Market Overview

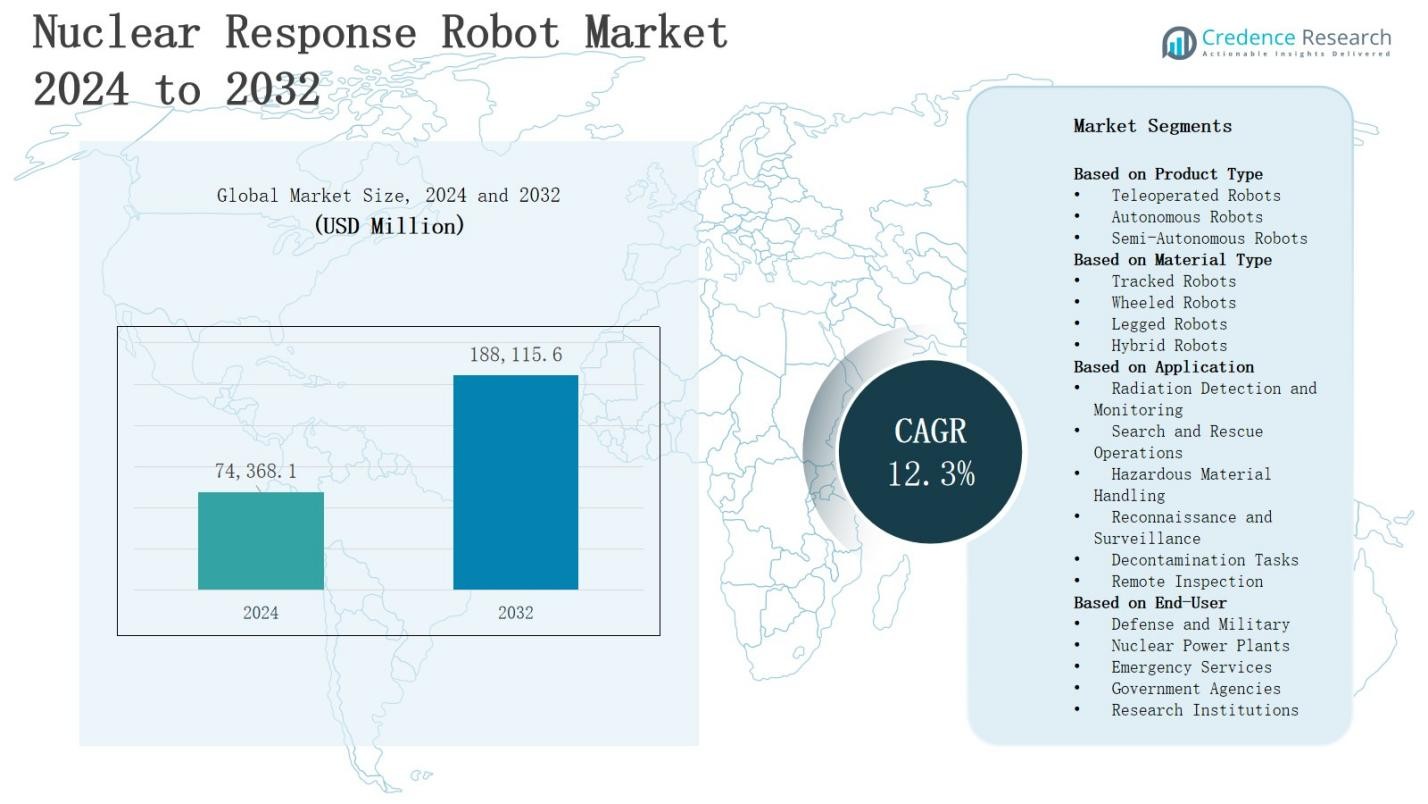

The Nuclear response robot market is projected to grow from USD 74,368.1 million in 2024 to USD 188,115.6 million by 2032, registering a CAGR of 12.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Nuclear response robot market Size 2024 |

USD 74,368.1 Million |

| Nuclear response robot market , CAGR |

12.3% |

| Nuclear response robot market Size 2032 |

USD 188,115.6 Million |

The nuclear response robot market grows due to increasing demand for advanced safety solutions in hazardous environments, rising investments in nuclear facility security, and the need for rapid, remote-controlled disaster response. Adoption strengthens with advancements in AI, machine learning, and sensor integration, enabling precise navigation, radiation detection, and autonomous operations. Governments and nuclear operators prioritize these systems to mitigate human exposure risks and enhance operational efficiency. Trends include the development of lightweight, modular robots, integration with drone-based inspection systems, and enhanced interoperability for multi-robot coordination, supporting broader applications in maintenance, decommissioning, and emergency response within nuclear facilities.

The nuclear response robot market spans North America, Europe, Asia-Pacific, and the Rest of the World, each contributing to global growth through distinct drivers. North America leads with advanced technology adoption and strong government support, while Europe benefits from strict nuclear safety regulations and collaborative R&D. Asia-Pacific grows rapidly with nuclear infrastructure expansion in China, India, and Japan. The Rest of the World, including the Middle East, Latin America, and Africa, adopts robots for emerging nuclear projects. Key players include AB Precision, Boston Dynamics, Hitachi, Mitsubishi, Elbit Systems, and General Dynamics.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The nuclear response robot market is projected to grow from USD 74,368.1 million in 2024 to USD 188,115.6 million by 2032, registering a CAGR of 12.3% during the forecast period.

- Rising demand for advanced safety solutions in hazardous environments and the need for remote-controlled disaster response drive market growth.

- AI, machine learning, and advanced sensor integration enhance navigation, radiation detection, and autonomous operations.

- Governments and defense agencies invest heavily to improve nuclear facility safety, disaster preparedness, and operational efficiency.

- Robots play a growing role in nuclear maintenance, decommissioning, waste handling, and precision operations under extreme conditions.

- High development and deployment costs, along with technical limitations in harsh environments, remain key challenges for adoption.

- North America holds 34% market share, Europe 27%, Asia-Pacific 29%, and the Rest of the World 10%, with leading players including AB Precision, Boston Dynamics, Hitachi, Mitsubishi, Elbit Systems, and General Dynamics.

Market Drivers

Rising Demand for Enhanced Safety in Hazardous Environments

The nuclear response robot market is driven by the critical need to protect human operators from high-radiation zones during nuclear accidents, maintenance, or decommissioning activities. It enables safe execution of tasks such as inspection, debris removal, and leak detection without exposing personnel to dangerous conditions. Governments and nuclear operators increasingly invest in robotic solutions to comply with safety regulations and prevent accidents. Growing awareness of occupational safety further strengthens adoption. The technology addresses challenges in confined, contaminated, or unstable environments.

- For instance, EDF Energy in the UK employs self-driven robots to inspect nuclear reactors, which enhances work productivity while reducing maintenance costs and human exposure to radiation.

Advancements in Robotics, AI, and Sensor Integration

Technological innovation significantly propels the nuclear response robot market by enhancing operational accuracy, efficiency, and adaptability. It benefits from AI-powered navigation, real-time data analytics, and high-resolution imaging systems that improve situational awareness. Advanced sensors enable precise radiation detection, thermal imaging, and structural integrity assessment in complex environments. Continuous improvements in autonomy and mobility allow robots to operate effectively in challenging terrains. The integration of machine learning enables predictive maintenance and decision-making.

Increasing Government and Defense Sector Investments

National security concerns and nuclear infrastructure safety drive substantial investments in the nuclear response robot market. It gains traction as governments allocate budgets for disaster preparedness, counter-terrorism, and rapid incident response capabilities. Defense agencies adopt these robots for operations in nuclear-powered military vessels and facilities. Funding initiatives focus on developing rugged, reliable, and deployable systems. Strategic partnerships between public agencies and private manufacturers encourage innovation and cost-effective production. Such investments ensure availability of advanced robotic solutions for immediate deployment during nuclear emergencies.

- For instance, Orano, a leading player in the nuclear industry, develops highly specialized manipulators used in radioactive material handling and decommissioning, supported by government contracts aimed at ensuring robust emergency response and infrastructure maintenance.

Growing Role in Nuclear Facility Maintenance and Decommissioning

Routine maintenance, inspection, and decommissioning projects create consistent demand in the nuclear response robot market. It supports critical tasks such as dismantling reactor components, removing radioactive waste, and performing precision welding or cutting under extreme conditions. Robots minimize downtime, improve accuracy, and reduce operational risks. The aging global nuclear infrastructure increases the need for automated systems to extend operational lifespans. Decommissioning of outdated reactors further boosts adoption. Enhanced cost-efficiency and safety benefits make robots integral to modern nuclear facility operations.

Market Trends

Integration of Artificial Intelligence and Autonomous Navigation

The nuclear response robot market is witnessing a strong shift toward AI-driven capabilities and autonomous navigation systems. It enables robots to perform complex missions without continuous human intervention, improving operational speed and safety. AI enhances decision-making by analyzing environmental data in real time, adapting to dynamic conditions, and optimizing movement paths. Advanced navigation systems allow precise maneuvering in confined or debris-filled spaces. This trend reduces human error and improves efficiency during nuclear disaster response and facility maintenance tasks.

Adoption of Modular and Customizable Robotic Platforms

Manufacturers are increasingly offering modular designs in the nuclear response robot market to address varied operational needs. It allows end users to customize robots with interchangeable tools, sensors, and mobility systems for specific missions. Modular architecture supports cost-effective upgrades, extending the operational life of the robots. This flexibility improves deployment efficiency across inspection, decontamination, and waste handling tasks. Demand for adaptable platforms grows as nuclear facilities seek versatile solutions that minimize downtime and operational disruptions.

- For instance, at the IAEA workshop, robot dogs with customizable sensor payloads and modular components were demonstrated for maintenance and rapid incident response at nuclear power plants, enabling quick adaptation to changing mission requirements.

Expansion of Remote Monitoring and Control Capabilities

The nuclear response robot market benefits from advancements in remote monitoring and control technologies that improve operator safety and mission precision. It incorporates high-definition cameras, radiation sensors, and real-time data transmission systems for enhanced situational awareness. Operators can manage robots from secure control centers far from hazardous zones, reducing exposure risks. Improved connectivity enables integration with unmanned aerial vehicles and other robotic assets. This trend supports multi-platform coordination during complex nuclear response operations.

- For instance, the Korea Atomic Energy Research Institute (KAERI) developed a remote-controlled unmanned ground vehicle combined with a drone for rapid radiation monitoring across nuclear plant sites, using radiation-hardened electronics and range-gated imaging cameras to operate effectively in low visibility conditions.

Focus on Lightweight, Durable, and Radiation-Resistant Materials

Material innovation is shaping the nuclear response robot market with the development of lightweight yet highly durable components. It enhances mobility while ensuring resistance to radiation, extreme temperatures, and corrosive environments. Advanced composites and specialized alloys extend operational lifespans and reduce maintenance requirements. Lighter designs enable easier transport and faster deployment in emergency scenarios. This trend addresses the need for high-performance robots capable of sustained operations in challenging nuclear facility conditions.

Market Challenges Analysis

High Development and Deployment Costs

The nuclear response robot market faces significant challenges due to the high costs associated with research, development, and deployment. It requires advanced engineering, specialized materials, and rigorous safety testing, which substantially increase production expenses. Budget constraints in certain regions limit large-scale adoption, especially in developing markets. Maintenance and repair of these robots demand skilled technicians and specialized parts, adding to the operational costs. Smaller nuclear facilities often struggle to justify the investment despite long-term safety benefits. The financial barrier slows market penetration and adoption across lower-budget sectors.

Technical Limitations and Harsh Operational Environments

Operating in high-radiation, high-temperature, and debris-filled environments presents major technical challenges for the nuclear response robot market. It demands robust designs that can withstand extreme conditions without compromising performance. Complex terrains and confined spaces require advanced mobility solutions, which can be difficult to engineer. Signal interference and connectivity issues in nuclear facilities hinder seamless remote operations. Frequent exposure to radiation degrades sensors and electronic components over time, requiring costly replacements. These limitations slow operational efficiency and necessitate continuous innovation to maintain reliability in critical missions.

Top of Form

Market Opportunities

Rising Global Focus on Nuclear Safety and Disaster Preparedness

The nuclear response robot market holds significant opportunities with the increasing emphasis on nuclear safety and disaster preparedness worldwide. It benefits from government initiatives, international safety regulations, and industry-wide mandates to enhance protection measures in nuclear facilities. Growing investments in emergency response infrastructure create demand for advanced robotic systems capable of rapid deployment. Expanding nuclear energy projects in emerging economies further widen the market scope. The adoption of robots for proactive safety inspections and incident prevention positions manufacturers to capture long-term contracts from both public and private sectors.

Technological Innovation and Cross-Sector Applications

Advancements in AI, machine learning, and material science present lucrative growth avenues for the nuclear response robot market. It can leverage innovations such as autonomous navigation, multi-sensor integration, and collaborative robotics to expand operational capabilities. Opportunities also arise from cross-sector applications, including hazardous waste management, deep-sea exploration, and defense operations involving radiological threats. Partnerships between robotics developers, research institutions, and nuclear operators can accelerate tailored solution development. Increasing demand for versatile, high-performance robots opens pathways for new product lines, service models, and international market expansion.

Market Segmentation Analysis:

By Product Type

The nuclear response robot market is segmented into teleoperated robots, autonomous robots, and semi-autonomous robots. Teleoperated robots dominate in scenarios requiring real-time human control for precision and safety. Autonomous robots gain traction with AI and sensor advancements that enable independent decision-making in complex environments. Semi-autonomous robots provide a balance between automation and operator oversight, appealing to facilities seeking flexibility. Demand across all categories is driven by the need for rapid deployment and reliable performance in hazardous zones.

- For instance, ENGIE Laborelec specializes in custom-built robotic solutions for nuclear power plants, designing high-precision robots tailored to tasks like non-destructive testing and repairs in highly radioactive environments.

By Material Type

Based on material type, the market includes tracked robots, wheeled robots, legged robots, and hybrid robots. Tracked robots excel in rough terrains and debris-filled areas, offering stability and mobility. Wheeled robots are preferred for speed and maneuverability in controlled environments. Legged robots navigate uneven surfaces and confined spaces effectively. Hybrid robots combine multiple mobility systems to optimize performance across varied conditions. This segmentation reflects the industry’s focus on operational adaptability and efficiency in high-risk settings.

- For instance, CuboRex developed tracked robots powered by NVIDIA Jetson Orin NX, capable of handling rough agricultural and construction sites with slopes up to 20°, supporting heavy loads of up to 70 kg to reduce labor costs and improve productivity.

By Application

By application, the market covers radiation detection and monitoring, search and rescue operations, hazardous material handling, reconnaissance and surveillance, decontamination tasks, and remote inspection. Radiation detection systems are critical for real-time safety monitoring during emergencies and routine operations. Search and rescue robots assist in locating and retrieving personnel in hazardous zones. Hazardous material handling reduces human exposure during waste processing. Reconnaissance, decontamination, and remote inspection tasks enhance safety, operational efficiency, and regulatory compliance in nuclear facilities worldwide.

Segments:

Based on Product Type

- Teleoperated Robots

- Autonomous Robots

- Semi-Autonomous Robots

Based on Material Type

- Tracked Robots

- Wheeled Robots

- Legged Robots

- Hybrid Robots

Based on Application

- Radiation Detection and Monitoring

- Search and Rescue Operations

- Hazardous Material Handling

- Reconnaissance and Surveillance

- Decontamination Tasks

- Remote Inspection

Based on End-User

- Defense and Military

- Nuclear Power Plants

- Emergency Services

- Government Agencies

- Research Institutions

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

North America

North America accounts for 34% of the global nuclear response robot market, driven by strong government funding, advanced nuclear infrastructure, and a high emphasis on disaster preparedness. It benefits from the presence of leading robotics manufacturers and technology innovators in the United States and Canada. Defense and homeland security agencies integrate these robots for nuclear-powered military assets and emergency operations. The region invests heavily in AI-driven robotics for precision and autonomy in hazardous missions. Growing nuclear energy projects in the U.S. and modernization of existing facilities strengthen market demand. Regulatory mandates for safety and incident prevention further support adoption across critical operations.

Europe

Europe holds 27% of the nuclear response robot market, supported by stringent nuclear safety regulations and strong investment in advanced robotics. Countries such as France, the UK, and Germany lead in deploying robotic systems for nuclear maintenance, decommissioning, and emergency response. The European Union funds research programs to enhance radiation resistance and mobility capabilities. Rising focus on upgrading aging reactors fuels the demand for robots in inspection and decontamination tasks. Partnerships between robotics firms and nuclear operators accelerate innovation. Defense applications, particularly in naval nuclear fleets, contribute to consistent market growth in the region.

Asia-Pacific

Asia-Pacific represents 29% of the nuclear response robot market, driven by rapid nuclear energy expansion in China, India, and Japan. It benefits from rising investments in automation and safety technologies to support large-scale nuclear infrastructure projects. Japan leads in robotic applications for nuclear disaster recovery, drawing from post-Fukushima initiatives. China focuses on indigenous robot production to meet safety and operational efficiency needs. India invests in multi-functional robots for nuclear research facilities and reactors. Regional growth is further supported by government-backed R&D programs and collaborations with global robotics leaders.

Rest of the World

The Rest of the World holds 10% of the nuclear response robot market, with demand primarily from the Middle East, Latin America, and Africa. It grows through nuclear energy investments, particularly in the UAE, Saudi Arabia, and Brazil. These regions adopt robots for facility construction, inspection, and safety compliance. Limited local manufacturing capacity drives imports from North America, Europe, and Asia-Pacific. Governments seek advanced solutions to strengthen nuclear safety frameworks. The growing interest in clean energy projects supports the long-term adoption of nuclear response robotics across emerging markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Energid Technologies

- Mitsubishi

- Carnegie Mellon University

- General Dynamics

- AB Precision (Poole) Ltd.

- Hitachi

- Boston Dynamics

- Romotec

- Ditch Witch ECA Robotics

- Chemring EOD Limited

- DCD-DORBYL (Pty) Ltd) / RSD

- First Response Robotics

- Elbit Systems

Competitive Analysis

The nuclear response robot market is characterized by a mix of established defense contractors, advanced robotics firms, and specialized technology developers competing to deliver high-performance solutions for hazardous environments. It features key players such as AB Precision (Poole) Ltd., Boston Dynamics, Carnegie Mellon University, Chemring EOD Limited, DCD-DORBYL (Pty) Ltd./RSD, Ditch Witch ECA Robotics, Elbit Systems, Energid Technologies, First Response Robotics, Mitsubishi, Hitachi, Romotec, and General Dynamics. These companies focus on enhancing mobility, autonomy, and radiation resistance to meet stringent nuclear safety requirements. Strategic partnerships with government agencies and nuclear operators are common, enabling access to funding and real-world deployment opportunities. Innovation centers on AI-driven navigation, modular design, and advanced sensor integration to improve operational efficiency in tasks like radiation detection, decontamination, and hazardous material handling. Regional competition is influenced by differing safety regulations, nuclear energy investments, and technological capabilities, with North America, Europe, and Asia-Pacific serving as the primary hubs for both production and demand.

Recent Developments

- On July 28, 2025, South Korea’s Korea Atomic Energy Research Institute unveiled its humanoid robot ARMstrong Dex, which demonstrated precise emergency-response capabilities by accurately tossing a water bottle into a barrel from ten feet away.

- On July 15, 2025, BPMI, a prime contractor for the U.S. Naval Nuclear Propulsion Program, partnered with Gecko Robotics to accelerate production of critical components for U.S. Navy nuclear-powered vessels.

- on June 27, 2025, the U.K.’s Nuclear Decommissioning Authority (NDA) announced a new robotics partnership, labeled Auto‑SAS, between AtkinsRéalis and Createc. Funded with up to £9.5 million, this project will remotely and autonomously sort and segregate nuclear waste at the Oldbury decommissioning site.

- On March 19, 2025, Sellafield Ltd. and AtkinsRéalis successfully operated the Spot robotic dog remotely at the Sellafield nuclear site—one of the first of such deployments at a licensed nuclear facility.

Market Concentration & Characteristics

The nuclear response robot market is moderately concentrated, with a mix of global defense contractors, robotics specialists, and research institutions competing to deliver advanced solutions for hazardous nuclear environments. It is characterized by high entry barriers due to the need for specialized engineering, compliance with stringent safety regulations, and substantial R&D investments. Leading players leverage proprietary technologies, AI integration, and durable materials to enhance performance, mobility, and radiation resistance. The market emphasizes customization, enabling robots to address diverse applications such as radiation monitoring, decontamination, and hazardous material handling. Strategic collaborations between manufacturers, government agencies, and nuclear operators drive innovation and field deployment. Demand is sustained by the aging nuclear infrastructure, expanding energy projects, and heightened safety standards. Competitive differentiation is based on operational reliability, multi-environment adaptability, and lifecycle cost efficiency, making technology leadership a key factor for long-term market positioning.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Material Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand will grow as global nuclear safety regulations tighten, requiring advanced remote-operated safety solutions.

- AI-driven autonomy will improve robots’ ability to handle complex nuclear tasks with minimal human intervention.

- Modular, customizable designs will enable flexible deployment across varied nuclear maintenance, inspection, and emergency operations.

- Integration with drones will enhance remote inspection, monitoring accuracy, and efficiency in hazardous nuclear environments.

- Governments will increase budgets for advanced robotics to strengthen national nuclear disaster preparedness and response capabilities.

- Advanced radiation-resistant materials will extend operational lifespan and durability of robots in extreme nuclear facility conditions.

- Cross-sector uses will expand, including hazardous waste management, defense, and high-risk industrial inspection applications.

- Asia-Pacific will boost domestic production to meet rising regional nuclear infrastructure demands and safety standards.

- Collaborative R&D initiatives will accelerate innovation in coordinated multi-robot operations for complex nuclear facility missions.

- Lifecycle cost optimization will drive adoption, balancing performance with long-term operational and maintenance expense efficiency.