Market Overview

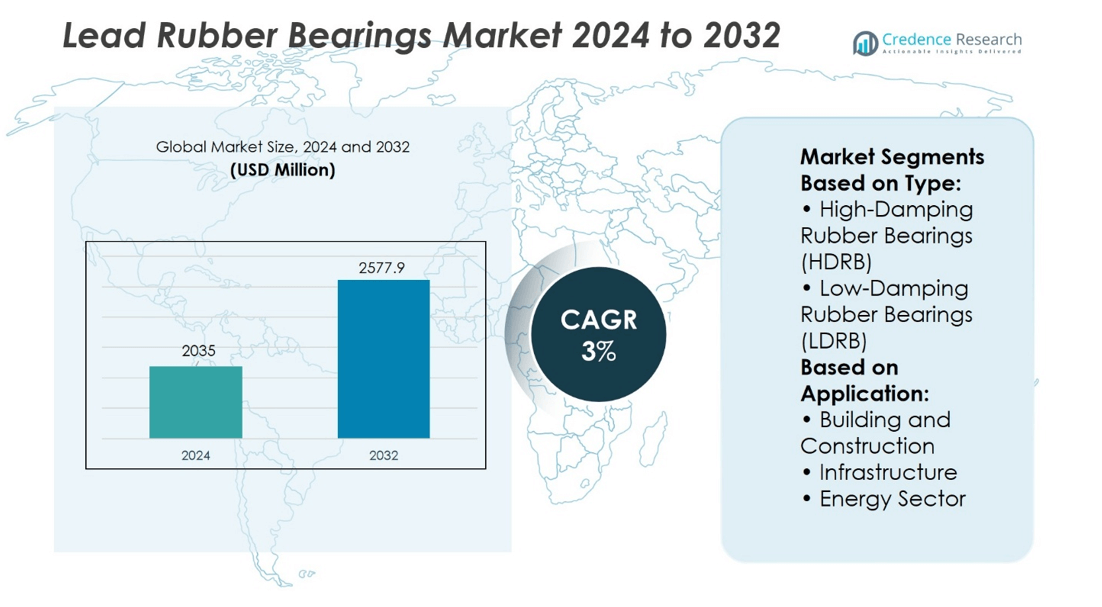

Lead Rubber Bearings Market size was valued at USD 2035 million in 2024 and is anticipated to reach USD 2577.9 million by 2032, at a CAGR of 3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Lead Rubber Bearings Market Size 2024 |

USD 2035 million |

| Lead Rubber Bearings Market, CAGR |

3% |

| Lead Rubber Bearings Market Size 2032 |

USD 2577.9 million |

The Lead Rubber Bearings Market grows through rising demand for seismic isolation systems in infrastructure and building projects, driven by stricter safety regulations and increasing urban development in earthquake-prone regions. It benefits from advancements in material engineering, enabling higher durability, improved damping efficiency, and adaptability to diverse structural requirements. Market growth is reinforced by the expansion of retrofit projects for aging infrastructure and the integration of smart monitoring technologies for real-time performance tracking. Sustainability initiatives and the use of eco-friendly manufacturing processes further shape industry direction, while customization capabilities strengthen adoption across transportation, energy, and high-value construction sectors.

The Lead Rubber Bearings Market shows strong presence across Asia-Pacific, North America, Europe, Latin America, and the Middle East & Africa, with Asia-Pacific leading due to high seismic activity and extensive infrastructure projects. North America and Europe follow, driven by stringent safety regulations and modernization programs. Key players include Bridgestone Corporation, Kurashiki Kako Co., Ltd., Maurer SE, Trelleborg AB, FIP Industriale S.p.A., HengShui ZhongBang Rubber Co., Ltd., and OILES Corporation, each focusing on innovation, quality standards, and project-specific engineering solutions.

Market Insights

- Lead Rubber Bearings Market size was valued at USD 2035 million in 2024 and is projected to reach USD 2577.9 million by 2032, at a CAGR of 3%.

- Rising demand for seismic isolation systems in infrastructure and building projects drives market expansion.

- Advancements in material engineering improve durability, damping efficiency, and adaptability to diverse structural needs.

- Competitive landscape features established manufacturers focusing on innovation, quality, and customized engineering solutions.

- High production costs and strict compliance requirements act as key restraints.

- Asia-Pacific leads the market share, followed by North America and Europe, with growth supported by infrastructure investments and safety regulations.

- Integration of smart monitoring technologies and sustainable manufacturing practices shapes future market direction.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Growing Demand for Seismic Protection in Infrastructure Projects

The Lead Rubber Bearings Market grows through the rising adoption of seismic isolation technologies in bridges, buildings, and industrial facilities. Governments and private developers incorporate these systems to enhance structural resilience and reduce earthquake damage. It offers a proven method to dissipate seismic energy and protect critical assets. Infrastructure modernization programs in earthquake-prone regions accelerate deployment rates. Regulatory bodies promote compliance with seismic safety standards, creating a consistent demand base. This strong alignment between safety requirements and engineering solutions drives continuous adoption.

- For instance, Bridgestone Corporation provided lead rubber bearings for the Yokohama Bay Bridge seismic retrofit, significantly increasing its capacity to endure strong earthquakes. These bearings, with a combined design load capacity of 21.5 million newtons, act as seismic isolators, absorbing and dissipating earthquake energy to protect the bridge.

Advancements in Material Engineering and Manufacturing Processes

The Lead Rubber Bearings Market benefits from technological progress in rubber compounding, lead core optimization, and precision manufacturing. Enhanced material formulations improve energy dissipation, load-bearing capacity, and durability. It enables the development of compact, high-performance bearings suited for diverse structural designs. Modern production methods ensure tighter tolerances and consistent product quality. Manufacturers invest in automation and quality control systems to meet international performance certifications. These advancements strengthen market competitiveness and expand application versatility.

- For instance, in 2022, mageba India opened a new production facility in Kolkata that tripled their annual manufacturing capacity of elastomeric seismic isolators expanding from an initial 0.5 million units per year to 1.5 million units per year.

Rising Investment in Urban Development and Public Safety

Large-scale urban development projects support the growth of the Lead Rubber Bearings Market by integrating seismic protection into new construction. Public safety priorities influence government procurement strategies for resilient infrastructure. It aligns with city planning initiatives that aim to safeguard populations and minimize post-disaster recovery costs. Infrastructure funding programs target transportation hubs, hospitals, and emergency facilities in seismic zones. Private sector developers increasingly adopt isolation systems to enhance asset value and meet investor expectations. This trend solidifies the role of lead rubber bearings in modern urban planning.

Expanding Retrofit and Rehabilitation Activities

The Lead Rubber Bearings Market gains momentum from the growing demand for retrofitting existing structures to meet updated seismic safety standards. Aging infrastructure in high-risk areas requires isolation system installation to extend operational lifespan. It offers a cost-effective approach to improving performance without full reconstruction. Engineering firms design customized retrofit solutions for heritage buildings, bridges, and industrial plants. Public funding and international aid programs support rehabilitation in disaster-prone regions. This focus on structural resilience drives sustained adoption across retrofit markets.

Market Trends

Integration of Lead Rubber Bearings in Smart Infrastructure

The Lead Rubber Bearings Market shows a clear trend toward integration with smart monitoring systems for real-time performance tracking. Infrastructure owners install sensors within bearings to measure displacement, temperature, and load during seismic events. It enables predictive maintenance and improves asset management efficiency. Digital connectivity supports automated reporting for engineers and regulatory agencies. The demand for data-driven maintenance strategies drives adoption in both new builds and retrofit projects. This combination of physical resilience and digital intelligence enhances overall infrastructure safety.

Adoption of High-Performance Material Compositions

The Lead Rubber Bearings Market advances through the development of enhanced rubber compounds and refined lead core designs. Manufacturers introduce materials with improved fatigue resistance, lower temperature sensitivity, and higher energy dissipation capacity. It enables bearings to perform consistently in extreme climates and under repeated seismic loading. Advanced testing protocols validate these materials for long-term reliability. International standards increasingly require such performance benchmarks, influencing procurement choices. This material innovation trend expands the range of structural applications.

- For instance, for the retrofit of the Swiss Viaduc de Chillon, mageba supplied 203 LASTO® LRB isolator bearings, each featuring an average diameter of approximately 1,200 mm and engineered to support a design load of approximately 20,000 kN per unit.

Customization for Diverse Structural Applications

The Lead Rubber Bearings Market evolves with increasing demand for project-specific bearing designs. Engineers work with manufacturers to develop bearings that match unique load profiles, geometric constraints, and seismic risk levels. It allows integration into a wide variety of infrastructure types, from suspension bridges to high-rise buildings. Modular design concepts enable rapid adaptation without extensive redesign costs. Tailored solutions gain preference in government tenders and private contracts. This shift toward customization reflects the growing complexity of modern infrastructure projects.

Focus on Sustainable and Low-Impact Manufacturing

The Lead Rubber Bearings Market aligns with global sustainability initiatives through the use of recyclable materials and energy-efficient production processes. Manufacturers invest in cleaner vulcanization methods and environmentally responsible lead sourcing. It reduces the environmental footprint of production while maintaining structural performance standards. Industry certifications for sustainable manufacturing strengthen market positioning. Green construction programs and eco-friendly procurement policies support adoption in environmentally conscious projects. This emphasis on sustainability complements performance-driven purchasing decisions.

- For instance, Trelleborg AB implemented a closed-loop rubber recycling system with an annual processing capacity of 3.6 million kilograms, significantly reducing raw material consumption in lead rubber bearing production.

Market Challenges Analysis

High Production Costs and Complex Manufacturing Requirements

The Lead Rubber Bearings Market faces cost pressures due to the high-quality materials and precision manufacturing processes required for optimal performance. Premium-grade rubber compounds, refined lead cores, and specialized steel plates increase production expenses. It demands advanced vulcanization equipment, strict quality control systems, and skilled labor to meet international performance standards. Small and medium manufacturers often face challenges in sustaining competitive pricing while ensuring compliance. Limited availability of certified raw materials can cause procurement delays and further raise costs. These factors create entry barriers for new players and limit pricing flexibility in competitive tenders.

Regulatory Compliance and Installation Constraints

Strict regulatory standards governing seismic isolation systems present operational challenges for the Lead Rubber Bearings Market. It must adhere to rigorous testing, certification, and inspection protocols before deployment in infrastructure projects. Compliance processes can be time-consuming and resource-intensive, especially in multiple jurisdictions with differing technical requirements. Installation in existing structures may involve complex engineering modifications, increasing project timelines and costs. Accessibility issues in retrofit applications can limit deployment feasibility. These regulatory and technical complexities require manufacturers and contractors to maintain strong design expertise and project coordination capabilities.

Market Opportunities

Rising Infrastructure Investments in Seismic-Prone Regions

The Lead Rubber Bearings Market holds strong growth potential through expanding infrastructure development in earthquake-prone areas. Governments and private investors prioritize seismic resilience in transportation networks, public facilities, and commercial structures. It offers a proven solution for reducing damage and ensuring operational continuity after seismic events. Large-scale urban renewal projects present opportunities for integrating isolation systems into both new construction and retrofit applications. International funding programs for disaster risk reduction further support adoption. This demand is expected to remain strong in regions with active seismic activity and strict building safety regulations.

Advancements Enabling Broader Application Scope

The Lead Rubber Bearings Market benefits from technological innovations that enhance product adaptability and efficiency. It now includes designs capable of withstanding higher loads, extreme environmental conditions, and complex structural geometries. Integration with smart monitoring systems expands its value proposition for asset management and predictive maintenance. These advancements make the technology suitable for critical infrastructure such as hospitals, data centers, and energy facilities. Growing interest from the private sector in safeguarding high-value assets creates new commercial opportunities. This combination of technical evolution and market diversification strengthens its long-term adoption outlook.

Market Segmentation Analysis:

By Type

The Lead Rubber Bearings Market divides into high-damping rubber bearings (HDRB), low-damping rubber bearings (LDRB), and others. HDRB types dominate applications that demand superior energy dissipation and vibration control in high-seismic regions. It offers enhanced durability and stability under repeated load cycles, making it suitable for critical infrastructure and tall structures. LDRB types find preference in projects requiring lower damping properties while maintaining flexibility and long service life. These bearings are often selected for moderate seismic zones or structures where cost optimization is a priority. The others segment includes specialized designs tailored for unique structural requirements, such as hybrid systems combining multiple isolation technologies.

- For instance, Maurer SE manufactured 2.4 million high-damping rubber bearings for large-scale bridge and building projects, each engineered to achieve optimal energy dissipation and vibration control under extreme seismic loads.

By Application

The Lead Rubber Bearings Market serves building and construction, infrastructure, and the energy sector, each with distinct performance requirements. In building and construction, these systems enhance seismic resilience for high-rise towers, residential complexes, and commercial buildings, enabling structural flexibility while meeting stringent safety codes. It supports both new developments and retrofitting of older structures to comply with updated seismic standards. In infrastructure, lead rubber bearings play a vital role in bridges, rail terminals, and airports, ensuring operational continuity and reducing repair needs after seismic events. Government-funded modernization projects and large-scale public works drive demand in this segment.

- For instance, Kurashiki Kako Co., Ltd. supplied 2.3 million lead rubber bearings for commercial and residential high-rise developments, engineered to provide optimal displacement capacity and energy dissipation in high-seismic urban zones.

Segments:

Based on Type:

- High-Damping Rubber Bearings (HDRB)

- Low-Damping Rubber Bearings (LDRB)

Based on Application:

- Building and Construction

- Infrastructure

- Energy Sector

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds a market share of 28.4% in the Lead Rubber Bearings Market, driven by stringent seismic safety regulations and significant investments in earthquake-resilient infrastructure. The United States accounts for the majority of regional demand, supported by large-scale public infrastructure projects, high-rise developments, and retrofitting of older structures to meet updated building codes. Canada contributes through seismic protection initiatives in British Columbia and other earthquake-prone provinces. It benefits from the presence of established manufacturers, advanced engineering capabilities, and strong collaboration between government agencies and the private sector to promote seismic isolation technologies. Adoption rates are further strengthened by insurance incentives for buildings with seismic mitigation measures. Continuous investment in smart city development and infrastructure modernization supports steady growth across both new construction and rehabilitation projects.

Europe

Europe commands 24.7% of the Lead Rubber Bearings Market, supported by proactive regulatory frameworks and long-term infrastructure resilience programs. Countries such as Italy, Greece, and Turkey lead demand due to higher seismic activity, while France, the United Kingdom, and Germany integrate lead rubber bearings into high-value infrastructure and transportation projects. It benefits from EU-wide initiatives promoting disaster risk reduction and the retrofitting of heritage buildings without compromising architectural integrity. Manufacturers in the region focus on developing environmentally sustainable bearings, aligning with the European Green Deal objectives. Investments in bridges, tunnels, and rail infrastructure enhance market penetration, with cross-border projects creating additional procurement opportunities. The emphasis on durability, energy efficiency, and advanced monitoring systems further drives the adoption of high-performance isolation bearings in both public and private sectors.

Asia-Pacific

Asia-Pacific holds the largest market share at 32.9%, fueled by rapid urbanization, high seismic risk zones, and substantial government infrastructure spending. Japan leads adoption with advanced engineering standards and nationwide seismic isolation programs, while China’s extensive bridge and high-rise construction projects generate significant demand. It also benefits from increasing installations in India, Indonesia, and New Zealand, where earthquake resilience is becoming a core part of construction planning. Manufacturers in the region invest in mass production capabilities to meet large-scale project requirements while maintaining international quality standards. Public infrastructure projects such as metro networks, airports, and energy facilities integrate lead rubber bearings to protect against seismic events and ensure operational continuity. The combination of cost-effective manufacturing and high-volume demand positions Asia-Pacific as a long-term growth hub for the market.

Latin America

Latin America accounts for 6.9% of the Lead Rubber Bearings Market, driven by seismic vulnerability in countries such as Chile, Mexico, and Peru. National building codes mandate seismic isolation in critical infrastructure, creating consistent demand for lead rubber bearings in hospitals, schools, and transportation networks. It benefits from retrofitting programs targeting older buildings in urban centers to enhance earthquake resilience. Local production remains modest, with many projects sourcing bearings from North American and Asian manufacturers. Growth is supported by public-private partnerships and regional infrastructure modernization efforts. Continued investment in energy and transportation sectors, combined with a focus on disaster risk mitigation, positions Latin America as a steadily expanding market for advanced seismic isolation solutions.

Middle East & Africa

The Middle East & Africa region represents 7.1% of the Lead Rubber Bearings Market, with demand concentrated in seismically active areas such as Turkey, Iran, and parts of North Africa. Gulf Cooperation Council (GCC) countries adopt these systems in high-value infrastructure and critical facilities despite relatively lower seismic exposure, focusing on long-term asset protection. It gains traction through government-led initiatives to improve disaster preparedness, particularly in strategic transportation and energy projects. In Africa, demand is emerging in countries with developing urban infrastructure and increased awareness of seismic safety. Local manufacturing capabilities remain limited, leading to reliance on imports from established global producers. International collaborations and funding from development agencies support adoption in public sector projects, creating opportunities for market expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Continental AG

- CEAT Tyres

- Michelin

- Apollo Tyres

- Cooper Tire Rubber

- Kumho Tire

- Trelleborg AB

- Sumitomo Rubber Industries

- Hankook Tire Technology

- MRF Tyres

Competitive Analysis

The Lead Rubber Bearings Market players include Bridgestone Corporation, Kurashiki Kako Co., Ltd., Maurer SE, Trelleborg AB, FIP Industriale S.p.A., HengShui ZhongBang Rubber Co., Ltd., and OILES Corporation. The competitive landscape of the Lead Rubber Bearings Market is defined by advanced engineering capabilities, consistent innovation, and a strong focus on meeting stringent seismic safety standards. Leading manufacturers prioritize research and development to improve damping performance, load-bearing capacity, and product durability. They invest in new material formulations, optimized lead core designs, and sustainable production methods to address both performance and environmental requirements. Strategic collaborations with construction firms, engineering consultants, and government agencies allow them to secure large-scale infrastructure and retrofit projects in seismic-prone regions. Geographic expansion, localized manufacturing, and efficient supply chain management help reduce lead times and adapt to region-specific regulations. Competitive differentiation is achieved through the ability to deliver certified, project-specific solutions for diverse applications, including bridges, high-rise buildings, and critical facilities, ensuring resilience and operational continuity in challenging environments.

Recent Developments

- In 2024, Schaeffler India, another major player, formed a strategic partnership with Tata Motors for the supply of bearings for their electric vehicles.

- In May 2024, Glencore announced an expansion of its lead recycling capacity in Europe by upgrading its Nordenham facility in Germany to process higher volumes of used lead-acid batteries. The move aligns with EU circular economy goals and rising demand for secondary lead.

- In June 2023, EnerSys initiated a non-binding Memorandum of Understanding with Verkor SAS to explore the establishment of a lithium battery gigafactory in the United States.

- In October 2023, The Timken Company, a global leader in engineered bearings and industrial motion products, announced its agreement to acquire Engineered Solutions Group, also known as Innovative Mechanical Solutions (iMECH), based in Houston, Texas. iMECH specializes in manufacturing thrust and radial bearings.

Market Concentration & Characteristics

The Lead Rubber Bearings Market demonstrates a moderate to high level of concentration, with a limited number of established manufacturers holding significant global market share. It is characterized by high entry barriers due to the need for specialized engineering expertise, advanced manufacturing capabilities, and strict compliance with international seismic safety standards. Leading companies differentiate through innovation in material science, precision manufacturing, and customized design solutions for diverse infrastructure projects. The market exhibits strong demand stability in seismic-prone regions, supported by regulatory mandates and long-term infrastructure resilience programs. It relies on rigorous testing, certification, and quality assurance processes to ensure reliability and performance under extreme conditions. Competitive dynamics are influenced by the ability to deliver large-scale, certified solutions within strict project timelines, often requiring close collaboration with engineering firms and government agencies. The integration of sustainable manufacturing practices, digital monitoring technologies, and tailored product configurations further defines the market’s evolving characteristics.

Report Coverage

The research report offers an in-depth analysis based on Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will grow in seismic-prone regions due to stricter safety regulations.

- Adoption will rise in urban infrastructure and smart city projects.

- Material innovations will improve durability and load-handling capacity.

- Retrofit projects will expand in aging infrastructure across key markets.

- Integration with smart monitoring systems will enhance asset management.

- Sustainable manufacturing practices will become a competitive advantage.

- Customization will increase to meet diverse project specifications.

- Strategic partnerships will strengthen global supply and project execution.

- Emerging economies will drive new opportunities in public infrastructure.

- Investment in advanced testing and certification will support market credibility.