| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Incinerators Market Size 2024 |

USD 26,171.15 million |

| Incinerators Market, CAGR |

7.15% |

| Incinerators Market Size 2032 |

USD 47,309.30 million |

Market Overview

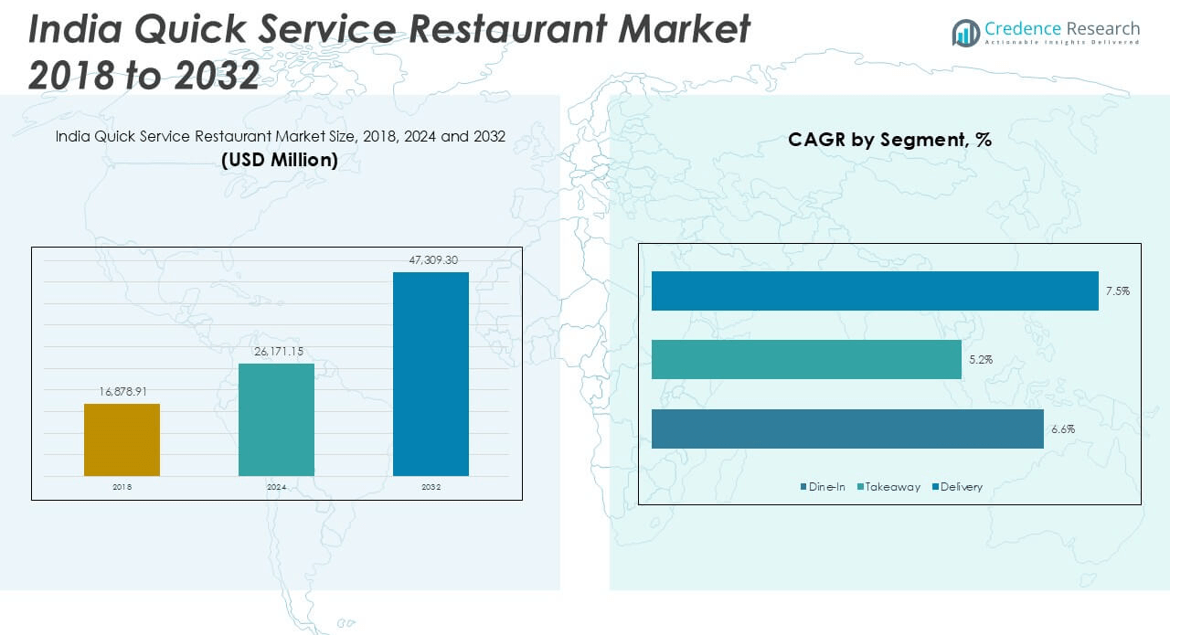

India Quick Service Restaurant market size was valued at USD 16,878.91 million in 2018, increased to USD 26,171.15 million in 2024, and is anticipated to reach USD 47,309.30 million by 2032, at a CAGR of 7.15% during the forecast period.

The India Quick Service Restaurant (QSR) market is dominated by key players such as Domino’s Pizza, McDonald’s, KFC, Pizza Hut, Haldiram’s, Nirula’s, and Popeyes. These brands maintain a strong presence through expansive franchise networks, localized menus, and robust digital delivery models. Domino’s leads in market penetration, while McDonald’s and KFC continue to expand aggressively in urban and semi-urban areas. Among domestic brands, Haldiram’s and Nirula’s capitalize on regional preferences and brand loyalty. Geographically, North India holds the largest share of the market at 32.5%, driven by high urban density, evolving consumer preferences, and a strong retail infrastructure that supports dine-in and delivery formats.

Market Insights

- The India Quick Service Restaurant (QSR) market was valued at USD 26,171.15 million in 2024 and is projected to reach USD 47,309.30 million by 2032, growing at a CAGR of 7.15% during the forecast period.

- Growth is driven by rising urbanization, busy lifestyles, and the increasing preference for convenience foods among millennials and working professionals, particularly in metropolitan and Tier 1 cities.

- Delivery-based QSR services dominate with a 45% share, supported by the rapid expansion of online food platforms like Zomato and Swiggy and increasing smartphone penetration.

- North India leads regionally with 32.5% of the market, followed by South India (27.4%), West India (24.1%), and East India (16%), fueled by infrastructure, disposable income, and food consumption patterns.

- Challenges include high operational costs, intense price competition, and supply chain inefficiencies in Tier 2 and Tier 3 cities, limiting scalability for smaller or new market entrants.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

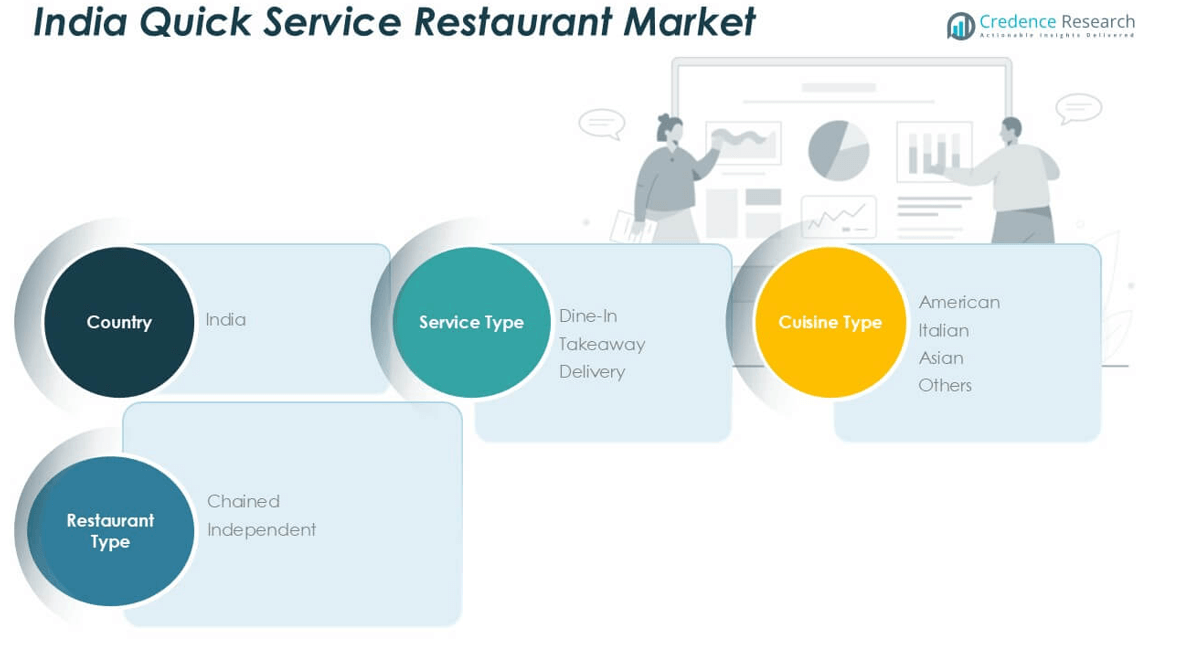

By Service Type:

In the India Quick Service Restaurant (QSR) market, the Delivery segment dominated in 2024, accounting for approximately 45% of the market share. The rise of food aggregator platforms like Swiggy and Zomato, coupled with increasing urbanization and busy lifestyles, has significantly boosted the demand for food delivery. Additionally, post-pandemic consumer preferences for contactless and home-based dining continue to drive this segment. Growing smartphone penetration and digital payment options have further streamlined the ordering process, encouraging a shift away from traditional dine-in services.

- For instance, Zomato completed over 612 million orders in FY2023, while Swiggy reported over 1.5 million active delivery partners, reflecting the operational scale and impact of delivery models on the QSR ecosystem.

By Cuisine Type

Among cuisine types, Asian cuisine held the largest share in 2024, contributing to around 38% of the market. Indian consumers show strong preferences for regional and familiar flavors, which fuels the popularity of Asian offerings, especially Indian-Chinese and North Indian fast foods. This segment benefits from affordability, widespread acceptance, and adaptability to local tastes. While American and Italian cuisines maintain a growing presence through brands like McDonald’s and Domino’s, Asian cuisine leads due to its deeper cultural integration and ease of customization across different regions.

- For instance, Haldiram’s, a major player in Indian fast food, operates more than 150 outlets across India and serves over 400,000 customers daily, primarily through Asian cuisine formats including North Indian thalis, chaats, and Indo-Chinese combinations.

By Restaurant Type

The Chained restaurant segment emerged as the leading category in 2024, capturing over 60% of the market share. Strong brand recall, standardized menus, and quality assurance have positioned chained QSRs as the preferred choice for consumers seeking convenience and consistency. National and international chains continue expanding into Tier 2 and Tier 3 cities, leveraging franchise models and robust marketing strategies. Additionally, their ability to invest in technology, loyalty programs, and delivery infrastructure enhances customer engagement and operational efficiency, solidifying their dominance over independent outlets.

Market Overview

Rising Urbanization and Changing Lifestyles

Rapid urbanization, coupled with shifting consumer lifestyles, is significantly boosting the QSR market in India. With growing work pressure and limited cooking time, urban consumers increasingly prefer convenient and quick meal options. This behavioral shift, especially among millennials and working professionals, is driving traffic towards QSR chains. The demand for on-the-go and ready-to-eat meals continues to increase, particularly in metropolitan and Tier 1 cities, creating a robust growth environment for both domestic and international QSR brands.

- For instance, McDonald’s India (West and South) reported over 11 million app downloads and 600,000 monthly active users, highlighting how urban tech-savvy consumers are engaging with fast food through digital convenience.

Digital Ordering and Delivery Ecosystem Expansion

The proliferation of online food delivery platforms such as Zomato, Swiggy, and Uber Eats has transformed the accessibility and reach of QSR outlets. Tech-enabled convenience, real-time tracking, contactless payment systems, and promotional offers are attracting a large consumer base. The pandemic further accelerated digital ordering habits, making online delivery a core channel for QSR revenue. QSR brands that adapt to digital trends and invest in app-based ordering, loyalty programs, and last-mile logistics are positioned for long-term growth.

- For instance, Domino’s India processed over 77 million online orders in FY2023, with digital sales contributing 75% to its total revenue, reflecting a sharp pivot toward app-driven customer engagement and delivery efficiency.

Aggressive Franchise Expansion by Leading Brands

National and international QSR brands are aggressively expanding through franchise models, entering Tier 2 and Tier 3 cities where the market remains relatively untapped. This strategy lowers operational risks and enables rapid scalability. Brands like McDonald’s, Domino’s, and KFC have successfully localized their menus to cater to Indian tastes, aiding market penetration. This growth strategy not only expands physical presence but also enhances brand recognition and loyalty, thereby driving consistent revenue streams and market share.

Key Trends & Opportunities

Growth in Health-Conscious and Specialty Menus

As consumer awareness of nutrition and health increases, QSR brands are introducing healthier menu options, including salads, plant-based proteins, and low-calorie alternatives. There is rising demand for gluten-free, vegan, and organic food offerings, particularly among younger consumers and fitness-focused urban populations. This trend presents a clear opportunity for QSR chains to diversify their menus and attract new customer segments, thereby enhancing customer retention and promoting brand differentiation in a competitive space.

- For instance, Rebel Foods introduced over 30 plant-based SKUs across brands like Faasos and EatSure, and partnered with GoodDot to scale meat alternatives to over 500 cloud kitchens across India.

Integration of Technology for Operational Efficiency

QSR operators are leveraging technology to streamline operations, reduce wait times, and improve customer service. The use of AI-based analytics for inventory management, digital kiosks for self-ordering, and cloud kitchens for delivery-only services is increasing. These innovations help optimize costs and expand customer touchpoints without the burden of heavy infrastructure investment. Technology-driven innovation provides QSR chains with a competitive edge and supports scalable growth, especially in high-demand urban centers.

- For instance, Jubilant FoodWorks, the master franchisee for Domino’s in India, implemented Smart Ordering Assistants and AI-driven demand forecasting across 1,800+ outlets, reducing delivery time to under 22 minutes in top metro areas.

Key Challenges

Rising Operational and Real Estate Costs

High rental prices in prime urban areas and rising input costs for raw materials significantly strain profit margins. Operating a physical QSR outlet requires considerable investment in real estate, staff, and supply chain logistics. Many smaller or independent QSR operators find it difficult to maintain profitability in such a cost-intensive environment. These financial pressures could limit market entry and expansion, particularly for emerging or regional players lacking the capital scale of larger chains.

Intense Market Competition and Price Sensitivity

The India QSR market is highly competitive, with numerous domestic and international players vying for consumer attention. Price sensitivity among Indian consumers further intensifies competition, compelling brands to offer frequent discounts and promotional deals, which can erode margins. Maintaining quality while keeping prices attractive is a continuous challenge. To stay relevant, brands must differentiate through customer experience, innovation, and value-added offerings while avoiding a race to the bottom on pricing.

Supply Chain and Infrastructure Constraints in Tier 2/3 Cities

While expansion into smaller cities offers growth potential, it also presents logistical challenges. Poor infrastructure, lack of skilled labor, and limited access to reliable cold chains or ingredient suppliers can affect service quality and operational efficiency. Establishing a consistent and scalable supply chain in these regions remains a hurdle for QSR operators. Without proper infrastructure support, brands may face difficulties in replicating the success seen in metropolitan markets.

Regional Analysis

North India

North India accounted for the largest share in the India Quick Service Restaurant market in 2024, contributing 32.5% to the overall revenue. The region’s dominance is driven by urban centers like Delhi NCR, Chandigarh, and Jaipur, where high population density and a fast-paced lifestyle boost QSR demand. The widespread presence of malls, high-street retail zones, and food courts fosters dine-in and takeaway services. Consumer preferences for branded and hygienic food options, coupled with growing adoption of food delivery apps, are driving consistent growth. Increasing disposable incomes and organized retail expansion further support regional market penetration.

South India

In 2024, South India held a 27.4% share of the India Quick Service Restaurant market. Metropolitan cities such as Bengaluru, Hyderabad, and Chennai have emerged as strongholds for both international QSR brands and local chains. A digitally savvy population and high smartphone penetration have led to widespread usage of delivery platforms. The region also benefits from a large working professional base and student population, both of which prefer convenient, affordable food options. Robust infrastructure, expanding food courts, and rising brand consciousness continue to enhance market potential, making South India a key growth engine in the QSR segment

West India

West India captured 24.1% of the India Quick Service Restaurant market in 2024, driven by urban hubs like Mumbai, Pune, and Ahmedabad. This region benefits from higher per capita income, a strong franchise culture, and the presence of premium retail spaces. Consumers in West India show a high preference for quick meals and global food brands, fueling the growth of chained QSRs. Mall culture, expanding co-working spaces, and increasing food tech penetration further amplify demand. A mix of cosmopolitan and regional tastes creates opportunities for menu innovation, sustaining regional momentum in both dine-in and delivery formats.

East India

East India held the smallest share in 2024, accounting for 16% of the India Quick Service Restaurant market. Despite lagging behind other regions, cities like Kolkata, Patna, and Bhubaneswar are witnessing rising QSR adoption. Urbanization, better retail infrastructure, and increased digital engagement are improving market access. While consumer spending power is comparatively lower, growing brand awareness and the entry of national QSR chains are expanding regional footprints. Delivery-led models are gaining traction, especially among the younger population. As infrastructure and disposable income improve, East India is expected to emerge as a promising growth zone in the long term.

Market Segmentations:

By Service Type

- Dine-In

- Takeaway

- Delivery

By Cuisine Type

- American

- Italian

- Asian

- Others

By Restaurant Type

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The India Quick Service Restaurant (QSR) market is highly competitive, with a mix of global giants and strong domestic players vying for market share. International brands such as Domino’s Pizza, McDonald’s, KFC, and Pizza Hut have established a robust presence through extensive franchising models, aggressive expansion, and localized menu offerings tailored to Indian tastes. These brands leverage economies of scale, consistent quality, and strong delivery infrastructure to maintain customer loyalty. Domestic players like Haldiram’s and Nirula’s continue to strengthen their regional dominance by combining traditional flavors with modern service formats. New entrants such as Popeyes are expanding rapidly, capitalizing on India’s growing appetite for Western fast food. The competitive landscape is further intensified by increasing investments in digital ordering platforms, loyalty programs, and kitchen automation. As consumer expectations evolve, brands are focusing on innovation, sustainability, and speed of service to differentiate and retain their position in this dynamic and fast-growing market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Domino’s Pizza

- KFC

- McDonald’s

- Pizza Hut

- Haldiram’s

- Nirula’s

- Popeyes

Recent Developments

- In July 2025, Domino’s India opened 184 new stores in FY25 and plans to open 230 more in the ongoing fiscal year, targeting a total of 280 new stores (250 in India, 30 in Turkey). Domino’s now has over 2,000 stores in India, making it the brand’s second-largest market globally.

- In February 2024, Westlife Foodworld, the operator of McDonald’s in southern and western India, experienced a significant decline in its third-quarter profits (Q3 FY24). This drop was primarily attributed to inflationary pressures and reduced consumer spending, leading to a decrease in the frequency of dining out. Specifically, the company’s consolidated profit after tax (PAT) fell by 59% to Rs 7.01 crore compared to the same period last year.

- In January 2023, Popeyes India added a new Shrimp Roll to its seafood menu. This move was part of the brand’s strategy to expand its offerings and appeal to the increasing demand for seafood options within the quick-service restaurant (QSR) sector in India.

Market Concentration & Characteristics

The India Quick Service Restaurant Market exhibits a moderately concentrated structure, with a few dominant players such as Domino’s Pizza, McDonald’s, KFC, and Pizza Hut holding significant market shares. It is characterized by the presence of both international chains and regional brands, with franchising models enabling rapid expansion across metropolitan and Tier 2 cities. Organized players leverage standardized operations, strong brand recall, and digital delivery platforms to maintain a competitive edge. The market favors chains offering affordability, speed, and consistency in service. Independent QSR outlets and regional players contribute to fragmentation in smaller cities. Consumer behavior in this market reflects a growing preference for convenience, digital ordering, and value-driven menus, particularly among young and urban populations. It remains highly competitive, with continuous innovation in menu offerings, loyalty programs, and technology integration shaping brand strategies. The ability to scale operations while adapting to regional tastes remains critical for long-term success.

Report Coverage

The research report offers an in-depth analysis based on Service Type, Cuisine Type, Restaurant Type and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The India QSR market is expected to witness steady expansion driven by rising urbanization and growing consumer demand for convenience-based dining.

- Increased penetration of online food delivery platforms will continue to boost sales for both chained and independent QSR outlets.

- Franchise-based expansion into Tier 2 and Tier 3 cities will unlock new growth opportunities for national and international brands.

- Demand for health-conscious menus, including plant-based and low-calorie offerings, will shape future menu innovation.

- QSR brands will increasingly invest in technology such as AI, digital kiosks, and cloud kitchens to improve efficiency and scalability.

- Competitive pricing and value-driven combo offerings will remain critical in retaining price-sensitive consumers.

- Regional customization of menus will help QSR chains cater to local tastes and improve customer engagement.

- Strategic partnerships with food delivery aggregators and fintech platforms will enhance customer convenience and loyalty.

- Real estate cost optimization through smaller, delivery-focused formats will be a key operational strategy.

- Market consolidation may increase as dominant players expand aggressively, creating challenges for small and unorganized QSR businesses.