Market Overview

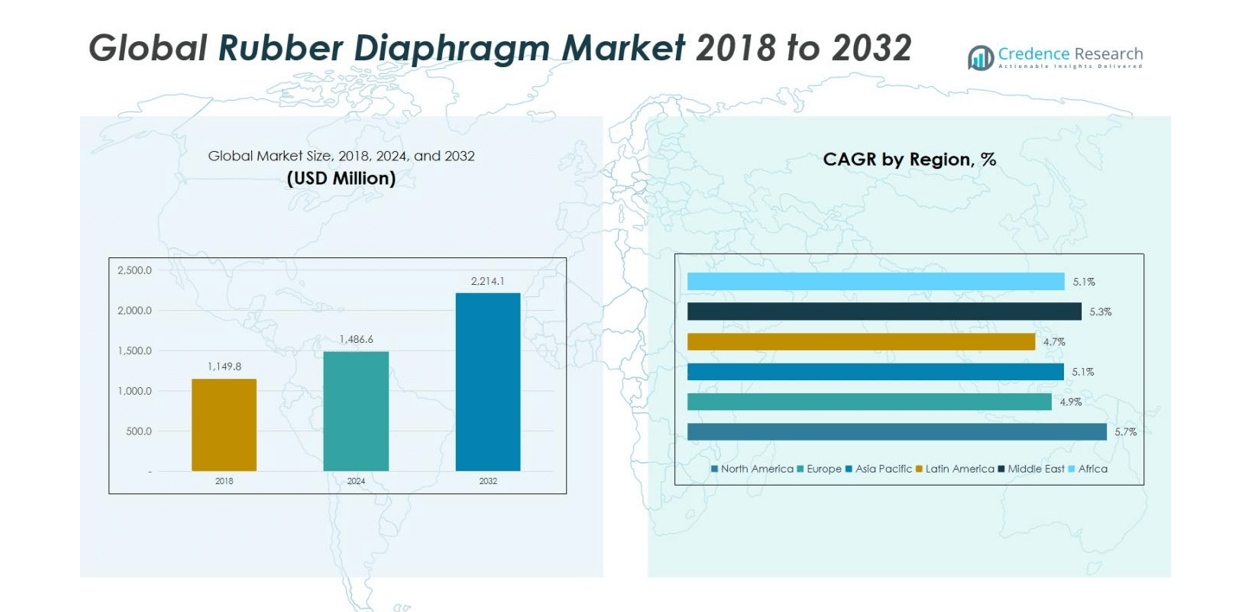

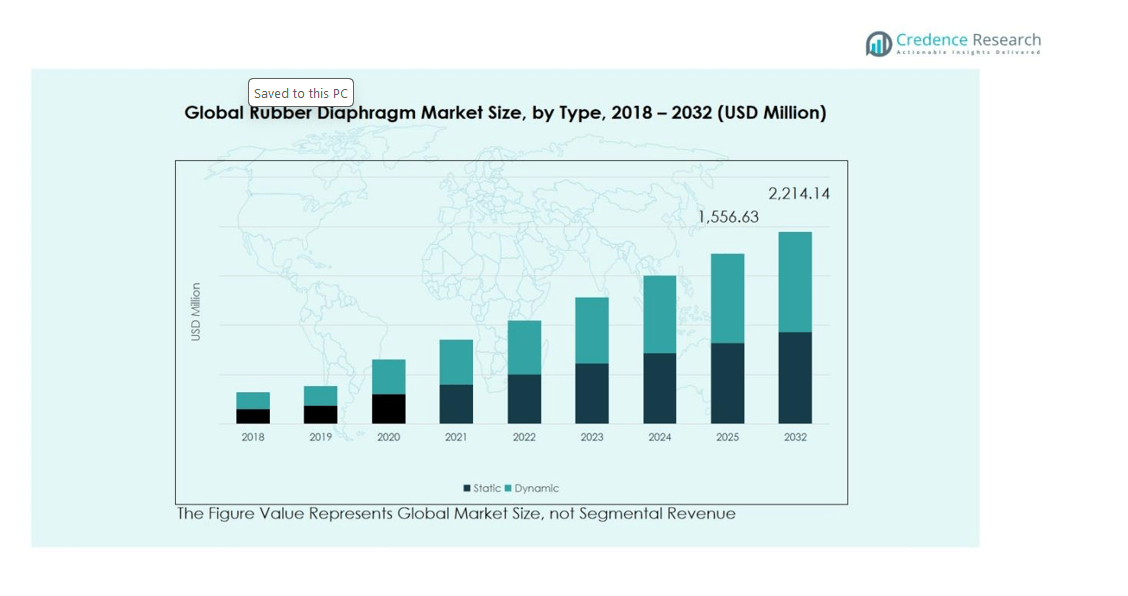

The Rubber Diaphragm Market size was valued at USD 1,149.8 million in 2018, increased to USD 1,486.6 million in 2024, and is anticipated to reach USD 2,214.1 million by 2032, at a CAGR of 5.16% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Rubber Diaphragm Market Size 2024 |

USD 1,486.6 million |

| Rubber Diaphragm Market, CAGR |

5.16% |

| Rubber Diaphragm Market Size 2032 |

USD 2,214.1 million |

The Rubber Diaphragm Market is led by prominent players including Jingzhong Rubber, Sealing Technologies, ContiTech, FUJIKURA RUBBER, Trelleborg, Garlock, Tekno, Bellofram, Chemprene, and Dazhong Rubber. These companies maintain a competitive edge through product innovation, high-performance elastomer development, and strategic collaborations with OEMs and end users. Asia Pacific dominates the market with a 34% share, driven by rapid industrialization, expanding automotive and healthcare sectors, and cost-effective manufacturing capabilities in China, Japan, and India. Europe accounts for approximately 28%, supported by strong automotive, aerospace, and industrial machinery demand, while North America holds around 22%, underpinned by advanced manufacturing infrastructure and rising adoption of high-performance diaphragms in industrial and automotive applications. Collectively, these leading players and regions shape global market trends, focusing on innovation, sustainability, and customized solutions for diverse end-use industries.

Market Insights

- The global Rubber Diaphragm Market was valued at USD 1,486.6 million in 2024 and is projected to reach USD 2,214.1 million by 2032, growing at a CAGR of 5.16%. The dynamic type segment leads with 62% share, while NBR material accounts for 38%, and the automotive end-user holds 35% of the market.

- Growth is primarily driven by rising demand from automotive and industrial sectors, where diaphragms are critical for fuel control, braking systems, emission management, and pressure regulation in pumps and valves.

- Market trends include the adoption of high-performance elastomers such as PTFE, silicone, and fluorosilicone, along with the integration of sustainable manufacturing practices to meet environmental regulations and customer demand for eco-friendly components.

- The market is moderately consolidated, with key players like Jingzhong Rubber, Sealing Technologies, ContiTech, FUJIKURA RUBBER, and Trelleborg focusing on innovation, material advancements, and strategic partnerships to expand global reach.

- Regionally, Asia Pacific dominates with 34% share, Europe holds 28%, North America 22%, followed by Latin America, the Middle East, and Africa, driven by industrial growth and infrastructure expansion

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Type:

The rubber diaphragm market is segmented into static and dynamic types. The dynamic segment dominates the market with 62% share due to its widespread use in applications that require flexibility and movement, such as pumps, valves, and actuators. These diaphragms are essential in controlling pressure variations and ensuring leak-free performance under dynamic conditions. Growing demand for automation in industrial and automotive systems continues to drive the adoption of dynamic diaphragms, while the static type, primarily used for sealing and isolation, maintains a steady presence in low-motion applications.

- For instance, Freudenberg Sealing Technologies supplies dynamic diaphragms for Bosch automotive actuators, ensuring high durability under vibration and temperature stress.

By Material:

Among the materials, NBR (Nitrile Butadiene Rubber) leads the market with an estimated 38% share, owing to its superior resistance to oils, fuels, and chemicals. This makes it highly suitable for automotive, oil & gas, and industrial applications. EPDM follows as a preferred choice in environments exposed to weathering and heat, particularly in water systems. Meanwhile, silicone and PTFE materials are gaining traction in healthcare and aerospace sectors for their biocompatibility and high-temperature stability, reinforcing the market’s shift toward performance-oriented materials.

- For instance, Parker Hannifin’s NBR-based O-rings are widely used in hydraulic systems for their dependable resistance to petroleum-based fluids. EPDM remains a preferred material in high-heat and outdoor applications such as water systems and HVAC equipment.

By End User:

The automotive segment holds the largest share, accounting for 35% of the global rubber diaphragm market, driven by the extensive use of diaphragms in braking systems, fuel control, and emission management. Industrial applications follow closely, supported by the increasing demand for pneumatic and hydraulic systems. The healthcare sector is emerging as a fast-growing segment due to rising adoption in medical devices and diagnostic equipment. Additionally, the oil & gas and water & wastewater management industries continue to contribute significantly, leveraging diaphragms for reliable sealing and flow control in harsh environments.

Key Growth Drivers

Rising Demand from Automotive and Industrial Sectors

The increasing use of rubber diaphragms in automotive and industrial systems is a primary growth driver for the market. These components are crucial for fuel regulation, braking systems, and emission control in vehicles, while industrial applications rely on them for pressure regulation and flow control in pumps and valves. As global manufacturing output expands and electric vehicle production accelerates, the demand for high-performance diaphragms that ensure precision and durability continues to rise, supporting steady market growth across developed and emerging economies.

- For instance, Mercedes-Benz utilizes rubber diaphragms in its fuel pumps and emission control systems, ensuring precise regulation under high-temperature conditions in their vehicles.

Advancements in Material Engineering

Material innovation is significantly driving market expansion by improving the performance, durability, and efficiency of rubber diaphragms. Manufacturers are investing in advanced materials such as fluorosilicone, PTFE, and composite blends that offer superior resistance to extreme temperatures, chemicals, and wear. These developments enhance the lifespan and reliability of diaphragms across critical industries such as aerospace, healthcare, and oil & gas. Continuous R&D in elastomer technology is enabling customized solutions tailored to industry-specific performance requirements, thereby strengthening the market’s technological foundation.

- For instance, Versiv Composites developed Ultraflex PTFE composite diaphragms that offer high chemical resistance and durability in pumps handling aggressive chemicals and corrosive materials, improving reliability and reducing leakage.

Expanding Applications in Healthcare and Water Management

The growing use of rubber diaphragms in healthcare devices and water treatment systems is fueling market growth. In the healthcare sector, diaphragms are used in diagnostic equipment, ventilators, and fluid control systems where biocompatibility and leak-proof performance are essential. Similarly, increasing investments in water and wastewater management are driving adoption in pumps, actuators, and control valves. With global focus shifting toward public health and sustainable infrastructure, demand for precision-engineered diaphragms with long-term operational stability is expected to accelerate further.

Key Trends & Opportunities

Shift Toward High-Performance Elastomers

A notable trend shaping the market is the shift toward high-performance elastomers that deliver enhanced mechanical and chemical resistance. Manufacturers are increasingly using materials such as PTFE-coated rubbers and silicone blends to meet stringent performance standards across automotive, aerospace, and industrial applications. This shift is not only improving product efficiency but also opening opportunities for premium diaphragm solutions in demanding environments, enabling manufacturers to capture high-value segments of the global market.

- For instance, PTFE coatings are applied to flexible elastomers in automotive sectors for door seals and engine gaskets, providing low friction, chemical resistance, and noise reduction, as demonstrated by Whitford Ltd’s Xylan® coatings used in these applications.

Growing Adoption of Sustainable Manufacturing Practices

Sustainability has become a key opportunity in the rubber diaphragm market. Companies are adopting eco-friendly production processes, including solvent-free molding and recyclable elastomer formulations. The integration of green materials reduces environmental impact while aligning with global regulations aimed at lowering industrial emissions. Additionally, partnerships between rubber producers and OEMs to develop long-lasting, energy-efficient components are creating new avenues for market expansion, particularly in regions emphasizing sustainable industrial growth.

- For instance, SRM Rubber Mouldings, which has developed biodegradable rubber compounds and recycling processes for end-of-life diaphragms, reducing environmental impact while maintaining product performance.

Key Challenges

Fluctuating Raw Material Prices

Volatility in raw material prices, particularly synthetic rubbers and specialty elastomers, poses a major challenge to manufacturers. Price fluctuations driven by supply chain disruptions, petrochemical costs, and geopolitical factors affect profit margins and production planning. Many producers face difficulties in maintaining competitive pricing while ensuring consistent quality. To mitigate this, companies are focusing on long-term supplier agreements and exploring bio-based material alternatives, though the transition remains gradual and cost-intensive.

Stringent Regulatory and Performance Standards

Compliance with stringent safety and performance standards across industries remains a key obstacle for market players. Sectors such as aerospace, healthcare, and oil & gas require diaphragms to meet exacting specifications related to temperature stability, chemical resistance, and longevity. Achieving certification for such high-performance applications often involves extensive testing, high R&D costs, and extended approval timelines. These challenges can limit market entry for smaller manufacturers and slow the overall commercialization of innovative diaphragm materials.

Regional Analysis

North America

The North America rubber diaphragm market was valued at USD 249.16 million in 2018, rising to USD 331.89 million in 2024, and is expected to reach USD 513.68 million by 2032, expanding at a CAGR of 5.7%. The region holds approximately 22% of the global market share, driven by strong demand from the automotive and industrial sectors in the U.S. and Canada. Advanced manufacturing infrastructure, coupled with a growing focus on emission control systems, fuels steady growth. Additionally, the increasing adoption of high-performance elastomers supports the market’s long-term expansion across diverse industrial applications.

Europe

Europe accounted for around 28% of the global market share, valued at USD 328.38 million in 2018, reaching USD 418.96 million in 2024, and projected to attain USD 612.87 million by 2032 at a CAGR of 4.9%. The region’s growth is fueled by the automotive, aerospace, and industrial machinery sectors, particularly in Germany, France, and the UK. Stringent regulatory standards emphasizing energy efficiency and emission control continue to drive diaphragm adoption. Additionally, the region’s focus on material innovation and the integration of eco-friendly manufacturing practices enhances product performance and market competitiveness.

Asia Pacific

Asia Pacific leads the rubber diaphragm market with a dominant 34% share, valued at USD 392.19 million in 2018, growing to USD 504.97 million in 2024, and projected to reach USD 747.94 million by 2032, registering a CAGR of 5.1%. The rapid expansion of the automotive, healthcare, and industrial sectors in China, Japan, and India underpins market growth. Strong investments in manufacturing infrastructure and increasing demand for fuel-efficient vehicles are boosting diaphragm applications. Furthermore, the availability of cost-effective raw materials and rising adoption of advanced sealing solutions continue to position Asia Pacific as the global growth hub.

Latin America

The Latin America rubber diaphragm market was valued at USD 84.16 million in 2018, rising to USD 106.08 million in 2024, and expected to reach USD 152.55 million by 2032, at a CAGR of 4.7%, holding about 7% of the global market share. Growth is primarily driven by the oil & gas, automotive, and water treatment industries, especially in Brazil and Mexico. Increasing industrial automation and infrastructure modernization are enhancing product adoption. However, fluctuating economic conditions and limited manufacturing capacity continue to restrain regional growth compared to more developed markets.

Middle East

The Middle East market accounted for USD 66.46 million in 2018, estimated at USD 86.75 million in 2024, and projected to reach USD 130.86 million by 2032, growing at a CAGR of 5.3% and representing nearly 5% of the global share. The market benefits from strong demand in the oil & gas, water management, and industrial sectors, particularly across GCC countries. Increasing investment in infrastructure projects and expansion of desalination and wastewater facilities are driving product demand. Additionally, the region’s gradual diversification into manufacturing supports the steady rise in diaphragm applications.

Africa

Africa’s rubber diaphragm market was valued at USD 29.43 million in 2018, reaching USD 37.93 million in 2024, and expected to hit USD 56.24 million by 2032, at a CAGR of 5.1%, contributing about 4% of the global market share. The growth is supported by expanding industrial and water & wastewater management activities, particularly in South Africa and Egypt. Government initiatives aimed at modernizing industrial infrastructure and enhancing water treatment capacity are increasing diaphragm adoption. However, the market remains in its early development phase, with limited local production and reliance on imports from Asia and Europe.

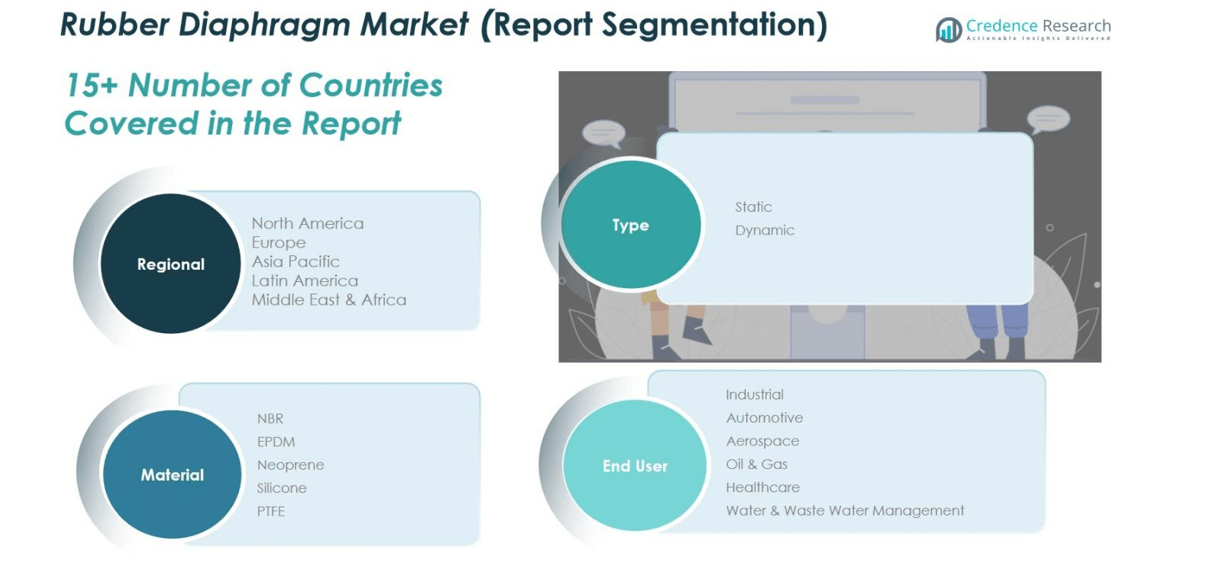

Market Segmentations:

By Type

By Material

- NBR (Nitrile Butadiene Rubber)

- EPDM (Ethylene Propylene Diene Monomer)

- Neoprene

- Silicone

- PTFE (Polytetrafluoroethylene)

By End User

- Industrial

- Automotive

- Aerospace

- Oil & Gas

- Healthcare

- Water & Wastewater Management

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Rubber Diaphragm Market features prominent players such as Jingzhong Rubber, Sealing Technologies, ContiTech, FUJIKURA RUBBER, Trelleborg, Garlock, Tekno, Bellofram, Chemprene, and Dazhong Rubber. These companies focus on product innovation, advanced material development, and strategic collaborations to strengthen their global presence. Leading manufacturers are investing in high-performance elastomers such as PTFE and silicone to enhance durability, chemical resistance, and temperature tolerance across demanding industrial and automotive applications. Partnerships with OEMs and end users are increasingly common, enabling customization and rapid integration into specialized systems. Moreover, key players are emphasizing sustainable production practices and expanding manufacturing capabilities in emerging regions, particularly in Asia Pacific, to meet rising global demand. The competitive environment remains moderately consolidated, with technological expertise, material innovation, and cost efficiency serving as primary differentiators driving long-term market leadership.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In July 2025, Techné Group, a Chinese industrial conglomerate, acquired French company EFFBE to enhance its presence in Europe. This strategic acquisition aims to integrate EFFBE’s rubber expertise with Techné’s metal 3D printing and composite processing capabilities.

- In August 2025, DiaCom Corporation announced the acquisition of RPP LLC, a designer and manufacturer of molded diaphragm seals and other custom engineered seals since 1963. This acquisition expands DiaCom’s capabilities in providing sealing solutions for various industries, including oil & gas, food & drug, medical, industrial, and water controls.

- In June 2023, GEA Group introduced a new line of diaphragm tanks using next-generation composite materials and energy-efficient designs, featuring weight reduction of up to 30%, enhanced resistance to corrosion and thermal degradation, and longer service life with reduced environmental impact.

- In June 2023, Parker Hannifin introduced an advanced range of semiconductor diaphragm valves designed specifically for high-purity applications in semiconductor production

Report Coverage

The research report offers an in-depth analysis based on Type, Material, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The rubber diaphragm market is expected to witness steady growth driven by rising demand in automotive and industrial applications.

- Increasing adoption of high-performance elastomers will enhance product durability and expand application areas.

- Technological advancements in material science will lead to the development of lightweight and temperature-resistant diaphragms.

- The healthcare sector will emerge as a major growth contributor with expanding use in medical devices and diagnostic systems.

- Growing investments in water and wastewater management will create new opportunities for diaphragm-based control systems.

- Sustainability initiatives will encourage manufacturers to adopt eco-friendly materials and production methods.

- The Asia Pacific region will continue to dominate the market due to strong industrialization and manufacturing expansion.

- North America and Europe will focus on innovation and regulatory compliance to maintain their market positions.

- Strategic partnerships and mergers will enhance product portfolios and global distribution networks.

- Continuous R&D investment will drive customization and performance improvements across key end-use industries.