Market Overview

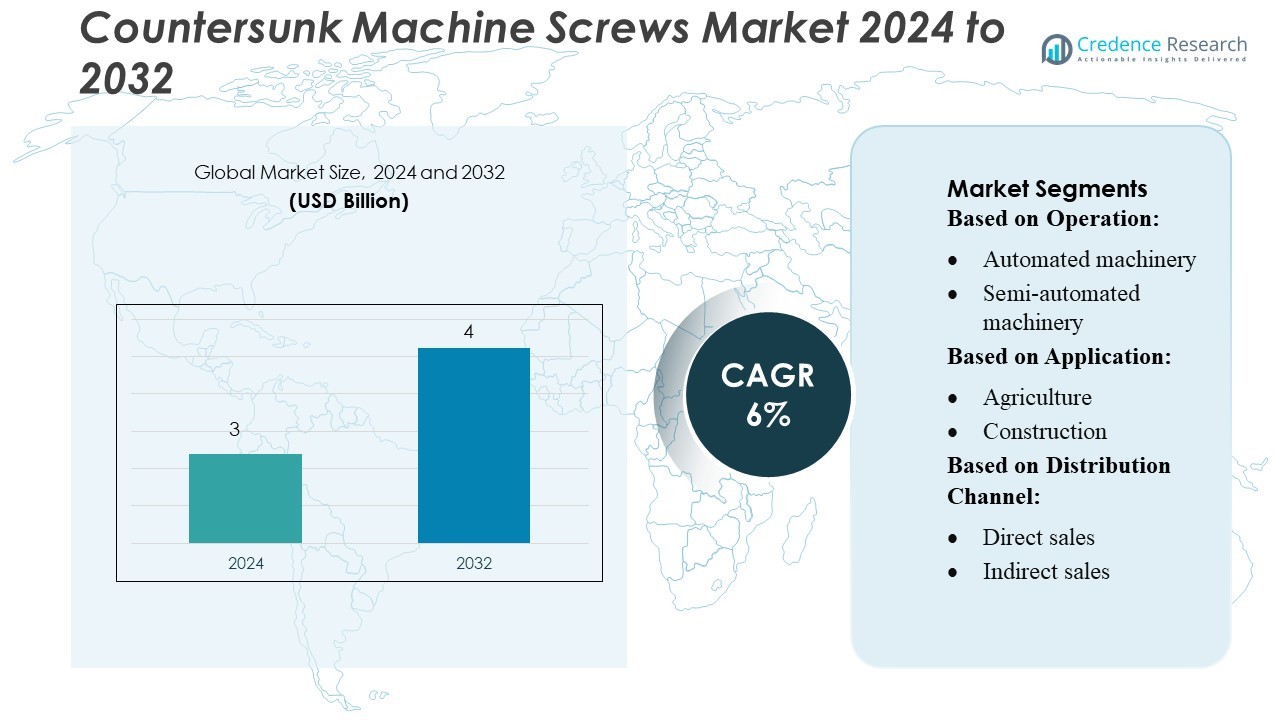

Countersunk Machine Screws Market size was valued USD 3 billion in 2024 and is anticipated to reach USD 4 billion by 2032, at a CAGR of 6% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Countersunk Machine Screws Market Size 2024 |

USD 3 Billion |

| Countersunk Machine Screws Market, CAGR |

6% |

| Countersunk Machine Screws Market Size 2032 |

USD 4 Billion |

The Countersunk Machine Screws Market is shaped by a competitive group of manufacturers that focus on precision engineering, advanced coatings, and high-strength materials to meet industrial performance demands. Key players include Eurotec, GRK Fasteners, SPAX International GmbH & Co. KG, Fischer, Fastenmaster, SFS Group, Rothoblaas, Grip-Rite, Kyocera Senco, and Simpson Strong-Tie, each strengthening their position through product innovation and expanded distribution networks. Asia-Pacific remains the leading regional market, accounting for approximately 40% of global demand, supported by large-scale manufacturing, strong construction activity, and extensive production capacity across China, India, Japan, and South Korea.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Countersunk Machine Screws Market was valued at USD 3 billion in 2024 and is projected to reach USD 4 billion by 2032, growing at a 6% CAGR, supported by rising demand in construction, automotive, and industrial machinery applications.

- Increasing adoption of precision-engineered fasteners and corrosion-resistant coatings drives market expansion, supported by automation in assembly processes and the need for high-strength fastening solutions across sectors.

- The market experiences steady trends toward lightweight designs, advanced alloy development, and enhanced coating technologies, with top players investing in R&D to strengthen product performance.

- Competitive intensity remains high as manufacturers expand distribution networks, optimize production efficiency, and address restraints such as fluctuating raw material prices and supply-chain disruptions.

- Asia-Pacific leads the global market with 40% share, followed by North America and Europe, while the construction segment dominates overall consumption with the largest share due to extensive infrastructure development and industrial manufacturing activity.

Market Segmentation Analysis:

By Operation

The automated machinery segment dominates the countersunk machine screws market with an estimated 42–45% share, driven by rapid adoption of CNC machining systems and fully integrated production lines that require high-precision fastening components. Automated systems demand screws with tighter dimensional tolerances, consistent head geometry, and improved fatigue resistance to support continuous, high-speed operations. Semi-automated machinery remains a stable secondary contributor as mid-scale manufacturers upgrade legacy lines. Meanwhile, manual and robotic machinery segments grow steadily, with robotics benefiting from increasing deployment of articulated arms in electronics and metalworking assembly.

- For instance, GRK Fasteners’ products evaluated under ICC-ES ESR-2442 demonstrate engineered performance suitable for automated assembly, with allowable shear capacities reaching 2,320 lbf and torsional strength verified through standardized ICC testing.

By Application

Construction represents the leading application segment, accounting for approximately 30–32% of total demand, supported by rising global infrastructure activity and the need for durable, flush-mount fasteners in metal frameworks, fittings, and heavy equipment. Packaging and food processing industries also show strong adoption due to regulatory emphasis on hygienic, vibration-resistant fastening. Agriculture and mining rely on countersunk screws for machinery exposed to harsh operating environments, while semiconductor manufacturing drives demand for micro-precision screws with superior corrosion resistance and ultra-fine threading. The “Others” category captures growing usage in DIY tools and specialized industrial assemblies.

- For instance, SPAX International GmbH & Co. KG’s countersunk stainless-steel screws (e.g., the A2 Ø 10 mm T-STAR plus full-thread type) deliver a characteristic tensile strength of 17,000 N (as per their ETA-12/0114 technical approval).

By Distribution Channel

Direct sales lead the market with an estimated 55–58% share, driven by manufacturers’ preference for long-term supply contracts, bulk procurement, and customization capabilities aligned with OEM specifications. Industrial buyers prioritize direct sourcing to ensure traceability, quality assurance, and consistent delivery schedules. Indirect sales continue to expand through distributors and online platforms as small and mid-size enterprises seek flexible order quantities, faster lead times, and broad product availability. Growth in e-commerce marketplaces further accelerates indirect channel penetration, particularly in aftermarket and maintenance applications across construction, machinery repair, and equipment refurbishment.

Key Growth Drivers

- Expanding Use in Precision Assembly Across Manufacturing

Demand for countersunk machine screws continues to rise as manufacturers prioritize precise, flush-mounted fastening solutions to enhance product aesthetics, ergonomics, and structural integrity. Industries such as electronics, automotive, and industrial equipment increasingly adopt these screws to reduce vibration, improve load distribution, and streamline assembly. Their compatibility with automated fastening systems also supports higher production efficiency. Additionally, rapid growth in lightweight metal components and miniaturized assemblies strengthens the need for high-tolerance screws designed for secure fit and improved surface smoothness.

- For instance, Fischer’s UltraCut FBS II 10 × 120 SK concrete screw features a saw-tooth geometry that enables fast cutting into concrete, and its special design supports three embedment depths (65 / 55 / 35 mm) as per its technical datasheet.

- Growth in Construction and Infrastructure Projects

The surge in global construction and infrastructure development drives wide use of countersunk machine screws in metal framing, architectural hardware, HVAC systems, and structural fixtures. Their ability to sit flush with surfaces ensures a cleaner finish and reduces snagging risks in high-traffic environments. Infrastructure modernization, especially in emerging economies, emphasizes durable, corrosion-resistant fasteners that meet strict safety and performance standards. Increased adoption of stainless steel, alloy steel, and coated variants further supports market growth by extending service life in demanding outdoor and industrial conditions.

- For instance, FastenMaster’s FlatLOK structural wood screw (part of its LOK Line) is evaluated per ICC-ES AC233 and its TER-1503-01 report shows it can achieve withdrawal loads exceeding 5,000 lbf in LVL-to-LVL connections.

- Advancements in Materials and Manufacturing Technologies

Innovations in material engineering and precision machining significantly boost the performance and adoption of countersunk machine screws. Manufacturers are producing hardness-enhanced, lightweight, and anti-corrosive variants using advanced alloys and surface treatments, enabling reliable performance in high-load and harsh-environment applications. CNC machining, cold forging, and automated quality inspection systems improve dimensional accuracy and reduce defects, making these screws suitable for aerospace, medical devices, and semiconductor equipment. Improved supply chain integration and customization capabilities also allow faster development of application-specific screw designs.

Key Trends & Opportunities

1. Rising Preference for High-Performance and Specialty Screws

A major trend involves the shift toward specialty countersunk machine screws designed for extreme temperatures, chemical exposure, or high-vibration environments. As equipment complexity grows, industries increasingly demand screws with enhanced mechanical strength, unique head geometries, and tamper-resistant features. This trend creates opportunities for manufacturers to expand premium product lines and integrate advanced testing processes. Demand for micro-sized screws in electronics and precision instruments is also rising, offering a lucrative segment for specialized fastener producers.

- For instance, HECO-TOPIX®-plus A2 countersunk timber screw (HTP-S-CS-VFT) integrates GripFit, MagicClose, and PerfectPitch drive systems and has a variable thread pitch to deliver controlled pull-out forces in facades, with head diameters ranging from 5.9 mm to 11.7 mm per their product specs.

2. Growth of Automated Assembly and Robotics Integration

The expanding adoption of industrial automation and robotics in machining, packaging, and metal fabrication facilities is creating strong opportunities for countersunk machine screws designed for consistent automated feeding and fastening. Manufacturers are focusing on uniform thread profiles, standardized dimensions, and high-speed compatibility to ensure smooth robotic operation. This trend encourages development of high-quality, low-tolerance screws that reduce jamming and improve cycle times. As smart factories accelerate globally, demand for automation-compatible fasteners is expected to grow significantly.

- For instance, Rothoblaas’ VGS EVO structural countersunk screw features a 20 µm multilayer C4 EVO coating and a high-strength steel core (fₙ,k = 1000 N/mm²), and it demonstrated zero corrosion after 1,440 hours in ISO 9227 salt-spray testing, enabling reliable use in automated outdoor assembly.

3. Increasing Use of Sustainable and Recyclable Materials

Sustainability-driven purchasing patterns are creating opportunities for countersunk screw manufacturers to introduce eco-friendly materials and processes. The market is seeing increased interest in recyclable stainless steel, low-energy manufacturing methods, and coatings free of harmful chemicals. Companies adopting circular-economy practices—such as reprocessing scrap metals into fasteners—are gaining competitive advantage. This trend aligns with stricter environmental regulations and growing corporate commitments to reduce carbon footprints across supply chains.

Key Challenges

1. Price Volatility of Metals and Raw Materials

Fluctuating prices of steel, aluminum, and alloying materials pose a significant challenge for countersunk machine screw manufacturers. Sudden increases in raw material costs directly affect production expenses and shrink profit margins, especially for companies operating on high-volume, low-margin models. Supply disruptions caused by geopolitical tensions or trade restrictions further aggravate cost instability. Manufacturers must adopt strategies such as long-term supplier contracts, diversified sourcing, and improved production efficiency to mitigate this challenge.

2. Intense Competition and Market Fragmentation

The market is highly fragmented, with numerous global and regional players competing primarily on price rather than differentiation. This environment puts pressure on manufacturers to continuously innovate while keeping costs competitive. Low-cost producers from emerging economies intensify pricing competition, making product quality, certification compliance, and consistent supply critical differentiators. Small and mid-tier manufacturers may struggle to invest in advanced machinery, automation, and quality systems required to remain competitive in international markets.

Regional Analysis

North America

North America holds an estimated 28–30% share of the global countersunk machine screws market, driven by strong demand from aerospace, defense, automotive, and precision manufacturing sectors. The region benefits from advanced production capabilities, high adoption of CNC machining, and stringent quality standards that favor premium fasteners. The United States dominates regional consumption due to ongoing aircraft modernization and steady growth in industrial automation. Rising investments in EV manufacturing and defense component refurbishment continue to expand screw demand. Robust supply chains and strong OEM–supplier relationships reinforce North America’s position as a key high-value market.

Europe

Europe accounts for roughly 25–27% of the global market, supported by its mature industrial base and strong emphasis on engineering-quality fasteners. Germany, France, and the U.K. lead consumption, primarily due to high production activity in automotive, machinery, rail, and aerospace systems. Strict regulatory frameworks and sustainability initiatives are pushing manufacturers toward corrosion-resistant alloys and high-performance coated screws. The region’s expanding renewable energy, industrial robotics, and precision equipment sectors continue to generate steady demand. Robust export activity and technologically advanced manufacturing standards keep Europe a critical market for premium countersunk screw solutions.

Asia-Pacific

Asia-Pacific leads the global market with an estimated 38–40% share, driven by rapid industrialization, large-scale manufacturing, and expanding construction activities. China, India, Japan, and South Korea remain major contributors, supported by strong electronics, automotive, consumer goods, and heavy machinery production. The availability of cost-effective manufacturing and extensive raw material supply further strengthens regional competitiveness. Growing semiconductor fabrication and increasing automation in packaging and assembly lines continue to accelerate fastener demand. APAC’s strong export base, coupled with increasing adoption of high-precision components, solidifies its dominance in the countersunk machine screws market.

Latin America

Latin America holds an estimated 6–7% share of the global countersunk machine screws market, influenced by expanding construction, agricultural machinery, mining equipment, and general manufacturing activity. Brazil and Mexico stand out as primary demand centers due to their sizeable industrial bases and growing investments in automotive and heavy engineering. The region is witnessing steady uptake of standardized and corrosion-resistant fasteners driven by harsh operating environments. Although reliance on imports remains high, the gradual growth of local machining capabilities and infrastructure modernization projects supports moderate but consistent market expansion across Latin America.

Middle East & Africa

The Middle East & Africa region represents approximately 4–5% of global demand, largely driven by construction, oil & gas equipment manufacturing, and industrial repair activities. Gulf countries contribute significantly due to ongoing infrastructure development and increased investment in industrial diversification initiatives. Demand for durable, corrosion-resistant countersunk screws remains particularly strong in high-temperature and offshore environments. Africa’s market is gradually expanding with rising manufacturing activities in South Africa, Egypt, and Nigeria. Although the region relies heavily on imported fasteners, increasing industrial clusters and construction megaprojects are expected to support steady long-term growth.

Market Segmentations:

By Operation:

- Automated machinery

- Semi-automated machinery

By Application:

By Distribution Channel:

- Direct sales

- Indirect sales

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Countersunk Machine Screws Market features a diverse mix of global and specialized manufacturers, including Eurotec, GRK Fasteners, SPAX International GmbH & Co. KG, Fischer, Fastenmaster, SFS Group, Rothoblaas, Grip-Rite, Kyocera Senco, and Simpson Strong-Tie. The Countersunk Machine Screws Market is defined by continuous innovation, strong quality standards, and expanding global manufacturing capabilities. Companies increasingly focus on developing high-performance screws with improved torque resistance, precise threading, and advanced corrosion-resistant coatings to meet rising demand from construction, automotive, electronics, and aerospace sectors. Competition is further shaped by the growing adoption of automated assembly lines, pushing manufacturers to produce screws with consistent dimensional accuracy and enhanced drive designs. Market participants also strengthen their position through wider distribution networks, improved supply-chain resilience, and increased investment in R&D aimed at optimizing materials, surface treatments, and sustainability-focused production processes.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In January 2025, Bossard Group acquired the Ferdinand Gross Group, a German fastening technology distributor with a presence in Germany, Hungary, and Poland. The acquisition expands Bossard’s market presence in Germany and Eastern Europe and allows the combined entity to offer a more comprehensive range of solutions to its customers in these regions.

- In December 2024, Bulten and ZJK Vietnam Precision Components Co., Ltd,The new joint venture plans to rent production facilities, which means limited investment costs and risk-taking for Bulten. Bulten’s ownership signed a letter of intent to establish operations in Vietnam through a joint venture.

- In November 2024, Sandvik Mining and Rock Solutions launched the MD/MDX Peg Bolt, a new ground support solution for underground mining that improves safety by providing a visual indicator of correct installation. A plastic disc protrudes through the bolt’s ID tab once the correct torque is applied, making it easy to see the bolt is installed properly, even after subsequent blasting cycles. This feature offers enhanced safety and peace of mind for miners.

- In April 2024, Norelem announced the launch of a leading global provider of standard parts and components for the manufacturing industry, norelem, has announced the launch of a new flexible. Made from aluminium, the clamping bolts offer a flexible clamping system to provide secure and powerful clamping for workpieces with regular and irregular outer contours.

Report Coverage

The research report offers an in-depth analysis based on Operation, Application, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will experience steady demand growth driven by expanding construction, automotive, and industrial manufacturing activities.

- Manufacturers will increasingly adopt advanced alloys and coatings to enhance corrosion resistance and long-term durability.

- Automation in assembly processes will accelerate the need for high-precision screws with consistent dimensional accuracy.

- The shift toward lightweight components will boost the development of optimized screw designs for improved strength-to-weight performance.

- Rising adoption of electric vehicles will support higher consumption of specialized fastening solutions.

- Global supply chains will become more localized to improve resilience and reduce lead times.

- Sustainability initiatives will encourage the use of eco-friendly materials and energy-efficient production methods.

- Demand for custom and application-specific screw geometries will increase as industries seek performance optimization.

- Digital quality control and smart manufacturing technologies will enhance productivity and reduce defect rates.

- Growing investments in infrastructure and urban development projects will reinforce long-term market expansion.