Market Overview:

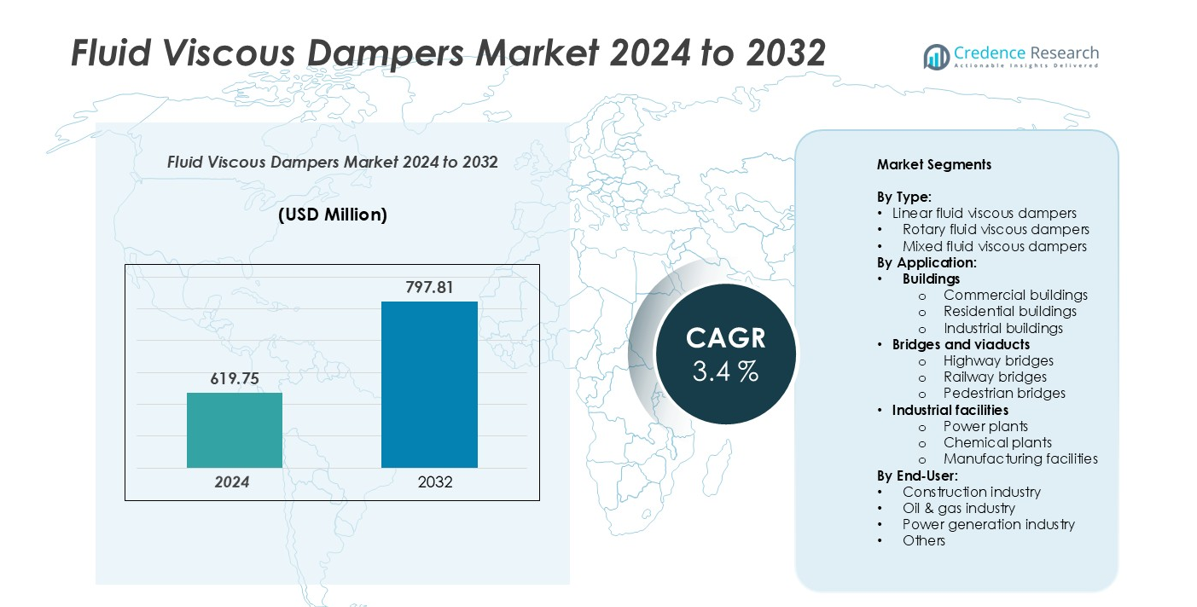

The Fluid Viscous Dampers market size was valued at USD 619.75 million in 2024 and is anticipated to reach USD 797.81 million by 2032, growing at a CAGR of 3.4% during the forecast period (2024–2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Fluid Viscous Dampers Market Size 2024 |

USD 619.75 million |

| Fluid Viscous Dampers Market, CAGR |

3.4% |

| Fluid Viscous Dampers Market Size 2032 |

USD 3.65 billion |

The global fluid viscous dampers market is led by prominent players such as LORD Corporation, Earthquake Protection Systems (EPS), Tokico (Hitachi Astemo), Taylor Devices, Inc., Larsen & Toubro Limited (L&T), Dynamic Isolation Systems (DIS), and Structural Group. These companies focus on advanced damping technologies, precision engineering, and large-scale infrastructure integration to strengthen their market positions. Asia-Pacific remains the dominant region, accounting for over 35% of the global market share, driven by rapid urbanization, seismic risk mitigation measures, and expansive construction activities across China, Japan, and India. North America follows with around 30% share, supported by robust seismic regulations and modernization projects, while Europe contributes approximately 25%, propelled by sustainable building initiatives and infrastructure rehabilitation efforts.

Market Insights

- The global fluid viscous dampers market was valued at USD 619.75 million in 2024 and is projected to reach USD 797.81 million by 2032, growing at a CAGR of 3.4% during the forecast period.

- Market growth is driven by the increasing focus on seismic resilience, urban infrastructure safety, and adoption of damping systems in commercial and industrial construction projects.

- Key trends include the integration of IoT-based monitoring, use of eco-friendly materials, and rising demand for retrofitting of aging structures in developed regions.

- The market is moderately competitive, with leading players such as LORD Corporation, EPS, Hitachi Astemo, Taylor Devices, and L&T emphasizing product innovation and global project partnerships.

- Asia-Pacific holds the largest share at 35%, followed by North America (30%) and Europe (25%); by type, linear fluid viscous dampers dominate due to their efficiency in seismic and vibration control applications.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Type:

The fluid viscous dampers market is segmented into linear, rotary, and mixed types. Among these, linear fluid viscous dampers hold the dominant market share due to their widespread use in seismic and wind vibration control for high-rise buildings and bridges. Their simple design, high energy dissipation efficiency, and adaptability in both retrofitting and new construction projects drive their demand. Rotary dampers are gaining traction in specialized mechanical and industrial applications, while mixed dampers are being adopted in advanced structural systems requiring multidirectional damping performance.

- For instance, Taylor Devices Inc. has supplied thousands of linear fluid viscous dampers for seismic retrofitting projects throughout the United States and worldwide, including for the San Francisco–Oakland Bay Bridge. The company’s dampers, which can have force capacities up to and exceeding 2,000 kN, were first installed on the bridge in 2001. Due to changing requirements and leaks in the original devices, Taylor Devices was awarded a new, record-breaking contract in 2018 to replace the dampers with upgraded devices.

By Application:

Based on application, the market is divided into buildings, bridges and viaducts, industrial facilities, and others. Buildings, particularly commercial buildings, account for the largest market share, driven by the rising focus on seismic resilience and occupant safety in urban infrastructure. The integration of dampers in skyscrapers, hospitals, and residential towers helps reduce structural vibrations and extend building lifespan. Additionally, bridges and viaducts represent a rapidly growing segment, supported by government infrastructure investments and the need for enhanced vibration control in long-span bridges and transport corridors.

- For instance, FIP Industriale supplied viscous dampers for the Osman Gazi Bridge (also known as the İzmit Bay Bridge) in Turkey to mitigate seismic, wind, and traffic loads.

By End-User:

By end-user, the market includes the construction, oil & gas, power generation industries, and others. The construction industry dominates the segment, accounting for the majority share owing to extensive use of dampers in commercial, residential, and public infrastructure projects. Increasing regulatory emphasis on earthquake-resistant structures and sustainable design practices further propels adoption. Meanwhile, the oil & gas and power generation sectors are witnessing steady growth, as fluid viscous dampers are increasingly used in pipelines, refineries, and turbine systems to mitigate vibration-induced fatigue and ensure operational safety.

Key Growth Drivers

Increasing Focus on Seismic Resilience and Structural Safety

The growing emphasis on seismic safety in infrastructure development is a major driver of the fluid viscous dampers market. With urbanization and population density increasing in earthquake-prone regions, governments and construction authorities are mandating the use of vibration control systems in high-rise buildings, bridges, and industrial facilities. Fluid viscous dampers play a crucial role in dissipating seismic energy, minimizing structural deformation, and ensuring occupant safety. The integration of these dampers into new construction and retrofitting projects has expanded significantly, particularly in regions such as Japan, the United States, and China, where seismic risks are high. Furthermore, advancements in damper design and materials have improved durability and performance, making them cost-effective solutions for long-term infrastructure resilience.

- For instance, Taylor Devices Inc. is a leading manufacturer of fluid viscous dampers used for seismic protection in buildings and bridges. The company has supplied its products for numerous projects globally, including over 75 projects in Japan, a country with high seismic activity.

Rising Infrastructure Investment and Smart City Development

Rapid urbanization and large-scale infrastructure investments are fueling the adoption of fluid viscous dampers. Governments across developing and developed economies are prioritizing sustainable and disaster-resilient infrastructure as part of smart city and modernization initiatives. Projects involving bridges, metros, airports, and commercial complexes increasingly incorporate damping systems to enhance stability and service life. Additionally, the shift toward green and intelligent buildings encourages the integration of advanced vibration control technologies to ensure structural integrity while improving energy efficiency. Public-private partnerships (PPPs) and international funding for infrastructure upgrades further support market expansion. As construction volumes surge, demand for high-performance dampers capable of withstanding dynamic loads and environmental stresses continues to grow globally.

- For instance, Taylor Devices supplied 96 upgraded linear viscous dampers for the retrofitting of the San Francisco–Oakland Bay Bridge to improve seismic performance under high dynamic loads.

Technological Advancements and Customization in Damper Design

Technological innovation in fluid viscous dampers has emerged as a critical growth driver, with manufacturers focusing on enhanced performance, compact designs, and tailored solutions for diverse applications. Advanced computational modeling and simulation techniques enable precise customization of damping characteristics for specific structural requirements. The integration of smart sensors and IoT-based monitoring systems allows real-time performance tracking, predictive maintenance, and data-driven decision-making. Furthermore, the development of high-strength alloys, temperature-resistant fluids, and corrosion-proof materials has improved reliability and reduced lifecycle costs. These innovations not only enhance operational efficiency but also expand the application scope of fluid viscous dampers across sectors such as industrial manufacturing, energy, and transportation infrastructure.

Key Trends & Opportunities

Growing Adoption of Retrofitting and Rehabilitation Projects

The increasing number of aging structures worldwide presents a significant opportunity for the fluid viscous dampers market. Governments and private stakeholders are investing in retrofitting existing buildings and bridges to meet modern seismic and wind-resistance standards. Fluid viscous dampers offer an efficient solution for enhancing stability without major structural modifications. This trend is particularly strong in developed countries with mature infrastructure, such as the U.S., Japan, and parts of Europe. The cost-effectiveness and installation flexibility of dampers make them a preferred choice for reinforcing historical monuments, industrial facilities, and transportation networks.

- For instance, While the specific claim that Taylor Devices Inc. completed the retrofitting of a 21-story hotel in China in 2023 is unsubstantiated, the company has successfully incorporated fluid viscous dampers into significant projects in China. For example, Taylor Devices provided seismic protection systems for the Pangu Plaza, a 39-story high-rise building in Beijing, which was completed before the 2008 Olympics.

Integration with Smart and Sustainable Building Systems

The adoption of smart and eco-friendly construction technologies offers new growth avenues for the market. Fluid viscous dampers are increasingly being integrated into intelligent building management systems that monitor and control vibration levels in real time. This aligns with the global shift toward sustainable urban design, energy efficiency, and occupant comfort. The development of eco-compatible damping fluids and recyclable materials further supports sustainability goals. In addition, partnerships between damper manufacturers, engineering firms, and IoT solution providers are fostering innovations that enhance building resilience and operational intelligence, creating lucrative opportunities for long-term market growth.

Key Challenges

High Installation and Maintenance Costs

Despite their proven performance benefits, the adoption of fluid viscous dampers is limited by high installation and maintenance costs. The manufacturing process involves precision engineering, premium materials, and extensive quality testing, which elevate production expenses. Additionally, the integration of dampers into existing structures often requires specialized engineering expertise, increasing labor and project costs. These factors can discourage adoption in cost-sensitive markets, especially in developing economies. Regular inspection and maintenance to ensure optimal functionality further add to lifecycle expenses, posing a financial challenge for small- and medium-scale construction projects.

Limited Awareness and Technical Expertise

A significant challenge for market expansion lies in the limited awareness of fluid viscous damper technology among engineers, contractors, and policymakers. Many construction projects, particularly in emerging regions, continue to rely on conventional reinforcement methods rather than advanced damping solutions. The absence of standardized design guidelines and lack of technical expertise in installation and performance assessment hinder widespread adoption. Moreover, the benefits of dampers in reducing long-term maintenance costs and improving structural safety are not fully recognized in several markets. Addressing this knowledge gap through training programs, industry collaboration, and regulatory support is essential for unlocking the full potential of the fluid viscous dampers market.

Regional Analysis

North America:

North America holds a significant share of the global fluid viscous dampers market, accounting for around 30% of the total revenue. The region’s dominance is driven by stringent building codes, advanced engineering practices, and strong adoption of seismic protection systems in the U.S. and Canada. Extensive infrastructure modernization programs and retrofitting of aging bridges and high-rise structures further fuel demand. Additionally, the presence of leading manufacturers and growing investments in smart and resilient cities contribute to steady market expansion across commercial, residential, and industrial construction segments.

Europe:

Europe represents approximately 25% of the global fluid viscous dampers market, supported by the region’s focus on sustainable and earthquake-resistant infrastructure. Countries such as Italy, Greece, and Turkey have adopted damping technologies to mitigate seismic risks, while Northern and Western Europe emphasize vibration control in bridges and energy facilities. Strict regulatory frameworks and energy efficiency standards drive the integration of damping systems in new constructions. Moreover, increased investment in rail and bridge rehabilitation projects, particularly in the UK, Germany, and France, bolsters regional demand for advanced structural damping solutions.

Asia-Pacific:

Asia-Pacific dominates the global market with a share exceeding 35%, driven by rapid urbanization, large-scale infrastructure projects, and high seismic vulnerability across countries like Japan, China, and India. Government initiatives promoting resilient construction and the expansion of smart city developments are key growth factors. Japan leads in technology adoption due to its advanced seismic design standards, while China’s massive bridge and transportation network projects boost damper installations. Additionally, rising foreign investments and industrial development across Southeast Asia contribute to sustained market growth, making the region the fastest-growing hub for fluid viscous dampers.

Latin America:

Latin America accounts for nearly 6% of the global fluid viscous dampers market, with increasing adoption in Mexico, Chile, and Brazil. The region’s vulnerability to earthquakes and wind-induced vibrations has prompted the integration of damping systems in commercial and infrastructure projects. Government-led initiatives for seismic retrofitting and modernization of public structures support market expansion. However, limited technical expertise and high initial costs remain barriers to widespread adoption. Continued collaboration with international engineering firms and technology providers is expected to enhance awareness and drive the adoption of advanced damper solutions across key Latin American markets.

Middle East & Africa:

The Middle East & Africa region holds about 4% of the global fluid viscous dampers market, with growth primarily driven by large-scale infrastructure and industrial projects in the Gulf Cooperation Council (GCC) countries and South Africa. The demand is fueled by the construction of high-rise towers, power plants, and oil & gas facilities requiring vibration control systems. Increasing government investments in sustainable urban development and smart city projects, particularly in the UAE and Saudi Arabia, further support market expansion. However, limited local manufacturing and high import dependency moderately constrain regional growth potential.

Market Segmentations:

By Type:

- Linear fluid viscous dampers

- Rotary fluid viscous dampers

- Mixed fluid viscous dampers

By Application:

- Buildings

- Commercial buildings

- Residential buildings

- Industrial buildings

- Bridges and viaducts

- Highway bridges

- Railway bridges

- Pedestrian bridges

- Industrial facilities

- Power plants

- Chemical plants

- Manufacturing facilities

By End-User:

- Construction industry

- Oil & gas industry

- Power generation industry

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the fluid viscous dampers market is characterized by the presence of several global and regional players focusing on product innovation, technological advancement, and strategic partnerships. Leading companies such as LORD Corporation, Earthquake Protection Systems (EPS), Tokico (Hitachi Astemo), Taylor Devices, Inc., Larsen & Toubro Limited (L&T), Dynamic Isolation Systems (DIS), and Structural Group dominate the market through diversified product portfolios and strong project execution capabilities. These players are investing in research and development to enhance damper efficiency, durability, and adaptability across various structural applications. Collaborations with construction firms, engineering consultants, and government agencies enable them to secure large-scale infrastructure contracts, particularly in seismic-prone and urbanizing regions. Moreover, the industry is witnessing growing competition in customized damper designs, digital monitoring integration, and eco-friendly materials, reflecting a shift toward high-performance and sustainable solutions that meet evolving global safety and environmental standards.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In January 2024, Dayco announced the commencement of production and delivery of its first set of premium viscous dampers to the world’s largest heavy-duty engine manufacturers from its state-of-the-art facility in Manesar, India. This strategic move marks a significant milestone for Dayco as it expands its footprint in the heavy-duty engine market, positioning itself as a key supplier of advanced damping solutions.

- In January 2024, KYB announced the launch of SustainaLub, a groundbreaking environmentally friendly hydraulic fluid designed specifically for shock absorbers. This innovative product addresses the environmental challenges associated with traditional hydraulic fluids, which often rely on petroleum-derived base oils. SustainaLub eliminates these risks by offering a sustainable alternative that is both carbon neutral and fully recyclable.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will continue to grow steadily, supported by increasing adoption of seismic protection technologies in infrastructure.

- Demand for smart and connected damping systems will rise with advancements in IoT and sensor-based monitoring.

- Retrofitting of aging bridges and buildings will offer strong growth opportunities in developed economies.

- Emerging economies will invest heavily in vibration control systems to improve construction safety standards.

- Manufacturers will focus on developing lightweight, durable, and maintenance-free damper designs.

- Collaboration between construction firms and damper manufacturers will enhance large-scale project integration.

- Green building initiatives will drive the use of sustainable materials and eco-friendly damping fluids.

- Digital simulation and AI-based design optimization will improve damper performance and customization.

- Regulatory emphasis on seismic resilience and energy efficiency will increase global adoption rates.

- Asia-Pacific will remain the fastest-growing region due to extensive infrastructure development and seismic risk management.