Market Overview

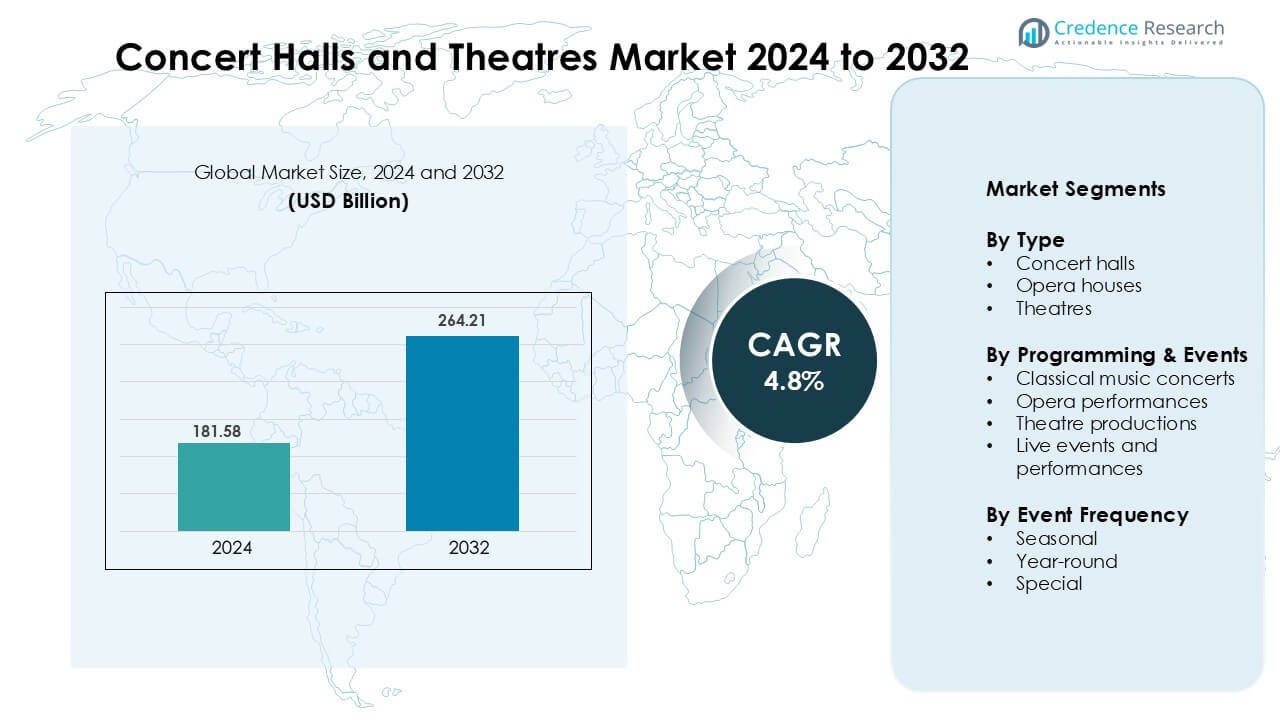

Concert Halls and Theatres Market was valued at USD 181.58 billion in 2024 and is anticipated to reach USD 264.21 billion by 2032, growing at a CAGR of 4.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Concert Halls and Theatres Market Size 2024 |

USD 181.58 Billion |

| Concert Halls and Theatres Market, CAGR |

4.8% |

| Concert Halls and Theatres Market Size 2032 |

USD 264.21 Billion |

The concert halls and theatres market is led by major players such as Eventbrite, Inc., AEG Presents, AXS, Paciolan, Inc., Tickets.com, LLC, Ticketfly, Inc., ShowClix, Inc., Vendini, Inc., Ticket Galaxy, Inc., and Universe, Inc. These companies dominate through their strong digital ticketing systems, event management capabilities, and strategic collaborations with artists and venues. North America emerges as the leading region, holding approximately 35% of the global market share, driven by advanced cultural infrastructure, high consumer spending on live entertainment, and widespread technological adoption. Continuous innovation in ticketing solutions and expanding hybrid event models further strengthen the region’s leadership and market competitiveness.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The global concert halls and theatres market is valued at USD 181.58 billion in 2024 and is projected to grow at a CAGR of 4.8% from 2025 to 2032, driven by increasing investments in cultural infrastructure and live entertainment demand.

- Market growth is primarily fueled by rising cultural tourism, technological advancements in venue management, and growing public and private sector funding for performing arts facilities.

- Key trends include the adoption of digital and hybrid event models, enhanced audience engagement through virtual access, and modernization of historic theatres to improve sustainability and accessibility.

- The competitive landscape features major players such as Eventbrite, AEG Presents, AXS, and Paciolan, focusing on digital ticketing innovation, strategic partnerships, and global event integration.

- North America leads with 35% market share, followed by Europe (32%) and Asia-Pacific (25%), while the theatres segment dominates with the highest revenue contribution among all facility types.

Market Segmentation Analysis:

By Type

Theatres represent the dominant segment in the concert halls and theatres market, accounting for a significant market share due to their versatile use and wide audience appeal. Theatres host a broad spectrum of performances, from plays to musicals, attracting consistent visitor turnout throughout the year. Their adaptability for various productions and strong cultural significance drive steady demand. Additionally, modernization initiatives and government support for performing arts infrastructure enhance growth prospects, while the ability of theatres to integrate advanced acoustics and digital technologies further strengthens their competitive advantage over traditional concert halls and opera houses.

- For instance, the National Centre for the Performing Arts in Mumbai installed a permanent Meyer Sound self-powered reinforcement system across two principal venues, replacing complex hired rigs and ensuring consistent sound coverage for multiple audiences.

By Programming & Events

The classical music concerts segment holds the largest share in programming and events, driven by its established global audience base and strong institutional backing from cultural organizations. These events often attract both local and international attendees, ensuring steady ticket revenues and sponsorships. The sustained popularity of orchestral performances and collaborations with renowned artists contribute to ongoing market dominance. Furthermore, the segment benefits from high cultural value, state funding, and long-term subscription models, supporting consistent performance scheduling and venue utilization compared to other event categories like theatre productions or live contemporary shows.

- For instance, Royal Philharmonic Orchestra found that 54 % of its recent audience were newcomers rather than long-term classical patrons, and the orchestra reported a drop in ticket bookings by around 30 % during one pandemic-impacted season highlighting the critical role of loyal institutional support and audience outreach in maintaining stability.

By Event Frequency

Year-round events lead the market in terms of frequency, capturing the highest market share due to continuous programming and strong operational sustainability. Venues hosting regular performances maintain higher occupancy rates and stable revenue streams, making this model the most commercially viable. The demand for consistent entertainment options and ongoing community engagement drives this segment’s growth. Moreover, partnerships with performing arts companies and educational institutions enable steady scheduling, ensuring cultural relevance and audience retention throughout the year compared to seasonal or special event formats.

Key Growth Drivers

Rising Cultural Engagement and Tourism Development

Increasing global interest in arts, culture, and heritage has become a major driver of growth in the concert halls and theatres market. Governments and private investors are focusing on expanding cultural tourism as part of urban revitalization strategies, leading to the construction and modernization of performing arts venues. Cities are leveraging these venues as cultural landmarks that attract both local residents and international tourists. Moreover, rising disposable incomes and growing participation in cultural events support consistent attendance and ticket sales. Festivals, music seasons, and international theatre collaborations further amplify visitor inflows. This synergy between tourism and performing arts strengthens the market’s economic contribution, fostering long-term investments and partnerships between municipalities, cultural organizations, and the private sector.

- For instance, Sydney Opera House hosts over 1,600 performances annually, attracts more than 10 million visitors, and engages over 700 local suppliers, illustrating how cultural infrastructure can serve as a tourism magnet.

Technological Integration and Modernization Initiatives

The adoption of advanced technologies has significantly transformed the concert halls and theatres landscape, enhancing audience experience and operational efficiency. Upgrades in acoustics, digital lighting, and stage automation have elevated production quality, while immersive sound and visual systems enrich the artistic presentation. Many venues are also investing in digital ticketing systems, virtual tours, and streaming platforms to reach broader audiences. These innovations cater to younger demographics and hybrid event models, expanding the revenue base beyond traditional ticket sales. Government-funded modernization programs and private sponsorships further drive infrastructure enhancement, ensuring venues remain competitive and adaptable to contemporary performance demands. This integration of technology not only boosts audience engagement but also improves sustainability through energy-efficient designs and digital management systems.

- For instance, Metropolitan Opera implemented the Met Titles system—installing individual multilingual subtitling screens at each seat—to improve accessibility for diverse audiences.

Government Support and Cultural Policy Initiatives

Public funding and policy support remain critical to the sustained growth of the concert halls and theatres market. Many governments recognize the performing arts as key contributors to social development, education, and national identity, leading to substantial budget allocations for maintenance, renovation, and program promotion. Cultural grants, tax incentives, and international partnerships encourage local artists and institutions to create innovative performances. Additionally, the inclusion of performing arts in urban development and tourism policies enhances visibility and accessibility. Such initiatives help stabilize market revenues by ensuring steady programming and audience engagement. The emphasis on preserving cultural heritage while encouraging contemporary expressions further diversifies artistic offerings, promoting inclusive growth across urban and regional venues.

Key Trend & Opportunity

Expansion of Digital and Hybrid Performance Models

A major trend reshaping the concert halls and theatres market is the rise of digital and hybrid event formats. Many venues now combine live performances with online streaming, enabling global audience participation and new monetization channels. This shift not only addresses accessibility barriers but also enhances resilience against disruptions such as pandemics. Digital technologies like augmented and virtual reality offer immersive experiences, transforming audience engagement. Furthermore, hybrid events allow performers to reach diverse demographics and international markets without geographical constraints. The trend also supports educational and outreach initiatives, as institutions can broadcast performances to schools and remote communities. This digital evolution represents a long-term opportunity for venues to diversify income streams and strengthen their global presence.

- For instance, The Berlin Philharmonic “Digital Concert Hall” has been running since the late 2000s, primarily using high-definition, and later 4K, camera systems provided by commercial partners like Sony and, more recently, Panasonic.

Growing Private Investments and Commercial Collaborations

Private investments and cross-sector collaborations are emerging as vital opportunities for market expansion. Corporate sponsorships, brand partnerships, and commercial events increasingly support financial sustainability in the performing arts sector. Real estate developers and investors view cultural venues as key components of mixed-use urban projects that enhance property value and community engagement. In addition, hospitality and tourism partnerships create bundled cultural experiences, boosting visitor spending. Such collaborations foster innovation in venue management, marketing, and audience outreach. With growing emphasis on cultural entrepreneurship, the integration of arts and business models offers venues new funding sources and operational flexibility, ensuring long-term growth and reduced reliance on public subsidies.

- For instance, Factory International’s new headquarters at Aviva Studios hosted the Manchester International Festival (MIF23) launch, with the associated Festival Square free public area welcoming 83,000 visitors as part of the festival’s total attendance of over 325,000, and the venue supported by a naming rights partnership with Aviva.

Key Challenge

High Operational and Maintenance Costs

Concert halls and theatres face substantial operational costs, particularly related to facility maintenance, staffing, and technical upgrades. Historic and large-scale venues require continuous investment in infrastructure to meet safety, comfort, and acoustic standards. Energy consumption, equipment modernization, and regular renovations significantly strain budgets, especially for non-profit organizations. Limited funding sources often force venues to balance artistic ambition with financial feasibility. Rising utility and labor costs further pressure profitability. This challenge necessitates innovative management approaches, such as energy-efficient retrofitting, digital automation, and diversified revenue generation. Without effective cost management strategies, many venues risk reduced programming capacity and long-term sustainability issues.

Audience Diversification and Retention Difficulties

Changing audience preferences and demographic shifts present significant challenges for the concert halls and theatres market. Traditional performing arts forms like opera and classical theatre often struggle to attract younger audiences, who favor more contemporary or interactive entertainment experiences. Additionally, competition from digital streaming platforms and alternative leisure options has reduced live event attendance in some regions. Venues must invest in creative marketing, inclusive programming, and educational outreach to remain relevant. Developing accessible pricing models and fostering community engagement are essential to sustain long-term audience growth. Failure to adapt to evolving cultural consumption patterns could limit future market expansion and weaken audience loyalty.

Regional Analysis

North America

North America holds a substantial share of the global concert halls and theatres market, accounting for approximately 32–35% of total revenue. The region’s dominance is driven by a strong cultural infrastructure, high disposable incomes, and a vibrant entertainment industry centered around cities such as New York, Los Angeles, and Toronto. Significant investments in venue modernization and digital integration further enhance audience engagement. Additionally, strong support from private sponsors and foundations sustains year-round programming. The growth of cultural tourism and diverse event offerings continues to reinforce North America’s leadership in the global performing arts market.

Europe

Europe commands around 30–32% of the global market share, supported by its rich artistic heritage and extensive network of historic opera houses and theatres. Major cultural hubs like London, Paris, Vienna, and Berlin continue to attract international audiences and performers. Government funding and cultural preservation initiatives play a key role in sustaining operations and promoting accessibility. The region’s emphasis on classical music, opera, and theatre festivals ensures consistent attendance. Furthermore, modernization projects integrating digital technologies and sustainability measures enhance venue performance, positioning Europe as a leading region in cultural excellence and performing arts innovation.

Asia-Pacific

The Asia-Pacific region accounts for nearly 22–25% of the concert halls and theatres market and is the fastest-growing region globally. Rapid urbanization, expanding middle-class populations, and increasing government investment in cultural infrastructure drive strong demand. Countries such as China, Japan, South Korea, and Australia are developing world-class venues to support international performances and cultural tourism. Rising interest in Western performing arts, alongside a revival of local traditions, enriches program diversity. The proliferation of hybrid and digital performances also broadens audience reach, positioning Asia-Pacific as a major growth engine in the global performing arts landscape.

Latin America

Latin America represents around 6–8% of the global concert halls and theatres market, supported by a growing appreciation for performing arts and cultural tourism. Countries such as Brazil, Mexico, and Argentina are leading contributors, with active investment in modernizing historic theatres and promoting local productions. The region’s diverse cultural heritage fosters a dynamic mix of classical and contemporary performances. Although economic fluctuations can affect funding, increased private sponsorships and international collaborations are improving market stability. Latin America’s emphasis on regional festivals and cross-cultural events continues to strengthen its position within the global performing arts ecosystem.

Middle East & Africa

The Middle East and Africa collectively hold an emerging market share of about 5–6%, with strong growth potential driven by cultural diversification and infrastructure expansion. Gulf countries, including the UAE, Saudi Arabia, and Qatar, are investing heavily in large-scale cultural projects and world-class performance venues to boost tourism and international engagement. In Africa, nations like South Africa and Nigeria are fostering performing arts as part of creative economy development. Although the market is nascent, rising public and private investment, coupled with increasing youth interest in live entertainment, is expected to accelerate future growth in this region.

Market Segmentations:

By Type

- Concert halls

- Opera houses

- Theatres

By Programming & Events

- Classical music concerts

- Opera performances

- Theatre productions

- Live events and performances

By Event Frequency

- Seasonal

- Year-round

- Special

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The concert halls and theatres market features a moderately fragmented competitive landscape, with a mix of global event organizers, ticketing platforms, and venue operators driving market growth. Key players such as Eventbrite, Inc., AEG Presents, AXS, Paciolan, Inc., Tickets.com, LLC, Ticketfly, Inc., ShowClix, Inc., Vendini, Inc., Ticket Galaxy, Inc., and Universe, Inc. play pivotal roles in event management, ticket distribution, and audience engagement. These companies leverage digital ticketing systems, data analytics, and mobile platforms to enhance accessibility and streamline user experience. Strategic partnerships with artists, production houses, and cultural institutions strengthen their market positions. Additionally, increasing focus on hybrid event models and technological innovation in venue operations fosters competitive differentiation. The market also witnesses growing consolidation through mergers and acquisitions, enabling firms to expand service portfolios and geographical reach. Continuous investment in digital infrastructure and audience analytics remains central to maintaining competitiveness in this dynamic cultural and entertainment sector.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In Jun 2025, AEG Presents: Acquired Gary Musick Productions and Destination Musick City to expand event production capabilities.

- In Jun 2025, Eventbrite, Inc.: Introduced the Lineup tool to help independent music venues highlight artists and reach more fans.

- In Jan 2025, Eventbrite, Inc.: Released a cultural study on Fourth Spaces, shaping venue programming for Gen Z and millennials.

Report Coverage

The research report offers an in-depth analysis based on Type, Programming & Events, Event Frequency and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The concert halls and theatres market will continue expanding due to growing global interest in live cultural and entertainment experiences.

- Digital transformation will redefine audience engagement through virtual access and interactive performance technologies.

- Hybrid event formats will become standard, combining physical attendance with online participation for broader reach.

- Sustainability initiatives will drive investments in energy-efficient designs and eco-friendly venue operations.

- Public-private partnerships will increase to support modernization and cultural preservation projects.

- Emerging economies in Asia-Pacific and the Middle East will witness significant growth in venue construction and cultural funding.

- Advanced data analytics will enhance ticketing, marketing, and audience targeting strategies.

- Collaboration between artists, technology firms, and venue operators will foster innovative performance formats.

- Theatres will maintain dominance due to versatility and consistent audience appeal across genres.

- Enhanced government policies and tourism integration will further strengthen the market’s long-term growth trajectory.