Market Overview

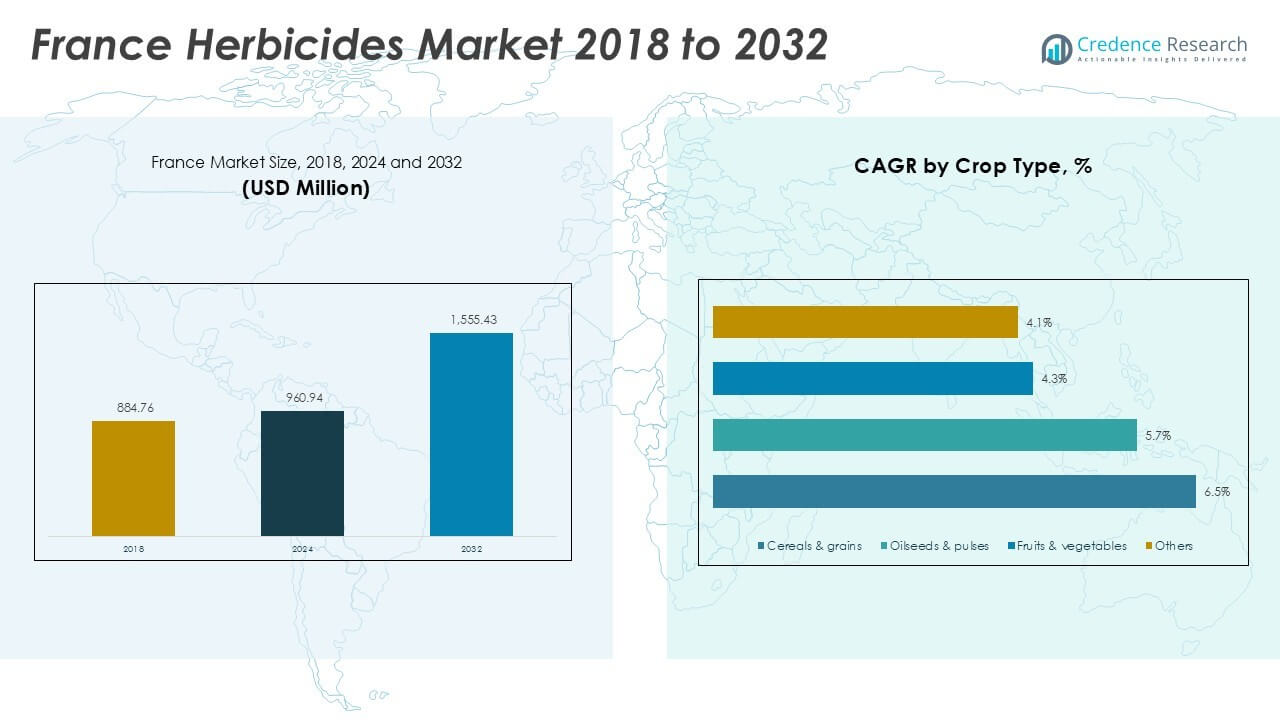

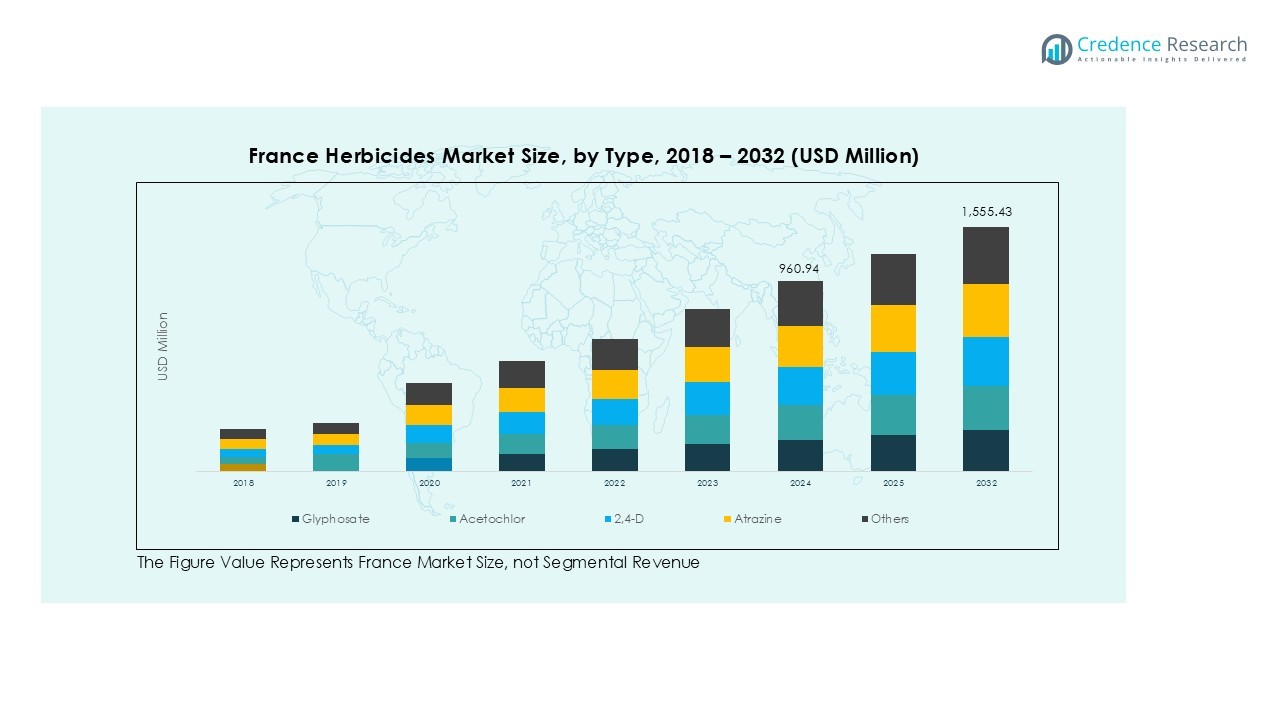

France Herbicides market size was valued at USD 884.76 million in 2018 and reached USD 960.94 million in 2024. The market is projected to grow further to USD 1,555.43 million by 2032, at a CAGR of 6.20% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| France Herbicides Market Size 2024 |

USD 960.94 Million |

| France Herbicides Market, CAGR |

6.20% |

| France Herbicides Market Size 2032 |

USD 1,555.43 Million |

The France herbicides market is led by ADAMA Agricultural Solutions France Limited, BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd, Syngenta Group, FMC Agricultural Solutions, UPL Limited, Belchim Crop Protection, and Gowan. These companies offer extensive herbicide portfolios covering glyphosate, 2,4-D, and bio-based solutions, addressing the needs of cereal, grain, and high-value crop farmers. North France dominates the market with nearly 30% share, supported by large-scale wheat and barley production and advanced mechanization. West France follows with around 22%, driven by diversified crop cultivation and rising adoption of sustainable weed control practices aligned with EU regulations.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- France herbicides market was valued at USD 960.94 million in 2024 and is projected to reach USD 1,555.43 million by 2032, growing at a CAGR of 6.20%.

- Rising demand for higher agricultural productivity and effective weed control is driving adoption, supported by government initiatives promoting sustainable farming practices.

- Glyphosate dominates the market with over 35% share, while foliar application leads with 45% share, driven by rapid action and efficient weed management in cereals and grains.

- The market is moderately consolidated, with key players including ADAMA, BASF, Bayer, Corteva, Syngenta, and UPL focusing on innovation, bio-based herbicides, and partnerships with cooperatives to expand reach.

- North France holds the largest regional share at nearly 30%, followed by West France with 22%, reflecting strong cereal cultivation and adoption of precision farming; Central and South France show steady growth with increasing fruit and vegetable production.

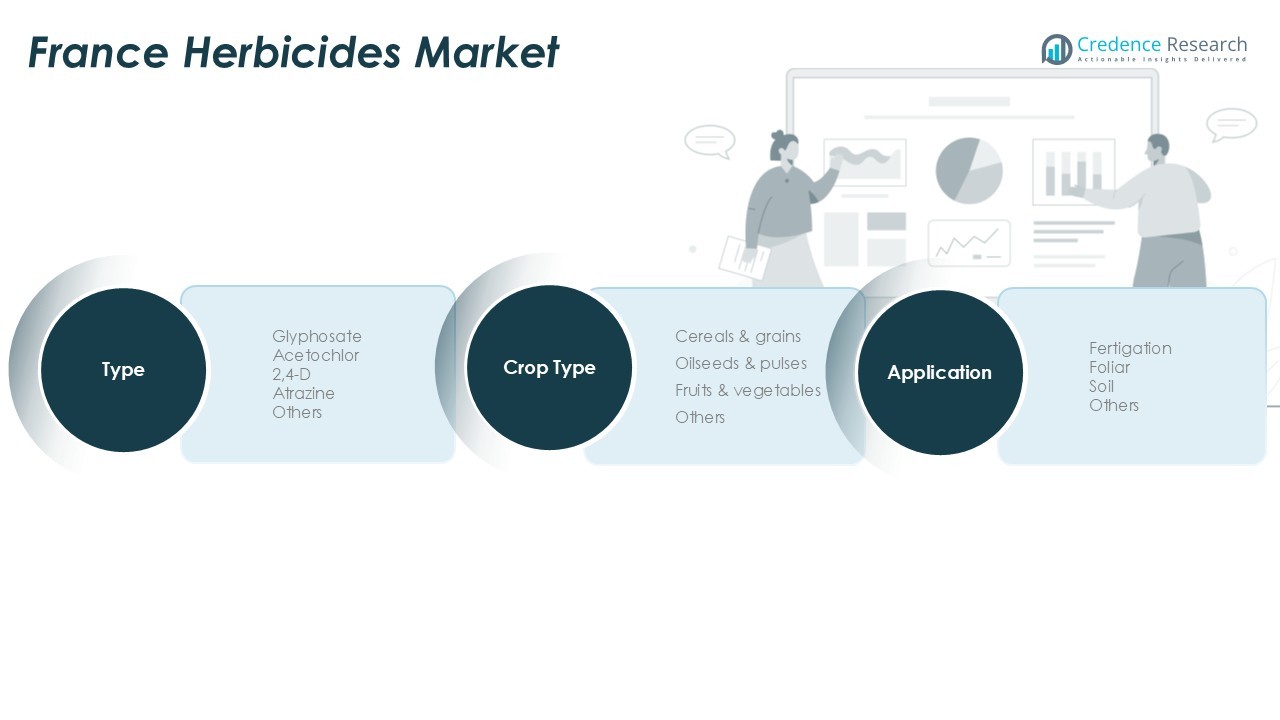

Market Segmentation Analysis:

By Type

Glyphosate dominated the France herbicides market in 2024, accounting for over 35% of total share. Its wide adoption stems from its effectiveness against a broad range of weeds and compatibility with multiple crop types. Farmers prefer glyphosate for its cost-efficiency and ease of application, especially in large-scale cereal production. Acetochlor and 2,4-D follow, driven by their use in selective weed control. Rising concerns about weed resistance and the need for higher crop yields are boosting demand for advanced formulations and integrated weed management solutions across the country.

- For instance, in 2024, France cultivated approximately 4.2 million hectares of wheat, a smaller area than normal due to excessive rainfall. While glyphosate-based programs were historically used for pre-sowing and stubble management, their application was heavily restricted in 2024.

By Application

Foliar application held the largest share, exceeding 45% in 2024, as it provides rapid action and higher efficacy. French farmers increasingly adopt foliar spraying to control weed growth during critical crop growth stages, ensuring better yields. Fertigation is gaining popularity due to precision farming techniques and efficient resource use. Soil applications remain significant for pre-emergence weed control. Growing mechanization and adoption of advanced sprayer technology are supporting foliar applications, making them a preferred choice in high-value crops and large-scale farming systems.

- For example, Arvalis research trials in France demonstrated up to 10% higher wheat yields with optimized foliar herbicide programs compared to untreated plots.

By Crop Type

Cereals & grains represented the leading crop segment, contributing more than 40% of market share in 2024. Wheat, barley, and corn cultivation drive herbicide consumption due to their extensive planting area in France. Rising demand for food security and government programs supporting sustainable crop production have strengthened herbicide use in this segment. Fruits & vegetables are also witnessing growing adoption, supported by the need to maintain high-quality produce. Increased focus on maximizing yield per hectare and reducing manual labor costs continue to fuel herbicide demand in major crop categories.

Key Growth Drivers

Expansion of Cereal and Grain Production

Poland’s strong cereal and grain sector drives herbicide demand, with wheat, maize, and barley production increasing annually. Rising acreage and higher yield targets require effective weed control to minimize competition for nutrients and water. Government support for mechanization and modern farming practices further fuels adoption, making cereals and grains the dominant crop segment for herbicide consumption.

- For instance, Poland harvested about 12.6 million metric tons of wheat in marketing year 2024/25 from 2.5 million hectares, reinforcing the need for glyphosate and selective herbicides.

Adoption of Precision and Modern Farming Practices

The shift toward precision farming and integrated pest management is accelerating herbicide usage in Poland. Farmers are increasingly using glyphosate and systemic herbicides for pre- and post-emergence weed control. Digital sprayer technologies and GPS-enabled machinery optimize coverage and minimize chemical wastage. These practices improve efficiency, lower input costs, and help farmers comply with EU sustainability regulations, driving consistent growth for advanced herbicide formulations.

- For example, research in Polish barley fields showed yields exceeding 7 tonnes per hectare under conservation rotation with targeted weed control.

Government Support and Food Security Initiatives

Poland’s focus on food security and agricultural productivity supports herbicide demand across major crop-growing regions. State-backed subsidies and EU Common Agricultural Policy (CAP) funds encourage adoption of improved weed management solutions. Investments in research, extension services, and farmer training programs promote responsible and efficient herbicide use. This government support also strengthens rural mechanization initiatives and boosts adoption of herbicide-tolerant crop varieties, ensuring higher yields. The drive to meet domestic consumption and maintain export competitiveness sustains steady herbicide market growth throughout the forecast period.

Key Trends & Opportunities

Growth of Bio-Based and Low-Residue Herbicides

Poland is witnessing a shift toward bio-based herbicides and low-residue formulations in response to EU regulations and consumer preference for safer agrochemicals. Demand from organic farming and high-value crops is rising, creating opportunities for suppliers of microbial, enzyme, and plant-extract-based herbicides. Companies investing in eco-friendly formulations and residue-free certifications are positioned to benefit from this trend as sustainability becomes a major differentiator in purchasing decisions.

- For instance, Borregaard’s Exilva bio-adjuvant has been tested in European cornfields to improve glyphosate rainfastness and reduce chemical load.

Integration of Digital Agriculture Solutions

Digital agriculture platforms are enabling farmers to improve herbicide efficiency through data-driven decision-making. Satellite imagery, AI-powered weed detection, and IoT-enabled sprayers allow variable rate application, reducing overuse and environmental impact. This precision approach lowers costs, improves yield outcomes, and ensures regulatory compliance. Growing availability of government and EU funding for precision agriculture adoption further supports this opportunity for herbicide manufacturers and agri-tech providers.

- For example, smart spraying systems such as Bosch-BASF’s ONE SMART SPRAY technology can identify weeds in milliseconds and activate nozzles only where needed.

Key Challenges

Regulatory Pressure and Active Ingredient Restrictions

Stringent EU regulations on chemical herbicide residues and periodic reviews of active ingredients create uncertainty for manufacturers. Several commonly used products, including glyphosate, face reauthorization debates that could lead to stricter usage guidelines or potential bans. This regulatory pressure forces companies to invest in reformulations and alternative solutions, increasing development costs. Compliance with maximum residue limits (MRLs) and environmental safety requirements remains a significant challenge for suppliers aiming to maintain market access while balancing farmer affordability and agronomic effectiveness.

Rising Weed Resistance and Evolving Pest Pressure

Herbicide-resistant weed populations are becoming a major challenge in Poland, threatening long-term productivity. Over-reliance on glyphosate and selective herbicides has led to resistant biotypes in maize, wheat, and oilseed rape fields. This drives demand for integrated weed management programs and crop rotation practices, but also raises input costs for farmers. Companies must innovate with new modes of action and combination products to address resistance challenges. Failure to manage resistant weeds effectively can result in yield losses and higher economic pressure on growers.

Regional Analysis

North France

North France held the largest share of the France herbicides market, contributing nearly 30% in 2024. The region’s dominance is supported by extensive wheat and barley cultivation, which drives high herbicide demand. Farmers in this area focus on glyphosate and foliar applications to maintain weed-free fields and ensure consistent yields. Government-backed programs promoting sustainable agriculture and precision farming have further increased herbicide adoption. Large farm sizes and advanced mechanization enable efficient herbicide spraying, making North France a key contributor to overall market growth and a hub for innovation in modern crop protection practices.

West France

West France accounted for around 22% of the herbicides market share in 2024. The region benefits from diverse crop cultivation, including cereals, maize, and forage crops, which require consistent weed control. Farmers in West France increasingly adopt integrated weed management solutions to address herbicide resistance challenges. Foliar and fertigation applications are widely used due to the prevalence of large farms and efficient irrigation infrastructure. Rising awareness of environmentally friendly herbicide formulations and strict regional regulations on chemical use are driving demand for sustainable and low-toxicity products, ensuring compliance with EU green agricultural policies.

Central France

Central France captured nearly 20% of the herbicides market share in 2024. The region’s focus on cereals and oilseeds drives steady herbicide consumption, with pre-emergence soil applications gaining popularity for effective weed control. Farmers adopt precision agriculture tools to optimize herbicide dosage and reduce operational costs. Crop diversification, supported by government initiatives, is leading to a wider adoption of selective herbicides. The presence of research institutions and demonstration farms in Central France is encouraging farmers to use advanced formulations that minimize residue levels, aligning with food safety and environmental sustainability requirements in the French agricultural sector.

South France

South France represented about 15% of the France herbicides market in 2024. The region’s warm climate supports high production of fruits, vegetables, and vineyards, driving significant demand for foliar-applied herbicides. Farmers focus on targeted applications to protect high-value crops and maintain product quality. Water scarcity in some areas is boosting interest in precision herbicide use and fertigation techniques that save resources. Sustainable farming initiatives and a shift toward bio-based herbicides are gaining traction as growers aim to meet EU sustainability standards and cater to the rising demand for organic and residue-free produce from both domestic and export markets.

Eastern France

Eastern France accounted for nearly 13% of the market share in 2024, making it the smallest but steadily growing region. The area focuses on mixed farming systems, including cereals, oilseeds, and livestock feed crops, which drive herbicide demand. Farmers adopt soil applications for pre-emergence control and invest in integrated weed management practices to improve efficiency. Increasing awareness of soil health and government incentives for reducing chemical overuse are influencing a gradual transition toward advanced and eco-friendly herbicide formulations. Modern equipment adoption and collaboration with cooperatives are helping growers optimize input costs while maintaining high crop productivity.

Market Segmentations:

By Type

- Glyphosate

- Acetochlor

- 2,4-D

- Atrazine

- Others

By Application

- Fertigation

- Foliar

- Soil

- Others

By Crop Type

- Cereals & Grains

- Oilseeds & Pulses

- Fruits & Vegetables

- Others

By Geography

- North France

- West France

- Central France

- South France

- Eastern France

Competitive Landscape

The France herbicides market is moderately consolidated, with key players such as ADAMA Agricultural Solutions France Limited, BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd, Syngenta Group, FMC Agricultural Solutions, UPL Limited, Belchim Crop Protection, and Gowan holding significant market positions. These companies compete through extensive product portfolios, including glyphosate-based, selective, and bio-based herbicides tailored for cereals, grains, and high-value crops. Strategic activities such as R&D investment, product innovation, and sustainable solutions are common as companies respond to EU regulations and rising demand for eco-friendly formulations. Partnerships with cooperatives and digital agriculture platforms strengthen their presence among French farmers. Recent trends include the development of low-residue herbicides and integrated weed management solutions to address herbicide resistance. Market players focus on expanding distribution networks and enhancing after-sales services to capture greater market share while aligning with France’s sustainability goals and precision farming practices.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- ADAMA Agricultural Solutions France Limited

- BASF SE

- Bayer AG

- Corteva Agriscience

- Nufarm Ltd

- Syngenta Group

- FMC Agricultural Solutions

- UPL Limited

- Belchim Crop Protection

- Gowan

Recent Developments

- In December 2023, ADAMA introduced its most advanced cross-spectrum herbicide called Kampai for the grain business. The new product provides the broadest application window for broadleaf and narrow-leaf weed control for cereal crops.

- In September 2023, American Water Chemicals (AWC) announced the launch of its European division, named Amaya Solutions Europe, SL. This strategic move marks a significant milestone in AWC’s global expansion efforts, aimed at enhancing its presence in the European market.

- In July 2023, ADAMA introduced new products, Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions, for imidazolinone-tolerant legumes like lentils, peas, and soybeans.

- In March 2023, BASF announced the launch of a novel corn herbicide named Surtain, which is set to be available for use in the United States in 2024. This innovative herbicide features solid encapsulation technology, marking it as the first of its kind in the industry.

- In January 2023, Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

Report Coverage

The research report offers an in-depth analysis based on Type, Application, Crop Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for herbicides will grow due to rising food security concerns and higher crop yields.

- Adoption of bio-based and low-toxicity herbicides will expand with stricter EU regulations.

- Digital farming and precision application technologies will improve herbicide efficiency and reduce waste.

- Development of herbicide-resistant weed management solutions will gain priority among manufacturers.

- Research in integrated weed management will encourage combined chemical and mechanical solutions.

- Foliar application will continue leading due to quick action and compatibility with modern sprayers.

- Glyphosate alternatives will gain traction as regulatory scrutiny over residues increases.

- Collaborations between suppliers and cooperatives will strengthen distribution and farmer training programs.

- Sustainable farming practices will drive demand for eco-friendly formulations and controlled dosage systems.

- Regional growth will remain strongest in North France, with West and Central regions catching up steadily.