel

- Alloy Steel

By End-use Industry

- Automotive

- Construction

- Energy

- Agriculture

- Others

By Thickness

- <0.02 mm

- 0.02 mm to 0.1 mm

- 0.1 mm to 0.5 mm

- 0.5 mm to 1.6 mm

- 1.6 mm & above

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the steel wire market is fragmented, with global and regional players competing on product quality, pricing, and supply capabilities. Leading companies such as ArcelorMittal S.A., Bridon-Bekaert Ropes Group, and Nippon Steel Corporation maintain strong positions through integrated production, diversified product portfolios, and long-term customer relationships. U.S.-based players like WireCo WorldGroup Inc. and Heico Companies’ Metal Processing Group focus on specialized wire solutions for industrial and energy sectors. Asian producers including HBIS GROUP, SHAGANG GROUP Inc., and KOBE STEEL, LTD. leverage scale and cost efficiency to strengthen export competitiveness. Companies continuously invest in coated and high-performance wires to meet evolving end-user demands in construction, automotive, and energy applications. Strategic capacity expansions, acquisitions, and joint ventures enhance market penetration in emerging regions. With growing emphasis on low-emission manufacturing and quality certifications, innovation and compliance have become key differentiators. The market remains moderately consolidated at the top, with intense competition among mid-sized and regional firms.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Bridon-Bekaert Ropes Group (Belgium)

- WireCo WorldGroup Inc. (U.S.)

- GRUPPO PITTINI S.p.A. (Italy)

- Nippon Steel Corporation (Japan)

- SHAGANG GROUP Inc. (China)

- Optimus Steel (U.S.)

- JFE Steel Corporation (Japan)

- Insteel Industries (U.S.)

- KOBE STEEL, LTD. (Japan)

- HBIS GROUP (China)

- ArcelorMittal S.A. (Luxembourg)

- Heico Companies’ Metal Processing Group (U.S.)

- Byelorussian Steel Works (Belarus)

Recent Developments

- In January 2025, China Steel Corporation (CSC) launched a new initiative to produce low-carbon wire rods aimed at enhancing export competitiveness. The wire rods, made from 1018 and 1022 materials with sizes ranging from 5.5mm to 8mm, are primarily commercial-quality low-carbon steel sourced from CSC’s blast furnace. Still, customers can also opt for wire rods from Dragon Steel’s electric furnace under the same pricing terms.

- In July 2023, KOBE Steel announced that its Kobenable Steel, a low-CO2 blast furnace steel product, has opted for special steel wire rods in automobiles in Japan for the first time.

- In March 2023, Systematic Group, one of the leading GI wire manufacturers in India has acquired a new manufacturing unit in Kolkata to expand their operations and introduce wires made from Green Steel in the country. This development has the helped the company to cater to the Eastern market region.

Report Coverage

The research report offers an in-depth analysis based on Grade, End-use Industry, Thickness and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for steel wire will grow steadily with rising infrastructure and construction investments worldwide.

- Automotive sector will remain a major consumer, driven by increasing vehicle production and component needs.

- Asia-Pacific will continue to lead global demand, supported by manufacturing expansion and urban development.

- Adoption of coated and high-performance wires will increase across marine, energy, and industrial applications.

- Renewable energy projects will boost demand for structural and tension wire components.

- Manufacturers will focus on enhancing corrosion resistance and product durability through advanced processing.

- Environmental regulations will drive innovation in energy-efficient and low-emission production technologies.

- Strategic mergers and capacity expansions will shape competitive dynamics among global and regional players.

- Digitization and automation in manufacturing will improve quality control and production efficiency.

- Supply chain localization in emerging markets will create new growth opportunities for regional producers.