Meat Packing Paper Market Overview:

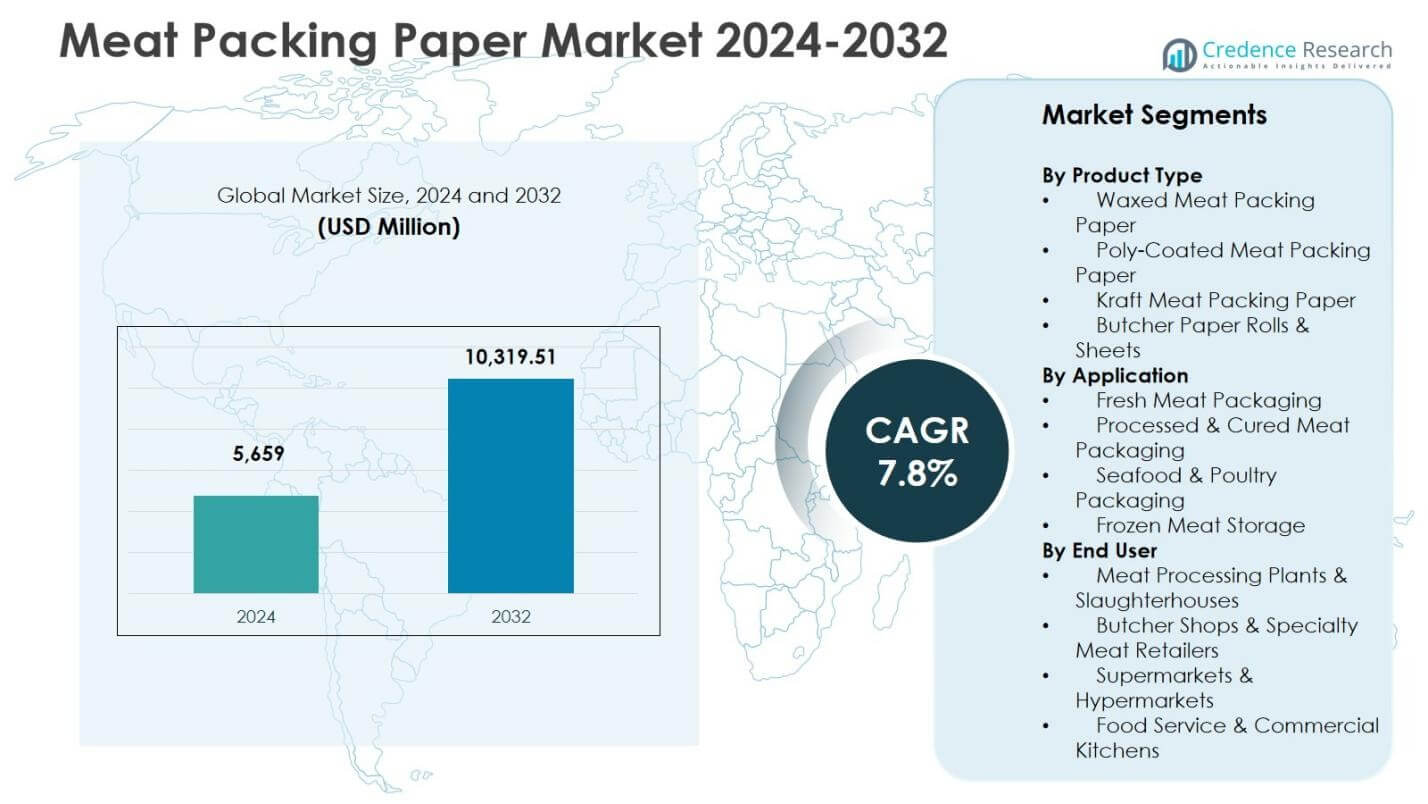

Meat Packing Paper Market size was valued USD 5,659 Million in 2024 and is anticipated to reach USD 10,319.51 Million by 2032, at a CAGR of 7.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Meat Packing Paper Market Size 2024 |

USD 5,659 million |

| Meat Packing Paper Market, CAGR |

7.8% |

| Meat Packing Paper Market Size 2032 |

USD 10,319.51 million |

Meat Packing Paper Market Insights

- Market growth is driven by rising demand for eco-friendly and recyclable kraft and poly-coated paper solutions, increasing packaged meat consumption, and expanding cold-chain and organized retail networks supporting higher usage across fresh and processed meat applications.

- Market trends reflect growing preference for moisture-resistant and grease-barrier butcher paper, with the Kraft Meat Packing Paper segment leading with 38.6% share in 2024 due to strength, sustainability, and suitability for hygienic wrapping needs.

- Leading manufacturers strengthen their presence through product innovation, barrier-enhanced coatings, freezer-grade formats, and collaboration with meat processors and retailers to improve performance, branding, and value-added packaging capability across fresh, cured, and frozen meat categories.

- Regional analysis shows North America holding 32.4% share in 2024, Europe capturing 27.9% share, and Asia-Pacific accounting for 24.6% share, supported by retail modernization, rising protein demand, and increasing adoption of paper-based meat packaging solutions.

Meat Packing Paper Market Segmentation Analysis:

By Product Type:

In the Meat Packing Paper Market, the Kraft Meat Packing Paper segment dominated the product type category with a 38.6% market share in 2024, supported by its high tensile strength, grease resistance, and suitability for eco-friendly packaging formats. Growing retailer preference for sustainable and recyclable packaging materials strengthens demand for kraft-based solutions in fresh and processed meat handling. The Waxed Meat Packing Paper, Poly-Coated variants, and Butcher Paper Rolls & Sheets segments continue expanding, driven by increasing hygienic wrapping needs, improved barrier protection, and rising adoption in specialty meat retail environments.

- For instance, PG Paper supplies MG (Machine Glazed) and MF (Machine Finished) bleached kraft paper for direct food contact in meat wrapping, offering customizable printing while maintaining food safety standards and high strength from the kraft pulping process.

By Application:

By application, Fresh Meat Packaging emerged as the leading segment with a 42.3% share of the Meat Packing Paper Market in 2024, driven by rising consumption of fresh-cut meat and the need for moisture-retentive, contamination-resistant wrapping solutions. Demand is reinforced by stricter cold-chain handling standards and retail focus on product shelf-life extension. Processed & Cured Meat Packaging, Seafood & Poultry Packaging, and Frozen Meat Storage segments are also growing, supported by expanding packaged protein consumption, export-oriented meat processing, and the integration of paper-based solutions as sustainable alternatives to plastic formats.

- For instance, Mondi also collaborated with HKScan on renewable paper-based packaging for Falukory sausages, Sweden’s best-seller. The solution replaces traditional wraps while maintaining product protection during transport and retail display.

By End User:

In terms of end user, Supermarkets & Hypermarkets accounted for the largest share of the Meat Packing Paper Market with 36.8% in 2024, owing to their high throughput of packaged meat products and reliance on durable, food-safe paper for in-store wrapping and display operations. Growth is driven by retail expansion, increased private-label meat sales, and emphasis on hygienic handling standards. Meat Processing Plants & Slaughterhouses, Butcher Shops & Specialty Meat Retailers, and Food Service & Commercial Kitchens also represent significant demand contributors as they adopt paper-based packaging for operational efficiency and sustainability compliance.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Rising Demand for Sustainable and Eco-Friendly Meat Packaging

The Meat Packing Paper Market benefits significantly from the accelerating global shift toward sustainable and recyclable packaging solutions. Governments, retailers, and meat processors increasingly prioritize eco-friendly alternatives to plastic films, driving strong adoption of paper-based formats across retail counters, butcher outlets, and meat processing facilities. Meat packing paper supports biodegradability, lower carbon emissions, and regulatory compliance for environmentally responsible packaging. In addition, growing consumer awareness regarding food safety and reduced plastic waste reinforces demand for kraft-based and waxed paper solutions. As sustainability becomes a core procurement criterion, manufacturers invest in upgraded paper barrier technologies that deliver performance while supporting circular-economy objectives.

- For instance, CoCopac partnered with a leading meat processor in June 2023 to supply Eco-Life meat interleaving paper. This initiative aims to reduce the environmental footprint in the meat industry by using sustainable, compostable paper that separates slices, absorbs moisture, and extends shelf life during freezing and packaging.

Expansion of Organized Retail and Cold-Chain Meat Distribution Networks

Rapid expansion of supermarkets, hypermarkets, and specialty meat retail chains strengthens demand for standardized, hygienic, and display-friendly meat packing materials. As modern retail formats handle higher packaged meat volumes, paper-based wrapping solutions gain prominence for fresh meat, poultry, and seafood segments due to durability and grease resistance. Growth in cold-chain logistics and chilled meat distribution further increases the use of packing paper that supports moisture retention and product integrity during storage and transport. This structural retail transformation fosters consistent procurement cycles, accelerates adoption of quality-certified paper variants, and positions meat packing paper as an essential packaging component across large-scale retail environments.

- For instance, Aldi UK, partnering with ABP Food Group and Graphic Packaging International, rolled out fiber-based pressed board trays for core and premium steak lines, reducing plastic by 90% and running on existing lines for cold-chain compatibility.

Increasing Meat Processing and Value-Added Product Manufacturing

The rising production of processed, cured, and ready-to-cook meat products acts as a key growth catalyst for the Meat Packing Paper Market. Meat processors increasingly require high-performance paper wraps to ensure hygiene, operational efficiency, and product protection across cutting, portioning, and packing stages. Demand strengthens further with the expansion of export-oriented meat processing facilities and contract packaging operations. Premium butcher paper, poly-coated wrapping sheets, and reinforced kraft papers support branding, shelf-life management, and regulatory compliance in value-added meat applications. As protein consumption trends shift toward packaged formats, the role of meat packing paper becomes more strategic within industrial processing ecosystems.

Key Trends & Opportunities

Transition Toward High-Performance Barrier and Coated Paper Solutions

A major trend shaping the Meat Packing Paper Market is the advancement of barrier-enhanced and coated paper technologies designed to improve grease resistance, moisture control, and tear strength. Manufacturers increasingly develop poly-coated and wax-treated papers that deliver functional performance comparable to plastics while maintaining recyclability advantages. This shift creates opportunities for innovation in specialty butcher paper, freezer-grade wraps, and antibacterial surface coatings tailored for food safety compliance. Integration of printing and branding features on packing paper also enables retail differentiation and traceability. As demand rises for premium packaging performance, suppliers investing in advanced paper engineering and coating processes gain strong competitive positioning.

- For instance, UPM Specialty Papers and Eastman developed a biopolymer-coated paper using BioPBS™ for grease and oxygen barriers in meat pies and confectionery, compatible with standard LDPE equipment and recyclable in fiber streams.

Growing Adoption of Paper Packaging Across Specialty Butcher and Premium Meat Retail

Premium meat counters, gourmet butcher shops, and specialty protein retailers increasingly adopt paper-based packaging to enhance product presentation and align with artisanal and sustainable brand positioning. This trend creates opportunities for customized butcher paper rolls, printed kraft wraps, and branded packaging formats designed to elevate consumer perception and reinforce freshness appeal. Paper packaging also supports transparency in authenticity-focused meat categories such as organic, grass-fed, and locally sourced products. Expansion of specialty meat retail networks, coupled with consumer preference for visually appealing and eco-conscious wrapping, opens new revenue streams for manufacturers offering tailored, value-added paper packaging solutions.

- For instance, Whole Foods Market uses poly-coated brown butcher paper at its meat counters to wrap fresh cuts, providing a printed design that highlights the store’s branding while containing meat juices effectively.

Key Challenges

Competition from Plastic Films and Vacuum Packaging Technologies

One of the primary challenges for the Meat Packing Paper Market is the strong presence of plastic films and vacuum-sealed packaging formats that offer extended shelf life, airtight sealing, and superior barrier performance. Large meat processors often rely on plastic-based solutions for long-distance cold-chain transport and export shipments, limiting full substitution by paper alternatives. Additionally, price competitiveness and efficiency advantages associated with automated plastic packaging lines create adoption barriers for paper formats in high-volume processing environments. Overcoming this challenge requires continual paper technology upgrades, improved moisture and oxygen resistance, and stronger value propositions emphasizing sustainability and regulatory alignment.

Cost Fluctuations in Raw Materials and Supply Chain Constraints

Volatility in pulp and paper raw material prices presents a significant challenge for manufacturers in the Meat Packing Paper Market. Rising costs of wood fiber, energy, and transportation increase production expenses and pressure margins, particularly for small and mid-scale producers. Supply chain disruptions, capacity constraints in specialty paper manufacturing, and fluctuating import-export dynamics further complicate sourcing stability. These challenges may lead to pricing inconsistencies for end users such as retailers and processors, affecting procurement decisions. To mitigate risks, market participants increasingly explore supply diversification, backward integration strategies, and process efficiencies to stabilize production economics and ensure consistent market availability.

Regional Analysis

North America

North America held a leading position in the Meat Packing Paper Market and accounted for 32.4% market share in 2024, driven by strong consumption of packaged meat, the presence of advanced meat processing facilities, and a well-established cold-chain distribution network. The region benefits from rapid adoption of sustainable, food-grade paper solutions across supermarkets, hypermarkets, and specialty butcher stores. Increasing regulatory emphasis on eco-friendly packaging and consumer preference for recyclable kraft and waxed papers further accelerates demand. Growth is reinforced by premium meat retail formats and private-label expansion, strengthening the adoption of high-performance butcher paper and coated wrapping solutions.

Europe

Europe represented a significant market and captured 27.9% market share in 2024, supported by stringent environmental regulations, strong sustainability policies, and rapid transition away from plastic-based packaging materials. Meat processors and retail chains increasingly adopt recyclable kraft and coated paper formats to align with circular-economy objectives and carbon-reduction commitments. Demand is further driven by the growth of processed meat and premium specialty butcher outlets across Western European countries. The region also witnesses investments in barrier-enhanced paper technologies and customized branding-enabled wrapping formats, strengthening the market position of paper-based meat packaging within retail, foodservice, and industrial processing environments.

Asia-Pacific

Asia-Pacific emerged as the fastest-growing regional market and accounted for 24.6% market share in 2024, fueled by rising meat consumption, expansion of organized retail, and rapid growth in meat processing industries across China, India, and Southeast Asia. Increasing urbanization and cold-chain infrastructure development drive higher demand for hygienic, moisture-resistant wrapping paper in fresh and processed meat distribution. Government initiatives promoting sustainable packaging and retailer preference for cost-efficient kraft and poly-coated paper formats further support adoption. Local manufacturing expansion and investments in specialty butcher paper production strengthen the regional supply ecosystem and enhance market penetration across retail and industrial segments.

Latin America

Latin America accounted for 8.7% market share in 2024, driven by the expansion of export-oriented meat processing industries in Brazil, Argentina, and Mexico, along with rising demand for packaged beef and poultry products in domestic retail markets. Meat packing paper adoption grows due to increasing hygiene standards, modernization of slaughterhouses, and growth in supermarket meat counters. The region experiences steady transition toward recyclable and cost-efficient kraft and waxed paper formats, particularly in fresh and chilled meat handling. Investments in value-added meat production and retail private-label programs further stimulate usage of durable butcher paper and wrapping sheet solutions.

Middle East & Africa

The Middle East & Africa region held 6.4% market share in 2024, supported by expanding urban retail networks, growth in modern grocery formats, and rising demand for packaged poultry and processed meat products. GCC countries experience increasing adoption of grease-resistant and food-safe meat packing paper across hypermarkets and quick-service food outlets. In Africa, market growth is driven by gradual modernization of meat processing facilities and strengthening cold-chain distribution. Sustainability-focused initiatives and the shift toward paper-based wrapping alternatives enhance long-term demand potential, while imports and regional investments in specialty paper supply support broader market development across key economies.

Meat Packing Paper Market Segmentations:

By Product Type

- Waxed Meat Packing Paper

- Poly-Coated Meat Packing Paper

- Kraft Meat Packing Paper

- Butcher Paper Rolls & Sheets

By Application

- Fresh Meat Packaging

- Processed & Cured Meat Packaging

- Seafood & Poultry Packaging

- Frozen Meat Storage

By End User

- Meat Processing Plants & Slaughterhouses

- Butcher Shops & Specialty Meat Retailers

- Supermarkets & Hypermarkets

- Food Service & Commercial Kitchens

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape in the Meat Packing Paper Market is shaped by major players such as Amcor plc, Berry Global Group Inc., Sealed Air Corporation, Mondi plc, Winpak Ltd, Sonoco Products Company, Pactiv Evergreen Inc., Ahlstrom-Munksjö Oyj, WestRock Company, and Georgia-Pacific LLC. The market features a balanced mix of global packaging conglomerates and specialty paper manufacturers that compete on product performance, sustainability credentials, and cost efficiency. Companies focus on developing grease-resistant, moisture-barrier, and recyclable kraft and coated paper solutions to meet rising regulatory and retailer expectations for eco-friendly meat packaging. Strategic priorities include investments in advanced coating technologies, expansion of freezer-grade and butcher-grade paper formats, and strengthening supply capabilities for fresh and processed meat distribution networks. Partnerships with meat processors and retail chains, portfolio diversification across waxed and poly-coated variants, and branding-enabled wrapping formats further define competition, as suppliers emphasize quality consistency, hygiene assurance, and sustainable value propositions to secure long-term procurement relationships in retail and industrial markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Amcor plc

- Berry Global Group Inc.

- Sealed Air Corporation

- Mondi plc

- Winpak Ltd

- Sonoco Products Company

- Pactiv Evergreen Inc.

- Ahlstrom-Munksjö Oyj

- WestRock Company

- Georgia-Pacific LLC

Recent Developments

- In April 2025, Amcor completed its $8.43 billion all-stock acquisition of Berry Global, creating a leading packaging powerhouse with combined revenues of $24 billion and enhanced capabilities in meat packaging solutions.

- In September 2025, ProAmpac partnered with Divilly Brothers to introduce ProActive Recyclable® FibreSculpt high-barrier fibre-based packaging for chilled cooked meats, enhancing recyclability while maintaining freshness and premium appearance.

- In December 2025, ProAmpac agreed to acquire TC Transcontinental Packaging, strengthening its position in flexible and paper-based packaging across food segments.

- In June 2024, Chevler launched brightly-coloured protective meat packaging paper within its Meat Saver Paper range to meet demand for enhanced visual appeal and product protection.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, End User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will witness sustained growth as retailers and processors increasingly adopt recyclable and eco-friendly meat packing paper solutions.

- Manufacturers will focus on developing stronger, grease-resistant, and moisture-barrier paper grades to support food safety and shelf-life requirements.

- Demand will rise from organized retail chains, specialty butcher outlets, and premium meat brands emphasizing sustainable packaging identity.

- Paper-based packaging will gain further preference over plastics due to tightening environmental regulations and corporate sustainability commitments.

- Innovation in coated, waxed, and freezer-grade paper formats will expand application opportunities across fresh, processed, and frozen meat segments.

- Branding, printability, and customization features on packing paper will strengthen product differentiation in retail meat displays.

- Investments in regional paper manufacturing and supply integration will enhance cost efficiency and market availability.

- Digital traceability, labeling compatibility, and hygiene-compliant packaging formats will become more important for processors and retailers.

- Emerging markets will contribute strongly as cold-chain expansion and meat processing capacity increase.

- Strategic partnerships between packaging suppliers and meat processors will accelerate product innovation and long-term procurement alignment.