Market Overview

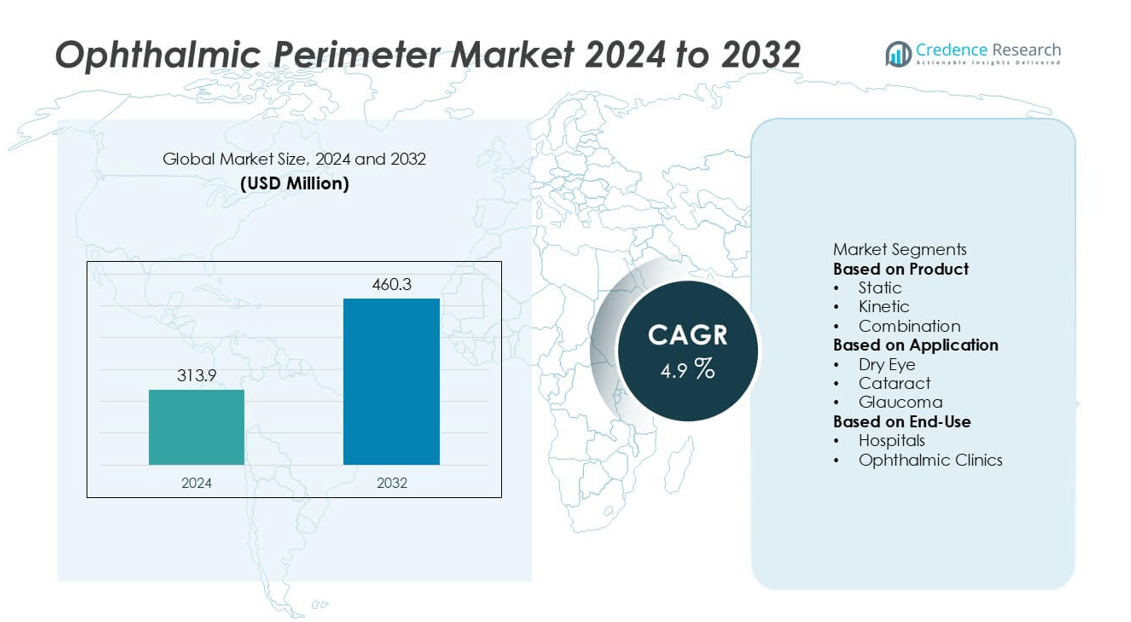

The Ophthalmic Perimeter Market was valued at USD 313.9 million in 2024 and is projected to reach USD 460.3 million by 2032, growing at a CAGR of 4.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ophthalmic Perimeter Market Size 2024 |

USD 313.9 million |

| Ophthalmic Perimeter Market, CAGR |

4.9% |

| Ophthalmic Perimeter Market Size 2032 |

USD 460.3 million |

The Ophthalmic Perimeter Market is driven by the rising prevalence of glaucoma, cataracts, and age-related vision disorders, coupled with growing demand for early diagnosis and preventive eye care. Expanding geriatric populations and increasing healthcare investments further strengthen the adoption of advanced perimeter systems.

The geographical landscape of the Ophthalmic Perimeter Market demonstrates strong adoption across North America and Europe, supported by advanced healthcare infrastructure, high awareness of eye health, and consistent technological innovation. Asia-Pacific is emerging as a high-growth region, driven by expanding healthcare facilities, rising elderly populations, and increasing demand for affordable diagnostic solutions. Latin America and the Middle East & Africa are gradually strengthening their presence with growing investments in healthcare modernization and preventive eye care initiatives. Key players shaping the market include Haag-Streit AG, known for precision diagnostic instruments, Topcon Corporation, a leader in ophthalmic imaging and perimetry solutions, and Nidek Co., Ltd., which emphasizes advanced, user-friendly devices. Other notable contributors include Heidelberg Engineering GmbH, recognized for innovation in diagnostic imaging, and Centervue S.P.A., with a focus on digital and automated perimeter systems. Together, these companies drive technological advancements and expand global access to high-quality vision care solutions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Ophthalmic Perimeter Market was valued at USD 313.9 million in 2024 and is projected to reach USD 460.3 million by 2032, growing at a CAGR of 4.9% during the forecast period.

- The market is expanding due to the rising prevalence of glaucoma, cataracts, and other vision-related disorders, with increasing emphasis on early detection and routine eye screening driving higher adoption of perimeters.

- Key trends include the shift toward automated and portable perimeters, integration of artificial intelligence for precise diagnostics, adoption of teleophthalmology for remote care, and demand for ergonomic, patient-friendly device designs.

- The competitive landscape features major players such as Haag-Streit AG, Topcon Corporation, Nidek Co., Ltd., Heidelberg Engineering GmbH, and Centervue S.P.A., who focus on innovation, digital integration, and global expansion strategies.

- Market restraints include the high cost of advanced perimeter systems, limited affordability in developing regions, shortage of skilled professionals for accurate test administration, and complexities in visual field interpretation.

- North America leads the market due to strong healthcare infrastructure and early adoption of advanced technologies, while Europe shows steady growth with government support and widespread glaucoma screening programs. Asia-Pacific is expected to register the fastest growth due to expanding healthcare access, while Latin America and the Middle East & Africa present gradual opportunities with ongoing healthcare modernization.

- The market outlook remains positive, supported by technological innovation, growing patient awareness, and increased healthcare investments, positioning perimeter systems as a critical component of modern eye care diagnostics.

Market Drivers

Rising Prevalence of Eye Disorders and Growing Need for Early Detection

The increasing prevalence of glaucoma, cataracts, and other vision-related disorders strongly drives the demand for advanced diagnostic equipment. Ophthalmic Perimeter Market plays a crucial role in assessing visual field defects, which are critical indicators of progressive eye disease. Early detection has become a priority in healthcare systems, with emphasis on reducing blindness and preserving vision. It enables ophthalmologists to track disease progression and customize treatment effectively. With growing global awareness about vision health, more patients undergo routine eye examinations. It strengthens the adoption of perimeters across both developed and emerging markets.

- For instance, The Topcon NW500, launched in 2022, is a retinal camera featuring a 12MP sensor for enhanced image quality, with a final output resolution of 7.1 megapixels. A successor to the TRC-NW400, it uses slit-scan technology for high-quality retina and optic nerve imaging.

Expanding Geriatric Population and Higher Risk of Vision Impairment

The steady rise in the elderly population has created a significant impact on the demand for vision care services. Ophthalmic Perimeter Market benefits from this demographic trend, as older adults face higher risk of glaucoma and age-related macular degeneration. It has become vital for healthcare providers to use reliable perimeter devices to ensure timely diagnosis and management of chronic eye conditions. Countries with increasing life expectancy continue to invest in advanced ophthalmic technologies. It contributes to higher penetration of perimetry devices across hospitals and eye care centers. This trend enhances market growth prospects over the forecast period.

- For instance, Nidek Co., Ltd. introduced the MP-3 microperimeter in 2015, which provides a comprehensive solution for elderly patients by combining structural and functional testing in a single system.

Technological Advancements and Integration of Automated Perimeters

Rapid advancements in diagnostic technology have transformed the way ophthalmologists evaluate patient conditions. Ophthalmic Perimeter Market has seen strong adoption of automated systems that reduce testing errors and improve patient comfort. It allows faster, more accurate visual field analysis while minimizing the dependency on manual interpretation. The integration of digital interfaces, data storage, and cloud connectivity enhances efficiency in clinical settings. Hospitals and clinics prefer automated devices that provide consistent outcomes and reduce the burden on medical staff. It creates a favorable environment for sustained innovation and wider adoption.

Increasing Healthcare Investments and Rising Access to Eye Care

Growing healthcare expenditure in both developed and developing regions supports the adoption of modern ophthalmic equipment. Ophthalmic Perimeter Market benefits from rising investments in hospital infrastructure and specialty eye clinics. It ensures better access to diagnostic tools for a larger segment of the population. Expanding insurance coverage and government programs further encourage patients to undergo regular eye screening. Emerging economies are witnessing strong demand for advanced medical devices due to increasing awareness and improved purchasing capacity. It highlights the importance of perimeters in strengthening preventive eye care strategies.

Market Trends

Growing Adoption of Automated and Portable Perimeters in Clinical Practice

Automation has emerged as a major trend in diagnostic ophthalmology, with perimeters evolving toward user-friendly and highly precise systems. Ophthalmic Perimeter Market reflects this shift, as clinics and hospitals prefer automated devices that enhance efficiency and reduce human error. It allows physicians to obtain accurate data with minimal patient discomfort, improving overall clinical outcomes. Portable and compact models are gaining popularity due to their flexibility in small practices and outreach programs. The convenience of mobility makes these devices suitable for screening in rural or underserved regions. It ensures broader patient coverage and enhances accessibility to quality eye care.

- For instance, The Heidelberg SPECTRALIS HRA+OCT is an advanced, modular ophthalmic imaging platform. It combines scanning laser and high-resolution Optical Coherence Tomography (OCT) for precise views of the eye. The SPECTRALIS platform was first introduced by Heidelberg Engineering in 2006 and has been continuously upgraded. It does not include automated perimetry, which is a separate test for measuring the visual field. Upgrades, such as the SHIFT technology that enables faster 125 kHz scans, have enhanced its speed and image quality over time, particularly for OCT angiography.

Integration of Artificial Intelligence and Data Analytics for Enhanced Diagnosis

Artificial intelligence has become a key enabler of advanced visual field testing and interpretation. Ophthalmic Perimeter Market is witnessing growing adoption of AI-based software that can analyze large datasets and detect subtle changes in patient vision. It helps practitioners improve accuracy in diagnosing early-stage glaucoma and other disorders. The ability to integrate predictive analytics enhances treatment planning and long-term monitoring. AI-driven platforms also support faster decision-making in busy clinical environments. It strengthens confidence among healthcare professionals in adopting digital perimeter technologies.

- For instance, Topcon Corporation developed AI-powered screening software in 2023, integrated with its automated perimeters to assist in detecting early glaucoma by analyzing patient data trends. It helps practitioners improve accuracy in diagnosing early-stage glaucoma and other disorders.

Expansion of Teleophthalmology and Remote Diagnostic Capabilities

Telemedicine continues to expand across multiple healthcare domains, and ophthalmology is no exception. Ophthalmic Perimeter Market benefits from the integration of teleophthalmology solutions that enable remote screening and diagnosis. It allows patients in distant locations to undergo visual field testing without traveling to specialized centers. The trend is particularly strong in regions with limited ophthalmologist availability. Remote diagnostic platforms combined with digital perimeter devices improve access to timely care. It creates a sustainable model for delivering preventive and routine eye health services.

Rising Demand for Patient-Centric and Ergonomic Device Designs

The design and usability of diagnostic devices play a critical role in patient compliance and test accuracy. Ophthalmic Perimeter Market is influenced by rising demand for ergonomic, patient-friendly systems that reduce discomfort during testing. It ensures better cooperation from patients, leading to reliable test results. Manufacturers are introducing compact designs with intuitive interfaces that minimize learning curves for practitioners. Patient-centric innovations such as shorter test durations and comfortable seating arrangements are gaining preference. It highlights the industry’s focus on enhancing both patient experience and clinical efficiency.

Market Challenges Analysis

High Cost of Advanced Devices and Limited Accessibility in Developing Regions

The cost of advanced perimeter systems presents a major barrier to widespread adoption. Ophthalmic Perimeter Market faces challenges in expanding into low- and middle-income regions where healthcare budgets remain constrained. It is difficult for small clinics and public hospitals to invest in premium diagnostic equipment despite rising demand for vision care. The high cost of installation, maintenance, and software upgrades further limits access. Patients in underserved areas often lack exposure to advanced eye screening technologies. It restricts timely detection of diseases such as glaucoma and slows down overall market penetration.

Shortage of Skilled Professionals and Complexities in Test Administration

Perimeter testing requires skilled ophthalmologists or trained technicians to achieve accurate results, which creates another challenge for healthcare providers. Ophthalmic Perimeter Market is impacted by a shortage of specialized professionals, especially in rural and semi-urban locations. It often leads to underutilization of equipment or inaccurate test outcomes. The complexity of interpreting visual field results demands consistent training, which smaller practices may not afford. Time-intensive procedures and patient discomfort can also affect test reliability. It highlights the need for continuous professional education and better-designed systems to minimize operational barriers.

Market Opportunities

Expansion in Emerging Economies and Growing Healthcare Infrastructure

The rapid development of healthcare infrastructure in emerging economies creates significant growth prospects for diagnostic equipment. Ophthalmic Perimeter Market is well-positioned to benefit from rising investments in specialty hospitals, clinics, and diagnostic centers. It supports wider access to advanced vision care technologies among larger populations. Government initiatives to expand screening programs and promote preventive healthcare further strengthen the adoption of perimeters. Rising disposable income and growing awareness about early detection of eye disorders enhance patient willingness to undergo regular examinations. It creates a favorable environment for market expansion across Asia-Pacific, Latin America, and parts of the Middle East.

Technological Innovation and Rising Adoption of Digital Health Solutions

The integration of digital health platforms and innovative device designs offers significant opportunities for future market growth. Ophthalmic Perimeter Market can leverage advancements in artificial intelligence, cloud-based data storage, and teleophthalmology to provide more accurate and accessible eye care. It enables healthcare providers to streamline diagnosis, improve monitoring, and deliver personalized treatment plans. Compact and portable devices open pathways for use in community screening programs and remote locations. Growing preference for patient-centric technologies drives continuous demand for modernized systems. It creates opportunities for manufacturers to expand product portfolios and strengthen their global market presence.

Market Segmentation Analysis:

By Product

The product segment of the Ophthalmic Perimeter Market is categorized into static, kinetic, and combination perimeters. Static perimeters dominate the market due to their accuracy in detecting early-stage glaucoma and ease of use in clinical environments. It provides consistent outcomes and is widely adopted by hospitals and specialty clinics. Kinetic perimeters hold steady demand in advanced diagnostic centers where detailed field mapping is required. Combination models are gaining traction as they integrate the advantages of both techniques in a single system. It reflects the growing demand for versatile devices that can meet diverse clinical requirements.

- For instance, Nidek Co., Ltd. introduced the MP-1 microperimeter in 2002. This device was among the first commercial microperimeters with automated real-time fundus tracking, which allows for repeatable, fundus-guided static perimetry with high-resolution imaging.

By Application

The application segment includes glaucoma, cataract, macular disease, and others. Ophthalmic Perimeter Market is strongly driven by the glaucoma segment, as it remains one of the leading causes of irreversible blindness worldwide. It highlights the importance of routine visual field testing in early detection and management. The cataract segment also shows stable growth, supported by rising surgical procedures and the need for accurate preoperative and postoperative assessment. Macular disease applications are expanding due to growing cases of age-related degeneration in elderly populations. It creates continuous demand for advanced diagnostic tools to support precise monitoring and timely interventions.

- For instance, Metrovision launched the MonCvONE-CR in 2024, a device designed to improve early glaucoma detection through enhanced visual field testing. It highlights the importance of routine visual field testing in early detection and management.

By End-Use

The end-use segment covers hospitals, ophthalmic clinics, and diagnostic centers. Hospitals hold a substantial share of the Ophthalmic Perimeter Market, supported by their ability to invest in advanced technologies and serve large patient volumes. It ensures availability of comprehensive diagnostic services under one roof. Ophthalmic clinics represent a fast-growing segment, driven by rising patient preference for specialized care and shorter waiting times. Diagnostic centers are expanding their adoption of perimeters due to increasing demand for affordable and accessible eye examinations. It underlines the importance of advanced visual field testing across multiple healthcare delivery settings.

Segments:

Based on Product

- Static

- Kinetic

- Combination

Based on Application

- Dry Eye

- Cataract

- Glaucoma

Based on End-Use

- Hospitals

- Ophthalmic Clinics

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Ophthalmic Perimeter Market, accounting for nearly 35% of the global market in 2024. The region benefits from advanced healthcare infrastructure, strong adoption of innovative diagnostic technologies, and a high level of awareness about vision health. It is supported by the presence of major manufacturers and research institutions that consistently introduce automated and AI-integrated perimeter systems. The United States dominates the regional market due to its well-established reimbursement policies and growing demand for preventive eye care. Canada also contributes significantly, driven by increasing investments in public healthcare programs. It is expected that North America will maintain its leadership position over the forecast period due to continuous technological advancements and strong clinical adoption.

Europe

Europe represents the second-largest market, with a share of approximately 28% in 2024. The region is characterized by widespread adoption of advanced ophthalmic devices and strong government support for healthcare innovation. It demonstrates robust demand in countries such as Germany, the United Kingdom, and France, where glaucoma screening and cataract management programs are well-integrated into healthcare systems. Rising incidence of age-related vision disorders across the continent fuels continuous need for perimeter testing. It also benefits from collaborative research initiatives that drive product development and expand clinical applications. Southern and Eastern European countries are gradually increasing adoption rates, supported by expanding healthcare investments. It is anticipated that Europe will sustain steady growth due to its structured healthcare system and emphasis on early disease detection.

Asia-Pacific

Asia-Pacific accounts for nearly 22% of the Ophthalmic Perimeter Market in 2024, making it one of the fastest-growing regions. The rapid increase in elderly populations in China, Japan, and India significantly raises demand for vision care services. It benefits from improving healthcare infrastructure, rising disposable incomes, and greater awareness about eye health among patients. Governments in the region are investing heavily in screening programs to address the burden of glaucoma and cataracts. Japan shows strong demand due to its high proportion of elderly citizens, while China and India represent large markets with growing adoption of affordable and portable devices. It is expected that Asia-Pacific will experience the highest growth rate during the forecast period, supported by strong demand in both urban and rural areas.

Latin America

Latin America represents around 8% of the global market in 2024. Growth in this region is supported by increasing investments in healthcare modernization and expanding private healthcare facilities. It faces challenges due to budget constraints in public hospitals, but rising demand for preventive eye care encourages adoption in urban areas. Brazil and Mexico lead the market due to higher patient awareness and greater availability of advanced equipment. Smaller countries are gradually improving diagnostic capabilities with the support of international collaborations and private sector involvement. It is projected that Latin America will expand steadily with rising investments in diagnostic centers and clinics.

Middle East & Africa

The Middle East & Africa holds nearly 7% of the Ophthalmic Perimeter Market in 2024. The region is still in the early stages of adopting advanced ophthalmic technologies, but it shows promising potential. It is supported by growing healthcare investments in Gulf countries, where modern hospitals and specialty clinics increasingly integrate advanced perimeter systems. Africa faces significant barriers due to lack of infrastructure and limited access to specialized care, yet awareness programs are driving gradual improvements. South Africa and the United Arab Emirates are leading markets due to better healthcare systems and patient awareness. It is anticipated that the Middle East & Africa will witness gradual but consistent growth, supported by government health initiatives and international partnerships aimed at reducing preventable blindness.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Centervue S.P.A.

- Takagi Seiko Co., Ltd.

- Heidelberg Engineering GmbH

- Metrovision

- Kowa Company, Ltd.

- Nidek Co., Ltd.

- Konan Medical USA, Inc.

- Optopol Technology Sp. z o.o.

- Haag-Streit AG

- Topcon Corporation

Competitive Analysis

The competitive landscape of the Ophthalmic Perimeter Market is shaped by leading players including Centervue S.P.A., Takagi Seiko Co., Ltd., Heidelberg Engineering GmbH, Metrovision, Kowa Company, Ltd., Nidek Co., Ltd., Konan Medical USA, Inc., Optopol Technology Sp. z o.o., Haag-Streit AG, and Topcon Corporation, all of which focus on advancing diagnostic technologies and strengthening market reach. These companies emphasize innovation through automated systems, AI-driven analysis, and integration of digital platforms to improve accuracy and efficiency in visual field testing. It is clear that product innovation, strong distribution channels, and research-driven strategies are central to their competitiveness. Many of these firms target expansion in emerging economies where rising healthcare investments and growing awareness of preventive eye care drive new demand. Strategic collaborations, acquisitions, and partnerships are also key tools for enhancing product portfolios and global presence. The competition remains intense, with players balancing technological advancement with affordability to cater to diverse healthcare settings. By focusing on patient comfort, faster testing, and accurate disease detection, these companies are positioning themselves to capture a larger share of the growing market, while maintaining compliance with evolving regulatory and clinical standards worldwide.

Recent Developments

- In November 2024, Konan Medical USA launched the objectiveFIELD visual field analyzer, the first FDA-cleared objective perimeter.

- In October 2024, the Heidelberg Engineering received FDA clearance for the SPECTRALIS Flex Module, enhancing imaging capabilities.

- In September 2024, Takagi Seiko announced the upcoming release of its Imaging System TD12.

Report Coverage

The research report offers an in-depth analysis based on Product, Application, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will continue to grow steadily with rising demand for early detection of glaucoma and other vision disorders.

- Automated and AI-integrated perimeters will gain wider acceptance among hospitals and clinics.

- Portable and compact devices will see strong demand in community screening and remote healthcare programs.

- Patient-friendly designs will improve compliance and enhance accuracy in visual field testing.

- Expansion in emerging economies will create new opportunities for manufacturers and distributors.

- Digital health integration and cloud-based data storage will become standard features in advanced systems.

- Strategic collaborations and partnerships will drive innovation and global market penetration.

- Increasing awareness of preventive eye care will encourage routine screening across larger populations.

- Training and education programs for healthcare professionals will play a vital role in ensuring accurate test outcomes.

- Continuous investment in research and development will shape future advancements and sustain competitive advantage.