Market Overview:

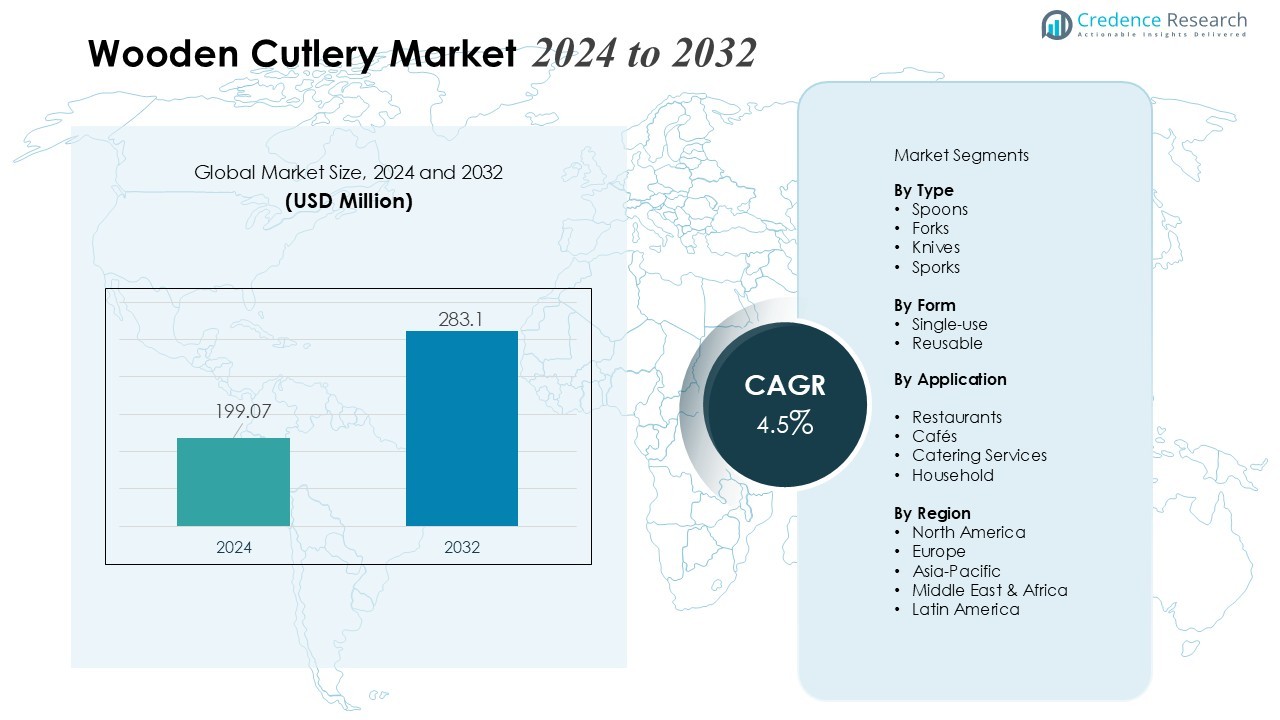

The Wooden Cutlery Market size was valued at USD 199.07 million in 2024 and is anticipated to reach USD 283.1 million by 2032, at a CAGR of 4.5% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Wooden Cutlery Market Size 2024 |

USD 199.07 Million |

| Wooden Cutlery Market, CAGR |

4.5% |

| Wooden Cutlery Market Size 2032 |

USD 283.1 Million |

Market growth is being driven by rising environmental awareness and increasing regulatory pressure against single-use plastics. Many foodservice operators, including quick‑service restaurants, cafes, and catering services, are shifting toward biodegradable and compostable cutlery. Improved manufacturing processes also enhance the durability and finish of wooden cutlery, making it a viable alternative to plastic while aligning with consumer demand for sustainable lifestyle choices.

Regionally, the market sees robust adoption across multiple geographies. North America and Europe remain significant players due to stricter regulations on plastic use and high consumer eco‑consciousness. Meanwhile, the Asia‑Pacific region — including rapidly urbanizing and populous countries — is witnessing accelerated uptake owing to expanding foodservice infrastructure and rising consumer awareness about sustainable living.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Wooden Cutlery Market was valued at USD 199.07 million in 2024 and is projected to reach USD 283.1 million by 2032, registering a CAGR of 4.5% during the forecast period. Growth is driven by environmental awareness and regulatory pressures against single-use plastics.

- Heightened consumer and business focus on sustainability encourages a shift from plastic to biodegradable wooden cutlery, reducing ecological footprint and supporting waste reduction initiatives.

- Restaurants, cafés, quick service outlets, and catering services form the primary demand base, with operators adopting wooden utensils to meet eco-conscious dining expectations and sustainability goals.

- Consumers increasingly prefer natural, chemical-free, and renewable materials, reinforcing wooden cutlery’s appeal over plastic and metal alternatives and aligning with eco-conscious lifestyles.

- Manufacturing innovations improve durability, finish quality, and design of wooden cutlery, addressing previous reliability concerns while enhancing consumer satisfaction and repeat usage.

- High production costs and dependence on sustainable timber remain key challenges, as raw material availability, pricing fluctuations, and deforestation regulations impact consistent supply and quality.

- North America leads with 34 % of global demand, Europe contributes 21 %, and Asia-Pacific along with emerging regions hold 45 %, with Asia-Pacific showing the fastest growth due to urbanization, foodservice expansion, and rising consumer awareness.

Market Drivers:

Market Drivers:

Growing Environmental Awareness and Plastic‑Waste Reduction

The Wooden Cutlery Market benefits substantially from heightened environmental awareness and increasing public concern about plastic pollution. Consumers and businesses increasingly reject single‑use plastic cutlery in favour of wood‑based alternatives that offer biodegradability and a lower ecological footprint. This shift toward environmentally friendly dining products drives demand steadily upward, especially among those valuing sustainability and waste reduction.

- For instance, Green Science Alliance developed a natural biomass material from paper waste, wood, plants, and scrap trees in 2019, enabling complete biodegradability in 180 days under composting conditions

Demand from Foodservice and Hospitality Sectors

Restaurants, cafés, quick‑service outlets, catering services, and other food‑service establishments represent a major demand base for wooden cutlery. Many operators adopt wood‑based utensils to align with their sustainability commitments and satisfy consumer expectations for eco‑friendly dining. Rising consumer preference for sustainable packaging and dining experiences encourages food‑service businesses to replace plastic cutlery with wooden alternatives.

- For instance, McDonald’s replaced plastic cutlery with paper-based variants in all its UK and Ireland restaurants during late 2022 and early 2023. This strategic transition, which was part of their ‘Plan for Change’ sustainability goals, is expected to eliminate approximately 858 metric tonnes of plastic each year from their system in that region alone.

Preference for Natural Materials and Lifestyle Alignment

Consumers increasingly favour products made from natural, chemical‑free, and renewable materials. Wood, bamboo, or similar sustainable resources provide an organic and “authentic” dining experience that resonates with those embracing natural or eco‑conscious lifestyles. This preference strengthens the appeal of wooden cutlery over conventional plastic or metal alternatives.

Innovation in Manufacturing, Quality, and Supply‑Chain Reach

Manufacturers continue to improve design, durability, and finish quality of wooden utensils, addressing earlier concerns about reliability and user experience. Advances in production and finishing processes make wooden cutlery more durable and appealing. Simultaneously, expansion of distribution channels — including online retail and direct-to-consumer sales — enables broader market penetration beyond institutional buyers. This combination of better product quality and easier accessibility supports market expansion.

Market Trends:

Rising Demand for Sustainable and Eco-Friendly Foodservice Solutions

The Wooden Cutlery Market is witnessing strong growth driven by increasing consumer preference for sustainable and biodegradable alternatives to plastic utensils. Regulatory initiatives promoting single-use plastic bans across North America, Europe, and Asia-Pacific have accelerated the adoption of wooden cutlery in restaurants, catering services, and household applications. It benefits from the growing awareness of environmental pollution and the demand for products that reduce carbon footprint. Manufacturers are focusing on offering premium-quality wooden utensils that combine durability with aesthetic appeal. Rising investments in research and development aim to improve product strength, water resistance, and cost efficiency. Partnerships with foodservice providers and e-commerce platforms are expanding distribution channels and enhancing market reach. Consumer trends indicate a shift toward eco-conscious dining experiences, reinforcing long-term demand for wooden cutlery.

- For instance, Huhtamaki’s BioWare line achieving 100% compostability under EN 13432 standards with over 90 days degradation in industrial facilities.

Technological Advancements and Strategic Market Expansion

Technological improvements in manufacturing processes have lowered production costs while ensuring high-quality, hygienic, and uniform wooden cutlery. Automation and precision cutting techniques have enhanced efficiency, allowing manufacturers to meet rising global demand without compromising on quality. It also benefits from innovative designs tailored to premium dining, casual catering, and takeaway services, increasing its adoption across diverse segments. Strategic collaborations, mergers, and acquisitions among key players support market expansion in emerging economies with growing foodservice sectors. Market players increasingly invest in sustainable sourcing of raw materials to maintain environmental compliance and brand credibility. Rising awareness of health and hygiene standards further drives the preference for wooden cutlery over plastic alternatives. Overall, these factors strengthen the market’s growth trajectory while positioning it as a critical solution in sustainable foodservice.

- For Instance, SSHL Machinery’s automated cutlery production lines use components such as servo feeders and hydraulic presses to optimize manufacturing efficiency, significantly reducing the number of operators required per shift and thereby decreasing overall labor costs.

Market Challenges Analysis:

High Production Costs and Raw Material Dependence

The Wooden Cutlery Market faces challenges due to the higher production costs compared to conventional plastic alternatives. It relies heavily on sustainable timber, which can be affected by seasonal availability, deforestation regulations, and fluctuating raw material prices. Maintaining consistent quality while sourcing eco-friendly wood adds pressure on manufacturers to optimize supply chains. Smaller producers may struggle to compete with established brands that benefit from economies of scale. Limited availability of certified sustainable wood in certain regions further restricts expansion. Market players must invest in efficient manufacturing techniques and material management to remain competitive.

Product Durability and Market Acceptance Constraints

Wooden cutlery often faces skepticism regarding durability and performance, particularly for hot or heavy meals. It can warp or break under specific conditions, affecting user experience and repeat purchases. Consumer preference for reusable or more robust alternatives, such as metal or bamboo, limits widespread adoption in some segments. It also faces logistical challenges in packaging and transportation to prevent damage. Educating end-users about product benefits and improving product design are critical to overcoming these hurdles. Market growth depends on addressing these durability concerns while maintaining eco-friendly attributes.

Market Opportunities:

Expansion in Eco-Conscious Foodservice and Retail Sectors

The Wooden Cutlery Market presents significant opportunities driven by the rising adoption of sustainable practices in the foodservice and retail industries. It benefits from increasing demand among restaurants, cafes, and catering services seeking eco-friendly alternatives to single-use plastic. Rising consumer awareness about environmental impact encourages retailers to stock biodegradable utensils, expanding market reach. Collaborations with e-commerce platforms enable broader distribution and direct access to environmentally conscious buyers. Innovation in product design, including premium and customizable cutlery, enhances appeal for high-end dining and corporate events. Government incentives promoting sustainable materials further stimulate adoption across diverse sectors.

Technological Innovations and Emerging Regional Markets

Technological advancements in automated manufacturing and wood treatment techniques offer opportunities to produce stronger, cost-effective, and water-resistant cutlery. It can cater to diverse consumer needs, including durable options for hot meals and large-scale catering. Emerging economies in Asia-Pacific and Latin America, with growing foodservice sectors and environmental regulations, provide untapped growth potential. Investment in sustainable sourcing and certification strengthens brand credibility and consumer trust. Expanding educational campaigns on environmental benefits supports wider market penetration. These factors position wooden cutlery as a viable and scalable solution in global sustainable foodservice markets.

Market Segmentation Analysis:

By Type

The Wooden Cutlery Market is primarily segmented into spoons, forks, knives, and sporks. Spoons and forks hold the largest share due to their frequent use in quick-service restaurants, catering, and household dining. Knives are gaining traction in premium and takeaway foodservice segments where cutting capability and durability are critical. Sporks serve niche segments combining multiple functionalities and appeal to convenience-focused consumers. It benefits from consistent demand across both individual and bulk purchases in foodservice channels. Product innovation in ergonomics and finish enhances usability, supporting wider adoption.

- For Instance, Driven by demand in quick-service restaurants and catering sectors, companies like Eco-Products are prominent suppliers in the rapidly growing market for wooden and compostable cutlery.

By Form

The market divides into single-use and reusable wooden cutlery. Single-use wooden utensils dominate due to regulatory restrictions on plastics and their widespread application in catering, fast-food, and event services. Reusable forms are emerging in premium dining, eco-conscious households, and corporate environments where sustainability and long-term use are priorities. It achieves increased acceptance through improvements in durability, water resistance, and finish quality. Expanding retail and e-commerce distribution channels further drive adoption of both forms, offering consumers flexibility in usage and purchase.

- For Instance,Huhtamaki’s sustainable product offerings include a ‘Future Friendly’ range of plain, compostable wooden cutlery made from responsibly sourced timber, providing a functional and eco-friendly alternative to single-use plastics.

By Application

Applications include restaurants, cafés, catering services, and household consumption. Foodservice establishments represent the largest segment due to regulatory pressures and consumer demand for sustainable dining solutions. Household usage grows steadily, driven by awareness of environmental impact and lifestyle preferences for natural materials. It supports market expansion through continuous product innovation, premium designs, and targeted distribution. Growing interest in eco-friendly events, takeaway meals, and institutional catering strengthens the demand across all application segments.

Segmentations:

By Type

- Spoons

- Forks

- Knives

- Sporks

By Form

By Application

- Restaurants

- Cafés

- Catering Services

- Household

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America – Clear Leadership with 34 % Share

North America holds 34 % of the global wooden cutlery demand. Strong enforcement of plastic-use restrictions and established foodservice and hospitality sectors support heavy adoption of wooden cutlery across restaurants, catering, and retail. High consumer spending capacity and sustainability awareness drive consistent use in both institutional and household segments. Well-developed supply chains and distribution networks ensure reliable product availability. This foundation helps maintain the region’s leadership in the global market.

Europe – Significant Contribution with 21 % Share

Europe accounts for 21 % of the global wooden cutlery market. Environmental regulations limiting single-use plastics, combined with widespread consumer preference for compostable products, push demand for wood-based cutlery in restaurants, cafés, public institutions, and retail. Demand remains stable across major markets such as Germany, France, and the United Kingdom. Certified sourcing and sustainable-wood supply chains reinforce confidence among buyers and regulators. This stability underpins Europe’s firm position in the global market.

Asia‑Pacific & Other Regions – Combined Share 45 %, Asia‑Pacific Leading Growth

Asia‑Pacific, together with other emerging regions including Latin America, Middle East, and Africa, constitutes the remaining 45 % share of the global market. Asia‑Pacific shows the fastest growth trajectory driven by rising urbanization, expanding foodservice industry, growing environmental awareness, and increasing demand for sustainable disposables in countries such as India, China, and Japan. Local manufacturing capabilities and access to raw-material sources help reduce costs and support broad deployment. Demand from institutional catering, food delivery, and retail segments in emerging economies positions this region as a key growth engine for the market.

Key Player Analysis:

- Bio Futura

- Biopac

- Caoxian Luyi Wooden

- Chefast kitchen accessories

- Ecoriti

- Greenwood (Dalian) Industrial

- Huhtamaki Group Oyj

- Leafware

- Mede Cutlery Company

- Natural Tableware

- Packnwood (First Pack)

- Pappco Greenware

- Vegware

- VerTerra Dinnerware

Competitive Analysis:

The Wooden Cutlery Market is highly competitive, with numerous global and regional players striving to expand their presence through product innovation, sustainable sourcing, and strategic partnerships. Leading manufacturers focus on improving durability, finish, and design quality to differentiate their offerings and meet growing consumer demand for eco-friendly alternatives. It benefits from collaborations with foodservice chains, retail distributors, and e-commerce platforms to enhance market penetration. Companies increasingly invest in automated production technologies and certified sustainable raw materials to optimize costs and ensure consistent supply. Pricing strategies, brand reputation, and compliance with environmental regulations play a crucial role in maintaining competitiveness. Emerging players leverage regional manufacturing advantages and niche product designs to capture local demand, particularly in high-growth regions like Asia-Pacific. Continuous focus on sustainability, product quality, and distribution efficiency drives market positioning and long-term growth opportunities.

Recent Developments:

- In September 2025, BioFuture hosted the BioFuture™ 2025 conference in New York City from October 13–15, focusing on innovation, policy, and investment in the biopharma sector, with a virtual partnering component following October 21–23.

- In February 2024, Vegware announced expansion of its compostable catering disposables range, including new bagasse products, to meet growing demand in the UK market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage:

The research report offers an in-depth analysis based on Type, Form, Application and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and ITALY economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Wooden Cutlery Market will continue to expand due to rising consumer preference for sustainable and biodegradable products.

- Increasing regulatory restrictions on single-use plastics globally will drive higher adoption across foodservice and retail sectors.

- Manufacturers will focus on improving product durability, water resistance, and finish to enhance user experience and acceptance.

- Growth in quick-service restaurants, cafés, and catering services will sustain consistent demand for wooden cutlery.

- E-commerce platforms and direct-to-consumer channels will play a critical role in increasing accessibility and market reach.

- Technological advancements in automated production and efficient supply chain management will reduce costs and improve scalability.

- Rising environmental awareness among households will expand adoption beyond institutional and commercial segments.

- Emerging markets in Asia-Pacific, Latin America, and Middle East will present significant growth opportunities due to urbanization and expanding foodservice infrastructure.

- Manufacturers will increasingly invest in certified sustainable raw materials to strengthen brand credibility and comply with environmental standards.

- Innovation in premium and customized wooden cutlery designs will attract niche segments and reinforce long-term market sustainability.