Autonomous Farm Equipment Market Overview:

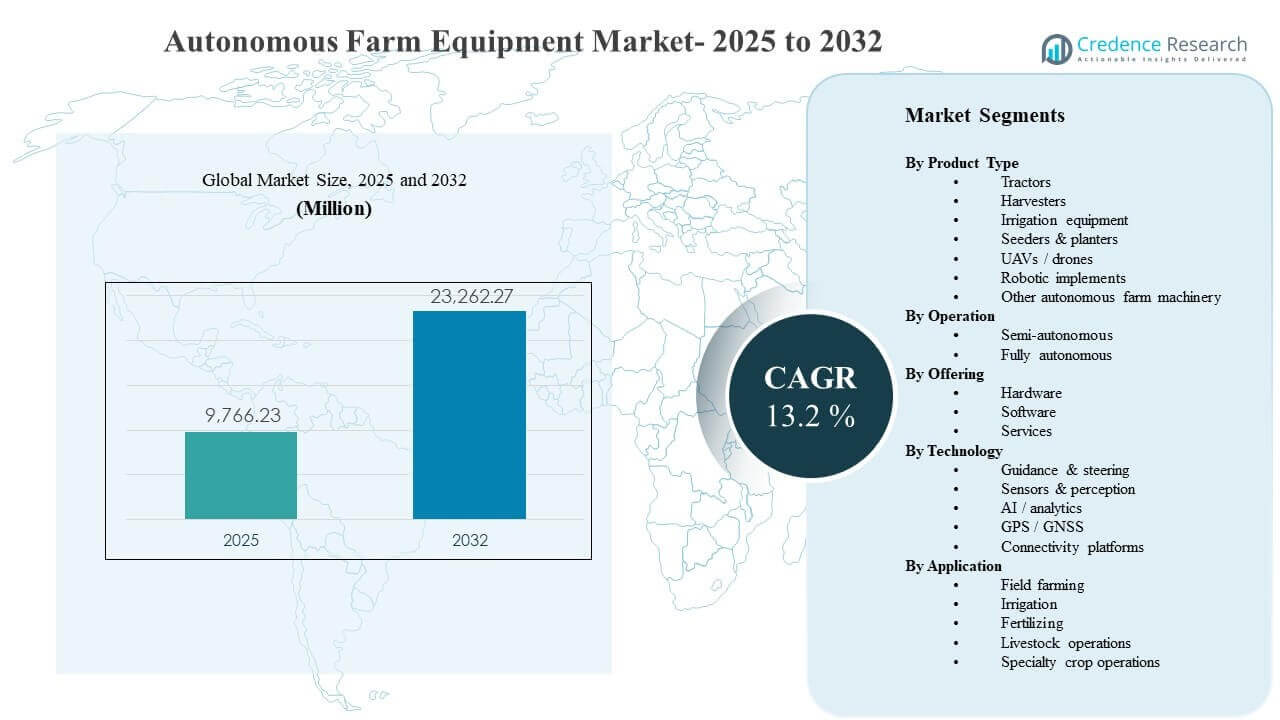

The global Autonomous Farm Equipment Market size was estimated at USD 9,766.23 million in 2025 and is expected to reach USD 23,262.27 million by 2032, growing at a CAGR of 13.2% from 2025 to 2032. Market expansion is primarily driven by accelerating adoption of autonomy to address persistent farm labor constraints and to improve operating efficiency during peak seasonal workloads across planting, spraying, and harvesting cycles. Continued advances in sensing, positioning, and connectivity are also supporting broader deployment across mixed fleets and varied field conditions.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Autonomous Farm Equipment Market Size 2025 |

USD 9,766.23 million |

| Autonomous Farm Equipment Market, CAGR |

13.2% |

| Autonomous Farm Equipment Market Size 2032 |

USD 23,262.27 million |

Key Market Trends & Insights

- North America accounted for 33.92% in 2025, supported by high mechanization levels and faster adoption of autonomy-ready platforms.

- Asia Pacific represented 29.54% in 2025, reflecting expanding mechanization and rapid uptake of precision-ag technology across large farming economies.

- Semi-autonomous systems held 66.90% share in 2025, as supervised autonomy scales more quickly under farm safety and operational preferences.

- Hardware contributed 58.60% share in 2025, driven by demand for sensors, GNSS/RTK components, compute, and steering/actuation systems.

- Tractors captured 33.80% share in 2025, as they remain the most utilized equipment platform and the primary entry point for autonomy upgrades.

Segment Analysis

Autonomous farm equipment adoption is progressing through a staged pathway where farms prioritize the highest-utilization machines and the most immediately monetizable workflows. Broad-acre operations typically deploy autonomy features first for guidance, steering, and implement control because these use-cases reduce operator fatigue, extend operating windows, and improve repeatability in row-level tasks. As autonomy matures, capability expansion is increasingly tied to higher-fidelity perception and decision-making, enabling more complex operations under variable terrain, weather, and crop conditions.

Commercialization is also shifting from one-time equipment purchases toward integrated “system” adoption, where buyers evaluate hardware performance alongside software intelligence, connectivity, and after-sales support. Farms operating mixed fleets are particularly sensitive to interoperability and ease of deployment, favoring solutions that integrate into existing precision workflows. Service layers are expanding through installation, calibration, monitoring, operator training, and uptime assurance, which improves reliability and accelerates adoption across farm sizes.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Tractors accounted for the largest share of 33.80% in 2025. Tractors are typically the first mechanization platform upgraded with autonomy because they deliver high annual utilization across multiple field activities and provide clearer return on investment. Autonomy-ready tractor platforms also enable longer operating hours during tight seasonal windows, directly improving productivity. Strong OEM and dealer ecosystems further support tractor-led adoption by simplifying deployments, upgrades, and ongoing support.

By Operation Insights

Semi-autonomous accounted for the largest share of 66.90% in 2025. Farms often adopt supervised autonomy before moving to fully unmanned operations due to safety requirements, liability concerns, and the need to maintain operational oversight in variable field environments. Semi-autonomous modes deliver immediate labor-efficiency benefits by reducing operator workload without demanding full process redesign. Stepwise implementation also fits mixed-fleet realities, allowing farms to scale autonomy across equipment types and seasons.

By Offering Insights

Hardware accounted for the largest share of 58.60% in 2025. Hardware remains the primary cost and adoption driver because autonomous operation requires robust sensors, GNSS/RTK positioning, onboard compute, ruggedized electronics, and steering/actuation components. Many farms also prioritize tangible, machine-level upgrades that can be deployed across multiple operations and crop cycles. As deployments scale, hardware upgrades frequently create pull-through demand for software layers and services to improve performance, reliability, and lifecycle value.

By Technology Insights

Sensors & perception typically anchor autonomy deployments because reliable detection, localization, and environmental understanding are foundational to safe operation in unstructured agricultural settings. Guidance and steering remain essential for repeatability and row-level precision, particularly for planting and cultivation workflows. AI/analytics is becoming increasingly important as farms look to optimize routes, implement control, and decision support using real-time and historical operational data. Connectivity platforms strengthen fleet monitoring, remote diagnostics, and software updates, improving uptime and accelerating feature rollout across deployed machines.

By Application Insights

Field farming remains the largest application area because it concentrates the highest equipment-hours and the most time-sensitive workflows across tillage, planting, spraying, and harvesting. Farms prioritize autonomy where it can alleviate peak-season labor bottlenecks and reduce cost per hectare through improved productivity and repeatability. Fertilizing and input application benefit from autonomy through more consistent coverage and reduced overlap, supporting both cost optimization and sustainability goals. Livestock and specialty crop operations adopt autonomy selectively where navigation complexity is higher and workflows require more advanced perception and safety handling.

Autonomous Farm Equipment Market Drivers

Labor Scarcity and Productivity Pressures

Farm operators face ongoing labor constraints, particularly during peak planting and harvesting windows, pushing demand for autonomy that reduces dependence on skilled operators. Autonomous and semi-autonomous workflows enable longer operating hours and more consistent task execution, improving throughput when timing is critical. Productivity gains are reinforced by repeatable machine performance in guidance, steering, and implement control, which reduces variability across fields. Over time, labor-driven adoption also supports a shift toward fleet optimization and standardized operations.

- For instance, RTK‑enabled steering solutions from suppliers such as John Deere StarFire and Trimble Ag RTK routinely achieve 1–2.5 cm pass‑to‑pass accuracy, minimizing skips and overlaps during critical operations. Over time, labor-driven adoption also supports a shift toward fleet optimization and standardized operations.

Precision Agriculture Expansion and Input Efficiency

Autonomous equipment increasingly complements precision agriculture by enabling more consistent coverage, better route planning, and improved variable-rate execution. Reduced overlap in spraying and fertilizing lowers input waste and supports cost control, especially in large-scale operations. Autonomy also improves repeatability, which strengthens data quality across seasons and enables better decision-making tied to yields and field variability. As farms digitize operations, autonomy becomes an execution layer that translates prescriptions into consistent field performance.

Technology Maturity in Positioning, Sensing, and Control

Improvements in GNSS/RTK availability, sensor performance, and onboard compute are making autonomy more reliable across diverse farm conditions. Better perception enables safer navigation around obstacles and improves implement control during complex operations. As the technology stack matures, OEMs and solution providers can deliver autonomy features at broader price points, expanding adoption beyond early adopters. Integration with connectivity and remote monitoring further improves reliability by accelerating troubleshooting and software updates.

OEM Ecosystems, Retrofits, and Service Enablement

OEM product roadmaps are increasingly centered on autonomy-ready platforms, supported by dealer networks that simplify deployment and maintenance. Retrofit pathways expand the addressable market by enabling autonomy upgrades for existing fleets, especially in tractors and implements. Service enablement—installation, calibration, training, and uptime support—reduces operational risk for buyers and speeds scaling across farm sites. These ecosystem dynamics improve adoption by lowering total cost of ownership uncertainty and improving perceived reliability.

- For instance, John Deere’s autonomous tractor program uses dealer‑installed autonomy kits and dealer‑run demo programs to introduce and support the technology in regional markets. Retrofit pathways expand the addressable market by enabling autonomy upgrades for existing fleets, especially in tractors and implements.

Autonomous Farm Equipment Market Challenges

Autonomous farm equipment deployment faces practical constraints tied to operating variability in real-world fields, including uneven terrain, weather effects, crop residue, and mixed obstacles that can reduce autonomy reliability. Integration across mixed fleets remains challenging, particularly where farms operate multiple OEMs with different digital ecosystems, connectivity standards, and software interfaces. Upfront investment can also be a barrier for smaller farms, especially when ROI depends on high utilization or complementary precision infrastructure such as RTK and connectivity.

- For instance, CNH Industrial’s integration of Raven Autonomy on platforms such as the Case IH Trident 5550 and Omnipower 3200 emphasizes a single connected stack, but growers still report relying on separate consoles and data pipelines when combining these machines with third‑party guidance or rate‑control systems, limiting true cross‑fleet interoperability despite hardware upgrades that deliver about 50% more power to the ground and higher operating speeds on Raven’s 3200 platform.

Safety, liability, and regulatory uncertainty can slow adoption, particularly for fully autonomous operations where oversight expectations are higher. Many farms remain cautious about removing operators entirely due to risk tolerance and the operational complexity of field conditions that change rapidly. Maintenance requirements for sensors and electronics in dusty, high-vibration environments can affect uptime if service coverage is limited. Data governance and cybersecurity concerns are also rising as equipment becomes more connected and dependent on software updates.

Autonomous Farm Equipment Market Trends and Opportunities

Autonomy is increasingly packaged as part of integrated precision platforms that combine machine automation with software intelligence, enabling farms to manage operations through unified dashboards and fleet orchestration tools. This integration supports new value propositions such as predictive maintenance, remote diagnostics, and continuous improvement through software updates. As farms seek higher utilization and better seasonal planning, these platform models create opportunities for recurring revenue streams and deeper customer lock-in through ecosystem adoption.

- For instance, AGCO’s FendtONE platform wirelessly synchronizes machine terminals with offboard planning software so operators can share identical task views across the entire fleet and transfer application maps and field data in real time between office and tractor terminals, enabling continuous optimization of machine settings and workflows based on live agronomic and operational data.

Service-led commercialization is expanding through managed deployments, training, and performance-based support models that reduce perceived risk for buyers. Farms operating mixed fleets are creating demand for interoperability layers that can coordinate guidance, steering, and operational data across different machines. UAV-enabled scouting and monitoring are also reinforcing autonomy demand by strengthening data inputs that guide variable-rate applications and targeted field actions. Together, these trends broaden adoption beyond equipment purchase decisions into system-level operating model upgrades.

Regional Insights

North America

North America held 33.92% share in 2025, supported by large commercial farms and strong precision-ag penetration. Adoption tends to focus on tractors, guidance, and scalable semi-autonomous workflows that fit existing farm practices. Mature dealer networks and service coverage improve uptime confidence and accelerate deployment across multiple sites.

Europe

Europe accounted for 18.18% share in 2025, driven by high mechanization, strong OEM presence, and increasing emphasis on input efficiency and sustainability-aligned farming practices. Adoption often prioritizes automation features that enhance consistency and reduce chemical use through precision execution. Structured support ecosystems and technology pilots also contribute to steady adoption.

Asia Pacific

Asia Pacific represented 29.54% share in 2025, supported by expanding mechanization and rapid modernization of farming operations in key agricultural economies. Large-scale farms and commercial growers are increasingly investing in precision systems that pair well with autonomy. Growth is also supported by broad uptake of UAV-enabled monitoring and data-driven field management.

Latin America

Latin America held 10.79% share in 2025, reflecting large commercial farming footprints paired with more uneven infrastructure readiness across markets. Adoption is typically strongest where export-oriented crop production drives investment in efficiency and yields. Autonomy penetration grows as farm operators scale precision workflows and service ecosystems strengthen.

Middle East & Africa

Middle East & Africa accounted for 7.57% share in 2025, supported by modernization initiatives and increasing interest in efficiency improvements under resource and labor constraints. Adoption tends to start with guidance and semi-autonomous workflows where deployment complexity is lower. As connectivity and service availability improve, the addressable market expands for advanced autonomy use-cases.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

Competition is shaped by OEM-led autonomy-ready platforms, retrofit enablement, and precision-ag ecosystems that combine equipment, positioning, sensing, and digital farm management layers. Differentiation increasingly depends on reliability under field variability, ease of deployment across mixed fleets, and the strength of dealer/service networks that support uptime. Vendors also compete on software intelligence, connectivity, and the ability to deliver continuous feature improvements through updates, diagnostics, and data-driven optimization.

Deere & Company is positioned around integrated autonomy through connected equipment ecosystems that combine machine automation, precision guidance, and digital operations management. Its approach emphasizes operational consistency and workflow integration across the crop cycle, supporting adoption through strong dealer coverage and service capabilities. Continued progress in autonomy features and connected workflows strengthens differentiation by improving ease of scaling across fleets and farm sites.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In January 2025, Deere & Company expanded its autonomous agriculture lineup by unveiling its first autonomy kit for large agricultural tractors alongside new autonomous capabilities for its high-horsepower 9RX tillage tractors, positioning these systems for limited release in 2025 and broader commercialization by 2026 in the autonomous farm equipment market.

- In November 2025, AGCO Corporation announced that at AGRITECHNICA 2025 it will showcase new autonomous and AI-powered systems such as OutRun and RowPilot, integrated across key brands like Fendt and Massey Ferguson, highlighting smart farming and mixed‑fleet management solutions that advance autonomy in farm machinery.

- In November 2025, DJI, through DJI Agriculture, launched new Agras T100, T70P and T25P spray and spreading drones with higher payloads, enhanced safety, and AI-powered automation features designed to improve precision crop protection, further embedding autonomous drone operations into agricultural workflows.

- In January 2026, Kubota Corporation accelerated its agricultural automation push by presenting the commercially available autonomous diesel Kubota M5 Narrow tractor and a new “transformer” robot concept called KVPR at CES, underscoring its strategy to extend autonomous operations beyond tasks like mowing and spraying.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 9,766.23 million |

| Revenue forecast in 2032 |

USD 23,262.27 million |

| Growth rate (CAGR) |

13.2% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type; By Operation; By Offering; By Technology; By Application |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Deere & Company; CNH Industrial; AGCO Corporation; Kubota Corporation; Mahindra & Mahindra Ltd.; DJI; Yanmar Holdings; Trimble Inc.; Topcon Corporation; Monarch Tractor |

| No. of Pages |

332 |

Segmentation

By Product Type

- Tractors

- Harvesters

- Irrigation equipment

- Seeders & planters

- UAVs / drones

- Robotic implements

- Other autonomous farm machinery

By Operation

- Semi- autonomous

- Fully autonomous

By Offering

- Hardware

- Software

- Services

By Technology

- Guidance & steering

- Sensors & perception

- AI / analytics

- GPS / GNSS

- Connectivity platforms

By Application

- Field farming

- Irrigation

- Fertilizing

- Livestock operations

- Specialty crop operations

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa