Market overview

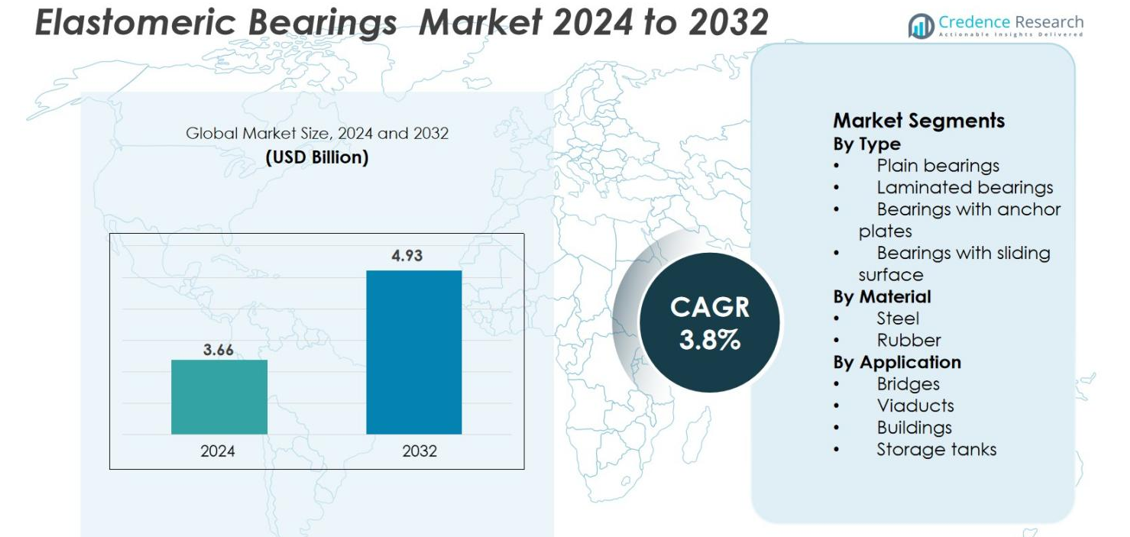

Elastomeric Bearings Market size was valued at USD 3.66 billion in 2024 and is anticipated to reach USD 4.93 billion by 2032, at a CAGR of 3.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Elastomeric Bearings Market Size 2024 |

USD 3.66 billion |

| Elastomeric Bearings Market, CAGR |

3.8% |

| Elastomeric Bearings Market Size 2032 |

USD 4.93 billion |

\The elastomeric bearings market is led by key companies such as MAURER SE, D.S. Brown, Freyssinet Limited, BRP Manufacturing, Cosmec Inc., Ekspan Limited, Redwood Plastics and Rubber, DOSHIN RUBBER PRODUCTS (M) SDN. BHD., Canam Group Inc., and Granor Rubber & Engineering Pty. Limited. These players focus on advanced elastomer formulations, enhanced load-bearing capacity, and compliance with global standards to maintain competitiveness. Asia-Pacific leads the market with a 34.8% share in 2024, driven by large-scale infrastructure projects and government-backed bridge expansion programs. Europe follows with a 28.7% share, supported by stringent quality regulations and modernization initiatives across the region’s extensive bridge and viaduct networks.

Market Insights

- The Elastomeric Bearings Market was valued at USD 3.66 billion in 2024 and is projected to reach USD 4.93 billion by 2032, growing at a CAGR of 3.8%.

- Market growth is driven by rising infrastructure development, bridge rehabilitation, and seismic-resistant construction projects worldwide, particularly in Asia-Pacific and Europe.

- A key trend is the adoption of advanced laminated and rubber-based bearings offering improved flexibility, vibration isolation, and durability under dynamic load conditions.

- The market is moderately consolidated, with key players such as MAURER SE, D.S. Brown, Freyssinet Limited, and DOSHIN RUBBER PRODUCTS focusing on innovation and sustainability.

- Asia-Pacific dominates with a 34.8% share, followed by Europe at 28.7% and North America at 26.4%, while laminated bearings lead the type segment with a 47.6% share due to superior load-bearing and seismic performance.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis

By Type

Laminated bearings dominate the elastomeric bearings market with a 47.6% share in 2024. Their layered rubber–steel structure provides superior load distribution, flexibility, and resistance to seismic and thermal movements. These bearings are widely adopted in bridge and viaduct construction due to their long service life and ability to accommodate both vertical loads and horizontal displacements. Growing infrastructure investments and modernization of existing bridges further drive demand. Additionally, innovations in vulcanization and bonding technology enhance durability and mechanical performance, strengthening the segment’s leadership position.

- For instance, steel-laminated elastomeric bearings combine neoprene or natural rubber layers vulcanized with steel plates, enhancing their capacity to accommodate vertical loads and horizontal displacements in bridges and viaducts.

By Material

Rubber-based elastomeric bearings hold a 62.4% share in 2024, driven by their excellent elasticity, corrosion resistance, and low maintenance needs. Natural and neoprene rubber materials are widely preferred for their ability to absorb vibrations and reduce structural stress under dynamic loads. The segment benefits from advancements in polymer compounding, improving temperature stability and fatigue resistance. Steel-reinforced rubber bearings further extend lifespan under heavy-load applications. Increasing adoption of sustainable, recyclable rubber compounds also contributes to the segment’s continued dominance across infrastructure and industrial applications.

- For instance, CECO has produced premium elastomeric bearings since 1982, combining steel reinforcements with natural and neoprene rubber to meet AASHTO and European standards, providing reliable structural flexibility for large-span bridges.

By Application

The bridges segment leads the elastomeric bearings market with a 54.2% share in 2024, supported by large-scale highway, railway, and urban bridge projects. Elastomeric bearings in bridges allow controlled movement and rotation under load and temperature variations, ensuring long-term structural safety. Governments worldwide are prioritizing bridge rehabilitation programs, boosting demand for high-performance bearing systems. Moreover, the expansion of cross-river connectivity projects in Asia-Pacific and Europe reinforces market growth. Advanced elastomer formulations offering enhanced load-bearing and weather resistance continue to support widespread use in modern bridge engineering.

Key Growth Drivers

Expanding Global Infrastructure Development

The rapid growth of infrastructure projects, including highways, railways, and bridges, is driving strong demand for elastomeric bearings. These components are essential for ensuring flexibility, load-bearing capacity, and vibration isolation in structural designs. Governments in Asia-Pacific and the Middle East are allocating significant budgets to build and rehabilitate bridges and transport corridors, directly supporting market expansion. For instance, large-scale projects under China’s Belt and Road Initiative and India’s Bharatmala program have accelerated bearing adoption. Additionally, urbanization and smart city programs across developing economies are increasing demand for durable, low-maintenance elastomeric solutions that can perform under high stress and variable environmental conditions.

- For instance, Dutco Tennant LLC supplies customized elastomeric bearings for smart city infrastructure projects in the Middle East, emphasizing load accommodation and vibration reduction in evolving urban environments.

Rising Adoption of Seismic Isolation Systems

The growing focus on seismic resilience in building and bridge design has accelerated the use of elastomeric bearings, particularly laminated and lead rubber types. These bearings minimize structural damage during earthquakes by absorbing and dissipating seismic energy, enhancing public safety and reducing maintenance costs. Japan, the United States, and New Zealand are integrating seismic isolation technologies into infrastructure codes, encouraging wider adoption. For instance, Freyssinet and MAURER SE have developed advanced elastomeric bearings capable of withstanding high horizontal displacements during seismic events. The trend toward performance-based engineering standards continues to fuel innovation in this field, boosting long-term market growth.

- For instance, MAURER SE, a market leader in seismic protection systems, manufactures elastomeric bearings with patented MSM® sliding layers, offering low friction and high durability, with a service life exceeding 50 years, complying with European and AASHTO standards.

Technological Advancements in Material Engineering

Innovations in polymer science and composite technology are significantly enhancing the performance of elastomeric bearings. The use of high-damping natural rubber, neoprene, and steel-reinforced layers improves mechanical strength, temperature tolerance, and resistance to environmental degradation. Companies like D.S. Brown and Granor Rubber & Engineering are developing customized formulations to extend service life and reduce deformation. Moreover, advanced bonding and vulcanization processes improve adhesion between rubber and steel laminates, ensuring stability under heavy dynamic loads. Such technological progress not only boosts product reliability but also aligns with sustainability goals by promoting recyclable materials and energy-efficient manufacturing processes.

Key Trends & Opportunities

Shift Toward Smart and Sustainable Bearing Solutions

The market is witnessing a shift toward eco-friendly and intelligent elastomeric bearing systems. Manufacturers are focusing on developing recyclable rubber compounds and low-carbon production methods to meet sustainability targets. Additionally, the integration of sensors into bearing assemblies enables real-time monitoring of load stress, displacement, and temperature variations. These smart bearings enhance predictive maintenance and structural health monitoring, minimizing operational downtime. With growing emphasis on green infrastructure and smart cities, sustainable and connected bearing technologies represent a major growth opportunity for both established players and emerging innovators.

- For instance, Angst+Pfister integrates advanced sensing materials directly into elastomer components, enhancing operational efficiency and enabling smart structural health monitoring, critical for smart city deployments.

Increasing Modernization and Retrofitting Projects

Aging infrastructure across North America and Europe has created strong demand for retrofitting and rehabilitation projects using modern elastomeric bearings. Many bridges and viaducts built decades ago are being upgraded with advanced bearing systems to improve safety and durability. For example, MAURER SE and Ekspan Limited have introduced retrofit-compatible elastomeric bearings designed for rapid installation without major structural modifications. This trend aligns with government programs that prioritize asset life extension and cost-effective maintenance over full reconstruction. Consequently, the retrofit segment provides significant revenue potential for manufacturers offering tailored, high-performance bearing solutions.

- For instance, the Kocher Viaduct on Germany’s A81 motorway was recently rehabilitated with MAURER’s modern sliding spherical bearings, replacing old stainless-steel rollers to enhance performance under heavy loads.

Expansion of Emerging Construction Markets

Rapid industrialization and public infrastructure spending in emerging economies like India, Indonesia, and Brazil are opening new opportunities for elastomeric bearing suppliers. These regions are investing heavily in bridge networks, metro systems, and port expansions. Domestic production of bearings is also increasing due to favorable trade policies and localization incentives. Companies entering these markets benefit from reduced logistics costs and growing public-private partnerships. The rising demand for durable, cost-effective elastomeric bearings in developing nations is expected to sustain high growth momentum over the next decade.

Key Challenges

Volatility in Raw Material Prices

Fluctuations in the prices of natural rubber, neoprene, and steel significantly impact production costs in the elastomeric bearings market. Rubber supply is vulnerable to climatic conditions and geopolitical disruptions in major producing regions such as Southeast Asia. Steel price volatility due to global trade tensions further complicates cost management for manufacturers. This instability challenges profit margins, especially for small and medium enterprises competing on price-sensitive contracts. To counter this, companies are diversifying sourcing strategies and investing in synthetic alternatives, though these measures increase R&D expenses and lengthen product development cycles.

Stringent Quality and Compliance Requirements

Elastomeric bearings must meet rigorous international standards such as EN 1337, AASHTO, and BS 5400, which regulate load capacity, material quality, and performance under dynamic stress. Compliance requires extensive testing, certification, and documentation, increasing operational complexity and cost. Non-compliance can lead to disqualification from large infrastructure tenders, limiting market access. Furthermore, regional variations in safety codes create additional hurdles for global manufacturers. Companies are investing in advanced testing facilities and digital quality assurance systems to maintain certification standards, but achieving consistent compliance remains a major challenge for the industry.

Regional Analysis

North America

North America accounts for 26.4% of the elastomeric bearings market in 2024, driven by bridge rehabilitation projects and modernization of aging transport infrastructure. The United States leads the region due to the Federal Highway Administration’s focus on seismic-resistant bridge designs and maintenance programs. Key manufacturers such as D.S. Brown and Canam Group Inc. supply advanced laminated bearings that comply with AASHTO standards. Canada’s infrastructure renewal initiatives further support steady demand. The region’s emphasis on quality assurance, performance testing, and sustainable material sourcing reinforces long-term market stability and technological adoption.

Europe

Europe holds a 28.7% share of the elastomeric bearings market in 2024, supported by extensive bridge and viaduct networks in Germany, France, and the U.K. The European Union’s infrastructure recovery plans and seismic retrofitting programs are boosting product adoption. Companies like MAURER SE, Freyssinet Limited, and Ekspan Limited dominate with advanced sliding and laminated bearing solutions. Strong regulatory frameworks under EN 1337 ensure product safety and durability. The growing integration of smart monitoring technologies and sustainable elastomeric materials further enhances Europe’s leadership in structural performance innovation.

Asia-Pacific

Asia-Pacific leads the global elastomeric bearings market with a 34.8% share in 2024, propelled by rapid urbanization and large-scale transport projects. China, India, and Japan are investing heavily in bridge, highway, and metro developments. Domestic producers, including DOSHIN RUBBER PRODUCTS and Granor Rubber & Engineering, cater to regional demand through cost-effective production and government-backed infrastructure funding. Rising seismic awareness and increased adoption of laminated rubber bearings in Japan drive technology advancement. The region’s focus on capacity expansion, local manufacturing, and smart city infrastructure sustains its dominant market position.

Latin America

Latin America represents 6.5% of the elastomeric bearings market in 2024, led by ongoing infrastructure modernization in Brazil, Mexico, and Chile. Expanding road connectivity, bridge restoration, and industrial construction projects stimulate demand. Local collaborations with global manufacturers like Freyssinet and MAURER SE are enhancing the availability of high-performance bearing systems. Government-backed investments in resilient and cost-efficient structures are further strengthening adoption. Although limited by funding constraints, public-private partnerships and cross-border trade agreements are expected to improve regional supply chain efficiency and long-term growth prospects.

Middle East & Africa

The Middle East and Africa collectively hold a 3.6% share of the elastomeric bearings market in 2024, driven by infrastructure expansion and bridge construction across the UAE, Saudi Arabia, and South Africa. Projects under Saudi Vision 2030 and the UAE’s urban development programs are increasing demand for heavy-duty bearings. Companies like Ekspan Limited and Redwood Plastics and Rubber are partnering with regional contractors to deliver high-quality products suited for extreme temperatures. The growing emphasis on durable, weather-resistant bearings and industrial modernization continues to strengthen regional market participation.

Market Segmentations

By Type

- Plain bearings

- Laminated bearings

- Bearings with anchor plates

- Bearings with sliding surface

By Material

By Application

- Bridges

- Viaducts

- Buildings

- Storage tanks

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the elastomeric bearings market is moderately consolidated, featuring a blend of global manufacturers and specialized regional suppliers. Key players include MAURER SE, D.S. Brown, Freyssinet Limited, BRP Manufacturing, Cosmec Inc., Redwood Plastics and Rubber, Ekspan Limited, DOSHIN RUBBER PRODUCTS (M) SDN. BHD., Canam Group Inc., and Granor Rubber & Engineering Pty. Limited. These companies compete through innovation in material technology, durability enhancement, and compliance with international standards such as AASHTO and EN 1337. Strategic initiatives focus on capacity expansion, partnerships with infrastructure contractors, and sustainable product development. For instance, MAURER SE has advanced its seismic isolation bearings with improved damping characteristics, while D.S. Brown continues to invest in elastomer formulation research to extend product lifespan. The increasing adoption of smart monitoring systems and customized bearing solutions further differentiates market leaders, strengthening their global footprint across bridge, viaduct, and building construction segments.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- D.S. Brown

- MAURER SE

- Redwood Plastics and Rubber

- Ekspan Limited

- Freyssinet Limited

- DOSHIN RUBBER PRODUCTS (M) SDN. BHD.

- Canam Group Inc.

- Granor Rubber & Engineering Pty. Limited

- Cosmec Inc.

- BRP Manufacturing

Recent Developments

- In June 2024, Freyssinet led essential repair operations to improve the structural stability of a major bridge in Puerto Rico. The project involved replacing the bridge’s lower anchorage caps and performing fillet welding, microcrystalline wax injection, and elastomeric wrapping.

- In December 2023, Timken Company completed the acquisition of Lagersmit, a Netherlands-based producer of advanced sealing solutions. This moves expanded Timken’s portfolio across marine, dredging, water, tidal energy, and various industrial sectors, strengthening its presence in the elastomeric bearings market.

- In February 2023, Timken Company purchased the assets of American Roller Bearing Company (ARB), a North Carolina-based manufacturer specializing in industrial bearings.

Report Coverage

The research report offers an in-depth analysis based on Type, Material, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for elastomeric bearings will continue to grow with expanding global infrastructure projects.

- Adoption of seismic isolation bearings will rise as earthquake-resistant design becomes a global standard.

- Advanced rubber formulations will enhance temperature tolerance and long-term durability.

- Integration of smart sensors in bearings will enable real-time performance monitoring.

- Sustainable materials and recyclable rubber compounds will gain wider acceptance.

- Public-private partnerships will boost investment in bridge and transport infrastructure.

- Retrofitting and modernization of aging bridges will drive steady replacement demand.

- Asia-Pacific will remain the dominant regional market supported by large-scale projects.

- European manufacturers will focus on high-quality and compliant bearings to maintain leadership.

- Collaboration between global and regional players will accelerate product innovation and market expansion.