Market Overview

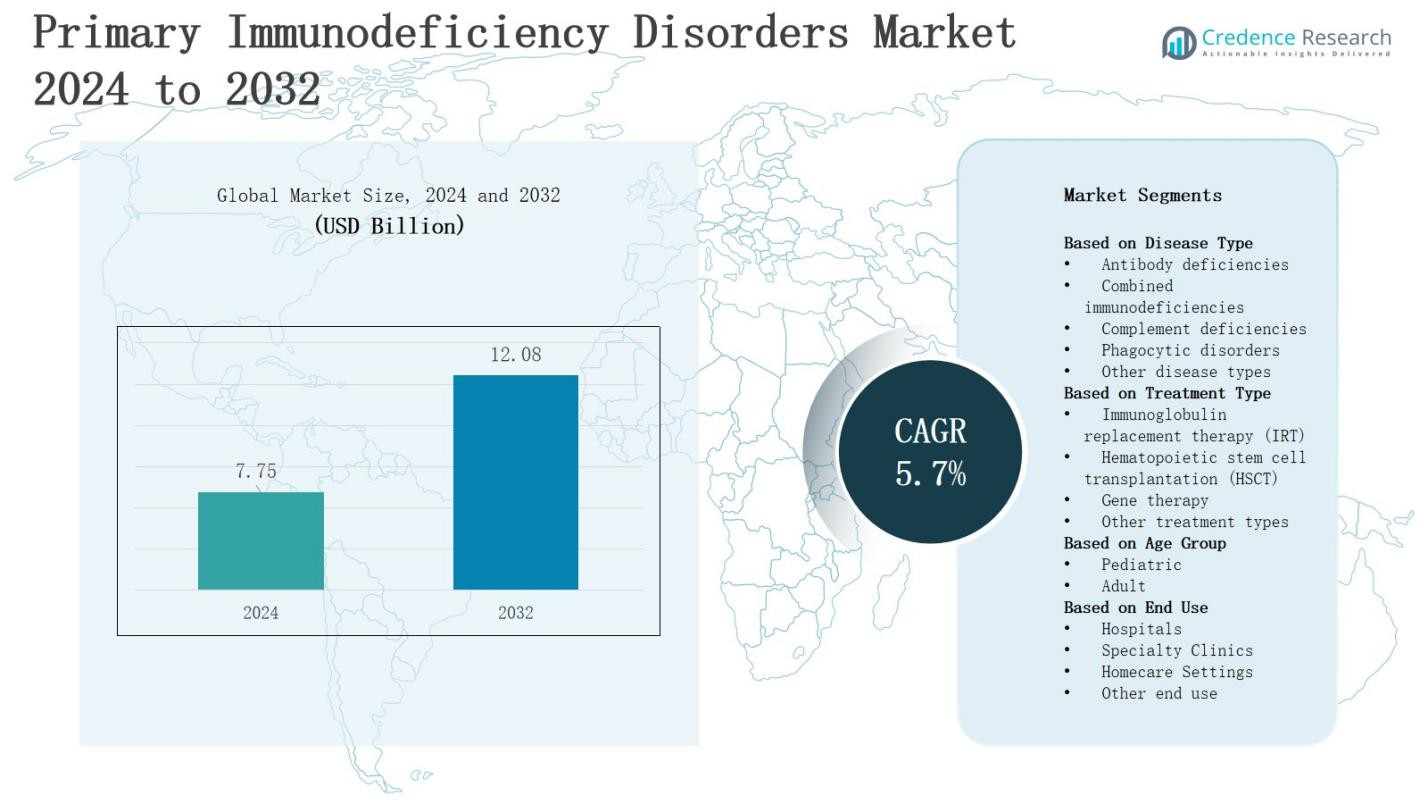

In the primary immunodeficiency disorders market, the revenue is projected to grow from USD 7.75 billion in 2024 to USD 12.08 billion by 2032, registering a CAGR of 5.7%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Primary Immunodeficiency Disorders Market Size 2024 |

USD 7.75 Billion |

| Primary Immunodeficiency Disorders Market, CAGR |

5.7% |

| Primary Immunodeficiency Disorders Market Size 2032 |

USD 12.08 Billion |

The primary immunodeficiency disorders market is driven by the rising prevalence of genetic and autoimmune disorders, increasing awareness of early diagnosis, and growing adoption of advanced therapies such as immunoglobulin replacement and gene therapy. Technological advancements in diagnostics, including next-generation sequencing, enhance accurate detection and personalized treatment strategies. Expanding healthcare infrastructure, supportive reimbursement policies, and increased funding for research further stimulate market growth. Additionally, the rising demand for novel biologics and targeted therapies, coupled with growing patient awareness about treatment options, is shaping trends, encouraging innovation, and fostering competitive developments across the global primary immunodeficiency disorders market.

The primary immunodeficiency disorders market demonstrates strong growth across key regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America leads with advanced healthcare infrastructure and high therapy adoption, while Europe benefits from robust government support and patient advocacy. Asia Pacific shows expanding access and rising awareness, and Latin America gradually improves treatment availability. The Middle East & Africa experiences steady growth through urban healthcare expansion. Key players driving the market include ADMA Biologics, Baxter International, Biotest (Grifol Group), Bluebird Bio, CSL Behring, F. Hoffmann La Roche, Leadiant Biosciences, Medac, Miltenyi Biotec, Takeda Pharmaceutical, Octapharma, and Orchard Therapeutics.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The primary immunodeficiency disorders market is projected to grow from USD 7.75 billion in 2024 to USD 12.08 billion by 2032, registering a CAGR of 5.7%.

- Rising prevalence of genetic and autoimmune disorders, early diagnosis awareness, and adoption of advanced therapies such as immunoglobulin replacement and gene therapy drive market growth.

- Technological advancements in diagnostics, including next-generation sequencing, improve accurate detection and enable personalized treatment strategies.

- North America leads the market with 40% share due to advanced healthcare infrastructure and high therapy adoption, followed by Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%).

- Key segments include antibody deficiencies (40% share), immunoglobulin replacement therapy (45% share), and the pediatric age group (55% share), supported by early intervention, targeted treatments, and ongoing research initiatives.

Market Drivers

Rising Prevalence of Genetic and Autoimmune Disorders

The primary immunodeficiency disorders market is significantly influenced by the increasing prevalence of genetic and autoimmune disorders worldwide. It drives demand for advanced diagnostic tools and effective treatment options. Growing patient populations require timely detection and personalized therapy to prevent severe complications. Enhanced screening programs and awareness campaigns encourage early diagnosis. Healthcare providers focus on implementing comprehensive treatment protocols. This trend accelerates investment in innovative therapies and broadens access to specialized care. Patient advocacy groups further support education and awareness initiatives.

- For instance, the Centers for Disease Control and Prevention (CDC) reports that over 4 million Americans live with an autoimmune disease diagnosis each year, which substantially increases the reliance on immunology-based therapies and diagnostics.

Advancements in Therapeutics and Diagnostics

The market benefits from continuous advancements in therapeutics and diagnostic technologies. It includes developments in immunoglobulin replacement therapy, targeted biologics, and gene therapy. Improved diagnostic tools, such as next-generation sequencing, support accurate identification of specific disorders. Pharmaceutical companies invest heavily in research and development to bring novel treatments to patients. Healthcare systems integrate advanced diagnostics to enable precision medicine. These innovations enhance patient outcomes, reduce hospitalizations, and expand treatment options across diverse populations.

- For instance, Neurotech received US approval in 2025 for Encelto, an intraocular implant gene therapy that restores partial vision in patients with macular telangiectasia type 2.

Growing Healthcare Infrastructure and Supportive Policies

Expanding healthcare infrastructure and supportive reimbursement policies drive market growth. It enables wider access to specialized treatments and diagnostic services. Governments and private organizations increase funding for rare disease research and patient support programs. Hospitals and clinics improve capabilities to manage complex immunodeficiency cases efficiently. Insurance coverage and financial assistance programs reduce treatment costs. Enhanced distribution networks ensure timely availability of therapies. These factors encourage market expansion and facilitate adoption of cutting-edge medical solutions.

Rising Awareness and Patient Advocacy

Rising awareness among patients, caregivers, and healthcare professionals supports market development. It emphasizes the importance of early diagnosis, treatment adherence, and lifestyle management. Patient advocacy groups play a critical role in educating communities about available therapies. Educational initiatives promote understanding of rare immunodeficiency conditions. Pharmaceutical companies collaborate with advocacy organizations to improve outreach. These efforts increase therapy adoption, encourage research participation, and stimulate demand for innovative treatment solutions globally.

Market Trends

Integration of Advanced Gene and Cell Therapies

The primary immunodeficiency disorders market shows strong trends in adopting advanced gene and cell therapies. It enables precise correction of underlying genetic defects, offering long-term solutions for patients. Biopharmaceutical companies focus on developing targeted gene-editing technologies and autologous cell therapies. Hospitals implement specialized programs to deliver these therapies safely. Regulatory approvals for novel treatments expand treatment options. Research collaborations accelerate innovation. Patient access to cutting-edge therapies improves clinical outcomes and overall quality of life.

- For instance, CRISPR Therapeutics and Vertex have reported promising results with ex vivo gene-edited therapies such as Casgevy (exagamglogene autotemcel), approved for sickle cell disease in 2023, underscoring the expanding role of regulatory greenlights in advancing cell- and gene-based treatments.

Expansion of Home-Based and Self-Administered Treatments

The market increasingly emphasizes home-based and self-administered treatment models. It allows patients to receive immunoglobulin therapy and supportive care outside hospital settings. Healthcare providers promote patient training programs to ensure safe administration. Pharmaceutical companies develop user-friendly delivery systems to enhance compliance. Remote monitoring technologies support treatment adherence and reduce complications. This trend reduces hospitalization burden and healthcare costs. Patient convenience and flexibility stimulate adoption of home-based therapies across regions.

- For instance, CSL Behring’s Hizentra® (approved by the FDA in 2010) is widely used for at-home subcutaneous immunoglobulin therapy, supported by self-administration training modules provided to patients.

Adoption of Digital Health and Telemedicine Platforms

The primary immunodeficiency disorders market integrates digital health tools and telemedicine platforms to improve care management. It enables real-time monitoring, virtual consultations, and remote patient support. Electronic health records enhance data sharing between specialists and primary care providers. Mobile apps help track symptoms and treatment adherence. Telemedicine expands access in rural and underserved regions. Healthcare systems utilize analytics to optimize treatment plans. Digital solutions streamline communication, improve patient engagement, and increase efficiency across care pathways.

Focus on Personalized Medicine and Precision Diagnostics

The market trends emphasize personalized medicine and precision diagnostics for better patient outcomes. It relies on genomic profiling and biomarker identification to guide treatment decisions. Pharmaceutical companies develop targeted therapies tailored to individual patient needs. Diagnostic labs adopt high-throughput sequencing technologies to detect rare immunodeficiency conditions. Personalized approaches minimize adverse effects and enhance therapy effectiveness. Healthcare providers implement customized treatment plans. These strategies improve patient quality of life, reduce hospitalization, and strengthen clinical decision-making across the global market.

Market Challenges Analysis

High Treatment Costs and Limited Access in Emerging Regions

The primary immunodeficiency disorders market faces challenges due to high treatment costs and limited access in emerging regions. It restricts patient adoption of advanced therapies, including immunoglobulin replacement and gene therapy. Healthcare infrastructure in low-income areas often lacks specialized facilities and trained professionals. Insurance coverage remains inconsistent, increasing out-of-pocket expenses for patients. Supply chain limitations and regulatory hurdles delay availability of critical therapies. These factors create disparities in treatment access and hinder overall market growth. Efforts to expand affordability and distribution channels remain critical for broader adoption.

Complex Diagnosis and Limited Awareness Among Healthcare Providers

The market encounters challenges from complex diagnosis and limited awareness among healthcare providers. It leads to delayed identification of rare immunodeficiency conditions, which can worsen patient outcomes. Standardized diagnostic protocols remain scarce in several regions, complicating early intervention. Misdiagnosis or underdiagnosis reduces therapy effectiveness and increases healthcare burden. Education programs for clinicians and diagnostic training initiatives remain insufficient. Lack of comprehensive epidemiological data further limits informed decision-making. Addressing these barriers is essential to improve disease detection and optimize patient care globally.

Market Opportunities

Expansion of Gene Therapy and Novel Biologics

The primary immunodeficiency disorders market presents significant opportunities through the development of gene therapy and novel biologics. It allows treatment of underlying genetic defects and rare immunodeficiency conditions with long-term efficacy. Biopharmaceutical companies invest in research to develop targeted therapies and personalized treatment solutions. Collaboration between academic institutions and industry accelerates innovation. Regulatory approvals for breakthrough therapies create new avenues for patient access. Expansion in this segment can enhance clinical outcomes and drive market growth. Increasing demand for curative therapies encourages continued investment and technological advancement.

Growth in Emerging Markets and Patient Awareness Initiatives

The market offers opportunities in emerging regions due to rising patient awareness and improving healthcare infrastructure. It supports expansion of diagnostic services and access to specialized therapies. Healthcare providers implement educational programs to enhance understanding of early detection and treatment options. Telemedicine and digital health platforms facilitate remote consultation and monitoring. Government initiatives and funding programs support rare disease management. Market penetration in these regions can increase therapy adoption and generate revenue growth. Enhanced outreach and advocacy initiatives strengthen patient engagement and overall market potential.

Market Segmentation Analysis:

By Disease Type

In the primary immunodeficiency disorders market, the antibody deficiencies segment dominates with an estimated market share of 40%. It benefits from high prevalence rates of conditions such as X-linked agammaglobulinemia and common variable immunodeficiency. Early diagnosis and established treatment protocols drive consistent demand for therapies targeting antibody deficiencies. Complement deficiencies, combined immunodeficiencies, phagocytic disorders, and other disease types collectively account for the remaining 60%, supported by growing awareness, advanced diagnostic capabilities, and increasing research investments.

- For instance, Octapharma’s Cutaquig, approved by the FDA in 2018, offers another subcutaneous immunoglobulin option, broadening therapy accessibility for patients with primary immunodeficiencies.

By Treatment Type

Immunoglobulin replacement therapy (IRT) leads the market by treatment type with a share of 45%. It remains the preferred first-line therapy due to proven efficacy in managing recurrent infections and improving patient quality of life. Hematopoietic stem cell transplantation (HSCT) and gene therapy collectively account for 35%, driven by increasing adoption of curative approaches for severe immunodeficiency cases. Other treatment types, including supportive therapies, comprise the remaining 20%, supported by growing clinical trials and evolving therapeutic innovations.

- For instance, Orchard Therapeutics’ Strimvelis, approved in Europe, achieved over 90% overall survival in patients with ADA-SCID following gene therapy treatment.

By Age Group

The pediatric segment holds a dominant market share of 55% within the primary immunodeficiency disorders market. It reflects the higher incidence of congenital immunodeficiency conditions detected in childhood. Early intervention, targeted therapies, and pediatric-focused healthcare infrastructure contribute to strong demand in this group. The adult segment accounts for 45%, supported by rising awareness of late-onset immunodeficiencies, improved diagnostics, and expanding access to advanced treatments such as gene therapy and IRT. Both segments benefit from ongoing research and patient support initiatives.

Segments:

Based on Disease Type

- Antibody deficiencies

- Combined immunodeficiencies

- Complement deficiencies

- Phagocytic disorders

- Other disease types

Based on Treatment Type

- Immunoglobulin replacement therapy (IRT)

- Hematopoietic stem cell transplantation (HSCT)

- Gene therapy

- Other treatment types

Based on Age Group

Based on End Use

- Hospitals

- Specialty Clinics

- Homecare Settings

- Other end use

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds the largest share in the primary immunodeficiency disorders market with 40%. It benefits from well-established healthcare infrastructure, advanced diagnostic technologies, and strong adoption of immunoglobulin replacement therapy and gene therapy. High prevalence of rare immunodeficiency conditions and substantial investment in research and development drive market growth. Favorable reimbursement policies and patient support programs improve treatment accessibility. Pharmaceutical companies actively collaborate with hospitals and academic institutions to launch innovative therapies. Awareness campaigns and early screening programs strengthen disease detection and management. The region remains a hub for clinical trials and regulatory approvals.

Europe

Europe accounts for 25% of the primary immunodeficiency disorders market. It benefits from robust healthcare systems, government funding for rare diseases, and widespread access to advanced therapies. Strong patient advocacy networks support awareness and early diagnosis, increasing therapy adoption. Research initiatives in gene therapy and biologics drive innovation. Healthcare providers integrate specialized treatment protocols to improve patient outcomes. Regional regulatory frameworks facilitate the approval of new therapies. Continuous expansion of diagnostic facilities and patient education programs enhances market penetration.

Asia Pacific

Asia Pacific represents 20% of the primary immunodeficiency disorders market. It experiences rising awareness of immunodeficiency disorders and expanding healthcare infrastructure in countries like Japan, China, and India. It benefits from growing adoption of immunoglobulin replacement therapy and gradual introduction of gene therapy solutions. Increasing government initiatives for rare disease management and improved diagnostic capabilities support market growth. Pharmaceutical companies focus on regional collaborations to enhance access to advanced treatments. Investment in training healthcare professionals strengthens patient care. Urban centers see greater therapy adoption, while rural areas gradually gain access to specialized care.

Latin America

Latin America holds 10% of the primary immunodeficiency disorders market. It shows gradual growth driven by increasing awareness, improving healthcare infrastructure, and government initiatives for rare disease management. Limited access to advanced therapies challenges market expansion, but growing investments in healthcare facilities support gradual improvement. Patient advocacy groups promote early diagnosis and treatment adherence. Companies focus on partnerships to expand therapy availability. Training programs for clinicians enhance treatment quality. Rising participation in clinical studies encourages adoption of innovative therapies.

Middle East & Africa

Middle East & Africa accounts for 5% of the primary immunodeficiency disorders market. It faces challenges from limited healthcare infrastructure and low awareness levels, restricting therapy adoption. It benefits from government programs to improve rare disease management and expanding urban healthcare facilities. International collaborations help provide access to immunoglobulin therapies and emerging gene therapies. Investment in diagnostic technologies enhances early detection. Educational initiatives aim to improve clinician expertise. Increasing support for patient advocacy and research fosters gradual market growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Miltenyi Biotec

- Octapharma

- Bluebird Bio

- Baxter International

- CSL Behring

- Hoffmann La Roche

- ADMA Biologics

- Takeda Pharmaceutical

- Leadiant Biosciences

- Biotest (Grifol Group)

- Medac

- Orchard Therapeutics

Competitive Analysis

The primary immunodeficiency disorders market exhibits a highly competitive landscape driven by continuous innovation and strategic collaborations. It features key players including ADMA Biologics, Baxter International, Biotest (Grifol Group), Bluebird Bio, CSL Behring, F. Hoffmann La Roche, Leadiant Biosciences, Medac, Miltenyi Biotec, Takeda Pharmaceutical, Octapharma, and Orchard Therapeutics. Companies focus on developing advanced therapies such as immunoglobulin replacement, gene therapy, and targeted biologics to address diverse patient needs. Strategic partnerships, mergers, and acquisitions help expand geographic reach and strengthen product portfolios. Heavy investment in research and development enables rapid introduction of novel treatments. Competitive differentiation relies on therapy efficacy, safety, and patient support services. Continuous engagement with healthcare providers and patient advocacy groups fosters brand recognition and market loyalty. It drives innovation, enhances clinical outcomes, and supports sustainable growth across the global market.

Recent Developments

- In April 2025, ADMA Biologics received U.S. FDA approval for an innovative immunoglobulin production process that increases antibody yields by approximately 20% from the same plasma volume.

- In June 2024, Grifols’ Biotest received U.S. FDA approval for Yimmugo®, an innovative intravenous immunoglobulin therapeutic designed to treat primary immunodeficiencies. The launch of Yimmugo® is expected to enhance treatment options for patients with these conditions.

- In early 2025, Bluebird Bio announced the completion of its acquisition by The Carlyle Group and SK Holdings. This strategic move aims to accelerate the development and commercialization of gene therapies for severe genetic diseases, including primary immunodeficiencies.

Market Concentration & Characteristics

The primary immunodeficiency disorders market demonstrates a moderately concentrated structure, with several global and regional players holding significant shares. It features key companies such as ADMA Biologics, Baxter International, Biotest (Grifol Group), Bluebird Bio, CSL Behring, F. Hoffmann La Roche, Leadiant Biosciences, Medac, Miltenyi Biotec, Takeda Pharmaceutical, Octapharma, and Orchard Therapeutics. Market concentration reflects a focus on innovation, advanced therapies, and specialized treatment solutions for rare immunodeficiency conditions. Companies compete through research and development of immunoglobulin replacement therapies, gene therapies, and targeted biologics. Strategic partnerships, mergers, and acquisitions support portfolio expansion and geographic reach. It relies on high-quality manufacturing, regulatory compliance, and strong clinician engagement to maintain market position. Patient support programs and awareness initiatives further strengthen competitiveness. The market balances innovation, accessibility, and treatment efficacy, driving steady growth while encouraging new entrants to explore niche opportunities.

Report Coverage

The research report offers an in-depth analysis based on Disease Type, Treatment Type, Age Group, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The primary immunodeficiency disorders market will witness increased adoption of gene therapies and targeted biologics.

- Early diagnosis and personalized treatment approaches will gain greater emphasis across patient populations.

- Expansion of healthcare infrastructure in emerging regions will improve access to advanced therapies.

- Technological advancements in diagnostics will enable faster and more accurate disease detection.

- Patient awareness and advocacy programs will drive demand for specialized treatments.

- Pharmaceutical companies will focus on developing novel therapies for rare and complex immunodeficiencies.

- Home-based treatment models and self-administration options will become more prevalent.

- Strategic collaborations and partnerships will strengthen market presence and global reach.

- Regulatory approvals and government initiatives will support faster introduction of innovative therapies.

- Investment in research and clinical trials will continue to enhance treatment efficacy and patient outcomes.