Market Overview

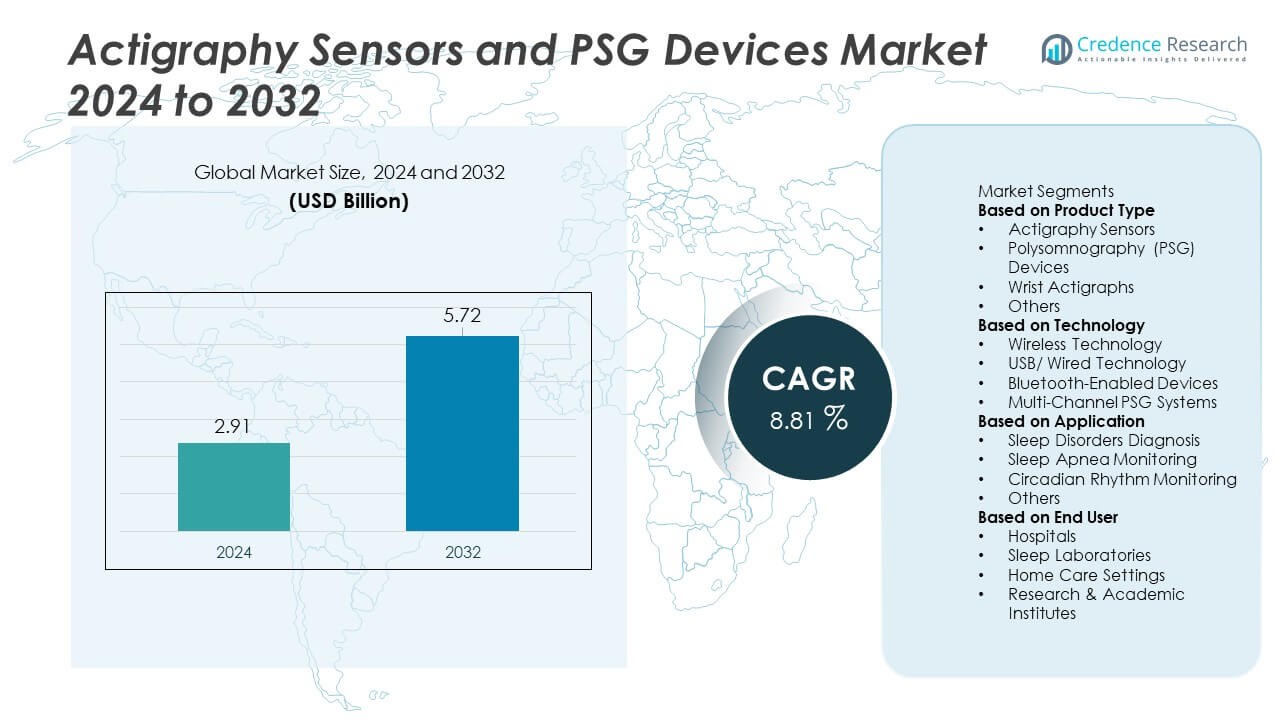

Actigraphy Sensors and PSG Devices Market size was valued at USD 2.91 billion in 2024 and is projected to reach USD 5.72 billion by 2032, expanding at a CAGR of 8.81% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Actigraphy Sensors and PSG Devices Market Size 2024 |

USD 2.91 Billion |

| Actigraphy Sensors and PSG Devices Market, CAGR |

8.81% |

| Actigraphy Sensors and PSG Devices Market Size 2032 |

USD 5.72 Billion |

The Actigraphy Sensors and PSG Devices market is shaped by leading companies such as Philips Healthcare, ResMed, Fitbit (Google), Garmin Ltd., Natus Medical Incorporated, Nihon Kohden Corporation, SOMNOmedics, ActiGraph LLC, Compumedics Limited, and Microlife Corporation, all driving advancements in clinical and home-based sleep monitoring. These players strengthen their portfolios with multi-parameter wearables, wireless PSG systems, and AI-based sleep-analysis platforms that support accurate diagnosis and long-term tracking. North America leads the market with 38% share, driven by strong digital health adoption, while Europe holds 30% share due to robust clinical infrastructure. Asia Pacific follows with 25% share, supported by rising awareness and expanding sleep-medicine services.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Actigraphy Sensors and PSG Devices market was valued at USD 2.91 billion in 2024 and is projected to reach USD 5.72 billion by 2032, expanding at a CAGR of 8.81% during the forecast period.

- Key growth drivers include rising global cases of insomnia and sleep apnea, with Actigraphy Sensors leading the product segment with 46% share due to strong adoption in home-based and long-term monitoring.

- Major trends include increasing integration of AI-driven analysis, expansion of multi-parameter wearable devices, and wider acceptance of wireless and Bluetooth-enabled systems for real-time sleep tracking.

- The competitive landscape is influenced by key players such as Philips Healthcare, ResMed, Fitbit (Google), Garmin, Natus Medical, Nihon Kohden, SOMNOmedics, ActiGraph, Compumedics, and Microlife, all focusing on accuracy, comfort, and remote monitoring capabilities.

- Regionally, North America leads with 38% share, Europe holds 30%, and Asia Pacific follows with 25%, while Latin America and Middle East & Africa account for 4% and 3%, driven by improving diagnostic access and growing awareness of sleep-health disorders.

Market Segmentation Analysis:

Market Segmentation Analysis:

By Product Type

Actigraphy Sensors held the dominant 46% share, driven by rising adoption in home-based sleep monitoring and long-term circadian rhythm assessment. These sensors offer continuous, non-invasive tracking, making them preferred for clinical studies and remote patient monitoring programs. Wrist actigraphs also gained strong traction due to comfort, portability, and higher compliance among patients. Polysomnography (PSG) devices maintained steady demand in hospital and sleep-lab settings where full-channel monitoring is required. Growth across this segment is supported by increasing sleep disorder prevalence and broader acceptance of wearable sleep-assessment tools.

- For instance, Philips Actiwatch Spectrum Pro records activity at a sampling rate of 32 Hz and stores up to 32 Mbits of raw movement data, supporting long-term studies of up to 50-60 days.

By Technology

Wireless technology accounted for the largest 52% share, supported by its ease of integration, high patient mobility, and suitability for modern sleep-monitoring workflows. Bluetooth-enabled devices expanded quickly as clinicians and users favored seamless data transfer through mobile apps. Multi-channel PSG systems remained essential in sleep laboratories for detailed physiological monitoring. USB/wired systems continued to serve baseline diagnostic needs in budget-sensitive environments. Growth across all technologies reflects rising telehealth adoption, increasing demand for home-based sleep testing, and technological advancements that improve accuracy and comfort.

- For instance, the ResMed AirView connectivity platform transmits sleep data over a cellular network and supports remote review for millions of connected devices.

By Application

Sleep disorders diagnosis dominated with a 55% share, driven by growing detection of insomnia, circadian rhythm disruptions, and behavior-linked sleep issues. Actigraphy and PSG devices play a central role in tracking long-term sleep patterns and supporting clinical decision-making. Sleep apnea monitoring followed strongly due to rising awareness of obstructive sleep apnea and expanding screening programs. Circadian rhythm monitoring gained momentum as employers and clinicians track sleep–wake patterns for shift workers and individuals with metabolic risks. Overall demand rises as sleep health becomes a critical component of preventive healthcare.

Key Growth Drivers

Rising Prevalence of Sleep Disorders Worldwide

Growing cases of insomnia, sleep apnea, and circadian rhythm disturbances increase demand for accurate and continuous monitoring tools. Patients and clinicians rely on actigraphy sensors for long-term home-based tracking, while PSG devices remain essential for detailed sleep-lab assessments. Higher awareness of sleep health, combined with lifestyle-related disruptions, drives more diagnostic evaluations. Hospitals, sleep centers, and home-care settings expand their use of digital sleep technologies. This rising clinical burden strengthens market adoption across developed and emerging regions.

- For instance, the Natus Medical Embla NDx PSG system records up to 64 physiological channels with a sampling rate of up to 4096 Hz (4 kHz) for high-resolution sleep studies.

Advancements in Wearable and Sensor-Based Technologies

New wearable sensors offer improved comfort, precision, and long-duration monitoring, making them ideal for remote assessments. Wireless and Bluetooth-enabled systems allow seamless data transmission to clinicians and cloud platforms. Multi-channel PSG devices incorporate enhanced signal processing to capture accurate sleep physiology. These innovations support earlier diagnosis and better management of chronic sleep conditions. Technological progress also boosts device usability and patient engagement, expanding deployment in home-monitoring programs.

- For instance, SOMNOmedics SOMNO HD records up to 55 channels (upgradable to 70) using a digital amplifier with 24-bit resolution and a sampling rate of up to 4 kHz per channel.

Growing Demand for Home-Based Sleep Testing Solutions

Home-based sleep assessments gain traction as patients seek convenient, cost-effective alternatives to laboratory studies. Actigraphy sensors provide continuous monitoring without disrupting daily routines, increasing compliance. Healthcare providers adopt home-testing models to reduce sleep-lab burdens and expand outreach. Remote diagnostics also align with telehealth expansion, enabling virtual consultations and real-time data sharing. This trend boosts adoption in chronic sleep disorder management, pediatric monitoring, and elderly care.

Key Trends & Opportunities

Integration of AI and Data Analytics in Sleep Monitoring

AI-driven platforms improve sleep-stage scoring, anomaly detection, and long-term pattern analysis. Automated insights enhance the accuracy of actigraphy and PSG data, supporting faster clinical decisions. Analytics tools enable personalized sleep interventions and better therapy adjustments. Device manufacturers integrate cloud-based dashboards to provide deeper insights for clinicians and researchers. This trend creates strong opportunities for digital health partnerships and advanced monitoring ecosystems.

- For instance, Fitbit’s sleep-staging algorithm processes accelerometer inputs sampled at 50 Hz and heart-rate signals captured every second during rest.

Expansion of Multi-Parameter Wearables and Consumer Sleep Technologies

Demand increases for devices that monitor movement, heart rate, oxygen saturation, and temperature in a single platform. Consumers adopt multisensor wearables to track overall sleep quality and wellness. Medical-grade versions support early screening and follow-up assessments. Retail channels and online platforms expand device availability. This trend creates opportunities for hybrid clinical–consumer solutions with broader market reach.

- For instance, WHOOP 4.0 captures strain and recovery metrics with a 5-LED, 4-photodiode PPG module and sends data to the app using Bluetooth Low Energy where it is processed into detailed insights.

Key Challenges

Data Accuracy Limitations in Consumer-Grade Sleep Devices

Many wearable devices lack the precision needed for clinical-grade diagnostics. Variability in sensor quality and limited multi-channel data reduces reliability for complex cases. Clinicians face challenges integrating consumer-generated sleep data into formal assessments. This accuracy gap requires stronger standards and validation studies. These issues limit the adoption of low-end devices in medical decision-making.

High Cost of Advanced PSG Systems and Limited Lab Capacity

Polysomnography remains the gold standard but requires expensive multi-channel systems and skilled technicians. Sleep labs often face long waiting lists due to limited capacity. High acquisition and maintenance costs restrict adoption in smaller clinics and emerging regions. These barriers slow widespread access to comprehensive sleep diagnostics and limit market penetration for advanced PSG devices.

Regional Analysis

North America

North America led the market with 38% share, supported by strong adoption of digital health devices and widespread awareness of sleep disorders. Hospitals and sleep centers integrate advanced PSG systems and AI-enabled actigraphy tools for accurate diagnosis. Home-based sleep testing also expands due to high telehealth usage and strong insurance support. The region benefits from well-established sleep labs, rising prevalence of sleep apnea, and strong adoption of multi-parameter wearables. Leading manufacturers invest heavily in U.S. and Canada due to high consumer spending and strong clinical demand for validated sleep-monitoring technologies.

Europe

Europe accounted for 30% share, driven by structured sleep-care pathways, strong clinical guidelines, and rising diagnosis of insomnia and sleep apnea. Countries such as Germany, the UK, and France lead adoption of multi-channel PSG systems in hospitals and sleep laboratories. Demand for home-based actigraphy grows as healthcare systems promote early detection and remote monitoring. Regulatory emphasis on device accuracy supports uptake of medical-grade technologies. Investments in digital health infrastructure and growing acceptance of wearable monitoring tools continue to strengthen Europe’s position in the market.

Asia Pacific

Asia Pacific captured 25% share, supported by rising healthcare spending, large patient pools, and growing awareness of sleep-related disorders. Urbanization, long working hours, and lifestyle changes increase demand for actigraphy and PSG diagnostics. China, Japan, India, and South Korea drive strong adoption as hospitals expand sleep-medicine departments. Home-care monitoring also grows due to rising interest in consumer wearables and mobile-linked devices. Government initiatives to improve chronic disease management further accelerate market demand, making Asia Pacific one of the fastest-growing regions.

Latin America

Latin America held 4% share, influenced by expanding hospital infrastructure and growing recognition of sleep apnea and circadian rhythm disorders. Brazil and Mexico lead market adoption as sleep labs upgrade PSG systems and clinicians increasingly recommend actigraphy for long-term monitoring. Economic constraints limit widespread access, but digital health programs and lower-cost wearable devices improve adoption. Increased awareness campaigns and partnerships with device manufacturers help strengthen diagnosis rates. Gradual modernization of healthcare facilities supports steady growth across the region.

Middle East & Africa

The Middle East & Africa region accounted for 3% share, driven by rising healthcare investment and increasing detection of sleep disorders linked to lifestyle changes and chronic illnesses. Gulf countries adopt advanced PSG systems as hospitals upgrade diagnostic capabilities, while African nations rely more on affordable actigraphy tools due to limited sleep-lab availability. Growing telehealth adoption supports remote sleep monitoring, helping expand access in underserved areas. Awareness initiatives and improving diagnostic capacity contribute to steady progress, despite infrastructure limitations across parts of the region.

Market Segmentations:

By Product Type

- Actigraphy Sensors

- Polysomnography (PSG) Devices

- Wrist Actigraphs

- Others

By Technology

- Wireless Technology

- USB/ Wired Technology

- Bluetooth-Enabled Devices

- Multi-Channel PSG Systems

By Application

- Sleep Disorders Diagnosis

- Sleep Apnea Monitoring

- Circadian Rhythm Monitoring

- Others

By End User

- Hospitals

- Sleep Laboratories

- Home Care Settings

- Research & Academic Institutes

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape analysis highlights major players such as Philips Healthcare, ResMed, Fitbit (Google), Garmin Ltd., Natus Medical Incorporated, Nihon Kohden Corporation, SOMNOmedics, ActiGraph LLC, Compumedics Limited, and Microlife Corporation, all of which drive innovation in the Actigraphy Sensors and PSG Devices market. These companies enhance their product portfolios through advanced wearable sensors, multi-parameter monitoring systems, and AI-enabled sleep-analysis software. Vendors focus on improving device accuracy, user comfort, and wireless connectivity to support both clinical and home-based sleep assessments. Strategic partnerships with hospitals, sleep laboratories, and digital health platforms strengthen market presence and expand product reach. Many players invest in cloud-based data platforms and remote monitoring tools to align with rising demand for telehealth-integrated sleep diagnostics. Competition intensifies as companies prioritize lightweight designs, long-battery performance, and validated clinical data to differentiate their solutions.

Key Player Analysis

- Philips Healthcare

- ResMed

- Fitbit (Google)

- Garmin Ltd.

- Natus Medical Incorporated

- Nihon Kohden Corporation

- SOMNOmedics

- ActiGraph LLC

- Compumedics Limited

- Microlife Corporation

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In July 2025, Natus Medical Incorporated announced that its NeuroWorks EEG software now integrates with the Moberg CNS monitor—extending performance in neuro-monitoring and PSG/EEG diagnostics.

- In April 2025, ResMed announced that its NightOwl™ home sleep-apnea test, which enables diagnosis of obstructive sleep-apnea at home, is now available across the U.S.

- In March 2025, ResMed revealed a brand evolution: it unified its portfolio under one identity to better serve healthcare providers and consumers in the sleep and breathing health market.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Technology, Application, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Adoption of advanced wearable actigraphy devices will rise as demand for home-based sleep testing grows.

- AI-driven analytics will enhance sleep-stage scoring and improve clinical decision-making.

- Wireless PSG systems will expand as hospitals seek more efficient and patient-friendly diagnostic setups.

- Multi-parameter monitoring will gain traction as users prefer integrated tracking of movement, heart rate, and oxygen levels.

- Telehealth platforms will increasingly incorporate sleep-monitoring tools for remote consultations.

- Consumer wellness devices will continue to influence clinical adoption through improved sensor accuracy.

- Sleep laboratories will upgrade to multi-channel digital PSG systems to handle rising patient volumes.

- Pediatric and elderly sleep monitoring will expand as awareness of long-term sleep health increases.

- Cloud-based data platforms will support large-scale sleep research and population-level monitoring.

- Emerging markets will strengthen adoption as healthcare infrastructure improves and awareness of sleep disorders rises.