Market Overview

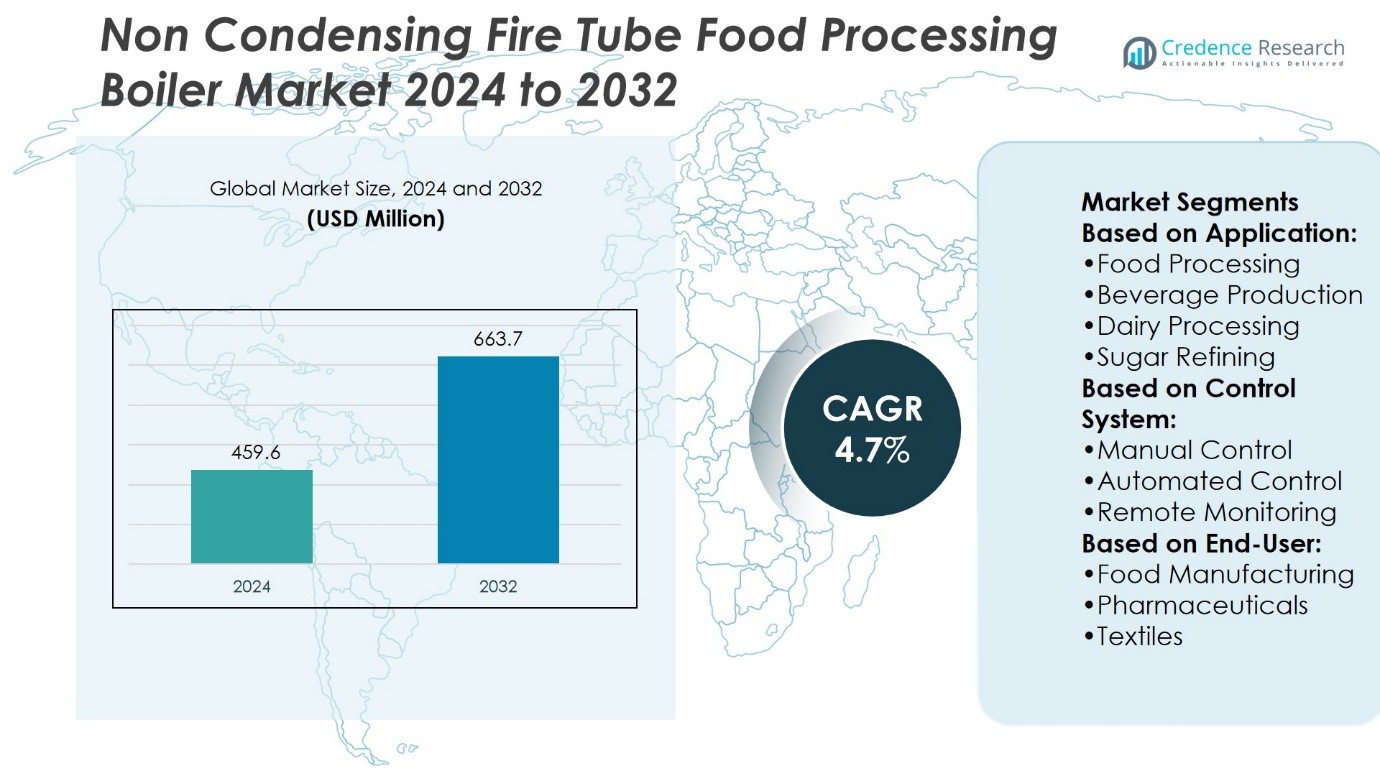

Non-Condensing Fire Tube Food Processing Boiler Market size was valued at USD 459.6 million in 2024 and is anticipated to reach USD 663.7 million by 2032, at a CAGR of 4.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Non-Condensing Fire Tube Food Processing Boiler Market Size 2024 |

USD 459.6 Million |

| Non-Condensing Fire Tube Food Processing Boiler Market, CAGR |

4.7% |

| Non-Condensing Fire Tube Food Processing Boiler Market Size 2032 |

USD 663.7 Million |

The Non-Condensing Fire Tube Food Processing Boiler Market is driven by rising demand for reliable steam generation in food, dairy, beverage, and sugar processing facilities. Industries value these systems for their durability, low maintenance needs, and ability to provide consistent output under variable loads. Regulatory focus on safety and hygiene strengthens adoption, while affordability supports preference among mid-sized processors. The market also shows a trend toward modernization, with manufacturers integrating automated controls, digital monitoring, and hybrid fuel options. Growing food production in emerging economies and replacement of aging infrastructure in developed regions sustain the relevance of non-condensing boilers.

The Non-Condensing Fire Tube Food Processing Boiler Market demonstrates strong regional diversity, with Asia-Pacific leading due to expanding food processing capacity, followed by North America and Europe with established dairy, beverage, and sugar industries. Latin America and the Middle East & Africa show steady growth driven by modernization and rising packaged food demand. Key players shaping the market include Babcock and Wilcox, Bosch Industriekessel, Cleaver-Brooks, Fulton, Forbes Marshall, Cochran, Hoval, Babcock Wanson, Clayton Industries, and BM GreenTech, each competing through durability, automation, and fuel flexibility.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Non-Condensing Fire Tube Food Processing Boiler Market was valued at USD 459.6 million in 2024 and is projected to reach USD 663.7 million by 2032, at a CAGR of 4.7%.

- Demand is driven by reliable steam generation needs in food, dairy, beverage, and sugar processing industries.

- The market shows a trend toward modernization with automated controls, remote monitoring, and hybrid fuel adaptability.

- Competition focuses on durability, cost efficiency, and compliance with strict safety and hygiene standards.

- A key restraint is pressure from energy efficiency regulations and competition from advanced boiler technologies.

- Asia-Pacific leads market share due to expanding food production capacity, while North America and Europe sustain demand through established industries.

- Latin America and the Middle East & Africa record steady growth, with modernization and rising packaged food demand supporting adoption.

Market Drivers

Rising Energy Demand and Dependable Steam Supply Requirements

The Non-Condensing Fire Tube Food Processing Boiler Market is driven by the growing need for reliable steam generation in large-scale food operations. It supports cooking, sterilization, drying, and packaging processes where continuous steam flow is critical. The industry values equipment that maintains steady pressure while handling fluctuating loads. Non-Condensing designs remain relevant because they provide robust performance with simple operation. The demand for dependable output strengthens adoption across dairy, bakery, and beverage facilities. It ensures production lines operate without interruptions, directly influencing product consistency and safety.

- For instance, Cochran’s official specification shows that the ST25 delivers an exact steam output range of 500 to 6 500 kg/hr at feed-and-allowance 100 °C .This numeric capacity underlines its ability to sustain continuous steam flow in demanding operational.

Preference for Durable and Low Maintenance Equipment

Food manufacturers prioritize machinery with long service life and limited maintenance requirements. The Non-Condensing Fire Tube Food Processing Boiler Market benefits from this preference due to the sturdy construction and straightforward design of these systems. The absence of complex condensing components reduces the likelihood of failures. It allows operators to minimize downtime and allocate fewer resources to repair work. Lower maintenance costs support strong adoption in mid-sized plants seeking efficiency. The proven durability of these boilers builds trust among food processing operators worldwide.

- For instance, Fulton’s VSRT-60 model generates a precise steam output of 2,070 lb/hr at feed-and-allowance 212 °F, driven by a fuel input of 2,392 MBH and equipped with a turndown ratio of 10:1, as specified in company documentation.

Compliance with Safety Regulations and Industry Standards

Stringent safety regulations in food processing environments encourage the use of equipment with reliable operating features. The Non-Condensing Fire Tube Food Processing Boiler Market responds with boilers designed to meet pressure vessel codes and hygiene requirements. Automatic control systems and integrated safety valves help maintain compliance. It reassures operators of stable performance under demanding conditions. Certification by international standards bodies increases acceptance among global buyers. The ability to pass safety audits strengthens the position of these boilers in regulated environments.

Cost Efficiency and Investment Practicality for Manufacturers

Food processors evaluate capital investments based on operating efficiency and long-term returns. The Non-Condensing Fire Tube Food Processing Boiler Market addresses this by offering systems with favorable cost-to-performance ratios. Energy efficiency may be lower than condensing models, but upfront affordability offsets this limitation. It remains an attractive option for facilities where initial investment budgets are restricted. Simple installation and lower water treatment needs also contribute to economic appeal. The balance between affordability, durability, and steady steam supply ensures continuous demand in diverse food processing segments.

Market Trends

Growing Modernization of Food Processing Facilities

The Non-Condensing Fire Tube Food Processing Boiler Market is influenced by the modernization of production plants. Food processors are upgrading legacy systems to improve efficiency and reliability. It supports integration with automated lines that require stable steam supply. Manufacturers focus on equipment that aligns with Industry 4.0 standards in plant operations. Control systems with digital monitoring functions enhance visibility of boiler performance. The trend creates consistent demand for non-condensing models with proven operational stability.

- For instance, Babcock Wanson’s BWR fire-tube models deliver exact steam outputs ranging from 10 000 kg/h up to 30 000 kg/h (at 15 bar and feedwater at 105 °C), with corresponding thermal power outputs from 6 545 kW to 17 685 kW.

Rising Focus on Sustainable Energy Practices

Food processors are adopting strategies that reduce energy use and emissions. The Non-Condensing Fire Tube Food Processing Boiler Market adapts with designs that improve fuel-to-steam efficiency while maintaining durability. It encourages the use of natural gas and bio-based fuels in place of heavy oil. Operators seek solutions that align with corporate sustainability goals. Small improvements in combustion efficiency are emphasized by manufacturers. This trend supports the role of non-condensing boilers where compliance and cost savings align.

- For instance, Bosch’s electric steam boiler ELSB produces a clean steam output between 350 and 7,500 kg/h, with a proven operational efficiency of up to 99.6%, as confirmed by company product documentation.

Increasing Customization for Industry-Specific Needs

Equipment providers are tailoring products to meet unique processing requirements. The Non-Condensing Fire Tube Food Processing Boiler Market reflects this through customized designs in capacity, layout, and fuel adaptability. It enables food processors to select boilers aligned with space constraints and production volumes. Compact footprints allow installations in facilities with limited room. The rise of specialty foods and regional producers drives demand for flexible systems. Customization enhances the appeal of traditional non-condensing units in competitive environments.

Integration of Advanced Monitoring and Control Systems

Manufacturers are embedding smart control systems to improve operational oversight. The Non-Condensing Fire Tube Food Processing Boiler Market incorporates features such as automated start-up, flame detection, and fuel monitoring. It strengthens operator safety and reduces manual oversight. Remote connectivity and predictive maintenance functions are becoming standard offerings. These systems extend equipment life and reduce unexpected downtime. The emphasis on digital enhancements positions non-condensing boilers as adaptable solutions in evolving food production lines.

Market Challenges Analysis

Rising Pressure from Energy Efficiency Regulations

The Non-Condensing Fire Tube Food Processing Boiler Market faces growing scrutiny due to evolving efficiency standards. Governments and regulatory agencies are mandating reductions in fuel consumption and emissions. It challenges manufacturers to upgrade traditional designs that typically offer lower efficiency than condensing models. Food processors operating in regions with strict compliance frameworks must balance affordability with regulatory requirements. Upgrades or retrofits increase costs for operators, reducing the appeal of older units. The challenge lies in sustaining competitiveness while meeting mandatory environmental benchmarks.

Competition from Alternative Boiler Technologies

The Non-Condensing Fire Tube Food Processing Boiler Market contends with direct competition from condensing and water tube systems. It creates pressure on traditional fire tube units, which often struggle to match the thermal efficiency and advanced features of newer technologies. Condensing systems attract buyers through higher energy savings over long operational cycles. Water tube designs also appeal to large-scale facilities due to faster steam generation. The need for differentiation becomes critical for suppliers of non-condensing units. Limited innovation in design intensifies the challenge of retaining share in a competitive equipment market.

Market Opportunities

Expansion Across Emerging Food Processing Regions

The Non-Condensing Fire Tube Food Processing Boiler Market holds growth potential in regions where food manufacturing capacity is expanding. Rapid urbanization and dietary shifts are increasing demand for packaged and processed food in Asia-Pacific, Latin America, and parts of Africa. It creates opportunities for suppliers to deliver cost-effective and durable steam generation systems. Smaller and mid-sized processors often prefer non-condensing units for their affordability and ease of maintenance. Local partnerships and distributor networks can strengthen market penetration. The expansion of food clusters in these regions supports wider adoption of proven fire tube technology.

Upgrades with Hybrid and Fuel-Flexible Designs

Opportunities exist for manufacturers to enhance traditional boilers with hybrid and multi-fuel capabilities. The Non-Condensing Fire Tube Food Processing Boiler Market can benefit from designs that integrate natural gas, biomass, or biogas as fuel options. It allows processors to align operations with sustainability targets while maintaining reliable steam supply. Development of retrofittable components and advanced burners can extend the lifecycle of installed units. Operators seeking lower transition costs may adopt upgraded systems rather than shifting to fully condensing technology. The flexibility to adapt fuel sources positions non-condensing fire tube boilers as a viable solution in diverse food processing environments.

Market Segmentation Analysis:

By Application

The Non-Condensing Fire Tube Food Processing Boiler Market finds strong adoption across food and beverage industries. Food processing facilities use these boilers for cooking, steaming, and sterilization, where reliable steam supply ensures product safety. Beverage production plants adopt them to support brewing, distillation, and pasteurization with stable temperature control. Dairy processing operations require consistent heat for pasteurization and drying of milk products, making fire tube designs practical. Sugar refining plants depend on high-capacity steam generation for crystallization and purification. It supports uninterrupted operation in facilities where continuous steam demand is critical.

- For instance, Forbes Marshall’s oil-and-gas fired boilers are available in a broad range of capacities, starting from 300 kg/hr and extending up to 35 tonnes/hr (35,000 kg/hr) for large-scale industrial use.

By Control System

Control system segmentation highlights the transition toward automated solutions. Manual control remains in use among smaller facilities that prioritize low investment and straightforward operation. The Non-Condensing Fire Tube Food Processing Boiler Market demonstrates rising preference for automated systems that offer precise fuel management and improved safety. Automated control units reduce operator workload and help maintain efficiency under variable loads. Remote monitoring capabilities are expanding adoption in modern plants, enabling supervisors to oversee performance and detect faults in real time. It enhances reliability while minimizing risks of unplanned downtime.

- For instance, their Max-Fire Series HRSG boiler handles steam generation from 10,000 up to 500,000 lb/hour, operates at design pressures up to 1,800 psig, and sustains steam temperatures reaching 1,050 °F, according to official product documentation.

By End User

End-user segmentation reflects the versatility of these boilers across multiple industries. Food manufacturing dominates demand, as the sector depends heavily on steam for processing and packaging. The Non-Condensing Fire Tube Food Processing Boiler Market also extends into pharmaceuticals, where controlled steam supports sterilization of equipment and production environments. Textile industries use boilers for dyeing and finishing, requiring stable and continuous steam delivery. Other industries, including chemicals and packaging, adopt fire tube units for their durable construction and manageable operating costs. It remains a cost-effective solution for sectors seeking robust performance with moderate efficiency requirements.

Segments:

Based on Application:

- Food Processing

- Beverage Production

- Dairy Processing

- Sugar Refining

Based on Control System:

- Manual Control

- Automated Control

- Remote Monitoring

Based on End-User:

- Food Manufacturing

- Pharmaceuticals

- Textiles

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America holds around 28% share of the Non-Condensing Fire Tube Food Processing Boiler Market, supported by its advanced food and beverage sector. The United States leads adoption with strong demand from large-scale packaged food and beverage manufacturers. It benefits from strict food safety standards that require consistent steam generation for sterilization and quality assurance. Canada complements growth with investment in dairy and meat processing facilities, where reliable boilers play a key role in operations. Energy efficiency regulations encourage facilities to balance cost with compliance, which sustains demand for durable Non-Condensing systems. The region also demonstrates interest in hybrid systems, but the strong legacy infrastructure ensures continued relevance of fire tube designs.

Europe

Europe accounts for approximately 24% share of the Non-Condensing Fire Tube Food Processing Boiler Market, driven by a well-established food processing and sugar refining industry. Germany, France, and the United Kingdom remain the leading adopters due to advanced dairy, bakery, and confectionery facilities. It benefits from long-standing infrastructure where retrofits and replacements dominate purchasing decisions. The European Union’s strict environmental policies are influencing gradual upgrades, but many facilities still operate Non-Condensing systems for their durability and reliability. Southern Europe demonstrates demand from wine and olive oil production facilities, where stable steam is critical. The presence of major global boiler manufacturers across the region strengthens accessibility to advanced Non-Condensing units tailored for specialized needs.

Asia-Pacific

Asia-Pacific leads with about 32% share of the Non-Condensing Fire Tube Food Processing Boiler Market, supported by rapid industrialization and growth in food processing capacity. China dominates adoption with extensive use across beverage, dairy, and sugar refining plants. India follows with rising investments in food manufacturing clusters driven by urbanization and population growth. Southeast Asia, including Indonesia, Thailand, and Vietnam, demonstrates strong demand for affordable and durable boilers in expanding packaged food and beverage sectors. Japan and South Korea contribute with technologically advanced facilities that still incorporate fire tube boilers for specific production lines. It remains the fastest-growing region due to favorable demographics, increasing food exports, and rising consumption of processed food.

Latin America

Latin America secures nearly 8% share of the Non-Condensing Fire Tube Food Processing Boiler Market, supported by growing investments in food and beverage processing. Brazil leads with sugar refining and beverage production facilities requiring reliable steam supply. Mexico demonstrates demand from bakery and meat processing operations tied to rising exports to North America. Argentina and Chile contribute with adoption in dairy and wine production sectors. It reflects preference for cost-effective solutions that balance performance with investment practicality. Expansion of regional food clusters supported by trade agreements ensures steady demand for robust boiler systems.

Middle East and Africa

The Middle East and Africa together account for around 8% share of the Non-Condensing Fire Tube Food Processing Boiler Market. The Middle East demonstrates demand from large-scale beverage and packaged food facilities in Saudi Arabia and the United Arab Emirates. Africa reflects adoption in emerging dairy and grain processing sectors, especially in South Africa and Nigeria. Limited infrastructure in some areas restricts large-scale deployment, but the market benefits from gradual modernization of food processing facilities. It shows opportunities for suppliers that offer durable, low-maintenance systems suitable for challenging operating environments. Growing population and demand for affordable processed foods sustain market activity in this region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Cochran

- Fulton

- Babcock Wanson

- Bosch Industriekessel

- Forbes Marshall

- Cleaver-Brooks

- BM GreenTech

- Hoval

- Clayton Industries

- Babcock and Wilcox

Competitive Analysis

The competitive landscape of the Non-Condensing Fire Tube Food Processing Boiler Market features including Babcock and Wilcox, Babcock Wanson, BM GreenTech, Bosch Industriekessel, Clayton Industries, Cleaver-Brooks, Cochran, Forbes Marshall, Fulton, and Hoval. The Non-Condensing Fire Tube Food Processing Boiler Market is characterized by strong competition among global and regional manufacturers offering durable steam generation solutions. Companies compete by focusing on product reliability, fuel flexibility, and integration of advanced control systems. Innovation centers on automation, remote monitoring, and hybrid fuel capabilities that improve operational efficiency and reduce downtime. Service networks and after-sales support remain critical differentiators, as food processors prioritize minimal disruption in production lines. Competitive strategies also emphasize compliance with evolving safety and environmental regulations, ensuring systems align with industry standards. The balance between cost efficiency, durability, and technological upgrades defines success in this competitive landscape.

Recent Developments

- In February 2025, Cleaver Brooks launched the EOS 500 Burner Control System, a high-precision parallel-positioning burner control with integrated flame safeguard capabilities on its official site.

- In May 2024, Miura Co acquired Cleaver-Brooks this acquisition will help Miura strengthen its foothold in both the global and commercial industrial boiler markets. Such steps are likely to accelerate Miura’s overseas growth since it is expected that international markets will account for 50% of the firm’s annual revenue, which is double their previous international earnings.

- In February 2024, Miura launched the Miura Care Program, an innovative preventative maintenance initiative developed in collaboration with Hartford Boiler. This program delivers a comprehensive and efficient maintenance experience, ensuring exceptional protection for boiler systems.

- In September 2023, Babcock Wanson successfully completed the installation of a comprehensive steam solution at IRC Cucina’s state-of-the-art centralized kitchen in Trafford Park. The project, powered by the high-performance BWD30 fire tube boiler, is designed to ensure the smooth and efficient operation of cooking processes, delivering consistently superior food quality.

Report Coverage

The research report offers an in-depth analysis based on Application, Control System, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will sustain demand from food, dairy, beverage, and sugar processing facilities.

- It will remain relevant in regions where cost efficiency outweighs high efficiency requirements.

- Manufacturers will invest in automation and digital monitoring to improve reliability.

- Fuel flexibility will gain importance as processors shift toward natural gas and biofuels.

- Emerging economies will drive growth through expansion of packaged food production.

- Replacement of aging infrastructure will create consistent opportunities across mature markets.

- Hybrid systems combining traditional boilers with modern controls will find wider adoption.

- Safety compliance and certifications will continue to influence purchasing decisions.

- Compact and customized designs will see higher demand in mid-sized facilities.

- The market will balance affordability with innovation to stay competitive against alternative boiler technologies.