| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| France Industrial Solvents Market Size 2024 |

USD 1,279.55 Million |

| France Industrial Solvents Market, CAGR |

6.98% |

| France Industrial Solvents Market Size 2032 |

USD 2,194.96 Million |

Market Overview

France Industrial Solvents Market size was valued at USD 1,279.55 million in 2024 and is anticipated to reach USD 2,194.96 million by 2032, at a CAGR of 6.98% during the forecast period (2024-2032).

The France industrial solvents market is witnessing robust growth driven by increasing demand from key industries such as automotive, pharmaceuticals, and construction. The rising emphasis on sustainable and bio-based solvents, fueled by stringent environmental regulations and consumer preference for eco-friendly products, is reshaping the market landscape. Technological advancements in solvent formulations are enhancing performance while reducing environmental impact, further boosting adoption across diverse sectors. Additionally, the growing trend of industrial expansion and modernization in France is propelling the need for high-performance solvents in manufacturing and processing activities. The shift towards green chemistry practices and the development of innovative, low-VOC (volatile organic compound) solvents are creating new opportunities for market players. As industries prioritize efficiency, safety, and environmental compliance, the demand for specialized solvents tailored to specific applications is expected to rise steadily, reinforcing the market’s upward trajectory throughout the forecast period.

The France industrial solvents market is characterized by a diverse geographical spread, with key regions such as Northern, Southern, Eastern, and Western France each contributing to the demand in distinct ways. Northern France leads in industrial production, particularly in automotive and pharmaceutical sectors, while Southern France benefits from a strong presence of the aerospace and chemical industries. Eastern France focuses on heavy manufacturing, and Western France is emerging with growth in renewable energy and food processing. Major global players dominate the market, including BASF SE, Shell Chemicals, and Solvay S.A., which are leveraging their advanced R&D capabilities and extensive product portfolios to meet the evolving needs of the industry. Other significant companies like Arkema S.A., INEOS Group, and Evonik Industries AG are also key contributors, focusing on sustainable and eco-friendly solvents. These companies are well-positioned to drive innovation and growth in the French industrial solvents market through technological advancements and strategic partnerships.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The France industrial solvents market was valued at USD 1,279.55 million in 2024 and is expected to reach USD 2,194.96 million by 2032, growing at a CAGR of 6.98% during the forecast period (2024-2032).

- The global industrial solvents market was valued at USD 34,660.50 million in 2024 and is expected to reach USD 60,647.79 million by 2032, growing at a CAGR of 7.24% during the forecast period (2024-2032).

- Increasing demand for eco-friendly, bio-based solvents due to stringent environmental regulations is a key driver.

- Technological advancements, particularly in automation and solvent recovery, are fueling market growth.

- The market is shifting towards low-VOC and sustainable solutions, creating new opportunities for bio-based solvents.

- Regulatory pressures, including restrictions on hazardous solvents, are limiting growth potential for certain chemicals.

- Northern France dominates the market, driven by industrial production hubs, followed by Southern and Eastern France with strong sectors in aerospace and pharmaceuticals.

- Major players like BASF SE, Shell Chemicals, and Solvay S.A. lead the market, focusing on innovation and eco-friendly solutions to maintain a competitive edge.

Report Scope

This report segments the France Industrial Solvents Market as follows:

Market Drivers

Growing Demand from Key End-Use Industries

The industrial solvents market in France is experiencing significant growth, primarily fueled by increasing demand from major end-use industries such as automotive, pharmaceuticals, and construction. Solvents play a critical role in manufacturing processes, including coatings, adhesives, pharmaceuticals, and cleaning agents. For instance, the French automotive sector has seen a rise in demand for specialized solvents used in electric vehicle battery production and lightweight material coatings. Similarly, the pharmaceutical industry’s focus on drug formulation and production efficiency is escalating solvent consumption. Construction activities across France, spurred by infrastructure modernization and urban development, further contribute to the robust demand for high-performance industrial solvents.

Shift Towards Eco-Friendly and Bio-Based Solvents

Environmental sustainability is becoming a decisive factor influencing the industrial solvents market in France. Stringent European Union regulations regarding emissions and chemical usage have pushed manufacturers to develop and adopt eco-friendly, bio-based solvents. For instance, the French government has introduced incentives for industries transitioning to bio-based solvents, particularly in the paints and coatings sector. Industries are increasingly replacing traditional petroleum-based solvents with alternatives derived from renewable resources, such as bio-alcohols, esters, and glycols. This shift not only supports regulatory compliance but also meets growing consumer expectations for greener and safer products. Companies investing in the research and development of low-VOC (volatile organic compound) and biodegradable solvents are gaining a competitive advantage, creating a significant driver for the overall market expansion.

Technological Innovations in Solvent Formulations

Advancements in chemical engineering and materials science are leading to the development of next-generation solvent solutions. Innovations aimed at improving solvent performance — such as higher solvency power, faster drying times, and lower toxicity — are reshaping market dynamics in France. Manufacturers are focusing on creating customized solvent blends that offer enhanced efficiency for specific industrial processes while minimizing environmental and health risks. Additionally, the emergence of solvent recycling and recovery technologies is contributing to the industry’s growth by offering cost-effective and sustainable solutions to solvent usage. These technological strides are encouraging industries to adopt advanced solvents, thereby driving consistent market growth.

Rising Industrialization and Economic Recovery

France’s ongoing industrialization, coupled with its economic recovery efforts following global disruptions, is positively impacting the industrial solvents market. Increased investments in manufacturing facilities, along with government initiatives supporting innovation and industrial competitiveness, are leading to higher solvent consumption across various sectors. The resurgence of small and medium enterprises (SMEs) and expansion of export-oriented industries are further stimulating the demand for quality industrial solvents. As businesses emphasize operational efficiency, product quality, and sustainability, the adoption of specialized solvents tailored to meet specific industry requirements is accelerating. This industrial momentum is expected to continue bolstering market growth throughout the forecast period.

Market Trends

Strong Shift Toward Green and Sustainable Solvents

The France industrial solvents market is undergoing a major transformation, with a notable shift toward green, bio-based, and sustainable solvents. Environmental regulations under the European Union’s REACH legislation and the European Green Deal are compelling industries to move away from traditional petrochemical-based solvents toward eco-friendly alternatives. For instance, France Chimie has reported a significant increase in the adoption of bio-based solvents across multiple industries, driven by regulatory incentives and sustainability commitments. Bio-based solvents derived from renewable sources such as corn, sugarcane, and soybeans are gaining traction due to their low toxicity, biodegradability, and reduced carbon footprint. In particular, sectors like paints and coatings, adhesives, and pharmaceuticals are aggressively incorporating bio-based solvents to meet sustainability goals without sacrificing product performance. Companies operating in France are increasing their investments in R&D to develop innovative, plant-based solvent technologies, ensuring compliance with evolving regulatory frameworks and responding to the growing demand for environmentally conscious solutions.

Technological Advancements Driving Product Innovation

Technological innovation is another key trend shaping the industrial solvents market in France. Advances in chemical engineering, material science, and process optimization are enabling the development of solvents that deliver superior performance while minimizing health and environmental risks. New solvent formulations with enhanced properties such as faster evaporation rates, higher solvency power, and reduced VOC emissions are finding increased application across diverse industries. Furthermore, solvent recycling and recovery technologies are gaining momentum, as manufacturers seek cost-effective and sustainable production methods. Companies are utilizing digital tools like AI and IoT to monitor solvent performance in real-time and optimize production processes, thereby improving efficiency and reducing waste. The move toward high-purity, specialty solvents designed for industries such as electronics, aerospace, and pharmaceuticals is also contributing significantly to market growth, reflecting the increasing demand for advanced manufacturing solutions.

Regulatory Pressures Reshaping Market Dynamics

The stringent regulatory environment in Europe continues to play a decisive role in influencing market trends within the French industrial solvents sector. Recent legislation restricting the use of certain hazardous chemicals, such as the classification of DMF (N,N-dimethylformamide) as a substance of very high concern (SVHC), is pushing industries to seek safer solvent alternatives. For instance, the OECD has highlighted France’s proactive approach in aligning industrial policies with environmental regulations to ensure compliance and competitiveness. Additionally, regulatory initiatives promoting circular economy practices and reduced emissions are accelerating the adoption of low-VOC and non-toxic solvent formulations. French companies are proactively reformulating products and re-engineering production processes to align with these regulations, often working closely with regulatory bodies and research institutions. These developments are not only ensuring public health and environmental safety but also strengthening the competitiveness of domestic industries in the global market, as compliance with high regulatory standards becomes a key differentiator.

Rising Industrial Activities and Market Expansion

The overall industrial expansion in France is positively impacting the demand for industrial solvents. Growth in sectors such as automotive manufacturing, pharmaceuticals, construction, and electronics is driving an increase in solvent consumption for applications like coatings, degreasing, formulations, and chemical synthesis. France’s push toward becoming a leader in electric vehicles and renewable energy technologies is creating new opportunities for solvent manufacturers, particularly for battery production and lightweight material fabrication. Furthermore, infrastructure modernization projects and rising investment in clean technologies are contributing to solvent demand across the construction and industrial maintenance sectors. The focus on operational efficiency, product quality, and environmental compliance is encouraging industries to adopt more specialized and high-performance solvent products. These factors are expected to maintain the upward momentum of the industrial solvents market in France throughout the forecast period.

Market Challenges Analysis

Stringent Environmental Regulations and Compliance Costs

One of the primary challenges facing the France industrial solvents market is the increasingly stringent environmental regulations imposed by both national and European Union authorities. Regulations such as REACH, CLP, and the European Green Deal demand significant reductions in volatile organic compound (VOC) emissions and limit the use of hazardous chemical substances. For instance, France Chimie has reported that compliance costs for chemical manufacturers have risen due to stricter enforcement of REACH regulations, requiring extensive documentation and testing. Manufacturers are required to invest heavily in research, development, and reformulation efforts to create compliant products, which often leads to higher production costs. Additionally, businesses face growing administrative and certification burdens to ensure adherence to evolving standards. Smaller and mid-sized companies, in particular, are struggling to meet these requirements due to limited resources, which restricts their ability to innovate or compete with larger, better-funded players. These regulatory pressures are not only raising operational costs but also slowing down product launches and market penetration, ultimately posing a serious constraint on market growth.

Volatility in Raw Material Prices and Supply Chain Disruptions

Another significant challenge impacting the industrial solvents market in France is the volatility of raw material prices coupled with ongoing supply chain disruptions. Most industrial solvents are derived from petrochemical feedstocks, and fluctuations in crude oil prices directly affect the cost structure of solvent manufacturing. The global supply chain, already strained by geopolitical tensions, energy crises, and logistical bottlenecks, further exacerbates the instability of raw material availability. French manufacturers are facing increased input costs and unpredictable supply timelines, which impact their ability to maintain steady production and fulfill orders. Additionally, the shift toward bio-based solvents, while environmentally beneficial, introduces new complexities, such as dependency on agricultural yields and competition with food resources. These factors collectively introduce uncertainties in pricing strategies and profit margins, forcing companies to either absorb the additional costs or pass them on to consumers, thereby affecting market competitiveness and growth potential.

Market Opportunities

The France industrial solvents market presents significant opportunities driven by the ongoing transition toward sustainable and eco-friendly solutions. With stringent environmental regulations pushing industries to reduce emissions and adopt greener practices, there is a growing demand for bio-based and low-VOC solvents. Manufacturers who invest in the development of innovative, sustainable solvent formulations stand to gain a competitive edge. The increasing emphasis on circular economy initiatives further supports opportunities for solvent recovery, recycling, and reuse technologies, opening new avenues for growth. Additionally, as industries such as automotive, construction, and pharmaceuticals expand their green initiatives, the need for high-performance, environmentally compliant solvents will rise, offering solvent producers the chance to align product offerings with evolving customer expectations and regulatory requirements.

Moreover, France’s strong focus on technological innovation, particularly in sectors like electric vehicles, renewable energy, and advanced manufacturing, creates new demand for specialized and high-purity solvents. Applications in emerging industries such as battery production, electronics manufacturing, and biopharmaceuticals require advanced solvent solutions with specific performance characteristics, presenting significant market potential. Growth in industrial modernization and infrastructure development, supported by government investment and recovery plans, further stimulates the need for industrial solvents in paints, coatings, adhesives, and cleaning agents. Companies that strategically expand their product portfolios, focus on R&D, and leverage sustainable practices are well-positioned to capitalize on these emerging opportunities, ensuring long-term growth and competitive advantage in the evolving French industrial landscape.

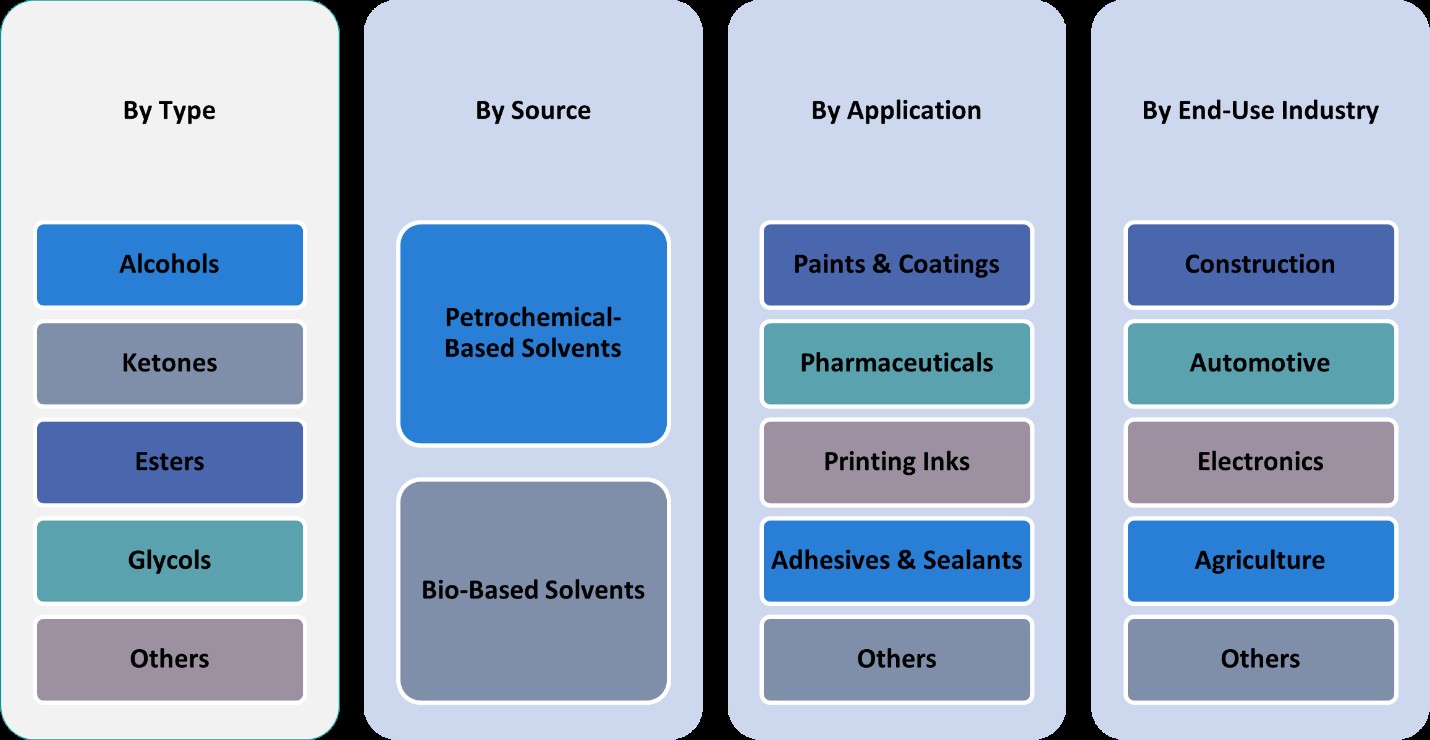

Market Segmentation Analysis:

By Type:

The France industrial solvents market, when segmented by type, shows diverse usage patterns across various industries. Alcohols represent a significant portion of the market, driven by their wide applicability in cleaning agents, paints, coatings, and pharmaceuticals. Their favorable solvency properties and relatively lower toxicity make them a preferred choice for eco-conscious manufacturers. Ketones, particularly acetone and methyl ethyl ketone (MEK), also capture a substantial share due to their strong solvency power and rapid evaporation rates, making them ideal for coatings, adhesives, and printing inks. Esters are gaining popularity as environmentally friendly solvents, supported by the push for low-VOC solutions across industrial applications. Glycols, known for their high boiling points and use in antifreeze formulations and chemical intermediates, are witnessing steady demand. The “Others” category, which includes hydrocarbons and chlorinated solvents, remains essential for heavy-duty industrial uses but faces regulatory challenges, pushing innovation toward safer alternatives. The trend toward bio-based and specialty solvents is further influencing product developments across all solvent types.

By Application:

Based on application, paints and coatings constitute the largest segment in the France industrial solvents market, fueled by strong demand from the construction and automotive sectors. Solvents are critical in adjusting viscosity and facilitating smooth application and drying of paints. Pharmaceuticals also represent a growing segment, where solvents are indispensable in drug formulation, extraction, and purification processes, particularly with the expansion of biopharmaceutical production. The printing inks sector benefits from solvent use in maintaining print quality and drying times, especially with the growth of the packaging industry. Adhesives and sealants rely on solvents for formulation stability and performance in bonding applications across construction and manufacturing. The “Others” category, covering sectors like agrochemicals and cleaning products, provides additional avenues for solvent utilization. The growing emphasis on sustainable and high-performance solutions is prompting innovation in all application areas, with manufacturers increasingly focusing on safer, efficient, and environmentally compliant solvent systems to meet industry-specific demands.

Segments:

Based on Type:

- Alcohols

- Ketones

- Esters

- Glycols

- Others

Based on Application:

- Paints & Coatings

- Pharmaceuticals

- Printing Inks

- Adhesives & Sealants

- Others

Based on End- Use:

- Construction

- Automotive

- Electronics

- Agriculture

- Others

Based on Source:

- Petrochemical-Based Solvents

- Bio-Based Solvents

Based on the Geography:

- Northern France

- Southern France

- Eastern France

- Western France

Regional Analysis

Northern France

Northern France accounted for the largest share of the France industrial solvents market, representing approximately 35% of the total market value. The region’s dominance can be attributed to its strong industrial base, including the presence of major automotive, pharmaceutical, and chemical manufacturing hubs. Cities like Lille and Rouen are key centers for production and research, driving consistent demand for industrial solvents in paints, coatings, adhesives, and pharmaceutical applications. Additionally, Northern France benefits from its strategic location close to major European trade routes, supporting solvent imports and exports. The robust infrastructure and ongoing investments in green technologies also reinforce the region’s leadership position in the market. Manufacturers are increasingly focusing on sustainable solutions to align with both domestic and EU regulations, creating additional opportunities for eco-friendly solvent products.

Southern France

Southern France holds the second-largest share, capturing around 28% of the France industrial solvents market. The region’s solvent demand is largely driven by its vibrant pharmaceutical, chemical, and aerospace sectors, particularly in cities like Marseille and Toulouse. Southern France’s warmer climate and agricultural base also foster demand for solvents used in agrochemical formulations and food processing applications. Moreover, the region is actively investing in renewable energy and biotechnology, creating new avenues for specialty and bio-based solvents. Growth in the construction and real estate sectors is further boosting the demand for solvents in paints, coatings, and sealants. Southern France’s commitment to innovation and sustainability initiatives positions it as a key region for future growth, encouraging manufacturers to expand their product portfolios to meet the evolving needs of diverse industries.

Eastern France

Eastern France contributes approximately 20% of the industrial solvents market share. This region is characterized by a strong presence of heavy industries, including manufacturing, machinery, and automotive sectors, particularly in areas like Strasbourg and Metz. Eastern France also has well-established chemical production facilities, supporting steady solvent consumption. Cross-border trade with Germany, Switzerland, and Luxembourg provides additional momentum for industrial activities and, consequently, solvent usage. However, environmental regulations and the push for greener alternatives are reshaping the demand landscape, leading to increased interest in low-VOC and biodegradable solvents. Investments in research, especially in chemical engineering and green manufacturing processes, are likely to enhance Eastern France’s contribution to the national market over the forecast period.

Western France

Western France accounts for the remaining 17% of the France industrial solvents market share. The region, which includes key cities like Nantes and Rennes, has a growing industrial sector focused on food processing, maritime, and renewable energy industries. Demand for industrial solvents in Western France is rising steadily, particularly in adhesives, coatings, and printing inks used in packaging industries. The region is also witnessing a surge in eco-conscious manufacturing practices, driving the adoption of bio-based and environmentally safe solvents. While Western France currently holds a smaller share compared to other regions, it presents strong growth potential due to its expanding industrial base and strategic government initiatives promoting innovation and sustainability. Manufacturers targeting the western region are increasingly focusing on customized, high-performance solvent solutions tailored to emerging industry needs.

Key Player Analysis

- BASF SE

- Shell Chemicals

- Solvay S.A.

- Arkema S.A.

- INEOS Group

- Evonik Industries AG

- Clariant AG

- Synthomer plc

- AkzoNobel N.V.

- Perstorp Holding AB

Competitive Analysis

The France industrial solvents market is highly competitive, with several leading global players shaping the landscape. BASF SE, Shell Chemicals, Solvay S.A., Arkema S.A., INEOS Group, Evonik Industries AG, Clariant AG, Synthomer plc, AkzoNobel N.V., and Perstorp Holding AB are some of the key players that dominate the market. Companies are focusing on the development of eco-friendly and bio-based solvents to meet the increasing demand for environmentally responsible products, driven by stringent regulations in the European Union. These players are also investing heavily in research and development to create solvents that meet high-performance standards while minimizing environmental impact. The focus on low-VOC (volatile organic compounds) and non-toxic solvents has further intensified competition, as businesses look to offer solutions that align with sustainability goals. Additionally, market players are actively forming strategic partnerships and alliances to expand their product portfolios and enhance market reach. Innovations in solvent recovery and recycling technologies are also key differentiators, allowing companies to provide cost-effective solutions while reducing waste. Competition in the market is further influenced by the ability to adapt to changing regulatory landscapes and consumer preferences for greener, safer products. Companies that can balance operational efficiency with sustainability initiatives are well-positioned to lead the market as demand for high-quality, eco-conscious solvents continues to grow.

Recent Developments

- In April 2025, Eastman announced off-list price increases for several EOD (Ethylene Oxide Derivatives) solvents, including Eastman™ DB Solvent, effective April 7, 2025, reflecting ongoing cost and market pressures.

- In March 2025, BASF reported generating approximately €11 billion in 2024 sales from products launched in the past five years, driven by R&D focused on sustainability, biodegradable materials, and digital transformation. The company filed 1,159 new patents in 2024, with 45% targeting sustainability. R&D investment in 2024 was €2.1 billion, with a similar budget planned for 2025.

- In March and April 2025, Shell is restructuring its global chemicals business to boost profitability and reduce capital spending by 2030. This includes exploring strategic partnerships in the U.S., potentially closing some European assets, and selling existing assets like the Singapore refinery and chemical complex. The company aims to streamline operations, focus on core businesses, and improve returns for shareholders.

- In March 2025, BASF is expanding its production capacity for aminic antioxidants at its Puebla, Mexico site, targeting the growing demand for long-life lubricants. The project is set for completion in 2026.

- In March 2025, ExxonMobil announced a $100 million upgrade to its Baton Rouge, Louisiana plant to produce ultra-high-purity (99.999%) isopropyl alcohol (IPA) for the semiconductor industry by 2027.

- In March 2024, Dow announced plans to invest in new ethylene derivatives capacity-including carbonate solvents-on the U.S. Gulf Coast. This investment, supported by the U.S. Department of Energy, aims to supply carbonate solvents for lithium-ion batteries, supporting the domestic EV and energy storage market. The facility will capture over 90% of CO₂ from ethylene oxide production, aligning with sustainability goals.

Market Concentration & Characteristics

The France industrial solvents market exhibits a moderate level of market concentration, with a mix of global and regional players operating across various segments. While large multinational corporations dominate the market due to their extensive product portfolios, strong R&D capabilities, and global reach, smaller and mid-sized companies are also carving out niches with specialized and eco-friendly solutions. The market is characterized by intense competition, driven by the need for innovation in solvent formulations that meet increasingly stringent environmental regulations. As sustainability becomes a key driver, companies are focusing on bio-based and low-VOC solvents, positioning themselves as environmentally responsible players. This shift toward greener solutions is encouraging innovation in both solvent recovery and recycling technologies. Furthermore, partnerships and collaborations between key players and research institutions are prevalent, facilitating the development of high-performance and sustainable products. The market’s dynamic nature underscores the growing importance of adapting to changing regulatory environments and evolving customer preferences.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Type, Application, End-Use, Source and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The demand for bio-based and sustainable solvents will continue to rise as industries focus on reducing their environmental impact.

- Increasing regulatory pressure in Europe will drive further innovation in low-VOC and non-toxic solvent solutions.

- Technological advancements in solvent recovery and recycling will play a crucial role in improving cost-efficiency and sustainability.

- The pharmaceutical and electronics sectors will remain significant drivers of demand for high-purity, specialty solvents.

- The automotive industry’s shift toward electric vehicles will increase the need for advanced solvents in battery production and lightweight materials.

- The construction industry’s growth, particularly in green building projects, will lead to higher demand for eco-friendly solvents in paints, coatings, and sealants.

- Companies will focus on expanding their product portfolios with eco-friendly solvents to meet consumer and regulatory demands.

- Partnerships and collaborations with research institutions will foster the development of innovative solvent formulations and technologies.

- Increased focus on circular economy practices will encourage solvent manufacturers to invest in recovery and reuse systems.

- The market will witness greater consolidation, as larger companies acquire smaller players to expand their sustainable product offerings.