Market Overview:

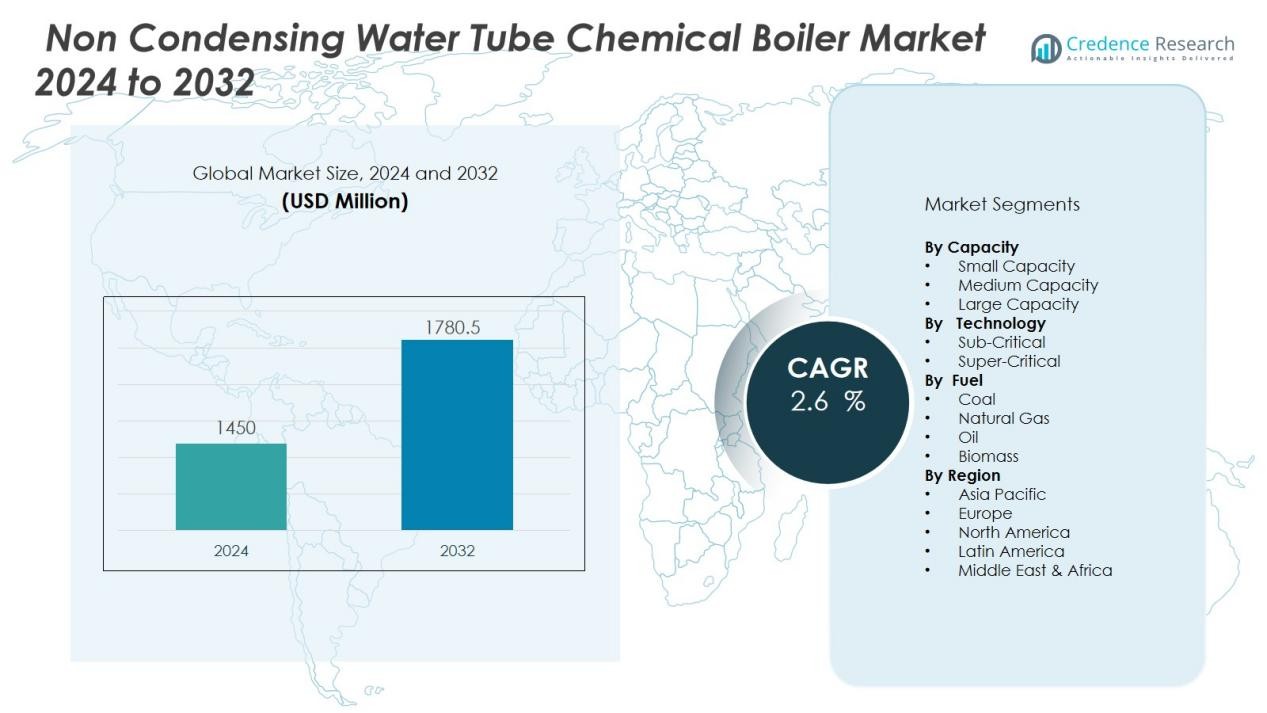

The Non Condensing Water Tube Chemical Boiler Market size was valued at USD 1450 million in 2024 and is anticipated to reach USD 1780.5 million by 2032, at a CAGR of 2.6 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Non Condensing Water Tube Chemical Boiler Market Size 2024 |

USD 1450 Million |

| Non Condensing Water Tube Chemical Boiler Market, CAGR |

2.6 % |

| Non Condensing Water Tube Chemical Boiler Market Size 2032 |

USD 1780.5 Million |

Key drivers include the growing need for reliable steam generation in chemical plants, rising industrialization, and stricter energy efficiency standards. These boilers are favored for their durability, ability to withstand harsh chemicals, and lower maintenance requirements compared to alternative systems. Expanding use in large-scale production facilities, coupled with demand for stable thermal energy output, further accelerates adoption. Additionally, the replacement of aging boiler infrastructure in mature markets is fueling sustained growth opportunities.

Regionally, Asia-Pacific leads the non-condensing water tube chemical boiler market, driven by rapid industrial expansion in China, India, and Southeast Asia. North America and Europe maintain significant shares due to modernization of existing chemical facilities and regulatory pressure for energy efficiency. Meanwhile, Latin America and the Middle East & Africa are emerging as growth regions, supported by increasing industrial investments and infrastructure development.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The non condensing water tube chemical boiler market was valued at USD 1450 million in 2024 and is projected to reach USD 1780.5 million by 2032, at a CAGR of 2.6%.

- Rising industrial demand for high-capacity boilers is a key driver, as chemical plants require consistent steam generation for large-scale production.

- Replacement of aging boiler infrastructure in mature markets is fueling adoption of modern, durable, and efficient systems.

- Regulatory pressure on energy efficiency and emissions is encouraging industries to shift toward advanced boiler solutions that reduce operating costs.

- High initial investment and maintenance costs remain significant challenges, limiting adoption among smaller chemical plants.

- Asia-Pacific led with 42% share in 2024, followed by North America with 28% and Europe with 20%, while Latin America and Middle East & Africa collectively accounted for 10%.

- Expansion of chemical production facilities in emerging economies such as India, China, Saudi Arabia, and Brazil continues to create long-term growth opportunities.

Market Drivers:

Rising Industrial Demand for High-Capacity Boilers:

The non condensing water tube chemical boiler market is gaining momentum due to growing industrial activity. Chemical plants require consistent and high-capacity steam generation for production processes. These boilers offer durability and efficiency, making them suitable for large-scale operations. It supports continuous plant performance, ensuring productivity and operational stability.

Increasing Replacement of Aging Boiler Infrastructure:

A major driver of the non condensing water tube chemical boiler market is the replacement of outdated systems. Many chemical plants in mature markets operate with aging boiler units that lack efficiency. Companies are investing in modern, robust boilers to reduce downtime and improve energy utilization. It creates steady demand for water tube designs that meet long-term operational needs.

- For instance, in 2023, Sabic integrated new water tube boilers at its Al Jubail complex, replacing aging equipment and ensuring stable production capacity with 220 tons of process steam per hour through Hitachi-designed units.

Regulatory Pressure and Focus on Energy Efficiency:

Stricter industry standards are pushing companies to adopt efficient thermal systems. The non condensing water tube chemical boiler market benefits from this trend as industries seek equipment that balances cost and compliance. Energy efficiency remains a critical factor in reducing operating expenses and maintaining competitiveness. It encourages chemical manufacturers to adopt advanced boiler solutions.

- For instance, Babcock & Wilcox reported that its O-Type water-tube industrial boilers cut fuel consumption by 150,000 MMBtu annually at a U.S. chemical plant through optimized combustion technology, directly aligning with stringent energy efficiency mandates.

Expansion of Chemical Production Facilities in Emerging Regions:

The non condensing water tube chemical boiler market is also driven by regional industrial expansion. Countries in Asia-Pacific and the Middle East are investing heavily in new chemical production plants. These facilities require reliable boilers capable of handling high volumes under demanding conditions. It strengthens market opportunities in fast-growing economies where industrialization is accelerating.

Market Trends:

Growing Focus on Modernization and Technological Integration:

The non condensing water tube chemical boiler market is witnessing a trend of modernization across established industries. Companies are investing in advanced designs that improve durability, heat transfer efficiency, and operational safety. Integration of automation and monitoring systems is becoming common, allowing better control over fuel usage and maintenance schedules. It supports higher productivity while reducing unplanned downtime in chemical processing facilities. Manufacturers are also offering customizable solutions to meet diverse plant requirements, which strengthens their competitiveness. This trend highlights a shift toward smarter and more adaptable boiler systems tailored for complex chemical operations.

- For instance, Cleaver-Brooks has integrated its Hawk 4000 advanced boiler management control, which can monitor over 50 operational parameters simultaneously, enabling precise fuel-to-air ratio adjustments to ensure consistent efficiency in chemical plant operations.

Rising Demand from Emerging Economies and Expanding Production Capacities:

The non condensing water tube chemical boiler market is also experiencing strong traction in emerging economies, driven by large-scale investments in new chemical plants. Rapid industrialization in Asia-Pacific and the Middle East is creating significant opportunities for suppliers. It aligns with governments promoting domestic chemical manufacturing to reduce reliance on imports. Expansion of production facilities demands reliable and high-capacity boiler systems, which reinforces the adoption of water tube designs. Global suppliers are forming partnerships and joint ventures in these regions to strengthen distribution networks and service support. This trend reflects a clear focus on expanding market presence in fast-growing industrial hubs.

- For instance, Babcock & Wilcox recently supplied its SPG water-tube boilers to a chemical facility in India, with each unit designed to generate up to 650 tons of steam per hour, ensuring uninterrupted high-volume industrial operations.

Market Challenges Analysis:

High Initial Investment and Maintenance Costs:

The non condensing water tube chemical boiler market faces challenges due to significant upfront capital requirements. Installation of these boilers demands heavy investment in equipment, piping, and supportive infrastructure. Smaller chemical plants often hesitate to adopt such systems because of budget limitations. It also involves ongoing maintenance expenses to ensure efficiency and safety, which further increases operational costs. Long payback periods can discourage investment, especially in markets with limited financial resources. This factor creates a barrier for wider adoption across developing regions.

Stringent Regulations and Availability of Alternatives:

The non condensing water tube chemical boiler market is also challenged by strict environmental regulations and growing competition from alternative technologies. Governments are tightening emission standards, pushing industries to seek cleaner and more efficient solutions. It makes non-condensing systems less favorable compared to condensing or hybrid designs. The presence of alternative energy systems, including waste heat recovery units and renewable-powered boilers, creates substitution risks. Compliance costs and adaptation to regulatory frameworks can limit market expansion. This challenge forces manufacturers to innovate and develop competitive features to retain industry relevance.

Market Opportunities:

Expansion of Industrial Capacity in Emerging Markets:

The non condensing water tube chemical boiler market presents strong opportunities through industrial expansion in Asia-Pacific, the Middle East, and Africa. Rapid growth of chemical manufacturing in these regions is creating consistent demand for reliable high-capacity boilers. Governments are investing in industrial corridors and special economic zones, which increases the need for advanced thermal energy systems. It strengthens prospects for global suppliers to establish partnerships and expand distribution networks. Local production support and after-sales services can further enhance competitiveness in these markets. This opportunity is especially strong where infrastructure and chemical production are scaling at a fast pace.

Adoption of Advanced Designs and Customization:

The non condensing water tube chemical boiler market is also positioned for growth through innovation and product customization. Industries are seeking systems with better fuel flexibility, automation, and digital monitoring features. It creates scope for manufacturers to design solutions that reduce operational downtime and improve efficiency. Customizable boilers tailored to specific plant processes provide value-added advantages to chemical producers. Growing interest in integrating automation with predictive maintenance tools expands demand for modern boiler systems. This opportunity allows suppliers to differentiate their offerings and secure long-term contracts with industrial clients.

Market Segmentation Analysis:

By Capacity:

The non condensing water tube chemical boiler market is segmented by capacity into small, medium, and large units. Large-capacity boilers dominate due to their ability to support high-volume chemical production. Medium units are gaining traction in mid-scale facilities where balanced efficiency and cost are priorities. It continues to find demand across diverse plant sizes, offering flexibility for both new installations and replacements. Small-capacity boilers hold a niche role in specialized applications with limited production requirements.

- For instance, Doosan Heavy Industries supplied two 800 MW supercritical once-through boilers to India’s Kudgi Power Plant, delivering 2,550 tons of high-pressure steam per hour.

By Technology:

By technology, the non condensing water tube chemical boiler market is divided into sub-critical and super-critical designs. Sub-critical technology maintains a strong presence due to its proven reliability in chemical industries. Super-critical designs are expanding as industries adopt higher efficiency systems that optimize energy usage. It provides an opportunity for manufacturers to meet varying operational requirements through advanced engineering. The demand for flexible and durable technology solutions strengthens the market outlook across industrial segments.

- For instance, Siemens Energy’s SST-800 super-critical steam turbine models are integrated with boilers capable of achieving steam pressures above 3,500 psi, enabling industries to enhance thermal efficiency significantly.

By Fuel:

The non condensing water tube chemical boiler market by fuel includes coal, natural gas, oil, and biomass. Natural gas-based boilers lead adoption due to lower emissions and operational efficiency. Coal-fired units remain relevant in regions with cost-sensitive industries and abundant coal supply. It reflects diverse regional energy policies and availability of resources. Biomass and oil-fired boilers are gaining space where sustainability initiatives and energy diversification are key priorities.

Segmentations:

By Capacity:

- Small Capacity

- Medium Capacity

- Large Capacity

By Technology:

- Sub-Critical

- Super-Critical

By Fuel:

- Coal

- Natural Gas

- Oil

- Biomass

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Asia-Pacific:

Asia-Pacific held 42% market share in the non condensing water tube chemical boiler market in 2024, leading globally. China and India drive demand with rapid chemical industry growth and investments in large-scale plants. Government initiatives promoting industrial self-reliance strengthen adoption of high-capacity boiler systems. It benefits from rising infrastructure spending and expansion of petrochemical complexes. Southeast Asian countries are also increasing their production capacity, creating steady demand for boilers. Strong manufacturing bases and cost-effective production enhance regional competitiveness in this market.

North America and Europe:

North America accounted for 28% market share in the non condensing water tube chemical boiler market in 2024, supported by modernization of industrial infrastructure. The United States leads regional demand due to a mature chemical sector and replacement of outdated boiler systems. Europe followed with 20% share, driven by regulatory compliance and focus on energy-efficient operations. It continues to benefit from investment in high-performance boilers despite stricter emission norms. Both regions are advancing toward digital integration and automation in boiler systems. Strong service networks also enhance adoption in established markets.

Latin America and Middle East & Africa:

Latin America and the Middle East & Africa collectively captured 10% market share in the non condensing water tube chemical boiler market in 2024. Brazil and Mexico are driving Latin America with steady growth in chemical production and industrialization. In the Middle East, Saudi Arabia and the UAE lead with investments in petrochemical and refining projects. It creates demand for reliable boiler systems capable of handling large-scale operations. Africa shows potential with growing industrial bases in South Africa and Nigeria. These emerging regions offer long-term opportunities as governments expand industrial capacity.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Alfa Laval

- Babcock and Wilcox

- Ariston Holding

- Babcock Wanson

- Bosch Industriekessel

- Bryan Steam

- BM GreenTech

- Clayton Industries

- Cochran

- Cleaver-Brooks

- Hurst Boiler & Welding

- Forbes Marshall

- Miura America

Competitive Analysis:

The non condensing water tube chemical boiler market is highly competitive, with global and regional players focusing on efficiency and innovation. Key companies include Alfa Laval, Babcock and Wilcox, Ariston Holding, Babcock Wanson, Bosch Industriekessel, Bryan Steam, BM GreenTech, Clayton Industries, and Cochran. Market participants emphasize product reliability, fuel flexibility, and compliance with energy standards to strengthen their presence. It remains driven by strategic investments in R&D, aiming to deliver boilers that meet demanding chemical industry requirements. Partnerships, service expansions, and customization strategies help players secure long-term contracts with industrial clients. Competition is also influenced by regional distributors and after-sales service networks that add value to end users. The market is expected to see stronger rivalry as emerging economies expand their chemical manufacturing base and global suppliers focus on capturing this growth.

Recent Developments:

- In August 2025, XCF Global announced the use of Alfa Laval technology to enhance pretreatment capabilities at its new RISE Reno facility.

- In July 2025, Babcock & Wilcox completed the sale of Diamond Power International to Andritz AG for $177 million.

- In June 2025, Ariston Group acquired an 80% stake in Z.R.E., enhancing its Components Division with new industrial electric heating solutions.

Report Coverage:

The research report offers an in-depth analysis based on Capacity, Technology, Fuel and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The non condensing water tube chemical boiler market will see steady demand from large-scale chemical plants.

- Expansion of petrochemical and specialty chemical facilities will drive consistent adoption of high-capacity boilers.

- Manufacturers will focus on offering customized designs with fuel flexibility and advanced automation features.

- Integration of digital monitoring and predictive maintenance will improve operational efficiency and system reliability.

- Replacement of outdated boilers in mature markets will create recurring opportunities for suppliers.

- Asia-Pacific will remain the dominant region with continued industrial expansion in China, India, and Southeast Asia.

- North America and Europe will maintain stable demand, supported by modernization projects and regulatory compliance.

- Emerging markets in Latin America, the Middle East, and Africa will provide new avenues for growth.

- Collaboration between global suppliers and regional distributors will enhance service networks and long-term partnerships.

- Sustainability concerns will encourage innovation in energy efficiency and fuel optimization within boiler systems.