| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| North America Data Center Containment Market Size 2024 |

USD 1,495.61 Million |

| North America Data Center Containment Market, CAGR |

11.06% |

| North America Data Center Containment Market Size 2032 |

USD 3,462.17 Million |

Market Overview

The North America Data Center Containment Market is projected to grow from USD 1,495.61 million in 2024 to an estimated USD 3,462.17 million by 2032, with a compound annual growth rate (CAGR) of 11.06% from 2025 to 2032. This significant growth reflects the increasing demand for efficient cooling solutions, energy management, and optimized data center operations.

Several key drivers are propelling the growth of the North America Data Center Containment Market. The increasing adoption of cloud computing, big data analytics, and the Internet of Things (IoT) has led to higher data center traffic, creating a need for better cooling solutions and space utilization. Additionally, rising energy costs, growing awareness about environmental sustainability, and the push for energy-efficient data centers are further contributing to the demand for containment systems. The ongoing trend towards modular and scalable data center designs is also supporting the market’s expansion.

Geographically, North America holds a dominant position in the data center containment market, driven by the presence of major data center operators and technological advancements in the region. The United States, in particular, is the largest contributor to the market due to its advanced infrastructure and high adoption of cloud services. Key players in the market include Schneider Electric, Vertiv Group, Eaton Corporation, and Rittal, who are continuously innovating to meet the growing demands for data center containment solutions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The North America Data Center Containment Market is projected to grow significantly from USD 1,495.61 million in 2024 to USD 3,462.17 million by 2032, with a CAGR of 11.06% from 2025 to 2032.

- Increasing adoption of cloud computing, IoT, and big data analytics is driving higher data center traffic, creating demand for more efficient containment systems.

- Rising energy costs and the need for sustainable data center operations are propelling the adoption of energy-efficient cooling solutions, further supporting market growth.

- High initial investment and implementation costs associated with advanced containment solutions can be a barrier, particularly for smaller data centers.

- Advancements in modular, scalable, and liquid cooling containment solutions are shaping the market and providing efficient alternatives to traditional cooling methods.

- The United States leads the market with significant investments in data center infrastructure, while Canada is witnessing growth due to favorable conditions and increasing adoption of green technologies.

- Companies such as Schneider Electric, Vertiv Group, Eaton Corporation, and Rittal are dominant players, continuously innovating to meet the rising demand for advanced containment solutions.

Market Drivers

Growing Awareness of Environmental Sustainability

Environmental sustainability has become a critical issue in industries worldwide, and the data center sector is no exception. With data centers accounting for a substantial portion of global energy consumption and carbon emissions, there is a growing emphasis on adopting green technologies and practices to reduce their environmental impact. Data center operators are under increasing pressure to meet environmental regulations and minimize their carbon footprint. Containment solutions help improve the efficiency of air handling within a data center, leading to reduced energy consumption, lower carbon emissions, and a more sustainable operation. For instance, cold aisle containment systems direct cold air directly to equipment while isolating hot exhaust air, resulting in lower cooling demands and reduced energy use. In addition to the environmental benefits, this approach also helps data centers achieve their sustainability goals by adhering to green building certifications, such as LEED (Leadership in Energy and Environmental Design). As environmental awareness rises among businesses, regulatory bodies, and consumers, the demand for energy-efficient and sustainable data center solutions, including containment systems, is expected to increase, contributing to the market’s growth.

Technological Advancements in Data Center Infrastructure

Technological advancements in data center infrastructure are also playing a significant role in driving the North America Data Center Containment Market. The evolution of IT infrastructure, including the adoption of high-density servers, hyper-converged infrastructure, and edge computing, has led to the need for more sophisticated containment systems. With data centers now housing more advanced and power-hungry equipment, the traditional methods of managing airflow and cooling are no longer sufficient. Newer containment solutions are designed to handle higher heat loads, improve space utilization, and enhance overall cooling efficiency. Innovations such as the integration of smart monitoring systems with containment solutions allow data center operators to gain real-time insights into temperature fluctuations, airflow distribution, and energy consumption. These insights enable more precise management of the cooling process and further reduce energy waste. Additionally, the increasing prevalence of modular data centers and the shift towards edge computing, where data processing occurs closer to the data source, require containment systems that are scalable and adaptable to rapidly changing infrastructure needs. The ongoing technological developments within the data center sector are thus driving the adoption of innovative containment solutions that meet the new demands of high-performance, flexible, and efficient data centers.

Increasing Demand for Energy-Efficient Cooling Solutions

One of the primary drivers for the growth of the North America Data Center Containment Market is the increasing demand for energy-efficient cooling solutions. Data centers consume vast amounts of energy, primarily for cooling purposes, as they house high-performance servers and other equipment that generate significant heat. Traditional cooling systems are becoming less efficient in handling the rising power demands of modern data centers, leading to inefficiencies and higher operational costs. For instance, companies like Güntner have implemented innovative cooling technologies such as high-density dry coolers and immersion cooling to address these challenges. These solutions not only enhance energy efficiency but also reduce water consumption and environmental impact. Containment strategies, such as hot and cold aisle containment, further optimize airflow and lower energy consumption while maintaining optimal operating temperatures. By reducing reliance on traditional cooling methods, data center operators can cut down on energy usage, which not only helps reduce operational costs but also addresses growing concerns over environmental sustainability. As energy prices continue to rise and regulatory frameworks around energy consumption become more stringent, energy-efficient containment solutions are expected to play an even more significant role in the market.

Rise in Cloud Computing and Data-Driven Applications

The increasing reliance on cloud computing and data-driven applications has significantly accelerated the demand for data center space and processing power, directly influencing the North America Data Center Containment Market. As more businesses migrate their operations to the cloud, the need for scalable, efficient, and high-performance data centers grows. For instance, the rise of hybrid cloud models and artificial intelligence (AI)-driven applications has prompted enterprises to adopt advanced containment solutions to manage high-density IT setups effectively. These solutions are critical in maintaining performance while managing the heat generated by intensive workloads such as AI training and big data analytics. Moreover, as organizations implement big data analytics, AI, and machine learning (ML), these data-intensive applications require high-performing data centers that are efficiently cooled and maintained. Efficient containment systems not only enhance operational efficiency but also improve uptime by reducing thermal risks in increasingly complex environments. This growing demand for robust data processing infrastructure underscores the importance of advanced containment strategies in supporting modern digital transformation.

Market Trends

Focus on Modular and Scalable Containment Solutions

Another significant trend in the North America Data Center Containment Market is the growing focus on modular and scalable containment solutions. The demand for flexible and scalable infrastructure is increasing as businesses seek to future-proof their data centers while maintaining cost-effectiveness. Modular containment systems offer the advantage of being easily scalable to accommodate growth in IT infrastructure without requiring major modifications or the construction of new data center spaces. These systems can be tailored to specific cooling requirements and adjusted to handle changing heat loads as data center operations expand or evolve. For example, containerized or modular data centers, which can be quickly deployed and customized for different cooling needs, are becoming increasingly popular in the North American market. These systems are ideal for enterprises that need to scale their data center operations rapidly to meet the growing demands of digital transformation, cloud services, and data-driven applications. Additionally, modular containment solutions are often more energy-efficient and easier to maintain, allowing operators to streamline their operations and reduce overall operational costs. The flexibility and scalability of modular containment systems make them an attractive option for both hyperscale data centers and smaller enterprises that require efficient cooling and space utilization.

Sustainability and Green Data Center Initiatives

Sustainability continues to be a key driver in the evolution of the North America Data Center Containment Market, with an increasing emphasis on green data center initiatives. The environmental impact of data centers, particularly regarding their high energy consumption and carbon footprint, has prompted operators to seek solutions that can help them reduce their environmental impact. Data center containment solutions that improve cooling efficiency, reduce energy consumption, and lower carbon emissions are now in high demand. Moreover, the implementation of energy-efficient containment strategies, such as hot and cold aisle containment, combined with renewable energy sources like wind and solar power, is becoming more common in North America. Many leading data center operators are actively pursuing certifications such as LEED (Leadership in Energy and Environmental Design) and achieving net-zero energy targets by integrating energy-saving technologies into their operations. These sustainability efforts are not only driven by regulatory requirements but also by corporate social responsibility (CSR) initiatives and customer expectations for eco-friendly practices. As more businesses and consumers prioritize sustainability, data center operators are increasingly investing in technologies that align with environmental goals, further boosting the demand for energy-efficient and sustainable containment solutions. Additionally, innovations such as using recycled materials for containment systems and adopting advanced cooling technologies like evaporative cooling are helping operators reduce their environmental footprint while maintaining optimal data center performance.

Integration of Smart Monitoring and IoT-Enabled Containment Systems

One of the most prominent trends in the North America Data Center Containment Market is the integration of smart monitoring and Internet of Things (IoT)-enabled systems. Data center operators are increasingly adopting advanced technologies such as IoT sensors, AI-driven analytics, and real-time monitoring systems to enhance the efficiency of their containment solutions. These smart systems allow operators to gain granular insights into key operational metrics, such as temperature, humidity, airflow patterns, and energy consumption, enabling proactive management of cooling systems. For instance, companies have reported significant reductions in equipment failures and downtime by implementing IoT-based monitoring systems that enable predictive maintenance. By leveraging IoT-enabled solutions, operators can identify inefficiencies and performance issues before they lead to equipment failure or downtime. Additionally, predictive analytics can be employed to optimize energy usage and reduce cooling costs by adjusting airflow and temperature settings in real-time. This integration of smart technologies ensures more precise control over the data center environment, improving operational efficiency, lowering energy costs, and extending the lifespan of IT equipment.

Adoption of Liquid Cooling and Hybrid Containment Solutions

With the continuous increase in the power and density of IT equipment, traditional air-based cooling systems are reaching their limits in terms of efficiency. As a result, there has been a growing trend toward the adoption of liquid cooling and hybrid containment solutions in North America’s data centers. Liquid cooling systems, which use water or specialized coolants to absorb and transfer heat from electronic components, are proving to be much more efficient than traditional air cooling in high-density environments. These systems offer significantly higher heat removal capabilities and are better suited for handling the growing power demands of modern servers and processors. For instance, data centers that have transitioned to liquid cooling have seen substantial improvements in thermal management and energy efficiency, allowing them to operate at higher densities without compromising performance. In hybrid containment systems, liquid cooling is integrated with traditional air-based containment, creating a more efficient and scalable solution for data centers. This approach not only enhances cooling performance but also reduces energy consumption and carbon emissions. As power consumption and heat generation in data centers continue to rise, hybrid and liquid cooling solutions will be critical for ensuring that containment systems remain effective and energy-efficient.

Market Challenges

High Initial Investment and Implementation Costs

One of the major challenges facing the North America Data Center Containment Market is the high initial investment required for the installation of advanced containment systems. Data center operators often face significant capital expenditures when upgrading or installing containment solutions, particularly those involving specialized technologies such as liquid cooling or modular systems. For instance, the adoption of modular containment systems has gained traction due to their scalability and cost-effectiveness, but their implementation still demands substantial upfront costs and expertise. While these solutions offer long-term operational savings by improving energy efficiency and cooling performance, the upfront costs can be a barrier for smaller businesses or those with limited budgets. Additionally, the complexity of implementing these systems requires specialized knowledge and skills, which can lead to additional expenses in terms of labor and training. As a result, the cost-effectiveness of containment solutions may not always be immediately apparent, and some operators may hesitate to invest in these systems without a clear understanding of the long-term financial benefits. Overcoming this challenge requires careful cost-benefit analysis and planning to ensure that operators can achieve a return on investment (ROI) within a reasonable timeframe.

Evolving Technological Demands and Compatibility Issues

As data centers continue to evolve with advancements in IT infrastructure, such as the increasing adoption of high-density servers, edge computing, and artificial intelligence (AI), containment solutions must keep pace with these technological changes. The rapid pace of innovation in data center technologies means that containment systems must be adaptable and scalable to accommodate new equipment and growing operational demands. Compatibility issues between legacy infrastructure and newer containment systems can pose a significant challenge, as upgrading to more efficient solutions often requires integrating new containment technologies with existing data center designs. This can result in operational disruptions and increased costs during the transition period. Furthermore, the integration of advanced technologies like IoT sensors and AI-driven systems into containment solutions adds another layer of complexity, requiring data center operators to manage both the physical and digital infrastructure effectively. Addressing these compatibility challenges and ensuring that containment solutions can evolve with the changing needs of data centers is crucial for maintaining operational efficiency and meeting future demands.

Market Opportunities

Growing Demand for Edge Data Centers and Distributed Computing

The increasing adoption of edge computing in North America presents a significant opportunity for the data center containment market. As businesses and organizations seek to reduce latency and improve the performance of applications, there is a growing need for localized, smaller data centers at the edge of networks. Edge data centers typically require high-performance, energy-efficient containment solutions to optimize space and cooling in environments with limited physical infrastructure. These data centers, often located closer to end-users, necessitate scalable containment systems that can handle high-density computing while ensuring energy efficiency and cost-effectiveness. The trend toward edge computing in sectors like IoT, 5G, and autonomous vehicles creates a substantial demand for compact and efficient containment systems. Data center operators can capitalize on this trend by offering customizable, modular containment solutions tailored to meet the specific needs of edge data centers, thereby tapping into a growing market segment.

Increasing Investment in Hyperscale Data Centers

The rise of hyperscale data centers, driven by the expansion of cloud service providers, is another key market opportunity for data center containment solutions. Hyperscale data centers, which handle massive amounts of data processing and storage for cloud services, require high-density, efficient cooling systems to manage the heat generated by densely packed IT equipment. These data centers are typically built to scale rapidly, and containment solutions play a vital role in optimizing airflow, reducing energy consumption, and improving the overall efficiency of cooling systems. As cloud adoption continues to grow across various industries, there will be an increased demand for containment systems that can support the needs of hyperscale facilities. This offers an opportunity for containment solution providers to develop innovative, scalable, and energy-efficient systems to serve the rapidly expanding hyperscale data center market in North America.

Market Segmentation Analysis

By Containment Type

Hot aisle containment remains one of the most widely adopted containment strategies. It isolates hot air generated by server racks and directs it toward the air conditioning units, enhancing cooling efficiency. As data centers grow in size and complexity, the need for effective heat management continues to drive the demand for HAC systems. Cold aisle containment is another key segment, where cold air is directed to the intake side of servers. This type of containment solution prevents hot and cold air from mixing, thereby enhancing the cooling efficiency and reducing energy consumption. With the growing need for cooling efficiency, CAC remains a popular choice for data center operators. Rack-based chimney containment solutions are gaining popularity due to their ability to target specific racks with focused airflow management. This system works by creating a chimney effect that isolates hot air, ensuring that it doesn’t mix with the cold air intake. This containment solution is particularly useful for high-density data centers. In-row cooling containment systems have emerged as a highly efficient solution for managing heat loads in high-density environments. This type of containment works by placing cooling units between server racks, allowing for better localized cooling. It is ideal for data centers that require precise temperature control and energy efficiency.

By Data Center Type

These large-scale facilities serve massive cloud services, and as they scale, the demand for efficient containment solutions increases. Hyperscale data centers often require sophisticated containment systems to manage high power loads and ensure operational efficiency. Enterprise data centers are typically owned and operated by individual organizations for internal use. These data centers are adopting containment solutions to reduce energy costs and improve operational efficiency, driving significant growth in this segment. The growth of cloud computing services, driven by companies like Amazon, Google, and Microsoft, has resulted in increased demand for energy-efficient data center solutions. These facilities require high-performance containment systems to handle the high-density equipment used for processing vast amounts of data. Colocation centers, where multiple organizations share data center space, also contribute to the demand for advanced containment solutions. These data centers require scalable containment systems to support diverse customer requirements for cooling, space, and power efficiency. Other smaller segments of the data center market, including edge computing centers, also require containment solutions, albeit on a smaller scale.

Segments

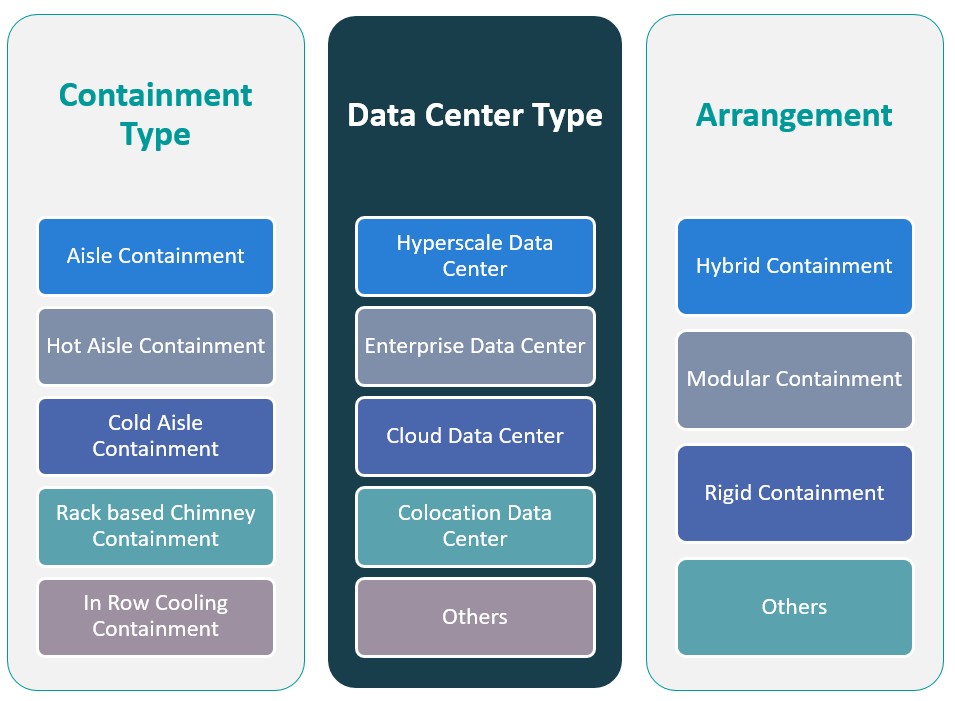

Based on Containment Type

- Aisle Containment

- Hot Aisle Containment

- Cold Aisle Containment

- Rack based Chimney Containment

- In Row Cooling Containment

Based on Data Center Type

- Hyperscale Data Center

- Enterprise Data Center

- Cloud Data Center

- Colocation Data Center

- Others

Based on Arrangement

- Hybrid Containment

- Modular Containment

- Rigid Containment

- Others

Based on Region

Regional Analysis

United States (85%)

The United States is the epicenter of the data center containment market in North America. It hosts a large number of hyperscale data centers, cloud service providers, and colocation facilities. The growth in cloud computing, big data analytics, and the Internet of Things (IoT) has intensified the need for high-performance, energy-efficient containment systems. Additionally, increasing concerns over data privacy and security, along with the push for green energy solutions, has prompted U.S. companies to invest heavily in sustainable data center technologies, including advanced containment systems. Major tech giants such as Amazon, Google, and Microsoft, which operate massive hyperscale data centers across the country, continue to drive the demand for cutting-edge containment solutions, particularly those that offer both cooling efficiency and scalability. The expansion of data centers in states like Virginia, Texas, and California is expected to contribute to sustained market growth.

Canada (15%)

Canada’s data center industry is also growing rapidly, albeit at a smaller scale than the United States. The demand for data center containment solutions in Canada is largely driven by the expansion of IT services, cloud infrastructure, and demand for colocation services. Key cities such as Toronto and Montreal are becoming data center hubs, attracting both domestic and international players due to their stable political environment, low energy costs, and access to renewable energy sources. The Canadian government’s emphasis on sustainability and green initiatives aligns with the growing demand for energy-efficient data center technologies, boosting the need for advanced containment solutions. Furthermore, the rise of edge computing and local data processing is fostering new investments in data centers that require highly efficient containment systems.

Key players

- Honeywell

- Vertiv

- Rittal

- Legrand

- Trane Technologies

Competitive Analysis

The North America Data Center Containment Market is highly competitive, with key players like Honeywell, Vertiv, Rittal, Legrand, and Trane Technologies leading the charge. These companies offer a diverse range of containment solutions, including hot and cold aisle containment, modular systems, and liquid cooling technologies. Honeywell stands out with its advanced environmental control systems and energy-efficient solutions, catering to both large-scale data centers and smaller operations. Vertiv, known for its comprehensive suite of power, cooling, and containment products, focuses on scalable and flexible solutions for hyperscale data centers. Rittal and Legrand are strong competitors with their robust offerings in modular and rigid containment solutions, providing high efficiency and customization. Trane Technologies has carved out a niche with its focus on energy-efficient cooling solutions and sustainability. Each player is leveraging technological innovations, strategic partnerships, and sustainability initiatives to maintain a competitive edge in the growing market.

Recent Developments

- In November 2023, Huawei introduced two new additions to its Smart Modular Data Center and SmartLi uninterruptible power supply (UPS) series – FusionModule2000 6.0, a modular small/medium-sized data center solution, and UPS2000-H, a small-footprint power supply solution running on SmartLi Mini.

- In February 2025, Trane Technologies expanded its data center solutions to include liquid cooling thermal management systems, introducing the Trane 1MW Coolant Distribution Unit for high-performance workloads.

- In 2025, Honeywell launched a data center management suite to improve efficiency and sustainability by integrating operational and IT infrastructure data.

- In March 2025, Vertiv introduced new solutions to support dense AI and high-performance computing workloads, including consolidated infrastructure management software and prefabricated modular overhead infrastructure.

- In March 2025, Siemens announced a $285 million investment in U.S. manufacturing, including establishing new facilities in California and Texas. This investment aims to enhance manufacturing capabilities and advance AI technologies, supporting sectors such as commercial, industrial, construction, and AI data centers.

Market Concentration and Characteristics

The North America Data Center Containment Market is moderately concentrated, with a few key players dominating the landscape. Leading companies such as Honeywell, Vertiv, Rittal, Legrand, and Trane Technologies hold significant market shares due to their established presence, extensive product portfolios, and technological innovations in containment solutions. These companies offer a range of products, from traditional hot and cold aisle containment to advanced liquid cooling and modular systems, catering to various data center types including hyperscale, enterprise, and colocation centers. The market is characterized by increasing competition driven by the growing demand for energy-efficient and sustainable data center solutions. Additionally, companies are focusing on strategic partnerships, acquisitions, and technological advancements to maintain their competitive edge. While large enterprises dominate the market, the rise of edge computing and modular data centers is opening opportunities for smaller, more specialized players to enter the market, contributing to moderate fragmentation.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Containment Type, Data Center Type, Arrangement and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- As environmental concerns rise, data centers will increasingly prioritize green technologies, driving demand for energy-efficient containment systems that minimize carbon footprints.

- The rapid expansion of hyperscale data centers will continue to fuel demand for advanced containment solutions capable of handling high-density, high-performance computing environments.

- With the growth of edge computing, data centers located closer to end-users will require scalable, modular containment solutions to manage localized computing needs efficiently.

- IoT and AI-based monitoring systems will become standard, allowing for real-time adjustments and predictive maintenance, enhancing the efficiency and effectiveness of containment strategies.

- Liquid cooling solutions will gain traction in the market due to their ability to efficiently manage higher heat loads, particularly in high-density data centers and specialized applications.

- As data centers become more flexible and adaptable, modular containment systems will dominate, allowing for easier expansion and modification as business needs change.

- With tightening environmental regulations, data centers will increasingly adopt containment systems that help meet energy efficiency standards and sustainability certifications such as LEED.

- The rise of cost-effective and compact containment solutions will cater to smaller data center operators who are looking to balance performance with budget constraints.

- As businesses continue to outsource their data storage, colocation centers will require more efficient containment systems to optimize space utilization and cooling efficiency.

- Companies will continue to form strategic partnerships and mergers to combine expertise, expand product portfolios, and meet the increasing demand for sophisticated containment solutions.