Market Overview

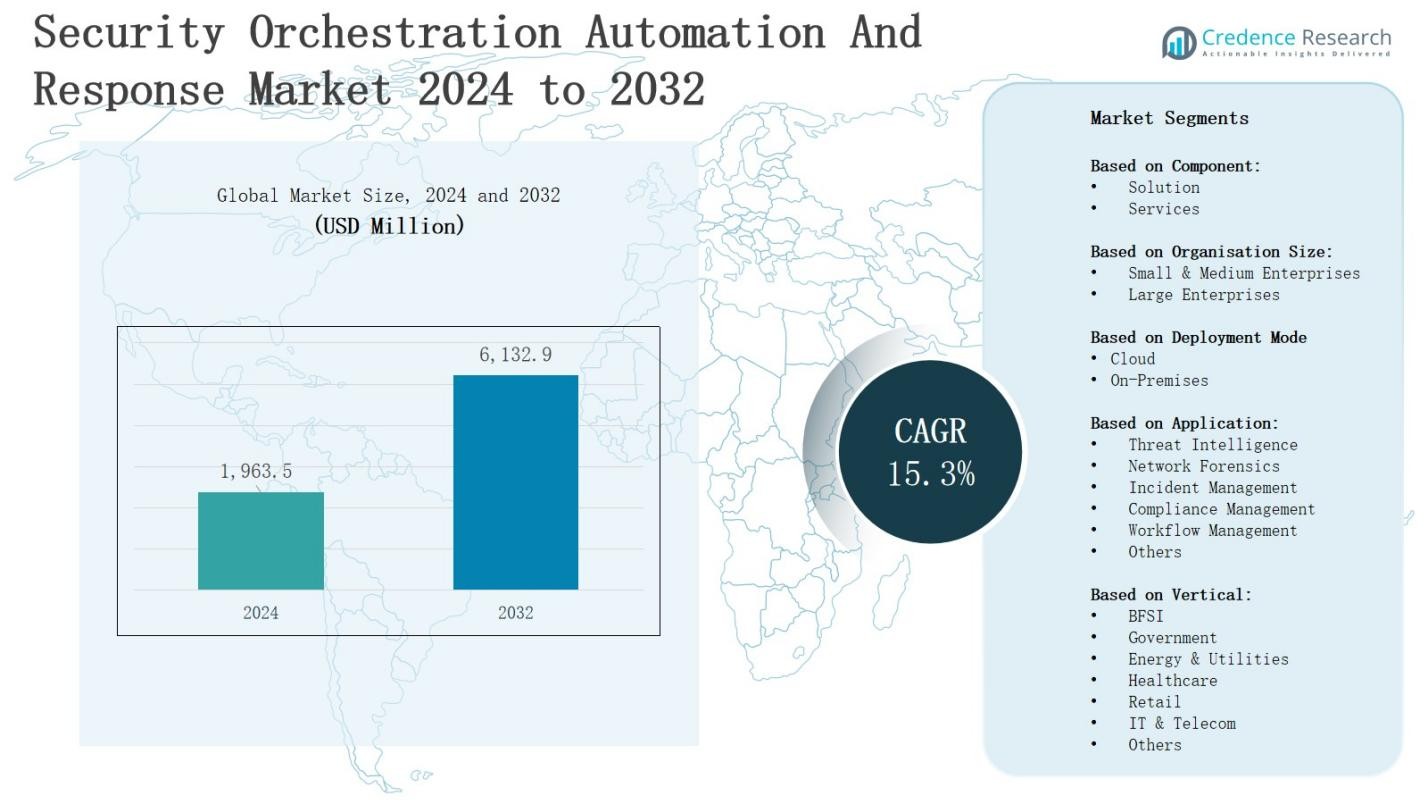

The security orchestration automation and response market is projected to grow from USD 1,963.5 million in 2024 to USD 6,132.9 million by 2032, registering a CAGR of 15.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Security Orchestration Automation And Response Market Size 2024 |

USD 1,963.5 Million |

| Security Orchestration Automation And Response Market, CAGR |

15.3% |

| Security Orchestration Automation And Response Market Size 2032 |

USD 6,132.9 Million |

The security orchestration automation and response (SOAR) market is driven by rising cyber threats, growing regulatory compliance needs, and the demand for faster incident response. Organizations adopt SOAR solutions to reduce manual workloads, streamline security processes, and improve threat detection accuracy. The increasing complexity of hybrid IT environments and the shortage of skilled cybersecurity professionals further accelerate adoption. Key trends include the integration of artificial intelligence and machine learning for advanced analytics, expansion of cloud-based SOAR platforms, and growing emphasis on automation to enhance efficiency. These dynamics position SOAR as a critical component of modern cybersecurity strategies.

The security orchestration automation and response market shows diverse regional dynamics, with North America leading at 38% share, supported by advanced cybersecurity adoption. Europe holds 27%, driven by strict regulations, while Asia-Pacific accounts for 22% as the fastest-growing region. Latin America captures 7%, supported by rising digital penetration, and the Middle East & Africa contribute 6% with growing investments in critical infrastructure security. Key players include IBM, Cisco Systems, Inc., Splunk Inc., FireEye, Rapid7, Swimlane, LLC, Tufin, ThreatConnect, DFLabs, Exabeam, and Shuffle.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The security orchestration automation and response market is projected to grow from USD 1,963.5 million in 2024 to USD 6,132.9 million by 2032, registering a strong 15.3% CAGR.

- Solutions dominate with 65% share in 2024, offering end-to-end orchestration and automation, while services at 35% remain vital for deployment, customization, and training to enhance long-term operational efficiency.

- Large enterprises lead with 62% share in 2024, supported by higher budgets and complex infrastructures, while SMEs at 38% increasingly adopt cloud-based SOAR due to affordability and rising cyberattacks.

- Cloud deployment holds 58% share in 2024, driven by scalability, cost efficiency, and hybrid workforce models, while on-premises at 42% stays critical in finance and government for data control.

- Regionally, North America leads with 38% share, Europe holds 27%, Asia-Pacific accounts for 22%, Latin America captures 7%, and Middle East & Africa contribute 6%, reflecting diverse adoption drivers globally.

Market Drivers

Rising Cybersecurity Threats and Growing Attack Surface

The security orchestration automation and response market is expanding due to escalating cyberattacks, including ransomware, phishing, and advanced persistent threats. Organizations face complex risks as digital transformation accelerates and connected systems increase. It enables faster detection and response to prevent breaches and minimize downtime. The growing adoption of IoT devices and cloud-based infrastructures broadens the attack surface. SOAR solutions provide automation to handle large-scale threats efficiently, strengthening resilience across industries.

- For instance, Amazon Web Services (AWS) disclosed in 2020 that it defended against a massive 2.3 Tbps DDoS attack, one of the largest recorded, showing how cloud-scale infrastructures are prime targets.

Regulatory Compliance and Governance Requirements

Tightening regulations and data protection laws drive adoption in the security orchestration automation and response market. Industries must comply with GDPR, HIPAA, and other mandates that enforce strict monitoring and reporting of security incidents. It helps organizations maintain compliance by automating workflows and generating audit-ready documentation. Rising penalties for non-compliance push firms to deploy robust systems. SOAR platforms provide consistent governance, reducing human error and ensuring standardized responses to incidents.

- For instance, in 2023, Microsoft added regulatory compliance automation features to its Sentinel platform, helping enterprises map incidents directly to GDPR reporting requirements.

Workforce Shortages and Need for Operational Efficiency

The shortage of skilled cybersecurity professionals significantly influences the security orchestration automation and response market. Enterprises struggle to manage rising alerts and complex incidents with limited staff. It allows security teams to automate repetitive tasks and prioritize high-value incidents. Automated workflows increase efficiency and reduce analyst fatigue. Organizations benefit from faster decision-making, lower response times, and improved collaboration across teams. These advantages strengthen demand for SOAR deployments globally.

Integration of AI and Advanced Analytics

The integration of artificial intelligence and machine learning is a vital driver in the security orchestration automation and response market. It enables predictive threat intelligence, real-time correlation, and adaptive response strategies. AI-driven platforms analyze vast data streams to detect anomalies and hidden risks. Organizations adopt AI to improve accuracy and limit false positives. Automated playbooks enhance incident handling across hybrid IT environments. This integration supports faster, smarter, and more proactive security operations.

Market Trends

Adoption of Cloud-Based SOAR Platforms

The security orchestration automation and response market is witnessing strong momentum toward cloud-based platforms. Organizations seek scalable, flexible, and cost-efficient solutions that integrate with multi-cloud environments. It supports remote workforces by enabling centralized monitoring and faster deployment of updates. Cloud-native SOAR tools provide seamless integration with existing security infrastructure. Vendors increasingly develop SaaS-based offerings to reduce operational overheads. This trend reflects the growing demand for agile and accessible security solutions across enterprises.

- For instance, Palo Alto Networks’ Cortex XSOAR offers automation-first response capabilities with over 1,000 integrations, helping security teams reduce manual processes and accelerate incident investigation.

Growing Integration with Threat Intelligence Feeds

Integration with advanced threat intelligence feeds represents a key trend in the security orchestration automation and response market. Security teams require real-time visibility into global threat landscapes to strengthen incident detection. It enables correlation of alerts with contextual data for improved decision-making. Enhanced threat feeds enrich automated playbooks with actionable insights. Organizations gain improved resilience by aligning responses with evolving risks. This trend accelerates the adoption of advanced SOAR platforms across industries.

- For instance, Splunk SOAR integrates with Recorded Future’s threat intelligence platform, allowing organizations to automatically correlate internal events with external threat indicators for faster triage.

Expansion of AI and Machine Learning Capabilities

Artificial intelligence and machine learning capabilities are transforming the security orchestration automation and response market. It empowers platforms to predict, prioritize, and adapt responses to emerging threats. AI-driven systems reduce false positives while identifying hidden attack patterns. Machine learning enhances playbooks by continuously refining responses through historical analysis. Organizations leverage these advancements to optimize analyst workloads. This trend reinforces SOAR’s role as a proactive and intelligence-driven component of cybersecurity frameworks.

Emphasis on Automated Incident Response and Collaboration

The growing emphasis on automated response and collaborative workflows defines the security orchestration automation and response market. It enables faster handling of incidents by integrating multiple security tools into unified dashboards. Automated response reduces dependency on manual intervention and speeds up containment. Collaborative functions allow seamless communication among security teams, IT staff, and management. Organizations strengthen security posture through shared visibility and coordinated response. This trend shapes SOAR as a central hub in security ecosystems.

Market Challenges Analysis

High Implementation Costs and Integration Complexities

The security orchestration automation and response market faces significant challenges related to high implementation costs and integration complexities. Many organizations struggle to allocate budgets for advanced SOAR platforms, particularly small and mid-sized enterprises. It often requires specialized expertise, extensive customization, and integration with existing tools such as SIEM and endpoint detection systems. These requirements increase deployment time and operational expenses. Vendors must address affordability and simplify integration to expand adoption across diverse industries.

Limited Awareness and Resistance to Automation Adoption

A lack of awareness and resistance to automation remain barriers within the security orchestration automation and response market. Decision-makers often hesitate to trust automated platforms for critical incident response, fearing loss of control and potential misconfigurations. It limits the pace of adoption, particularly in traditional industries with established manual processes. Training and skill gaps further restrict effective use of SOAR solutions. Overcoming these concerns requires strong vendor support, user education, and proven case outcomes to build confidence.

Market Opportunities

Expansion Across Emerging Economies and Mid-Sized Enterprises

The security orchestration automation and response market presents strong opportunities across emerging economies and mid-sized enterprises. Rapid digital transformation in regions such as Asia-Pacific, Latin America, and the Middle East creates demand for advanced cybersecurity frameworks. It enables organizations to address rising threats without overburdening limited security staff. Vendors offering scalable and cost-effective solutions can capture this segment. Growing adoption of cloud services and expanding e-commerce ecosystems further enhance opportunities for SOAR implementation.

Growth Potential in AI-Driven and Industry-Specific Solutions

Opportunities in the security orchestration automation and response market are expanding through AI-driven and industry-focused solutions. It allows organizations in sectors such as healthcare, finance, and energy to manage sector-specific compliance needs while strengthening security posture. AI integration provides predictive threat detection, improved analytics, and adaptive responses. Vendors tailoring platforms to industry regulations and workflows gain competitive advantage. The demand for automated, intelligent, and vertical-specific SOAR tools positions the market for sustained long-term growth.

Market Segmentation Analysis:

By Component

Based on component, solutions dominate the security orchestration automation and response market with around 65% share in 2024, while services hold 35%. Solutions lead due to their ability to deliver end-to-end orchestration, automation, and response functions that integrate across diverse security environments. It enables faster adoption as organizations seek scalable platforms to reduce manual workloads and improve incident response. Services remain important for deployment, customization, and training, driving long-term platform efficiency.

- For instance, IBM Security SOAR enables automated workflows and has been deployed by enterprises to handle phishing and malware incidents at scale through its playbook-driven approach.

By Organisation Size

By organization size, large enterprises account for 62% share in 2024, while small and medium enterprises hold 38%. Large enterprises dominate due to higher cybersecurity budgets, complex IT infrastructures, and the need for compliance with stringent regulations. It supports demand for advanced SOAR platforms to manage large-scale incidents and diverse threat landscapes. SMEs are steadily increasing adoption, driven by rising cyberattacks and availability of cost-effective, cloud-based SOAR solutions.

- For instance, JPMorgan Chase invests over $600 million annually in cybersecurity, deploying automation and orchestration tools to manage thousands of daily incident alerts.

By Deployment Mode

Based on deployment mode, the cloud segment leads with 58% share in 2024, while on-premises deployment accounts for 42%. Cloud dominates due to its scalability, cost-efficiency, and ability to support remote and hybrid workforce models. It allows organizations to reduce infrastructure costs while ensuring rapid deployment and seamless updates. On-premises solutions remain significant in industries such as finance and government where data privacy and regulatory compliance demand higher control and security.

Segments:

Based on Component:

Based on Organisation Size:

- Small & Medium Enterprises

- Large Enterprises

Based on Deployment Mode

Based on Application:

- Threat Intelligence

- Network Forensics

- Incident Management

- Compliance Management

- Workflow Management

- Others

Based on Vertical:

- BFSI

- Government

- Energy & Utilities

- Healthcare

- Retail

- IT & Telecom

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America dominates the security orchestration automation and response market with a 38% share in 2024. The region leads due to advanced cybersecurity infrastructure, high adoption of cloud services, and strong presence of global vendors. It benefits from early adoption of AI-driven solutions and integration with threat intelligence platforms. Regulatory frameworks such as HIPAA and CCPA push enterprises to deploy SOAR systems. Large enterprises and government institutions drive sustained investments, ensuring steady growth across the region.

Europe

Europe accounts for a 27% share in 2024, driven by strict data protection regulations such as GDPR and the growing threat of cyberattacks. The security orchestration automation and response market in Europe is strengthened by strong demand from BFSI, government, and healthcare sectors. It supports incident response automation to comply with strict reporting timelines. Adoption is high among enterprises seeking standardized workflows and governance. The presence of regional vendors further enhances adoption, fueling consistent expansion.

Asia-Pacific

Asia-Pacific holds a 22% share in 2024, making it the fastest-growing regional segment. The security orchestration automation and response market here is driven by rapid digital transformation, rising cybercrime, and growing investments in IT infrastructure. It benefits from large-scale adoption across sectors such as telecom, e-commerce, and banking. Rising government initiatives to strengthen cybersecurity frameworks further support market growth. SMEs increasingly embrace cloud-based SOAR solutions, creating strong opportunities for vendors targeting emerging economies.

Latin America

Latin America represents a 7% share in 2024, with growth supported by rising digital penetration and expanding e-commerce activities. The security orchestration automation and response market in this region is influenced by increasing ransomware and phishing attacks targeting enterprises. It creates demand for automated platforms that can handle complex incidents with limited security staff. Industries such as BFSI and retail are adopting SOAR platforms to strengthen resilience. The region shows potential for accelerated adoption with cloud-driven solutions.

Middle East & Africa

The Middle East & Africa account for a 6% share in 2024, driven by rising investments in digital infrastructure and national cybersecurity programs. The security orchestration automation and response market in this region is influenced by growing threats to oil and gas, government, and financial sectors. It supports critical infrastructure protection through automation of response workflows. Enterprises adopt SOAR platforms to reduce dependency on manual monitoring. Strong government support positions the region for steady adoption in the coming years.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- IBM

- FireEye

- Cisco Systems, Inc.

- Rapid7

- Splunk Inc.

- Swimlane, LLC

- Tufin

- ThreatConnect

- DFLabs

- Exabeam

- Shuffle

Competitive Analysis

The security orchestration automation and response market is highly competitive with global and regional players focusing on innovation, integration, and scalability. IBM, Cisco Systems, Inc., and Splunk Inc. lead the market with comprehensive SOAR platforms that integrate AI, threat intelligence, and cloud capabilities. FireEye and Rapid7 strengthen their portfolios with advanced detection and response functions tailored for enterprises facing evolving threats. Swimlane, LLC and Exabeam focus on user-friendly automation and analytics-driven workflows to improve operational efficiency. ThreatConnect, Tufin, and DFLabs emphasize orchestration and compliance management solutions that address governance and regulatory needs across industries. Shuffle builds traction by offering open-source, lightweight orchestration tools for SMEs seeking cost-effective alternatives. It remains shaped by rising cybersecurity threats, complex IT environments, and the demand for automation in incident management. Market players compete by expanding partnerships, investing in R&D, and offering flexible deployment models across cloud and on-premises environments to capture diverse customer bases. Strategic differentiation relies on delivering faster response times, seamless integration, and tailored industry-specific use cases.

Recent Developments

- In July 2025, Palo Alto Networks announced the acquisition of CyberArk in a $25 billion cash and stock deal. The move enhances Palo Alto’s SOAR and identity security capabilities by integrating privileged access and AI-driven identity solutions into its cybersecurity platform.

- In April 2025, Splunk launched Splunk SOAR as a native SaaS on Microsoft Azure, enabling automation of security workflows and faster response by integrating Azure services and third-party tools.

- In November 2023, DirectDefense launched ThreatAdvisor 3.0, a SOAR platform designed to enhance SOC efficiency by automating threat monitoring, incident response, and compliance management, including integration with other security solutions.

- In March 2025, Tines expanded its partnership with Elastic to combine Elastic’s Search AI Platform with Tines’ Workflow Automation, aiming at faster issue resolution, improved operational efficiency, and reduced costs with AI-driven analytics and automated workflows.

Report Coverage

The research report offers an in-depth analysis based on Component, Organization Size, Deployment Mode, Application, Vertical and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Growing adoption of AI-driven SOAR platforms will enhance predictive threat detection and adaptive responses.

- Cloud-based deployments will continue expanding, supporting scalability and hybrid workforce security requirements worldwide.

- Vendors will focus on industry-specific solutions tailored to healthcare, finance, energy, and government needs.

- Integration with threat intelligence feeds will strengthen real-time situational awareness and contextual decision-making processes.

- Increasing automation will reduce analyst fatigue, improving efficiency and faster incident containment across enterprises.

- Regulatory compliance requirements will drive wider deployment, ensuring consistent governance and standardized reporting processes.

- SMEs will accelerate adoption of affordable SOAR solutions to address growing cybersecurity risks and threats.

- Partnerships and acquisitions will intensify, expanding solution portfolios and strengthening market presence globally.

- Enhanced workflow automation will streamline collaboration between IT teams, security analysts, and business stakeholders.

- Demand for unified dashboards and cross-platform integration will position SOAR as a central cybersecurity hub.