Market Overview

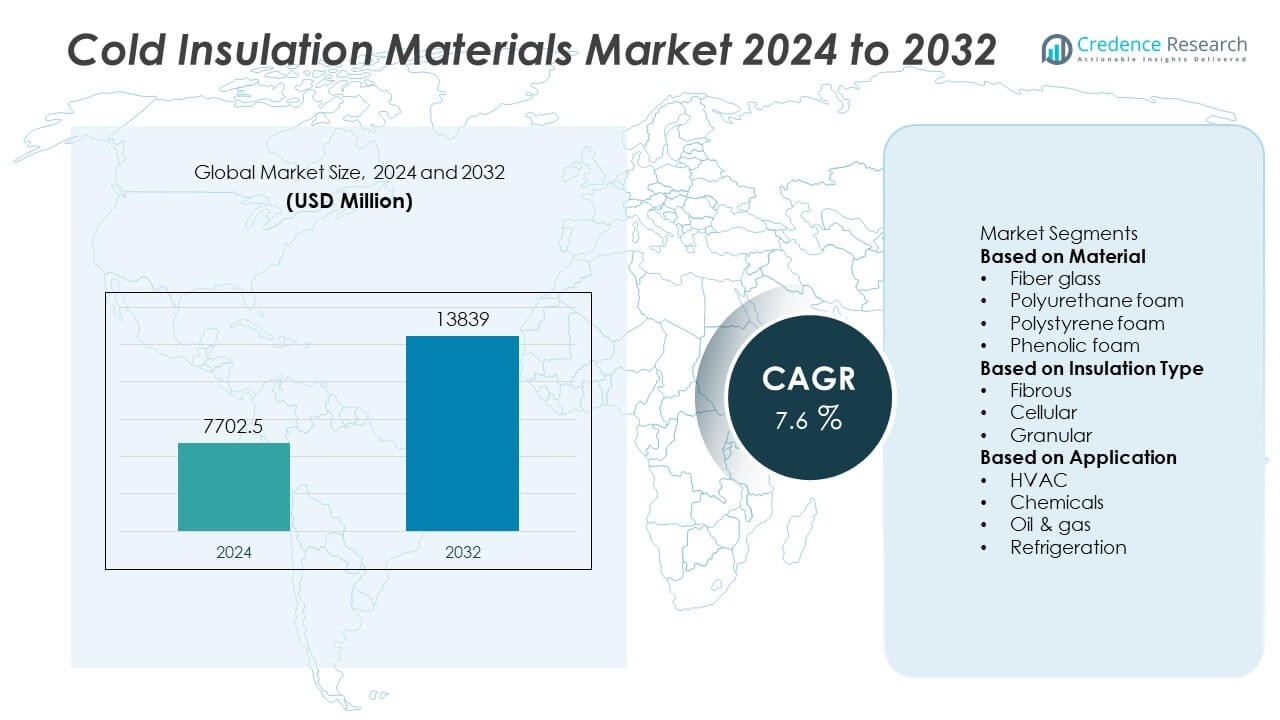

The Cold Insulation Materials Market was valued at USD 7,702.5 million in 2024 and is projected to reach USD 13,839 million by 2032, growing at a CAGR of 7.6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Cold Insulation Materials Market Size 2024 |

USD 7,702.5 Million |

| Cold Insulation Materials Market, CAGR |

7.6% |

| Cold Insulation Materials Market Size 2032 |

USD 13,839 Million |

The Cold Insulation Materials Market grows due to rising demand for energy-efficient solutions across industrial, commercial, and residential sectors. It supports temperature-sensitive applications by reducing thermal losses and improving system performance. Increasing regulations on energy conservation and sustainability drive adoption of advanced insulation materials. Technological innovations enhance material properties such as thermal resistance and durability, expanding application scope.

The Cold Insulation Materials Market exhibits strong regional variation driven by industrial development and regulatory frameworks. North America leads adoption with a focus on energy efficiency in commercial and residential buildings, supported by stringent environmental regulations. Europe follows closely, driven by sustainable construction practices and innovations in eco-friendly insulation solutions. The Asia Pacific region shows rapid growth fueled by expanding industrial infrastructure and urbanization, with countries like China and India investing heavily in cold storage and refrigeration sectors. Key players driving advancements in this market include Armacell, known for its flexible foam insulation technologies; Owens Corning, which specializes in fiberglass and foam products; Saint-Gobain, a leader in innovative insulation materials; and Kingspan Group, recognized for high-performance insulation systems.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Cold Insulation Materials Market size was valued at USD 7,702.5 million in 2024 and is projected to grow steadily during the forecast period.

- Increasing demand for energy-efficient solutions in commercial and residential construction drives market growth worldwide.

- Growing adoption of sustainable and eco-friendly insulation materials influences trends across regions.

- Leading companies focus on technological innovation to improve product performance and reduce environmental impact.

- High initial installation costs and availability of cheaper alternatives restrain market expansion in some regions.

- North America and Europe remain prominent markets due to stringent regulations and infrastructure modernization.

- Rapid industrialization and urbanization in Asia Pacific boost demand for cold insulation materials in emerging economies.

Market Drivers

Rising Demand for Energy Efficiency in Industrial and Commercial Buildings Driving Market Expansion

The Cold Insulation Materials Market experiences growth propelled by increasing emphasis on energy-efficient solutions in industrial and commercial sectors. It helps reduce thermal losses in refrigeration systems, cryogenic storage, and HVAC applications, leading to significant energy savings. Strict government regulations on energy consumption push industries to adopt advanced insulation materials that maintain low temperatures effectively. The material’s ability to minimize heat transfer extends equipment life and reduces operational costs. Growing awareness about sustainable practices further accelerates demand. Industries such as food processing, pharmaceuticals, and petrochemicals benefit from enhanced temperature control. This growing focus on energy conservation supports widespread market adoption.

- For instance, Armacell developed a flexible elastomeric foam that achieves thermal conductivity as low as 0.032 W/m·K, which substantially lowers heat loss in HVAC systems and industrial refrigeration, enabling clients to reduce energy consumption and maintenance frequency.

Technological Advancements in Insulation Materials Enhancing Performance and Versatility

The market benefits from continuous innovation in cold insulation materials that improve thermal resistance and durability. New developments in aerogels, vacuum insulation panels, and polymer foams provide superior insulating properties while reducing material thickness and weight. These materials offer enhanced resistance to moisture, compression, and chemical exposure, broadening their application scope. The Cold Insulation Materials Market gains from these technological breakthroughs that improve installation ease and lifecycle performance. Industries requiring strict temperature control, such as cryogenics and LNG storage, increasingly rely on these advanced solutions. Innovations also address environmental concerns by offering recyclable and low-global warming potential options. This progression strengthens the market’s ability to meet diverse industrial demands.

- For instance, Owens Corning introduced a high-performance spray foam insulation with a closed-cell density of 2.2 pounds per cubic foot, delivering improved compressive strength and R-value that enhances durability in cryogenic storage tanks.

Expansion of Cold Chain Infrastructure Accelerating Market Demand Worldwide

Global growth in cold chain logistics, especially in the food and pharmaceutical sectors, drives demand for effective cold insulation materials. It ensures product integrity during transportation and storage by maintaining stable low temperatures. Emerging economies invest heavily in cold storage facilities, refrigerated transport, and distribution networks to reduce spoilage and meet safety standards. The Cold Insulation Materials Market supports these infrastructure developments with materials that provide reliable thermal barriers. Regulatory bodies enforce strict temperature controls for perishable goods, reinforcing the need for high-performance insulation. This expansion fosters new applications and increases material consumption. Continuous infrastructure upgrades in healthcare and agriculture sectors also stimulate growth.

Stringent Environmental Regulations Promoting Sustainable Insulation Solutions

Environmental policies targeting energy efficiency and emissions reduction influence the Cold Insulation Materials Market significantly. Manufacturers respond by developing eco-friendly insulation products with lower environmental impact throughout their lifecycle. It supports compliance with regulations limiting volatile organic compounds (VOCs) and greenhouse gas emissions associated with traditional materials. The market shifts toward bio-based, recyclable, and non-toxic alternatives that maintain performance standards. This regulatory pressure encourages investment in research and adoption of greener technologies. End-users prefer materials aligned with sustainability goals to enhance their environmental credentials. This dynamic strengthens the market’s role in promoting responsible industrial practices.

Market Trends

Increasing Adoption of Advanced Aerogel and Vacuum Insulation Technologies Enhancing Market Growth

The Cold Insulation Materials Market shows a clear shift toward advanced technologies like aerogels and vacuum insulation panels (VIPs). These materials deliver superior thermal resistance with minimal thickness, making them ideal for space-constrained applications in refrigeration and cryogenics. It offers enhanced durability and moisture resistance compared to traditional insulation options, improving overall system efficiency. Industries such as LNG storage, pharmaceuticals, and cold chain logistics actively incorporate these technologies to meet stringent thermal requirements. Manufacturers invest in research to improve aerogel production scalability and reduce costs, expanding its commercial use. This trend underscores the market’s focus on high-performance, lightweight insulation solutions.

- For instance, data from the U.S. Department of Energy shows that vacuum insulation panels can achieve thermal conductivity values as low as 0.004 W/m·K, significantly outperforming traditional insulation materials and enabling up to a 50% reduction in insulation thickness in refrigeration systems.

Growth of Cold Chain Infrastructure and Refrigerated Transport Driving Material Demand

Expansion in global cold chain logistics and refrigerated transportation fuels demand for reliable cold insulation materials. It plays a critical role in maintaining product quality and safety in sectors like food processing and pharmaceuticals, where temperature control is paramount. Emerging markets are increasing investments in refrigerated warehouses and transport fleets, stimulating consumption of advanced insulation solutions. The Cold Insulation Materials Market supports these developments with materials that offer consistent thermal performance and compliance with safety standards. Innovations targeting ease of installation and longer service life further boost adoption. The rise of e-commerce and demand for fresh, perishable goods reinforce this growth trend.

- For instance, a study published by the International Institute of Refrigeration highlights that advanced insulation panels used in refrigerated transport reduce temperature fluctuations inside containers by up to 3°C during transit, thereby maintaining product quality and extending shelf life for perishable goods.

Focus on Sustainability and Eco-Friendly Insulation Products Gaining Traction

Sustainability drives innovation and purchasing decisions within the Cold Insulation Materials Market. It encourages the development of eco-friendly products that reduce carbon footprint and adhere to environmental regulations. Manufacturers prioritize bio-based, recyclable, and low-VOC materials to align with growing consumer and regulatory demands for green solutions. This trend enhances the market’s appeal among industries aiming to improve their environmental credentials without compromising performance. Investments in sustainable production technologies and raw material sourcing expand the availability of greener insulation options. It reflects a broader industrial movement toward responsible manufacturing and energy conservation.

Integration of Smart and Multifunctional Insulation Systems Boosting Market Potential

The Cold Insulation Materials Market increasingly explores smart insulation systems that incorporate sensors and adaptive materials. These innovations enable real-time monitoring of temperature and insulation performance, facilitating predictive maintenance and operational efficiency. It benefits sectors requiring precise thermal control, such as pharmaceuticals and aerospace. Multifunctional materials combining insulation with fire resistance or mechanical strength are gaining popularity, enhancing safety and durability. Collaborations between material scientists and technology firms accelerate development of these integrated solutions. This trend points to a future where insulation materials provide enhanced functionality beyond traditional thermal protection.

Market Challenges Analysis

High Initial Costs and Complex Installation Procedures Hindering Market Expansion

The Cold Insulation Materials Market faces challenges due to the high upfront costs associated with advanced insulation products like aerogels and vacuum insulation panels. These materials often require specialized installation techniques and trained personnel, which increases project expenses and limits adoption in cost-sensitive applications. It encounters resistance in industries where budget constraints and quick turnaround times prioritize cheaper, conventional insulation alternatives. The complexity of retrofitting existing infrastructure with newer insulation systems further restrains market growth. Manufacturers must address these cost and installation barriers to encourage wider acceptance and deployment across diverse sectors.

Raw Material Availability and Performance Limitations Impacting Market Reliability

The Cold Insulation Materials Market also contends with issues related to raw material supply and product performance consistency. Limited availability of high-quality raw materials such as silica for aerogels or specialized films for vacuum panels affects production scalability and pricing stability. It faces challenges ensuring long-term durability and maintaining thermal performance under harsh environmental conditions, especially in outdoor or industrial settings. Variations in material properties can lead to insulation failure or increased maintenance costs, undermining customer confidence. Industry players need to focus on enhancing raw material sourcing and improving product reliability to sustain market momentum.

Market Opportunities

Expanding Demand for Energy-Efficient Buildings Creating Growth Opportunities

The Cold Insulation Materials Market benefits from increasing global emphasis on energy-efficient construction and sustainable building practices. It supports the development of advanced insulation solutions that significantly reduce thermal losses in residential, commercial, and industrial buildings. Governments worldwide promote stricter building codes and regulations mandating improved insulation standards, driving market expansion. Growing urbanization and infrastructure development further increase the need for effective thermal management. Companies investing in research to enhance insulation materials’ performance and reduce installation complexity can capitalize on these emerging opportunities. The trend toward green building certifications also boosts demand for high-quality cold insulation products.

Rising Adoption in Industrial and Cold Chain Sectors Driving Market Potential

The Cold Insulation Materials Market finds substantial opportunities in industrial applications, including refrigeration, cold storage, and logistics. It plays a critical role in maintaining temperature control for pharmaceuticals, food products, and chemicals during transportation and storage. Expansion in the cold chain infrastructure globally fuels the need for reliable and efficient insulation materials. Technological advancements enabling lighter, thinner, yet more effective insulation solutions open new avenues in these sectors. Companies focusing on customized solutions for specific industrial requirements can gain a competitive edge. This growing adoption supports sustained growth and diversification within the market.

Market Segmentation Analysis:

By Material

The Cold Insulation Materials Market segments by material into foam glass, polyurethane foam, extruded polystyrene, aerogel, and others. Foam glass remains prominent due to its excellent thermal insulation properties, non-combustibility, and resistance to moisture and chemicals. Polyurethane foam offers high thermal resistance and structural strength, making it suitable for refrigeration and cold storage applications. Extruded polystyrene provides durability and moisture resistance, favored in industrial and commercial insulation projects. Aerogel, known for its ultra-low thermal conductivity, finds use in high-performance applications despite higher costs. Each material type addresses specific insulation requirements, influencing material selection based on application demands and environmental conditions.

- For instance, Knauf Insulation produces foam glass with a compressive strength of up to 3.5 MPa and thermal conductivity around 0.08 W/m·K, ensuring durability and excellent insulation in chemical processing plants.

By Insulation Type

By insulation type, the Cold Insulation Materials Market classifies into rigid board insulation, flexible insulation, and spray foam insulation. Rigid board insulation leads the market due to its ease of installation, high compressive strength, and stable thermal resistance, ideal for pipeline and refrigeration system insulation. Flexible insulation offers adaptability around irregular surfaces and is widely used in HVAC systems and cold storage. Spray foam insulation provides seamless coverage and excellent air sealing properties, contributing to enhanced energy efficiency in building envelopes. The choice of insulation type impacts installation efficiency, thermal performance, and maintenance costs across industries.

- For instance, BASF’s spray foam insulation products demonstrate closed-cell densities of 2.0 pounds per cubic foot, delivering an R-value of approximately 7.0 per inch, which enhances air sealing and thermal performance in commercial refrigeration installations.

By Application

In terms of application, the Cold Insulation Materials Market serves industrial, commercial, and residential sectors. The industrial segment dominates due to extensive use in cold storage facilities, refrigeration units, and chemical processing plants requiring consistent low-temperature environments. Commercial applications include supermarkets, office buildings, and hospitals where temperature control and energy conservation are critical. Residential applications focus on improving building envelope insulation to reduce heating and cooling demands, supporting energy efficiency goals. Each application segment demands tailored insulation solutions, driving product innovation and diversification in the market.

Segments:

Based on Material

- Fiber glass

- Polyurethane foam

- Polystyrene foam

- Phenolic foam

Based on Insulation Type

- Fibrous

- Cellular

- Granular

Based on Application

- HVAC

- Chemicals

- Oil & gas

- Refrigeration

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

The Cold Insulation Materials Market demonstrates a diverse regional distribution, with North America accounting for a significant market share. The region benefits from stringent energy efficiency regulations and high investments in infrastructure development. Key industries such as oil & gas, chemical processing, and cold storage facilities actively deploy cold insulation materials to improve thermal efficiency and reduce operational costs. The U.S. Department of Energy has reported that improved insulation in industrial applications can reduce energy loss by up to 30%, reinforcing market demand. Manufacturers in North America focus on developing eco-friendly insulation products that comply with local environmental standards, driving adoption further.

Europe

Europe holds a considerable share of the Cold Insulation Materials Market, supported by the region’s aggressive environmental policies and sustainability targets. Countries like Germany, the UK, and France lead in adopting advanced insulation solutions in commercial and industrial sectors. The European Commission’s emphasis on reducing carbon emissions encourages the use of materials with superior thermal properties. Data from Eurostat indicates that energy consumption in European manufacturing facilities can be cut by nearly 25% through effective insulation strategies. This regulatory environment compels manufacturers to innovate and expand cold insulation product lines, supporting market growth.

Asia Pacific

The Asia Pacific region exhibits rapid growth and occupies a growing market share in cold insulation materials due to accelerating industrialization and urbanization. Emerging economies such as China, India, and South Korea invest heavily in infrastructure and cold chain logistics to support their expanding manufacturing and food storage sectors. The Ministry of Industry and Information Technology of China reported that industrial energy consumption could be lowered by 20% through improved insulation technology adoption. Increasing awareness of energy conservation and government initiatives for sustainable manufacturing practices propel the market in this region. Local manufacturers and international players actively collaborate to meet rising demand.

Middle East & Africa

The Middle East & Africa region holds a moderate share of the Cold Insulation Materials Market, driven primarily by oil & gas industry requirements and harsh climatic conditions necessitating efficient thermal insulation. Countries like Saudi Arabia, UAE, and Qatar invest in refining and petrochemical industries, which rely extensively on cold insulation materials for pipelines and storage tanks. According to reports from the International Energy Agency, improved insulation in the Middle East’s industrial plants can reduce cooling energy demand by up to 15%. The region’s market growth is influenced by ongoing infrastructure projects and increasing awareness about energy efficiency in industrial operations.

Latin America

Latin America occupies a smaller but steadily growing share in the Cold Insulation Materials Market. Brazil and Mexico are leading countries driving demand through investments in the manufacturing, food processing, and chemical sectors. The National Institute of Metrology in Brazil highlights that proper insulation in industrial refrigeration can improve energy savings by 18%. Efforts to modernize infrastructure and meet international environmental standards support adoption rates. The region faces challenges related to fluctuating raw material costs but presents opportunities through expanding industrial applications and government incentives for energy-efficient technologies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Kingspan Group

- Bauder

- Owens Corning

- BASF

- Saint-Gobain

- Armacell

- Knauf Insulation

- VASmann

- Rockwool

- Interplasp

Competitive Analysis

Leading players in the Cold Insulation Materials Market include Armacell, BASF, Kingspan Group, Owens Corning, Rockwool, Knauf Insulation, Saint-Gobain, Bauder, Interplasp, and VASmann. These companies maintain competitive positions through continuous innovation, expanding product portfolios, and strategic partnerships. Armacell has advanced its elastomeric foam insulation technology, achieving thermal conductivity values as low as 0.034 W/m·K, enhancing energy efficiency in HVAC applications. BASF focuses on developing bio-based and recyclable insulation materials, aligning with sustainability goals and reducing environmental impact. Kingspan Group invests heavily in R&D, introducing vacuum insulation panels with superior insulation performance, reaching thermal resistance (R-value) up to 50 per inch. Owens Corning leverages its global manufacturing footprint to ensure consistent supply and customization options for diverse industries. These key players actively pursue geographic expansion and acquisitions to strengthen market presence, particularly in high-growth regions. Their competitive strategies include cost optimization, enhancing product durability, and meeting evolving regulatory requirements, which collectively drive market leadership. Their ability to innovate while managing supply chains effectively positions them strongly in the growing Cold Insulation Materials Market.

Recent Developments

- In July 2025, BASF continues to be a prominent global leader in polyurethane-based cold insulation, valued for its low thermal conductivity and vapor permeability, making it ideal for freezing and cold storage applications. This type of insulation is crucial for maintaining temperature-sensitive environments in various industries.

- In April 2025, Bauder was mentioned among major technical insulation players. It remains active in the technical and cold insulation market, emphasizing sustainable, energy-efficient, and innovative fiber-based products for various industries, including HVAC and industrial cooling.

- In April 2025, Armacell, known for its flexible elastomeric foams, introduced innovations in technical insulation, focusing on enhanced thermal performance and adaptability in cold environments.

Market Concentration & Characteristics

The Cold Insulation Materials Market exhibits a moderately concentrated structure, with a few leading players commanding a significant share through strong brand presence, technological innovation, and extensive distribution networks. It features a blend of established multinational corporations and regional manufacturers competing on product quality, performance, and sustainability. The market’s characteristics include a strong emphasis on energy efficiency, compliance with evolving environmental regulations, and growing demand for eco-friendly and recyclable insulation solutions. It demands continuous investment in research and development to improve thermal resistance, durability, and ease of installation. Product differentiation plays a critical role, with companies offering specialized materials tailored for diverse applications such as industrial refrigeration, building insulation, and cold storage. Supply chain integration and strategic partnerships contribute to market stability and expansion into emerging regions. The market’s competitive landscape encourages innovation while maintaining cost-effectiveness, driving manufacturers to enhance raw material sourcing and optimize production processes. It supports a dynamic environment where adaptability to regulatory changes and customer requirements dictates long-term success.

Report Coverage

The research report offers an in-depth analysis based on Material, Insulation Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Cold Insulation Materials Market will see increased adoption driven by stricter energy efficiency regulations worldwide.

- Innovation in sustainable and recyclable insulation materials will accelerate to meet environmental goals.

- Expansion in cold storage infrastructure, especially in emerging economies, will boost market demand.

- Integration of smart insulation solutions with IoT and sensor technologies will gain traction.

- The construction sector will remain a significant growth driver due to rising demand for green buildings.

- Industrial refrigeration applications will expand, driven by growth in the food and pharmaceutical industries.

- Lightweight and flexible insulation materials will become preferred for easier installation and handling.

- Manufacturers will focus on enhancing thermal performance while reducing material thickness.

- Regional markets in Asia-Pacific and Latin America will experience rapid growth due to urbanization and industrialization.

- Collaborations between manufacturers and technology providers will increase to develop advanced insulation products.