Market Overview:

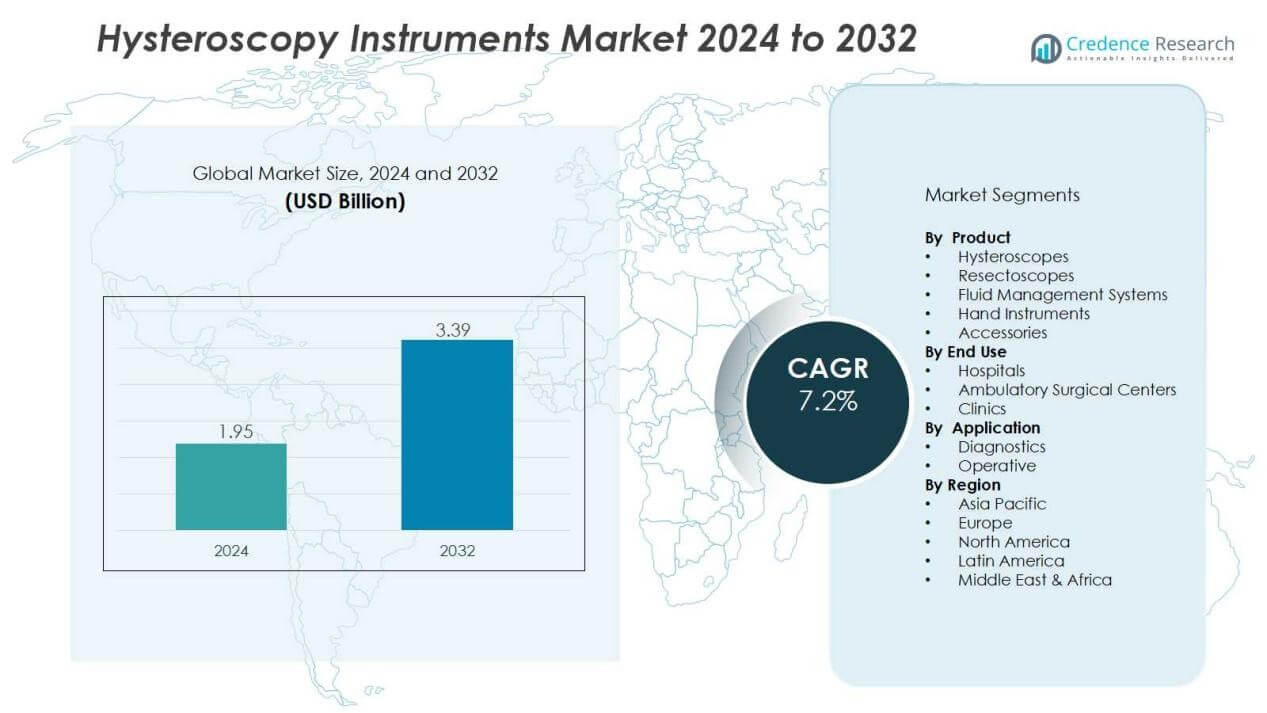

The hysteroscopy instruments market size was valued at USD 1.95 billion in 2024 and is anticipated to reach USD 3.39 billion by 2032, at a CAGR of 7.2 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Hysteroscopy Instruments Market Size 2024 |

USD 1.95 Billion |

| Hysteroscopy Instruments Market, CAGR |

7.2% |

| Hysteroscopy Instruments Market Size 2032 |

USD 3.39 Billion |

Key growth drivers include increasing awareness of women’s reproductive health, rising infertility rates, and a higher incidence of abnormal uterine bleeding. The growing preference for outpatient and day-care hysteroscopy procedures has also boosted demand for advanced instruments that improve patient outcomes while reducing recovery time. Technological innovations, such as digital imaging and disposable hysteroscopes, are improving procedure efficiency and safety. Furthermore, supportive government initiatives and expanding healthcare infrastructure in emerging economies are contributing to wider market penetration.

Regionally, North America holds a major share due to well-established healthcare facilities, high adoption of advanced medical devices, and strong presence of key manufacturers. Europe follows closely, supported by favorable reimbursement policies and growing awareness of minimally invasive treatments. The Asia-Pacific region is projected to record the fastest growth, fueled by rising healthcare investments, increasing patient pool, and rapid technology adoption in China, India, and Southeast Asia.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The hysteroscopy instruments market was valued at USD 1.95 billion in 2024 and is expected to reach USD 3.39 billion by 2032 at a CAGR of 7.2%.

- Rising incidence of gynecological disorders, including uterine fibroids and abnormal bleeding, is driving steady demand.

- Growing infertility rates linked to lifestyle changes are increasing the adoption of diagnostic hysteroscopy.

- Technological advancements such as high-definition imaging, digital platforms, and disposable hysteroscopes enhance accuracy and safety.

- High costs of advanced equipment and lack of reimbursement policies remain key barriers in emerging markets.

- North America held 38% share in 2024, supported by advanced healthcare facilities and strong presence of global players.

- Asia-Pacific secured 22% share and is projected to grow fastest due to expanding healthcare infrastructure and rising patient pool.

Market Drivers:

Market Drivers:

Rising Incidence of Gynecological Disorders and Infertility:

The hysteroscopy instruments market is driven by the increasing prevalence of conditions such as uterine fibroids, abnormal bleeding, and infertility. A growing number of women seek early diagnosis and treatment for these conditions, creating steady demand for hysteroscopic procedures. Rising infertility rates linked to lifestyle changes further expand the adoption of diagnostic hysteroscopy. It benefits both patients and clinicians by providing minimally invasive options for faster evaluation and treatment.

- For instance, in June 2022, UroViu Corp introduced the Hystero-V, a single-use hysteroscope integrated with the Always Ready platform, which eliminates equipment reprocessing and reduces average procedure setup time to less than 2 minutes.

Growing Demand for Minimally Invasive Procedures:

Patients and healthcare providers prefer minimally invasive approaches that reduce hospital stays and recovery times. The hysteroscopy instruments market benefits from this shift, as it offers safer alternatives to traditional surgical interventions. Shorter procedure durations and reduced post-operative complications increase patient satisfaction and hospital efficiency. It supports the ongoing transformation of gynecological care toward advanced outpatient settings.

- For instance, Medtronic’s TruClear system enables safe removal of intrauterine abnormalities with procedure times as short as 13 minutes, and in a multicenter evaluation, 92% of procedures were completed in a single treatment session, minimizing follow-up intervention needs.

Technological Advancements in Imaging and Instrumentation:

Innovations such as digital imaging, high-definition optics, and disposable hysteroscopes are fueling market growth. These advancements improve accuracy, safety, and ease of use during diagnostic and operative procedures. The hysteroscopy instruments market gains momentum as manufacturers integrate advanced visualization and precision tools. It enables healthcare providers to deliver more effective and reliable outcomes in both complex and routine cases.

Expanding Healthcare Infrastructure and Supportive Policies:

Emerging economies are investing heavily in healthcare infrastructure, creating opportunities for wider hysteroscope adoption. The hysteroscopy instruments market grows with increased accessibility to modern medical equipment across hospitals and clinics. Government initiatives promoting women’s health and reimbursement support further boost the uptake of advanced hysteroscopy devices. It strengthens the position of minimally invasive gynecological care as a global standard.

Market Trends:

Integration of Advanced Visualization and Digital Technologies:

The hysteroscopy instruments market is experiencing a strong trend toward advanced visualization tools that enhance accuracy and efficiency. High-definition cameras, digital imaging systems, and improved light sources are making procedures more precise and reliable. Surgeons benefit from clearer visuals, which reduce risks during diagnosis and operative interventions. Disposable hysteroscopes are also gaining ground, offering infection control and cost efficiency for outpatient centers. Integration of AI-assisted imaging and real-time data analysis further strengthens procedure outcomes. It positions digital technology as a core driver of innovation in gynecological care.

- For instance, Olympus launched its CH-S700-08-LB camera head in September 2024, featuring true 4K imaging technology that can reproduce a wide color gamut of over 1 billion colors under the ITU-R BT. 2020 standard, providing four times finer detail than conventional HD systems.

Shift Toward Outpatient and Ambulatory Care Settings:

Healthcare providers are increasingly adopting hysteroscopy procedures in outpatient and ambulatory care environments. The hysteroscopy instruments market aligns with this shift by offering compact, easy-to-use, and less invasive instruments. Patients prefer outpatient settings due to shorter recovery times and reduced healthcare costs. Hospitals and specialty clinics also benefit from improved patient throughput and resource optimization. The growing demand for office-based hysteroscopy strengthens the role of portable and disposable devices. It reflects a broader trend of decentralizing advanced care to more accessible and cost-effective environments.

- For instance, in May 2024, Minerva Surgical launched the HERizon Disposable Hysteroscope, featuring a 4.8mm outer diameter sheath for in-office procedures, supporting direct visualization polypectomy and IUD removal without the need for traditional reprocessing, thus enabling rapid patient turnover in outpatient settings.

Market Challenges Analysis:

High Cost of Equipment and Limited Accessibility in Emerging Markets:

The hysteroscopy instruments market faces challenges due to the high cost of advanced devices and imaging systems. Many hospitals in low- and middle-income regions struggle to afford these technologies, restricting access to modern gynecological care. Limited insurance coverage and lack of reimbursement policies further discourage patients from opting for minimally invasive procedures. It restricts adoption in markets where cost sensitivity is high, slowing overall growth. Manufacturers must address affordability through cost-effective solutions to ensure wider reach.

Shortage of Skilled Professionals and Patient Awareness Gaps:

A major challenge for the hysteroscopy instruments market is the shortage of trained specialists capable of performing advanced procedures. Many healthcare facilities lack expertise in handling digital imaging tools and modern hysteroscopes. Patient awareness of minimally invasive gynecological treatments also remains low in developing regions. It limits demand and reduces adoption rates despite the availability of advanced technologies. Training initiatives, awareness programs, and broader education efforts are critical to overcoming these barriers.

Market Opportunities:

Expanding Role of Outpatient and Ambulatory Care Facilities:

The hysteroscopy instruments market has significant opportunities in the expansion of outpatient and ambulatory care centers. Growing patient preference for minimally invasive, office-based procedures supports the need for compact, portable, and disposable devices. Hospitals and clinics benefit from improved efficiency, reduced procedure times, and cost savings. It creates strong potential for manufacturers to design instruments tailored for faster turnaround in outpatient settings. Rising demand for affordable solutions in urban and semi-urban regions further broadens this opportunity. Companies that focus on innovative device formats will capture a growing share of this segment.

Rising Healthcare Investments in Emerging Economies:

Rapid healthcare investments in Asia-Pacific, Latin America, and the Middle East open new avenues for growth. The hysteroscopy instruments market is well-positioned to benefit from government initiatives aimed at improving women’s health. Expanding hospital infrastructure and increasing insurance coverage support the adoption of advanced diagnostic and surgical tools. It enables wider access to minimally invasive care, especially in regions with high unmet needs. Partnerships between global manufacturers and local distributors can accelerate entry into these fast-growing markets. Companies that establish strong regional footprints will gain long-term competitive advantages.

Market Segmentation Analysis:

By Product:

The hysteroscopy instruments market is segmented into hysteroscopes, resectoscopes, fluid management systems, hand instruments, and accessories. Hysteroscopes hold the largest share due to their critical role in both diagnostic and operative procedures. Rising demand for high-definition and disposable hysteroscopes drives growth in this category. Resectoscopes also contribute significantly, supported by their use in treating fibroids and polyps. It benefits from continuous innovation in optical technologies that improve accuracy and patient safety.

- For instance, Karl Storz developed the Intrauterine Bigatti Shaver (IBS®), a morcellator with available 19 French and 24 French diameters that enables simultaneous tissue resection and removal.

By Application:

The market is divided into diagnostics and operative applications. Operative hysteroscopy dominates due to its effectiveness in managing uterine abnormalities such as adhesions, fibroids, and polyps. Diagnostics is also growing steadily, supported by rising infertility cases and increasing awareness of women’s health. It provides faster, minimally invasive evaluation of uterine conditions, improving patient outcomes. Growing preference for early detection strengthens demand across both application segments.

- For instance, in a randomized trial evaluating fluid management during operative hysteroscopy, the use of a suction-assisted fluid management system reduced the median fluid deficit to 0 mL compared with 450 mL when only gravity was employed.

By End Use:

End-use segmentation includes hospitals, ambulatory surgical centers, and clinics. Hospitals account for the largest share, supported by advanced infrastructure and availability of skilled specialists. Ambulatory surgical centers are gaining traction due to rising demand for outpatient hysteroscopy procedures. Clinics also contribute, particularly in regions with expanding private healthcare networks. It reflects the broader shift toward more accessible and cost-effective care delivery across diverse healthcare environments.

Segmentations:

By Product:

- Hysteroscopes

- Resectoscopes

- Fluid Management Systems

- Hand Instruments

- Accessories

By Application:

By End Use:

- Hospitals

- Ambulatory Surgical Centers

- Clinics

By Region:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

North America:

North America held 38% market share in 2024, making it the largest regional segment. The hysteroscopy instruments market in this region benefits from advanced healthcare infrastructure and high adoption of minimally invasive technologies. The presence of leading medical device manufacturers ensures consistent innovation and product availability. Favorable reimbursement policies encourage hospitals and clinics to integrate advanced hysteroscopy instruments. It supports rapid adoption across both diagnostic and operative procedures. Rising awareness of women’s health and early diagnosis further strengthen the regional outlook.

Europe:

Europe accounted for 29% market share in 2024, driven by supportive government policies and strong clinical adoption. The hysteroscopy instruments market in Europe is supported by well-established healthcare systems and structured reimbursement frameworks. Growing demand for minimally invasive procedures in countries such as Germany, France, and the UK drives instrument usage. Manufacturers expand presence in the region by offering innovative devices aligned with clinical needs. It benefits from rising patient awareness and growing focus on outpatient care. Increased investments in research and development further sustain growth.

Asia-Pacific:

Asia-Pacific secured 22% market share in 2024, with strong growth expected through the forecast period. The hysteroscopy instruments market is expanding in this region due to rising healthcare investments and growing patient base. Countries such as China, India, and Japan are witnessing rapid adoption of advanced gynecological instruments. Expanding hospital infrastructure and government initiatives to improve women’s health accelerate market penetration. It creates opportunities for global players to strengthen local partnerships and distribution networks. Rising disposable incomes and urbanization further contribute to the region’s growth momentum.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- KARL STORZ

- Richard Wolf GmbH

- Olympus

- Stryker

- B. Braun

- Cooper Surgical

- Medtronic

- Hologic

- Boston Scientific

- Medicon

Competitive Analysis:

The hysteroscopy instruments market is competitive, with global players driving innovation and expanding product portfolios. Key companies include KARL STORZ, Richard Wolf GmbH, Olympus, Stryker, B. Braun, and Cooper Surgical. Leading manufacturers focus on advanced hysteroscopes, resectoscopes, and digital imaging solutions to improve procedural accuracy and patient outcomes. It benefits from continuous product development, mergers, and collaborations aimed at strengthening global distribution networks. Market participants also emphasize cost-effective solutions and disposable instruments to capture demand in outpatient and ambulatory settings. Strong R&D investments, combined with training initiatives for healthcare professionals, support adoption across developed and emerging markets. Competition remains high as players work to differentiate through technology integration, product quality, and expanded after-sales support services.

Recent Developments:

- In July 2024, Richard Wolf GmbH and Photocure ASA entered into a strategic partnership to co-develop and commercialize a high-definition flexible blue light cystoscope for advanced bladder cancer diagnostics.

- In September 2025, Olympus announced the U.S. launch of the VISERA™ S OTV-S500 imaging platform for ENT and urology, integrating advanced diagnostic features.

Report Coverage:

The research report offers an in-depth analysis based on Product, Application, End Use and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The hysteroscopy instruments market will witness sustained demand due to rising cases of gynecological disorders.

- It will benefit from increasing adoption of minimally invasive procedures across hospitals and specialty clinics.

- Advancements in digital imaging and disposable hysteroscopes will drive higher procedural accuracy and safety.

- The shift toward outpatient and ambulatory care facilities will create new growth avenues for manufacturers.

- Healthcare investments in emerging economies will expand access to modern hysteroscopy equipment.

- It will gain traction through government initiatives promoting women’s health and early diagnosis programs.

- Training programs and awareness campaigns will help overcome skill gaps in advanced hysteroscopic procedures.

- Manufacturers will focus on cost-effective solutions to address affordability concerns in price-sensitive regions.

- Collaborations between global companies and regional distributors will strengthen market penetration and supply chains.

- It will evolve with integration of AI-assisted imaging and digital platforms to improve procedural efficiency.