| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| China Industrial Solvents Market Size 2024 |

USD 4,291.10 million |

| China Industrial Solvents Market CAGR |

9.22% |

| China Industrial Solvents Market 2032 |

USD 8,691.69 million |

Market Overview

China Industrial Solvents market size was valued at USD 4,291.10 million in 2024 and is anticipated to reach USD 8,691.69 million by 2032, at a CAGR of 9.22% during the forecast period (2024-2032).

The China industrial solvents market is driven by strong demand across various industries, including chemicals, pharmaceuticals, automotive, and construction. Rapid industrialization and urbanization, coupled with the expansion of manufacturing and infrastructure development, are key factors fueling market growth. Additionally, technological advancements in solvent formulations and application techniques are enhancing the efficiency and versatility of industrial solvents. The rising emphasis on sustainability and stricter environmental regulations are pushing industries to adopt eco-friendly and low-VOC solvents, further influencing market dynamics. The increasing focus on green chemistry and the shift toward more sustainable production processes also play a significant role in shaping the market’s future. These trends are expected to continue driving the market’s expansion, with demand for industrial solvents set to rise steadily over the forecast period.

Geographically, China’s industrial solvents market is concentrated in key regions such as East China, South China, Southwest China, and Northeast China, each contributing to the growth of the sector. East China, including cities like Shanghai and Beijing, leads the market due to its strong industrial base and robust demand across various sectors like automotive, electronics, and pharmaceuticals. South China, with hubs such as Guangzhou and Shenzhen, sees significant demand driven by electronics and manufacturing industries. Key players in the China industrial solvents market include prominent companies such as China National Petroleum Corporation (CNPC), Sinopec Group, Formosa Plastics Corporation, and Reliance Industries Limited, which play crucial roles in the production and distribution of solvents. Other significant players include Mitsubishi Chemical Holdings Corporation, Sumitomo Chemical Co., Ltd., and LG Chem Ltd., which contribute to technological advancements and the supply of a wide range of solvents across different industries.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The China industrial solvents market was valued at USD 4,291.10 million in 2024 and is projected to reach USD 8,691.69 million by 2032, growing at a CAGR of 9.22% during the forecast period.

- The global industrial solvents market was valued at USD 34,660.50 million in 2024 and is expected to reach USD 60,647.79 million by 2032, growing at a CAGR of 7.24% during the forecast period (2024-2032).

- The market is driven by the expanding industrial sectors like chemicals, pharmaceuticals, and automotive, increasing the demand for solvents.

- Technological advancements in solvent production are enhancing efficiency and fostering new applications across industries.

- The shift toward eco-friendly, low-VOC solvents is a key trend, influenced by stringent environmental regulations.

- The market faces restraints due to fluctuating raw material prices and complex regulatory compliance for emissions and toxicity.

- Competitive landscape includes major players like China National Petroleum Corporation (CNPC), Sinopec Group, and Formosa Plastics Corporation, driving innovation and market growth.

- Regionally, East China dominates the market, followed by South China, with growing solvent demand driven by industrial and manufacturing expansion.

Report Scope

This report segments the China Industrial Solvents market as follows:

Market Drivers

Rapid Industrialization and Urbanization

China’s continuous industrialization and urbanization are significant drivers of growth in the industrial solvents market. As the country develops and modernizes its infrastructure, there is an increased demand for various products, such as paints, coatings, adhesives, and cleaning agents, all of which rely heavily on industrial solvents. For instance, the China Government Work Report 2025 highlights the country’s strategic focus on industrial modernization, emphasizing the expansion of manufacturing facilities and infrastructure development. The expansion of manufacturing facilities across sectors such as automotive, electronics, and chemicals generates substantial demand for solvents to meet production and operational requirements. Moreover, the growth of urban centers and the increase in construction activities further fuel solvent demand, especially in industries like construction and coatings. These trends suggest a robust outlook for industrial solvent consumption as the industrial base in China continues to evolve.

Technological Advancements in Solvent Production

Technological advancements in the production and application of industrial solvents are playing a key role in the growth of the Chinese market. Innovations in solvent formulations have resulted in more efficient, versatile, and cost-effective solutions that cater to diverse industrial needs. For instance, the development of high-performance solvents with improved solvent strength and faster drying times benefits industries like coatings and adhesives. Additionally, the growing availability of specialized solvents for use in emerging technologies, such as electronics and pharmaceuticals, is also contributing to market growth. These advancements in solvent production ensure that industries can meet stringent production standards, ultimately driving demand for these materials.

Regulatory Push for Environmentally Friendly Solutions

Stringent environmental regulations and the rising awareness of sustainability are increasingly influencing the industrial solvents market in China. With growing concerns over air pollution and health risks associated with solvent emissions, the Chinese government has implemented tighter environmental controls, encouraging the adoption of low-VOC (volatile organic compounds) and eco-friendly solvents. These regulations are compelling industries to shift toward greener alternatives, promoting the development and adoption of environmentally safer products. Solvents that are biodegradable, non-toxic, and low in emissions are gaining traction in various industrial applications, including automotive and manufacturing. As these regulatory frameworks evolve, businesses are increasingly aligning with environmental goals, further driving the growth of the market.

Expanding Demand Across Key End-Use Industries

The industrial solvents market in China is also being fueled by growing demand from key end-use industries, including chemicals, pharmaceuticals, paints and coatings, and electronics. For instance, the Asia Pacific Industrial Solvents Market Report highlights the increasing consumption of solvents in China’s manufacturing sector, particularly in chemicals and pharmaceuticals. The chemical manufacturing sector, which produces a wide range of products such as agrochemicals, lubricants, and specialty chemicals, relies heavily on solvents for various processes such as extraction, purification, and formulation. Additionally, the pharmaceutical industry, particularly in the production of active pharmaceutical ingredients (APIs) and formulation processes, requires high-quality solvents to ensure the efficacy and safety of their products. The increasing production of electronic devices and automotive products, coupled with the rising popularity of industrial coatings in construction, has further boosted the demand for solvents. This broad and diverse application base across multiple industries ensures steady and sustained growth in China’s industrial solvents market.

Market Trends

Shift Toward Eco-Friendly and Sustainable Solvents

A prominent trend in China’s industrial solvents market is the increasing demand for eco-friendly and sustainable solvent options. With growing concerns over environmental pollution and health risks associated with traditional solvents, there is a significant shift toward low-VOC (volatile organic compounds), biodegradable, and non-toxic solvents. For instance, the Green Solvents and Bio-Solvents Market highlights that industries such as paints and coatings, adhesives, and pharmaceuticals are increasingly adopting bio-based solvents to comply with environmental regulations. This trend is being driven by both consumer preferences for safer, greener products and stricter government regulations aimed at reducing industrial emissions and pollution. Industries, especially those in the automotive, coatings, and adhesives sectors, are embracing green chemistry practices and adopting solvents that align with sustainability goals. The shift toward eco-friendly solvents is expected to accelerate as businesses focus on compliance with environmental standards and contribute to reducing their carbon footprint.

Increasing Use of Solvents in Emerging Technologies

Another key trend is the growing use of industrial solvents in emerging technologies such as electronics, pharmaceuticals, and renewable energy. For instance, the Asia Pacific Industrial Solvents Market highlights the increasing consumption of solvents in China’s manufacturing sector, particularly in electronics and pharmaceuticals. As the demand for electronic devices and electric vehicles (EVs) continues to rise, there is an increasing need for solvents in applications like cleaning, coatings, and production processes. In the pharmaceutical sector, solvents are crucial for the synthesis and formulation of drugs, including the growing production of biologics and personalized medicine. Solvents are also playing an essential role in the manufacturing of batteries, particularly in the renewable energy sector, where the demand for solvents to produce lithium-ion batteries is escalating. This trend indicates that industrial solvents will continue to evolve to meet the specific needs of these high-tech sectors, driving market growth in the long term.

Automation and Process Optimization in Solvent Use

The industrial solvents market in China is also witnessing a trend toward automation and process optimization. Companies are increasingly adopting automated systems for solvent handling, mixing, and dispensing, which enhance operational efficiency and reduce human error. Automation allows for more precise control over solvent usage, minimizing waste and improving overall process efficiency. Additionally, automation systems help companies comply with stringent safety and environmental standards by reducing the risk of accidents and emissions. The trend of process optimization is being driven by the need for higher productivity, cost reduction, and enhanced safety protocols, making it an important factor in shaping the future of solvent use in industrial applications.

Growth of E-Commerce and Online Sales Channels

The rise of e-commerce and online sales channels is another notable trend impacting China’s industrial solvents market. With digital platforms facilitating direct interactions between manufacturers and end-users, more businesses are turning to online channels to procure industrial solvents. E-commerce platforms offer customers greater convenience, competitive pricing, and easier access to a broader range of solvent products. This shift is particularly evident in smaller businesses and industries where ordering in bulk or through traditional distribution channels may not be as efficient. As e-commerce continues to grow, it will reshape the distribution dynamics of industrial solvents, providing new opportunities for market expansion and customer engagement in China.

Market Challenges Analysis

Stringent Regulatory Compliance and Environmental Concerns

One of the major challenges facing the China industrial solvents market is the increasing pressure to comply with stringent environmental regulations. As the government enforces stricter controls on volatile organic compound (VOC) emissions and harmful chemical pollutants, manufacturers face the complex task of meeting these regulations while maintaining cost-effectiveness and product performance. The shift toward eco-friendly solvents, while beneficial in the long term, can be expensive and technically challenging for industries to implement. Many traditional solvents, which are more cost-effective, still offer superior performance in certain applications, making it difficult for businesses to transition to greener alternatives without incurring significant additional costs. Moreover, maintaining compliance with these evolving environmental standards requires continuous investment in research, development, and adaptation of production processes, adding an extra layer of complexity to solvent manufacturing and distribution.

Fluctuating Raw Material Prices and Supply Chain Disruptions

Another significant challenge for the industrial solvents market in China is the volatility in raw material prices and supply chain disruptions. Many industrial solvents are derived from petrochemical products, which are susceptible to fluctuations in oil prices and supply chain interruptions. For instance, the European Central Bank Economic Bulletin discusses global supply chain disruptions and their effects on economic activity, highlighting the impact of raw material shortages on industrial production. These price fluctuations can lead to increased production costs, affecting the profitability of solvent manufacturers. Additionally, geopolitical factors, such as trade tensions and natural disasters, can cause delays and shortages in raw material supplies, further complicating the supply chain. Such uncertainties create challenges for manufacturers in terms of inventory management, pricing strategies, and meeting customer demands on time. The market’s reliance on global supply chains also increases vulnerability to disruptions, which can result in higher costs and reduced market stability for Chinese solvent producers.

Market Opportunities

The China industrial solvents market presents numerous growth opportunities, particularly driven by the rising demand for eco-friendly and sustainable products. As environmental regulations become more stringent, industries are increasingly compelled to adopt low-VOC, biodegradable, and non-toxic solvents. This shift presents a significant opportunity for solvent manufacturers to innovate and develop greener alternatives that meet the needs of both regulatory requirements and consumer preferences. The growing focus on sustainability in sectors such as automotive, coatings, and construction offers a pathway for businesses to differentiate themselves by providing environmentally responsible products. As Chinese industries continue to align with global sustainability trends, there is substantial room for growth in the production and adoption of green solvents.

Another promising opportunity lies in the expansion of industrial solvent use in emerging technologies. China’s rapid advancements in electronics, electric vehicles (EVs), renewable energy, and pharmaceuticals create new avenues for solvent applications. In the electronics sector, solvents are critical for cleaning and coating components, while in the growing EV industry, solvents are essential for manufacturing batteries and other components. Similarly, the pharmaceutical industry’s demand for solvents in drug production and formulation continues to rise as China’s healthcare sector expands. These high-growth industries present a lucrative opportunity for industrial solvent manufacturers to cater to evolving market needs. By developing specialized solvents tailored for these advanced technologies, manufacturers can position themselves as key players in a rapidly changing market.

Market Segmentation Analysis:

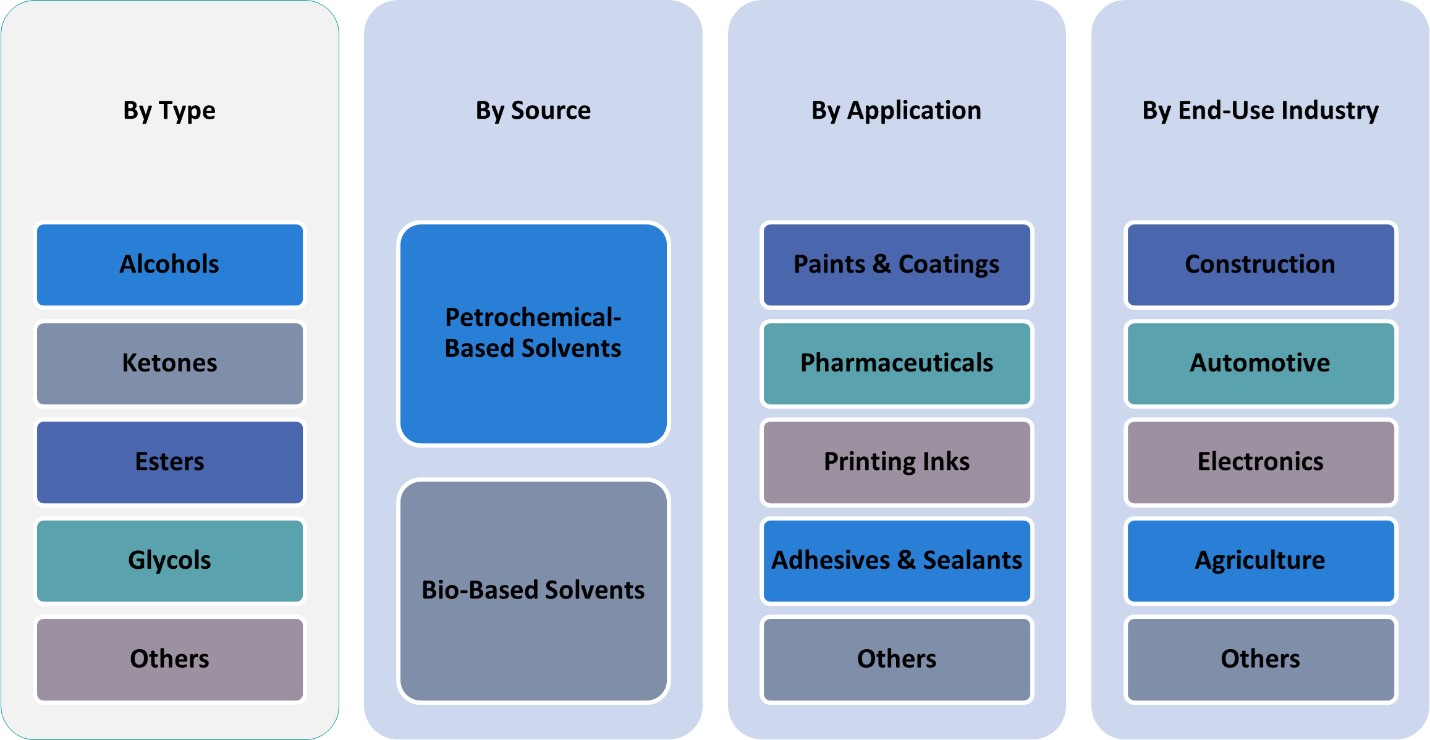

By Type:

The China industrial solvents market is segmented by type into alcohols, ketones, esters, glycols, and others. Alcohols are among the most widely used solvents due to their versatility and strong solvent power. They are commonly employed in the production of paints, coatings, adhesives, and pharmaceuticals, offering a balance between efficiency and cost-effectiveness. Ketones, especially acetone and methyl ethyl ketone (MEK), are essential for their ability to dissolve a wide range of substances and their quick evaporation rate. These properties make ketones ideal for use in coatings, cleaning agents, and chemical manufacturing. Esters, known for their pleasant odor and low toxicity, are often utilized in the paint and coatings industry, as well as in cosmetics and perfumes. Glycols, particularly ethylene and propylene glycol, are widely used in antifreeze formulations, paints, and as solvents in the production of plastics. The “others” category includes specialized solvents such as chlorinated hydrocarbons and terpenes, which cater to niche applications where specific solvent properties are required.

By Application:

The industrial solvents market in China is also segmented by application into paints and coatings, pharmaceuticals, printing inks, adhesives and sealants, and others. The paints and coatings segment holds the largest share, driven by the strong demand in the construction, automotive, and consumer goods sectors. Solvents play a critical role in formulation, thinning, and ensuring smooth application of paints and coatings. The pharmaceutical sector is another significant application area, where solvents are used in drug formulation, extraction, and purification processes. With the growing healthcare industry in China, demand for solvents in this sector is increasing. Printing inks also represent a crucial segment, as solvents are necessary for controlling ink viscosity and ensuring proper adhesion to paper, plastic, and other materials. Adhesives and sealants are another major application for industrial solvents, especially in the automotive, construction, and packaging industries, where strong bonding agents are essential. The “others” segment encompasses a variety of smaller applications, such as cosmetics, cleaning agents, and lubricants.

Segments:

Based on Type:

- Alcohols

- Ketones

- Esters

- Glycols

- Others

Based on Application:

- Paints & Coatings

- Pharmaceuticals

- Printing Inks

- Adhesives & Sealants

- Others

Based on End- Use:

- Construction

- Automotive

- Electronics

- Agriculture

- Others

Based on Source:

- Petrochemical-Based Solvents

- Bio-Based Solvents

Based on the Geography:

- Beijing

- Shanghai

- Guangzhou

- Shenzhen

Regional Analysis

East China

East China, which includes major economic hubs like Beijing and Shanghai, holds the largest share of the market, accounting for nearly 40% of the total market. This region benefits from its strong industrial base, extensive manufacturing activities, and well-established chemical industries. Shanghai, being a leading commercial center, has a high demand for solvents in the paints and coatings, automotive, and electronics sectors, while Beijing’s demand is driven by its growing pharmaceutical and construction industries. The favorable business environment, coupled with robust infrastructure, positions East China as the dominant region in the industrial solvents market.

South China

South China, primarily represented by Guangzhou and Shenzhen, accounts for approximately 25% of the market. The region’s manufacturing power, particularly in electronics, automotive, and consumer goods, significantly drives solvent demand. Shenzhen, with its rapid technological advancements and flourishing electronics industry, is a major consumer of industrial solvents, especially in the production of electronic components and displays. Guangzhou’s manufacturing and chemical industries also rely heavily on solvents for various applications, including coatings, adhesives, and printing inks. The region’s proximity to key ports and trade routes further enhances its market share and access to raw materials.

Southwest China

Southwest China, including cities like Chengdu and Chongqing, represents about 15% of the market share. While this region is not as industrially developed as East or South China, it is gaining traction due to the rapid development of manufacturing and infrastructure projects. Solvents are increasingly in demand in the construction and automotive sectors, both of which are growing rapidly in the region. The rise of green chemistry and eco-friendly products is also creating opportunities for solvent manufacturers to cater to industries in Southwest China, where the demand for sustainable and low-VOC solvents is expected to increase.

Northeast China

Northeast China, encompassing regions like Liaoning and Heilongjiang, holds about 10% of the market share. This region’s solvent demand is primarily driven by its heavy industries, including steel, petrochemicals, and automotive manufacturing. While not as dynamic as other regions in terms of growth, Northeast China still plays a key role in the overall industrial solvents market. The demand for solvents in the region is influenced by its strong industrial base, though the growth rate in this region is slower compared to more industrially diverse regions like East or South China.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- China National Petroleum Corporation (CNPC)

- Formosa Plastics Corporation

- Reliance Industries Limited

- Sinopec Group

- Mitsubishi Chemical Holdings Corporation

- Sumitomo Chemical Co., Ltd.

- Toray Industries, Inc.

- LG Chem Ltd.

- Tata Chemicals Ltd.

- SK Innovation Co., Ltd.

Competitive Analysis

The competitive landscape of the China industrial solvents market is characterized by the presence of several prominent players who dominate production, innovation, and distribution. Key players such as China National Petroleum Corporation (CNPC), Sinopec Group, Formosa Plastics Corporation, Reliance Industries Limited, Mitsubishi Chemical Holdings Corporation, Sumitomo Chemical Co., Ltd., Toray Industries, Inc., LG Chem Ltd., Tata Chemicals Ltd., and SK Innovation Co., Ltd. are actively shaping the market. These companies leverage their strong manufacturing capabilities, extensive distribution networks, and advanced technological innovations to maintain a competitive edge. These companies invest heavily in research and development to create more efficient and environmentally friendly solvent products, responding to both consumer demand and regulatory pressures for sustainability. Furthermore, strong vertical integration in the supply chain allows for better control over raw material costs and production efficiency. In addition to product innovation, competition in the market is driven by the ability to meet stringent environmental regulations, particularly those related to VOC emissions and toxicity levels. Companies are increasingly focusing on developing low-VOC, biodegradable, and non-toxic solvents to align with China’s growing environmental standards. Additionally, regional competition is intensifying as local companies, particularly in high-growth areas like East and South China, expand their capabilities to cater to local industries, including automotive, electronics, and pharmaceuticals. Companies are also vying for market share through strategic partnerships and acquisitions to enhance their product portfolios and geographic reach, ensuring their long-term competitiveness in this dynamic market.

Recent Developments

- In April 2025, Eastman announced off-list price increases for several EOD (Ethylene Oxide Derivatives) solvents, including Eastman™ DB Solvent, effective April 7, 2025, reflecting ongoing cost and market pressures.

- In March 2025, BASF reported generating approximately €11 billion in 2024 sales from products launched in the past five years, driven by R&D focused on sustainability, biodegradable materials, and digital transformation. The company filed 1,159 new patents in 2024, with 45% targeting sustainability. R&D investment in 2024 was €2.1 billion, with a similar budget planned for 2025.

- In March and April 2025, Shell is restructuring its global chemicals business to boost profitability and reduce capital spending by 2030. This includes exploring strategic partnerships in the U.S., potentially closing some European assets, and selling existing assets like the Singapore refinery and chemical complex. The company aims to streamline operations, focus on core businesses, and improve returns for shareholders.

- In March 2025, BASF is expanding its production capacity for aminic antioxidants at its Puebla, Mexico site, targeting the growing demand for long-life lubricants. The project is set for completion in 2026.

- In March 2025, ExxonMobil announced a $100 million upgrade to its Baton Rouge, Louisiana plant to produce ultra-high-purity (99.999%) isopropyl alcohol (IPA) for the semiconductor industry by 2027.

- InMarch 2024, Dow announced plans to invest in new ethylene derivatives capacity-including carbonate solvents-on the U.S. Gulf Coast. This investment, supported by the U.S. Department of Energy, aims to supply carbonate solvents for lithium-ion batteries, supporting the domestic EV and energy storage market. The facility will capture over 90% of CO₂ from ethylene oxide production, aligning with sustainability goals.

Market Concentration & Characteristics

The China industrial solvents market exhibits a moderate level of concentration, with a few large multinational and domestic players dominating the landscape. While global giants with advanced technological capabilities lead in terms of production and innovation, local companies continue to play a significant role by catering to regional demand and offering cost-competitive solutions. The market is characterized by high competition, particularly in sectors such as paints and coatings, pharmaceuticals, and chemicals. Innovation in environmentally friendly solvents, driven by regulatory pressures for low-VOC and biodegradable products, is a key differentiator among market players. Additionally, companies are focusing on enhancing their distribution networks to reach diverse industrial sectors, from electronics to automotive. The growing emphasis on sustainability and regulatory compliance is reshaping the market, pushing companies to invest in green technologies and solutions. As demand for solvents continues to expand across various industries, market dynamics are expected to evolve with increased focus on both performance and environmental impact.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, End-Use, Source and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The China industrial solvents market is expected to continue growing at a strong pace, driven by expanding industrial sectors and urbanization.

- Increasing demand for eco-friendly, low-VOC solvents will drive product innovation and push manufacturers toward sustainable solutions.

- Technological advancements in solvent formulations will improve efficiency and enable more specialized applications across industries.

- Stricter environmental regulations will prompt more companies to focus on developing biodegradable and non-toxic solvents.

- The shift toward electric vehicles and renewable energy sources will create new opportunities for industrial solvents in battery production and related industries.

- Growth in the pharmaceutical and healthcare industries will lead to a rise in demand for high-purity solvents for drug formulation and production.

- Expansion in the electronics sector will drive the need for solvents in cleaning and coating applications.

- Increased automation and process optimization in solvent handling will enhance operational efficiency and reduce waste in industrial applications.

- The competitive landscape will see more consolidation as companies seek strategic acquisitions and partnerships to expand market share.

- Regional demand will remain diverse, with East and South China continuing to dominate, while Southwest and Northeast regions experience accelerated growth.