Market Overview

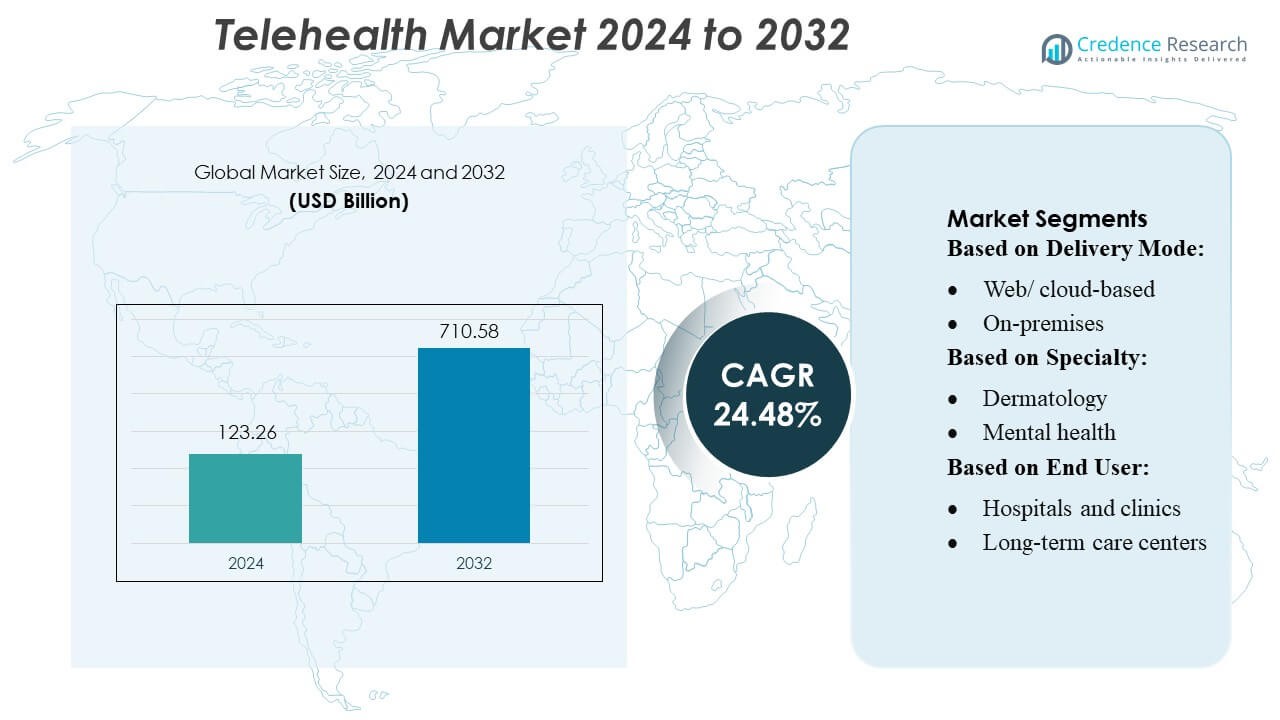

Telehealth Market size was valued USD 123.26 billion in 2024 and is anticipated to reach USD 710.58 billion by 2032, at a CAGR of 24.48% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Telehealth Market Size 2024 |

USD 123.26 Billion |

| Telehealth Market, CAGR |

24.48% |

| Telehealth Market Size 2032 |

USD 710.58 Billion |

The telehealth market is supported by a diverse mix of technology providers, virtual-care platforms, and healthcare solution innovators that continue to expand digital access and enhance clinical efficiency. These players focus on strengthening remote monitoring capabilities, improving interoperability with electronic health records, and integrating AI-driven tools to support virtual diagnostics and patient management. Strategic partnerships with hospitals, insurers, and government programs further accelerate adoption across care settings. North America leads the global telehealth market with approximately 40% market share, driven by advanced digital infrastructure, supportive reimbursement systems, and strong patient acceptance of virtual healthcare services.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The telehealth market was valued at USD 123.26 billion in 2024 and is projected to reach USD 710.58 billion by 2032, growing at a CAGR of 24.48% during the forecast period.

- Rising demand for remote patient monitoring, increasing digital adoption, and wider use of AI-driven virtual care tools strongly drive market expansion across all major care settings.

- Key trends include rapid integration of electronic health records, growth of hybrid care models, and broader acceptance of virtual consultations among both patients and providers.

- Competition intensifies as companies enhance platform scalability, strengthen data security, and form strategic partnerships to expand service capabilities across specialties and end-user segments.

- North America leads with 40% regional share, supported by advanced digital infrastructure, while cloud-based delivery dominates segment-wise with nearly 70% share, driven by scalability and lower operational costs.

Market Segmentation Analysis:

By Delivery Mode:

The web/cloud-based delivery mode holds the dominant share in the telehealth market, accounting for around 70% due to its easy accessibility, low maintenance needs, and ability to support large patient volumes without heavy infrastructure. Cloud platforms allow healthcare providers to manage appointments, medical records, and virtual consultations from any location, making them highly convenient for both providers and patients. The on-premises segment remains smaller because it requires higher installation and maintenance costs, but it is still preferred by institutions that prioritize strict control of sensitive patient data and enhanced internal security.

- For instance, Global Med’s secure virtual-health system has facilitated over 63 million remote consultations across more than 60 countries, leveraging its cloud-native architecture to deliver care in rural clinics, veteran hospitals, and even remote correctional facilities.

By Specialty:

Within the specialty segment, dermatology leads the market as the largest sub-segment because skin-related issues can be effectively diagnosed through high-quality images and videos, reducing the need for in-person visits. This specialty benefits from strong patient adoption, rising cases of skin conditions, and widespread smartphone usage for remote assessments. Other areas such as mental health, cardiology, neurology, orthopedics, gynecology, and additional specialties are growing steadily, driven by the need to improve appointment access, reduce wait times, and offer continuous care for chronic conditions through virtual consultations.

- For instance, Medtronic has demonstrated strong telehealth innovation through its CareLink™ network: more than 720,000 patients across 6,600 clinics in 33 countries now use it for remote monitoring of their cardiac devices.

By End User:

In the end-user category, hospitals and clinics dominate the telehealth market due to their large patient base, established digital systems, and ability to integrate telehealth into routine clinical workflows. These facilities rely on virtual consultations to reduce crowding, support follow-up care, and manage chronic disease patients more efficiently. Healthcare providers, long-term care centers, and other medical facilities also contribute to market growth, adopting telehealth primarily to reach patients in remote areas, improve monitoring of elderly populations, and reduce operational pressures on physical healthcare environments.

Key Growth Drivers

- Growing Demand for Remote Patient Monitoring

The market grows as healthcare systems adopt remote patient monitoring to improve chronic disease management and reduce hospital readmissions. Telehealth platforms enable continuous tracking of vitals, medication adherence, and symptom progression, allowing clinicians to intervene early and avoid complications. The rising prevalence of diabetes, cardiovascular disorders, and respiratory diseases further accelerates adoption. Providers benefit from reduced operational burden, while patients gain convenient access to care without frequent visits. This shift toward proactive and data-driven care strongly boosts telehealth expansion globally.

- For instance, EHR that automatically generates clinical notes after a doctor records a patient visit — saving more than four and a half minutes per patient and reducing documentation time by 20-40% daily.

- Expansion of Digital Infrastructure and Connectivity

Improved broadband access, rising smartphone penetration, and enhanced cloud capabilities significantly strengthen telehealth adoption. High-speed connectivity enables reliable video consultations, seamless data transfer, and real-time communication between patients and providers. Governments and private organizations continue investing in digital health ecosystems, further supporting telehealth integration into routine care pathways. Enhanced IT infrastructure also enables scalability, allowing providers to manage higher patient volumes efficiently. These advancements collectively increase telehealth reliability, accessibility, and acceptance across urban and rural populations.

- For instance, MDLIVE supports a national clinical network of over 2,000 providers across more than 7,500 medical licenses, all coordinated through a single, HiTrust-certified, cloud-based platform.

- Increasing Focus on Cost-Effective Healthcare Delivery

Healthcare providers increasingly rely on telehealth to reduce operational costs, streamline workflows, and minimize the burden on overcrowded hospital facilities. Virtual consultations lower administrative expenses, reduce unnecessary emergency visits, and optimize resource allocation. Insurers and government bodies are also expanding reimbursement frameworks to encourage digital care adoption. For patients, telehealth reduces travel time, consultation expenses, and waiting periods, making it a highly cost-effective alternative. These financial advantages reinforce sustained demand for telehealth solutions across both developed and emerging markets.

Key Trends & Opportunities

- Integration of AI and Predictive Analytics

The rise of AI-driven diagnostics, triage tools, and predictive analytics presents a major opportunity for telehealth platforms. AI enhances clinical decision-making, supports early detection of complications, and automates routine tasks such as symptom assessment and report generation. Machine learning models can analyze patient-generated data to identify health risks and recommend timely interventions. As AI technologies mature, telehealth providers can deliver more personalized, efficient, and scalable care solutions, creating significant competitive differentiation and improving long-term patient outcomes.

- For instance, American Well’s Converge™ platform integrates a Biobeat remote monitoring system that continuously tracks up to 15 vital signs (including blood pressure, heart rate, oxygen saturation, and respiratory rate), and uses AI-powered algorithms to generate real-time early warning scores for patient deterioration.

- Growing Adoption of Hybrid Care Models

Healthcare systems increasingly adopt hybrid models that combine virtual and in-person care to enhance patient experience and clinical efficiency. Telehealth is now integrated into primary care, follow-up consultations, mental health support, and chronic disease management, enabling flexible and continuous care delivery. Providers benefit from better scheduling efficiency and broader reach, while patients receive seamless transitions between online and physical visits. This emerging hybrid approach creates opportunities for telehealth platforms to expand service offerings and strengthen their position within integrated care networks.

- For instance, Philips’ eICU / eCareManager platform supports remote monitoring of more than 10,000 ICU patients annually, enabling centralized care coordination and early deterioration alerts.

- Rising Opportunities in Rural and Underserved Regions

Telehealth platforms are well-positioned to address healthcare gaps in remote and underserved areas where access to specialists and advanced medical facilities is limited. Expanding digital networks and government-led telemedicine initiatives create new opportunities to reach populations with inadequate healthcare infrastructure. Virtual consultations reduce travel barriers and improve timely access to diagnosis, chronic disease management, and preventive care. These regional expansion opportunities also support long-term market growth, especially in emerging economies investing in digital health transformation.

Key Challenges

- Data Privacy and Cybersecurity Risks

Telehealth platforms face persistent challenges related to data security, privacy protection, and regulatory compliance. Large volumes of sensitive patient information stored on digital systems increase vulnerability to cyberattacks, unauthorized access, and data breaches. Providers must invest heavily in encryption, secure cloud frameworks, and compliance with healthcare regulations such as HIPAA and GDPR. Failure to address these risks can reduce patient trust and hinder adoption. Ensuring robust cybersecurity measures remains essential for maintaining system integrity and safeguarding digital healthcare services.

- Limited Digital Literacy and Technology Access

Despite strong growth, telehealth adoption is hindered by disparities in digital literacy and unequal access to reliable internet or smart devices, particularly among elderly populations and low-income groups. Users may struggle with navigating applications, managing online consultations, or troubleshooting technical issues, reducing the effectiveness of virtual care. Healthcare providers must invest in user-friendly platform designs and patient education to bridge this gap. Without addressing these barriers, the benefits of telehealth may remain inaccessible to significant portions of the population.

Regional Analysis

North America

North America holds the largest share of the telehealth market at around 40%, supported by strong digital infrastructure, high internet penetration, and early adoption of virtual care services. The United States drives most of the demand, as healthcare providers use telehealth to manage chronic diseases, reduce hospital visits, and expand access. Supportive reimbursement policies and rising consumer acceptance further encourage growth. The region also benefits from advanced electronic health record systems and wide use of smartphones, making telehealth an essential part of routine healthcare delivery.

Europe

Europe accounts for roughly 25–28% of the telehealth market, driven by government-led digital health initiatives and increasing demand for remote care among aging populations. Countries such as the UK, Germany, and France continue expanding teleconsultation services to reduce hospital congestion and improve healthcare efficiency. Strong regulatory frameworks and national e-health programs support the adoption of secure telemedicine platforms. Improved broadband access and growing acceptance of virtual appointments make Europe a mature and steadily expanding market for telehealth solutions.

Asia-Pacific

Asia-Pacific holds an estimated 20–24% share and is the fastest-growing region in the telehealth market. Rapid smartphone penetration, affordable data plans, and expanding digital infrastructure drive widespread adoption. Governments in China, India, and Japan actively promote telemedicine to improve rural healthcare access and reduce pressure on overcrowded hospitals. The region’s large population base and rising chronic disease burden create strong demand for remote consultations and virtual monitoring. Private healthcare providers also invest heavily in telehealth platforms, accelerating overall market growth.

Latin America

Latin America represents about 6% of the global telehealth market, with growth supported by expanding mobile connectivity and increasing demand for remote healthcare in underserved communities. Brazil and Mexico lead the region in adopting virtual care solutions to address doctor shortages and improve patient access. Telehealth use increased as providers embraced virtual consultations for cost-effective and convenient care delivery. Although infrastructure challenges persist, rising government support and growing familiarity with digital health tools continue to strengthen regional adoption.

Middle East & Africa

The Middle East & Africa region holds approximately 5–10% of the telehealth market. Growth is driven by investments in digital healthcare systems, particularly in GCC countries such as the UAE and Saudi Arabia. These nations promote telemedicine to enhance service quality and support national health transformation programs. In Africa, mobile-based health platforms help overcome limited access to medical specialists and long travel distances. Expanding internet coverage and government-backed initiatives continue to improve adoption, making telehealth an increasingly valuable solution for the region.

Market Segmentations:

By Delivery Mode:

- Web/ cloud-based

- On-premises

By Specialty:

- Dermatology

- Mental health

By End User:

- Hospitals and clinics

- Long-term care centers

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the telehealth market is shaped by leading players such as Global Med, Medtronic, Doctor On Demand, Cerner Corporation (Oracle), MD Live, American Well, Koninklijke Philips N.V., Teladoc Health Inc., Siemens Healthineers, and GE Healthcare. The telehealth market features an increasingly competitive landscape driven by rapid digital transformation, strong demand for remote care, and continuous innovation in virtual health technologies. Companies focus on enhancing platform interoperability, strengthening data security, and integrating advanced tools such as AI-assisted diagnostics and remote monitoring systems. Market participants also invest in scalable cloud-based solutions, user-friendly mobile applications, and virtual triage capabilities to improve patient engagement and clinical efficiency. Partnerships with hospitals, insurers, and technology firms remain central to expanding service coverage and improving care coordination. As regulatory support and reimbursement frameworks evolve, competition intensifies, encouraging providers to differentiate through specialized services, seamless care delivery, and improved patient experience.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Global Med

- Medtronic

- Doctor On Demand

- Cerner Corporation (Oracle)

- MD Live

- American Well

- Koninklijke Philips N.V

- Teladoc Health Inc

- Siemens Healthineers

- GE Healthcare

Recent Developments

- In July 2025, Ayush Wellness launched Aayush Health, a digital platform offering remote doctor consultations and digital health records, aiming to improve healthcare access to India’s Tier 2 and Tier 3 cities. This launch highlights telehealth’s expanding reach into developing countries, reinforcing its role in bridging healthcare gaps and driving inclusive growth across the Indian market.

- In May 2025, Airvet CEO and Founder Brandon Werger says companies are betting on Kitty and Rex’s wellness to boost human productivity. Airvet offers discounted pet insurance options from multiple providers, pharmacy benefits with home delivery, food discounts, and even backup care.

- In April 2025, Novo Nordisk on Tuesday said it will offer its weight loss drug Wegovy through telehealth providers Hims & Hers Health, Ro and LifeMD to expand access to the Hims and Hers shares rocket 23%. Patients will be able to access Novo Nordisk’s new direct-to-consumer online pharmacy.

- In June 2024, Apollo Telehealth, in partnership with the Government of Manipur, opened a telemedicine-driven primary health center (PHC) in Borobeka, Manipur, to improve healthcare access for residents.

Report Coverage

The research report offers an in-depth analysis based on Delivery Mode, Specialty, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand as more patients choose virtual consultations for routine and follow-up care.

- Healthcare providers will integrate telehealth into regular clinical workflows to improve efficiency.

- Remote patient monitoring will grow as chronic disease management shifts toward continuous digital oversight.

- AI-enabled triage and diagnostic tools will enhance accuracy and reduce clinician workload.

- Hybrid care models combining virtual and in-person services will become standard practice.

- Telehealth adoption will increase in rural and underserved regions due to improved connectivity.

- Regulatory frameworks and reimbursement policies will continue to support digital care delivery.

- Hospitals will invest more in secure, interoperable platforms to streamline virtual services.

- Consumer demand will rise as telehealth platforms become easier to use and more reliable.

- Expansion of wearable devices and connected sensors will strengthen real-time health monitoring.