| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Middle East Cheese Market Size 2024 |

USD 1,978.03 Million |

| Middle East Cheese Market, CAGR |

2.66% |

| Middle East Cheese Market Size 2032 |

USD 2,441.06 Million |

Market Overview

Middle East Cheese Market size was valued at USD 1,978.03 million in 2024 and is anticipated to reach USD 2,441.06 million by 2032, at a CAGR of 2.66% during the forecast period (2024-2032).

The Middle East cheese market is experiencing steady growth, driven by shifting consumer preferences toward Western dietary habits and the increasing popularity of cheese as a key ingredient in both traditional and international cuisines. Rising urbanization and disposable incomes have fueled demand for convenient and processed food products, including packaged cheese. Additionally, the expanding retail infrastructure and the growth of modern trade channels have enhanced product availability and accessibility across the region. Health-conscious consumers are also contributing to the demand for low-fat and organic cheese options, prompting manufacturers to innovate and diversify their offerings. The rising influence of global food chains and quick-service restaurants further supports market expansion. Moreover, government initiatives to boost domestic dairy production and reduce reliance on imports are encouraging local cheese manufacturing. These factors, combined with a growing young population and an increasing number of expatriates, are shaping consumption trends and driving the overall growth of the cheese market in the Middle East.

The geographical landscape of the Middle East cheese market is shaped by diverse consumer preferences, strong import dependencies, and varying levels of domestic production across countries such as the UAE, Saudi Arabia, Turkey, Israel, Iran, and the broader region. Urban centers and countries with higher disposable incomes exhibit stronger demand for premium and specialty cheese varieties, while traditional cheese types remain popular in culturally rooted markets. The UAE and Saudi Arabia lead in terms of consumption, driven by evolving food habits and expanding retail and hospitality sectors. Meanwhile, Turkey and Iran are notable for their rich dairy traditions and local cheese production. Prominent key players operating in the Middle East cheese market include Arla Foods, Savencia Fromage & Dairy, Clover Industries Limited, Danone, Hochland SE, Parmalat S.p.A., Al Ain Dairy, FrieslandCampina, and Ruwag Food Industries. These companies focus on product innovation, regional partnerships, and distribution expansion to cater to the region’s evolving dietary trends.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Middle East cheese market was valued at USD 1,978.03 million in 2024 and is expected to reach USD 2,441.06 million by 2032, growing at a CAGR of 2.66%.

- The global cheese market was valued at USD 97,440.00 million in 2024 and is projected to reach USD 1,46,171.12 million by 2032, growing at a CAGR of 5.20% during the forecast period.

- Rising urbanization and shifting dietary habits are boosting cheese consumption across both traditional and Western cuisines.

- Consumers are increasingly drawn to premium, flavored, and spreadable cheese varieties, driven by innovation and changing tastes.

- Major players such as Arla Foods, Danone, and Savencia Fromage & Dairy are investing in new product development and expanding their regional distribution networks.

- High dependency on imports and fluctuating trade regulations pose challenges to consistent supply and pricing in the region.

- Saudi Arabia and the UAE lead the market due to growing retail infrastructure and high per capita consumption.

- Traditional cheese production in Turkey and Iran continues to support domestic markets while contributing to regional exports.

Report Scope

This report segments the Middle East Cheese Market as follows:

Market Drivers

Rising Urbanization and Changing Dietary Preferences

The rapid pace of urbanization across the Middle East has significantly influenced consumer lifestyles and dietary habits. As more people migrate to urban centers, they are exposed to diverse culinary cultures, including Western cuisines that feature cheese as a staple ingredient. For instance, a report by the Food and Agriculture Organization (FAO) highlights that urban households in Saudi Arabia and the UAE are increasingly incorporating cheese into their diets due to its versatility and convenience. The growing middle-class population, especially in countries like Saudi Arabia, the UAE, and Qatar, is increasingly seeking convenience and variety in their diets, which has led to higher consumption of processed and packaged cheese products. Additionally, the influence of social media and international travel has further broadened consumer exposure to global food trends, reinforcing the adoption of cheese in everyday meals and snacks. These evolving dietary patterns have positioned cheese as a preferred choice among urban consumers, thereby driving market growth across the region.

Expansion of Retail and Foodservice Channels

The growth of modern retail formats and foodservice outlets is another key driver of the Middle East cheese market. Supermarkets, hypermarkets, and convenience stores are expanding their presence in both urban and semi-urban areas, offering a wide range of cheese products from both domestic and international brands. Simultaneously, the rise of quick-service restaurants (QSRs), cafes, and international food chains has boosted the use of cheese in ready-to-eat meals, pizzas, burgers, and bakery items. These outlets not only increase cheese consumption but also serve as platforms for introducing new flavors and product innovations. Moreover, the availability of cheese through e-commerce platforms and grocery delivery services has enhanced accessibility, catering to tech-savvy consumers who prioritize convenience, thereby supporting sustained demand.

Supportive Government Policies and Local Dairy Production

Government initiatives aimed at enhancing food security and reducing dependence on cheese imports have led to increased investments in local dairy production across the Middle East. For instance, a report by Farrelly Mitchell highlights that Saudi Arabia’s Vision 2030 plan includes subsidies and infrastructure development to boost domestic cheese manufacturing capabilities. Countries such as Saudi Arabia and the UAE are actively promoting domestic cheese manufacturing through subsidies, infrastructure development, and strategic partnerships with global dairy players. These efforts not only reduce supply chain disruptions but also foster the growth of regional cheese brands capable of competing with imported products. In addition, collaborations with international dairy companies have facilitated knowledge transfer, technological advancements, and capacity building, contributing to improved product quality and market competitiveness. This supportive policy environment continues to play a critical role in boosting the Middle East cheese market’s long-term sustainability and growth.

Rising Health Awareness and Demand for Specialty Cheese

Health consciousness among consumers is gaining momentum across the Middle East, leading to a surge in demand for healthier and specialty cheese variants. Consumers are increasingly looking for organic, low-fat, lactose-free, and plant-based cheese options to align with their dietary restrictions and wellness goals. This shift has encouraged manufacturers to invest in product innovation and clean-label formulations, incorporating natural ingredients and avoiding artificial additives. The availability of specialty cheeses, such as goat cheese and vegan alternatives, has expanded the market’s consumer base, including health enthusiasts and individuals with dietary sensitivities. Furthermore, the growing trend of protein-rich diets and awareness of cheese as a good source of calcium and other nutrients have reinforced its inclusion in daily meals, thereby driving market expansion.

Market Trends

Surging Demand for Processed and Convenient Cheese Products

The Middle East cheese market is witnessing a strong shift toward processed and ready-to-use cheese products, fueled by changing consumer lifestyles and time constraints. For instance, a report by the Saudi Ministry of Environment, Water, and Agriculture highlights that urban households increasingly rely on shredded and sliced cheese for quick meal preparations. Urban consumers, particularly working professionals and young families, increasingly prefer cheese that is easy to store, cook, and consume. Processed cheese slices, spreads, cubes, and shredded variants are gaining traction due to their convenience and longer shelf life. In response, manufacturers are expanding their product portfolios to include a variety of flavors, packaging formats, and usage options, targeting both retail and foodservice segments. The growing influence of Western fast-food culture and the rise in snacking habits further amplify the consumption of processed cheese across the region.

Emergence of Health-Focused and Functional Cheese Varieties

Health and wellness trends are significantly shaping consumer choices in the Middle East cheese market. With rising awareness of nutritional content, consumers are actively seeking healthier cheese alternatives, such as low-fat, low-sodium, and high-protein options. For instance, a survey by the UAE Ministry of Health reported that consumers are gravitating toward low-fat and plant-based cheese options as part of their wellness journeys. Functional cheese varieties enriched with probiotics, calcium, and vitamins are also gaining popularity among health-conscious demographics. Moreover, lactose-intolerant and vegan consumers are fueling demand for dairy-free and plant-based cheese substitutes. In response, industry players are investing in R&D and clean-label innovations to meet evolving dietary needs. This trend is expected to accelerate further as regional consumers become more informed about the health implications of their food choices.

Growing Popularity of Specialty and Artisanal Cheeses

The Middle East market is experiencing rising interest in premium, specialty, and artisanal cheeses, driven by evolving consumer tastes and the expanding gourmet food culture. Consumers are showing increased willingness to explore diverse cheese textures and flavors beyond traditional options. Imported cheese varieties such as Gouda, Camembert, Brie, and Blue cheese are gaining attention among affluent consumers and expatriates. At the same time, there is a growing appreciation for locally made artisanal cheeses that reflect regional taste preferences and culinary heritage. This trend is particularly prominent in the hospitality sector, where luxury hotels, fine-dining restaurants, and boutique delis are incorporating specialty cheeses into their menus to enhance customer experience.

Digitalization and E-Commerce Driving Market Accessibility

The expansion of digital retail and food delivery platforms is transforming the cheese market in the Middle East. Consumers are increasingly using e-commerce platforms to explore, compare, and purchase a wide range of cheese products. Online grocery apps, specialty food websites, and subscription-based dairy services are playing a critical role in reaching tech-savvy and convenience-driven consumers. Additionally, brands are leveraging digital marketing and social media to engage with customers, promote new launches, and build brand loyalty. This digital shift has not only improved product accessibility across urban and semi-urban regions but has also enabled small and niche brands to gain visibility in a highly competitive market landscape.

Market Challenges Analysis

High Dependence on Imports and Supply Chain Vulnerabilities

One of the primary challenges facing the Middle East cheese market is its high dependence on imported cheese products, especially premium and specialty varieties. Despite growing local dairy initiatives, many countries in the region still rely heavily on imports to meet consumer demand, particularly for European cheeses that dominate the premium segment. This reliance exposes the market to global supply chain disruptions, fluctuating import tariffs, and currency exchange risks, all of which can impact pricing and product availability. Furthermore, geopolitical instability and trade restrictions in the region can further hinder the smooth flow of dairy imports, causing delays and limiting product choices for consumers. These factors collectively pose a significant challenge to market stability and long-term growth, especially in countries with limited domestic dairy infrastructure.

Stringent Regulatory Standards and Rising Health Concerns

The Middle East cheese market also faces challenges related to regulatory compliance and growing health awareness among consumers. Governments across the region are implementing stricter food safety regulations, labeling requirements, and quality standards to protect public health and promote transparency. For instance, the Saudi Food and Drug Authority (SFDA) has introduced new labeling requirements mandating clear disclosure of fat and sodium content in cheese products, increasing compliance costs for manufacturers. While these regulations are necessary, they can increase operational costs for manufacturers, especially small and medium-sized enterprises (SMEs) that may struggle to comply with evolving standards. Additionally, the rising incidence of lifestyle-related health issues such as obesity, heart disease, and lactose intolerance has led to increased scrutiny of high-fat and high-sodium food products, including cheese. Health-conscious consumers are becoming more selective, reducing their consumption of conventional cheese and opting for healthier alternatives. This shift creates pressure on traditional cheese producers to reformulate their products or lose market share to newer, health-driven brands. Balancing taste, nutrition, and compliance remains a critical challenge for stakeholders in the region’s cheese industry.

Market Opportunities

The Middle East cheese market presents significant growth opportunities driven by the region’s expanding population, increasing urbanization, and rising disposable incomes. As more consumers embrace Western food habits and international cuisines, demand for diverse cheese varieties continues to rise. This trend opens the door for manufacturers to introduce new product lines that cater to evolving taste preferences, including flavored, spiced, and fusion cheeses. Additionally, the hospitality and foodservice sectors are witnessing steady growth, with hotels, cafes, and quick-service restaurants incorporating cheese-based dishes to appeal to a broader customer base. This creates consistent demand for both bulk and specialty cheese products, offering opportunities for local and international suppliers to scale their operations in the region.

Moreover, the rising focus on health and wellness among consumers creates a favorable environment for the development and marketing of functional and specialty cheese products. There is growing demand for organic, low-fat, high-protein, lactose-free, and plant-based cheese alternatives, particularly among younger consumers and health-conscious individuals. This shift allows manufacturers to diversify their offerings and position their brands within niche segments. Additionally, advancements in cold chain logistics and packaging technology are improving the shelf life and quality of cheese products, facilitating wider distribution across the region, including remote and underserved areas. E-commerce and digital marketing further enhance visibility and direct-to-consumer engagement, offering small and emerging brands the opportunity to compete alongside established players. Together, these trends signal strong potential for innovation, investment, and expansion within the Middle East cheese market.

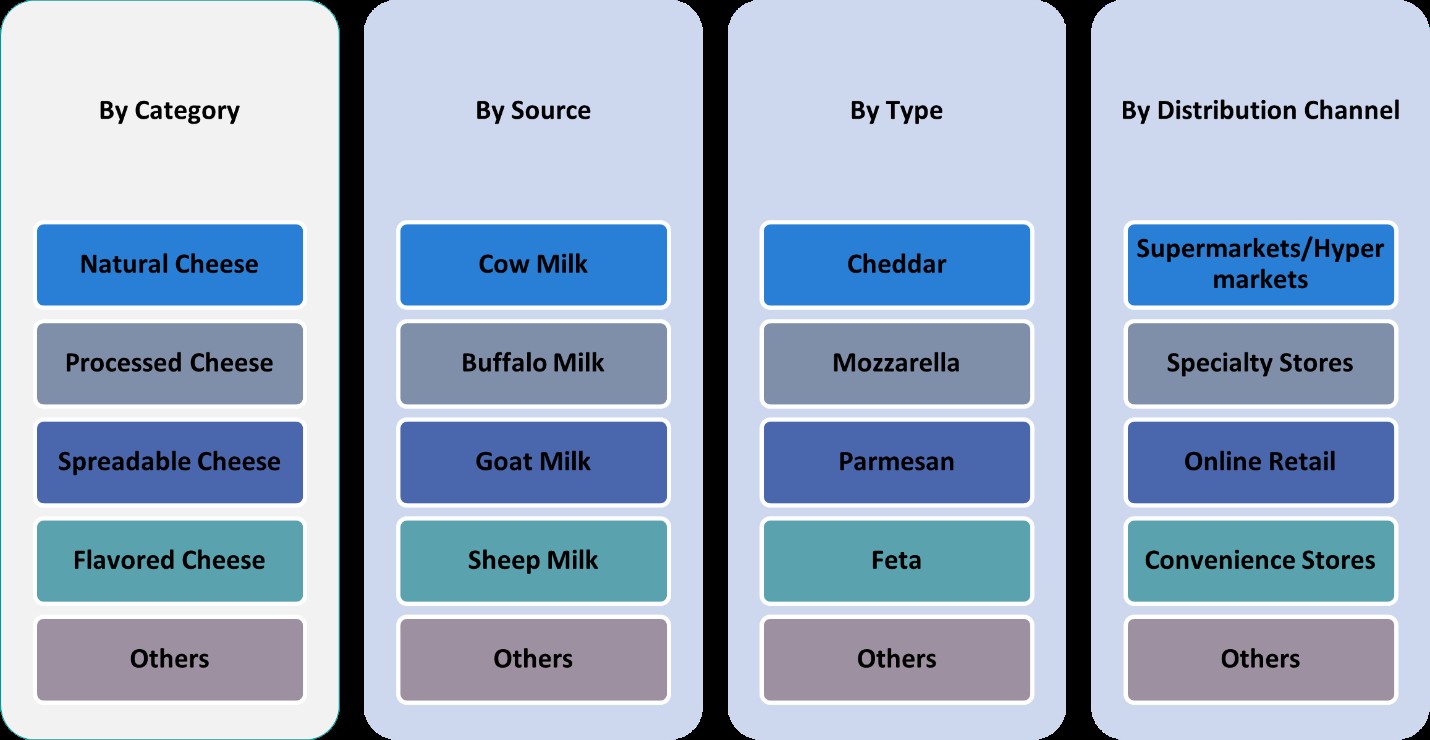

Market Segmentation Analysis:

By Category:

The Middle East cheese market is segmented into Cheddar, Processed Cheese, Spreadable Cheese, Flavored Cheese, and Others. Among these, processed cheese holds a significant market share due to its convenience, longer shelf life, and wide application in fast foods, snacks, and home-cooked meals. It is especially popular among young consumers and busy households. Cheddar cheese also enjoys strong demand, driven by its versatility in traditional dishes and Western-style recipes. The spreadable cheese segment is witnessing notable growth, as it caters to breakfast consumption trends and is commonly used with breads and crackers. Flavored cheeses, infused with herbs, spices, or regional seasonings, are gaining popularity among consumers looking for unique taste experiences, especially in hospitality and premium retail. The “Others” category, which includes specialty and artisanal cheeses, is gradually expanding as consumers show growing interest in gourmet and international varieties. Each category presents specific opportunities, allowing manufacturers to target diverse consumer groups across both mass and premium segments.

By Source:

Based on source, the Middle East cheese market is divided into Cow Milk, Buffalo Milk, Goat Milk, Sheep Milk, and Others. Cow milk dominates the market due to its wide availability, lower production cost, and familiarity among consumers across the region. It is commonly used in the production of processed and cheddar cheese. Buffalo milk, known for its high fat content, is also gaining attention for producing rich and creamy cheese types, especially in traditional cooking. Goat and sheep milk cheeses are emerging as premium offerings, valued for their distinctive flavor and easier digestibility, making them popular among health-conscious and lactose-sensitive consumers. These variants are especially appealing in the gourmet and specialty cheese categories. The “Others” segment, which includes plant-based or alternative milk sources, is still niche but gradually gaining traction with the growing vegan population and demand for dairy-free options. This diversity in sourcing allows producers to innovate and cater to a wide range of dietary needs and taste preferences across the region.

Segments:

Based on Category:

- Cheddar

- Processed Cheese

- Spreadable Cheese

- Flavored Cheese

- Others

Based on Source:

- Cow Milk

- Buffalo Milk

- Goat Milk

- Sheep Milk

- Others

Based on Type:

- Cheddar

- Mozzarella

- Parmesan

- Feta

- Others

Based on Distribution Channel:

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail

- Convenience Stores

- Others

Based on the Geography:

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

Regional Analysis

United Arab Emirates (UAE)

The United Arab Emirates holds a market share of approximately 23% in the Middle East cheese market, making it one of the key contributors to regional revenue. The UAE’s high per capita income, cosmopolitan population, and strong tourism sector drive robust demand for a wide range of cheese products. Consumers in the UAE are highly receptive to international cuisines, which fuels the popularity of both traditional and Western-style cheeses, including cheddar, mozzarella, and cream cheese. Moreover, the expanding retail infrastructure and presence of global supermarket chains enable widespread availability of imported and specialty cheeses. The foodservice sector—particularly cafes, bakeries, and fast-food outlets—further supports cheese consumption, making the UAE a lucrative market for both domestic and international suppliers.

Kingdom of Saudi Arabia (KSA)

Saudi Arabia commands the largest market share in the region at approximately 30%, supported by its vast population and rising demand for packaged and processed foods. As the country undergoes social and economic transformation under Vision 2030, changing lifestyles and increasing urbanization are significantly influencing dietary patterns. Cheese is a staple in many Saudi households, with processed and spreadable variants enjoying consistent popularity. Government-led initiatives to boost local dairy production and reduce dependency on imports are also stimulating domestic cheese manufacturing. Additionally, the expansion of food retail chains and QSRs (Quick Service Restaurants) is further increasing cheese usage in ready-to-eat meals and snacks, solidifying KSA’s dominant position in the regional market.

Turkey

Turkey represents a market share of about 18% in the Middle East cheese market, benefiting from its rich dairy heritage and strong domestic production. Turkish cheese varieties such as beyaz peynir, kasar, and tulum are widely consumed both within the country and across neighboring regions. The country’s strategic geographical location and established export infrastructure enable it to serve as a major supplier of cheese to other Middle Eastern nations. Furthermore, growing demand for authentic, artisanal, and traditional cheeses among health-conscious and culturally inclined consumers across the region continues to elevate Turkey’s role as a leading producer and exporter of regional cheese varieties.

Israel

Israel accounts for an estimated market share of 11% in the Middle East cheese market, driven by strong domestic demand and product innovation. The country boasts a diverse dairy sector with advanced technology and high-quality standards, allowing it to produce a wide range of cheeses, from soft and spreadable options to aged and specialty varieties. Israeli consumers tend to favor both local and European cheese types, and there is a growing interest in organic and lactose-free alternatives. The market is also supported by strong retail distribution channels and a dynamic food culture that integrates cheese in various daily and gourmet dishes. Israel’s focus on high-value products and innovation gives it a competitive edge in niche segments across the region.

Key Player Analysis

- Arla Foods

- Savencia Fromage & Dairy

- Clover Industries Limited

- Danone

- Hochland SE

- Parmalat S.p.A.

- Al Ain Dairy

- FrieslandCampina

- Ruwag Food Industries

Competitive Analysis

The Middle East cheese market features a competitive landscape characterized by the presence of both global and regional players focusing on innovation, brand expansion, and product diversification to gain market share. Leading companies such as Arla Foods, Savencia Fromage & Dairy, Clover Industries Limited, Danone, Hochland SE, Parmalat S.p.A., Al Ain Dairy, FrieslandCampina, and Ruwag Food Industries play a significant role in shaping the industry dynamics. These key players are leveraging their global expertise to introduce a wide range of cheese products that cater to evolving regional tastes, including processed, cheddar, and specialty cheeses. Strategic partnerships with local distributors, investment in cold chain logistics, and the introduction of health-focused and premium cheese variants have been common approaches among these companies. Many are also localizing production or sourcing to reduce import reliance and improve supply chain efficiency. Additionally, branding and marketing strategies targeting the growing health-conscious and urban consumer base have enabled these players to strengthen their regional footprint.

Recent Developments

- In March 2025, Arla Foods Ingredients partnered with Valley Queen in South Dakota to increase production of Nutrilac® ProteinBoost, a high-protein whey concentrate, to meet growing demand in North America.

- In March 2025, Sargento introduced three innovations—Natural American Cheese, Seasoned Shredded Cheese in collaboration with McCormick, and Shareables snack trays in partnership with Mondelez International.

- In March 2025, Saputo USA debuted its spicy mozzarella cheese at the International Pizza Expo, combining traditional mozzarella with habanero jack for a zesty twist.

- In February 2025, Kraft Heinz emphasized innovation across three platforms—taste elevation, easy-ready meals, and snacking. This includes new product launches like Lunchables Spicy Nachos and value-sized Kraft Mac & Cheese to cater to shifting consumer preferences.

- In November 2024, Lactalis highlighted emerging trends such as premiumization, hot eating cheeses like Président Extra Creamy Brie, and sustainability-focused products like Seriously Spreadable Black Pepper cheese.

Market Concentration & Characteristics

The Middle East cheese market exhibits a moderate to high level of market concentration, with a few dominant players holding a significant share due to their established brand presence, extensive distribution networks, and diverse product offerings. Multinational companies, in collaboration with regional producers, play a key role in supplying both mass-market and premium cheese products across various formats such as processed, spreadable, and specialty cheeses. The market is characterized by a strong reliance on imports, especially in countries with limited domestic dairy production capabilities, while nations like Turkey and Iran maintain a robust local production base. Consumer preferences in the region are shaped by a mix of traditional eating habits and growing acceptance of Western food trends. Urbanization, rising disposable incomes, and expanding retail infrastructure further define the market, supporting the steady growth of packaged and value-added cheese products. Innovation, product quality, and localization remain central to competitiveness in this evolving landscape.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Category, Source, Type, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The Middle East cheese market is expected to witness steady growth driven by urbanization and evolving consumer preferences.

- Demand for premium and artisanal cheeses will rise as consumers seek diverse flavor profiles and quality offerings.

- Processed and spreadable cheese segments will continue to dominate due to convenience and versatility in daily meals.

- Local production is likely to expand as countries invest in dairy infrastructure to reduce import dependency.

- Health-conscious trends will drive innovation in low-fat, organic, and lactose-free cheese products.

- E-commerce and modern retail formats will play a larger role in cheese distribution across urban centers.

- Strategic partnerships between international brands and regional producers will become more common.

- Consumer education and awareness campaigns will influence preferences toward nutritional and functional cheese products.

- Government support for domestic dairy farming may enhance supply chain efficiency and product accessibility.

- Technological advancements in processing and packaging will improve shelf life and product quality.