Market Overview

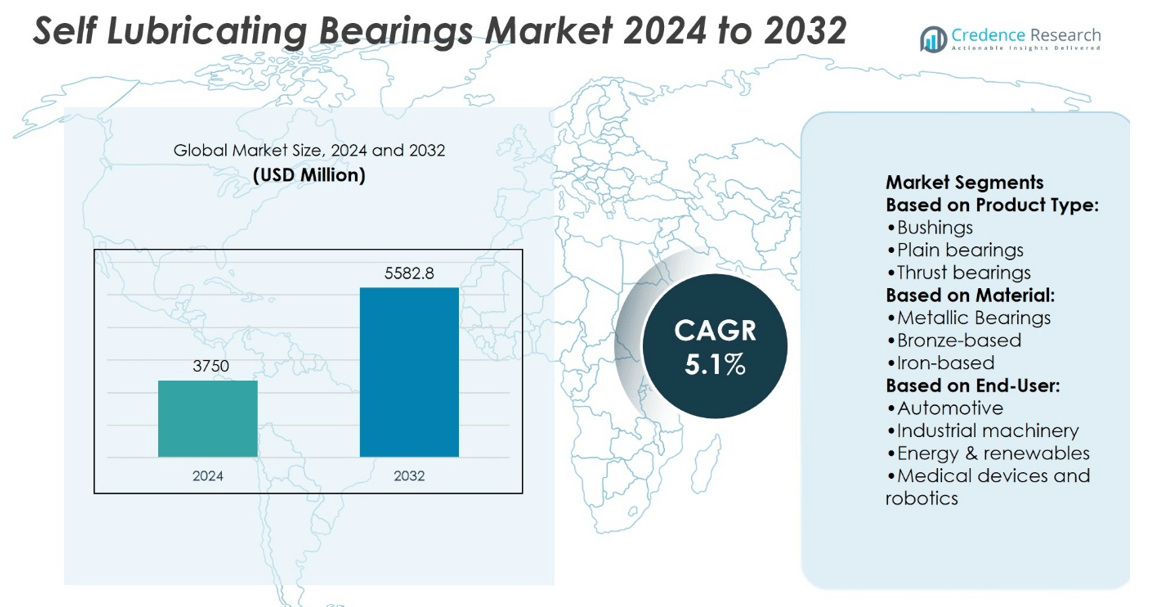

Self-Lubricating Bearings Market size was valued at USD 3750 million in 2024 and is anticipated to reach USD 5582.8 million by 2032, at a CAGR of 5.1% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Self-Lubricating Bearings Market Size 2024 |

USD 3750 million |

| Self-Lubricating Bearings Market, CAGR |

5.1% |

| Self-Lubricating Bearings Market Size 2032 |

USD 5582.8 million |

The Self-Lubricating Bearings Market grows through strong demand for maintenance-free, durable, and cost-efficient components across automotive, aerospace, industrial machinery, and renewable energy sectors. Key drivers include the need to reduce downtime, enhance energy efficiency, and meet strict environmental standards. It benefits from wider use in electric vehicles, robotics, and medical devices where precision and reliability are critical. Trends highlight advances in composite and polymer materials, lightweight designs, and customized solutions tailored to specific applications. Expanding adoption in emerging economies and increasing focus on sustainability further strengthen the role of self-lubricating bearings in modern engineering systems.

The Self-Lubricating Bearings Market shows strong regional presence with Asia-Pacific leading through large-scale automotive and industrial growth, followed by Europe with advanced automotive and renewable energy projects, and North America supported by aerospace and defense demand. Latin America and Middle East & Africa display steady adoption across mining, energy, and infrastructure. Key players shaping the market include NSK Ltd., igus GmbH, OILES Corporation, NTN Corporation, Daido Metal Co., Ltd., GGB Bearing Technology, RBC Bearings Incorporated, AMES Group, CSB Sliding Bearings, and GKN Sinter Metals.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- Self-Lubricating Bearings Market size was valued at USD 3750 million in 2024 and is projected to reach USD 5582.8 million by 2032, at a CAGR of 5.1%.

- Strong demand for maintenance-free and durable components drives adoption across automotive, aerospace, machinery, and renewable energy sectors.

- Trends highlight wider use in electric vehicles, robotics, and medical devices requiring precision and reliability.

- Competitive landscape features global leaders focusing on composite innovations, lightweight designs, and tailored bearing solutions.

- Market restraints include high production costs and performance limitations in extreme load or temperature conditions.

- Asia-Pacific leads the market with strong automotive and industrial growth, Europe follows with advanced renewable projects, and North America benefits from aerospace and defense demand.

- Latin America and Middle East & Africa show steady adoption across mining, energy, and infrastructure, while key players such as NSK Ltd., igus GmbH, OILES Corporation, NTN Corporation, and Daido Metal Co., Ltd. shape the competitive space.

Market Drivers

Growing Demand for Maintenance-Free Solutions in Industrial Applications

Self-Lubricating Bearings Market benefits from industries seeking low-maintenance components that extend equipment life. These bearings reduce the need for external lubricants and scheduled servicing. Industrial machinery, construction equipment, and textile systems prefer products that ensure consistent operation under heavy load conditions. It improves productivity by lowering downtime and cutting operating costs for manufacturers. Long service intervals align with lean production models and efficiency goals. The market grows as industrial buyers prioritize durability and reduced maintenance costs.

- For instance, NSK’s EA7‑grease filled bearings underwent 5 000 000 oscillations at a preload of 49 N and oscillation frequency of 30 Hz without failure, demonstrating extended maintenance intervals under heavy micro‑vibration conditions.

Expanding Role in Automotive Systems for Efficiency and Reliability

Self-Lubricating Bearings Market finds strong demand in the automotive sector focused on efficiency. Automotive systems require parts that withstand friction and resist wear in critical environments. Bearings in steering, suspension, and transmission systems deliver reliable performance without frequent servicing. It supports lighter vehicle designs while meeting emission and efficiency targets. OEMs adopt self-lubricating options to extend vehicle lifespan and improve consumer satisfaction. The trend strengthens with electric vehicles where compact and durable bearings are critical.

- For instance, OILES also offers the 500F‑SL1 series for low-speed, mid-load uses. These bearings tolerate up to 5 N/mm² pressure when dry, or 8 N/mm² with periodic lubrication. Velocity limits reach 0.15 m/s dry, and up to 0.25 m/s with lubrication. PV values cap at 0.50 N/mm²·m/s and 0.80 N/mm²·m/s respectively.

Rising Adoption in Aerospace and Defense Applications

Self-Lubricating Bearings Market addresses aerospace and defense needs for components that withstand extreme conditions. Aircraft and military vehicles use bearings that operate in high temperatures and variable loads without failure. It supports long missions by reducing lubricant dependency in inaccessible areas. Manufacturers adopt advanced composite and polymer-based bearings to meet strict safety standards. The technology ensures consistent reliability for both civilian and defense aircraft. Market growth follows increased demand for lightweight, maintenance-free, and high-performance systems.

Increased Focus on Energy Efficiency and Sustainable Design

Self-Lubricating Bearings Market aligns with global interest in energy-efficient and sustainable engineering practices. Bearings lower friction losses, which reduces energy use across mechanical systems. It plays a role in meeting stricter energy regulations for industrial and transport equipment. Manufacturers emphasize eco-friendly materials and recyclable composites in product design. This approach supports corporate sustainability initiatives and regulatory compliance. The technology appeals to industries seeking both cost reduction and environmental responsibility.

Market Trends

Increasing Use of Advanced Composite Materials to Enhance Durability

Self-Lubricating Bearings Market shows a trend toward advanced composites that combine strength with reduced weight. Manufacturers design bearings with polymer blends, PTFE, and reinforced resins to extend service life. It improves resistance against wear, corrosion, and extreme temperature variations. These materials ensure performance in demanding sectors such as automotive, aerospace, and heavy machinery. Producers highlight material innovations to differentiate offerings in competitive markets. The shift supports reliable operations while reducing reliance on external lubrication.

- For instance, igus uses advanced composite materials combining polymers, fibers, and solid lubricants for high durability. The iglidur® H4 bearing handles surface pressure up to 65 MPa at +20 °C, and still supports 7 MPa at +200 °C. It maintains long-term speeds of 1 m/s rotary, with short-term limits of 1.5 m/s rotary, 1.1 m/s oscillating, and 2 m/s linear.

Rising Integration in Electric Vehicles and Hybrid Platforms

Self-Lubricating Bearings Market gains momentum from the adoption of electric and hybrid vehicles. Automakers rely on bearings that minimize friction in compact drivetrains. It enables quieter operation and longer part lifespan in battery-driven systems. Components are designed for reduced maintenance, aligning with the lifecycle of EV platforms. Manufacturers target steering, suspension, and motor assemblies with specialized designs. Growth in EV adoption strengthens demand for self-lubricating bearing technologies across global markets.

- For instance, Daido Metal’s self‑lubricating bearings target EV needs with compact, high‑durability designs. The DAIDYNE DDL05 metal‑polymer bearing operates from –200 °C to +280 °C, supports specific loads up to 49 MPa, and slides at speeds up to 60 m/min, with friction coefficients ranging 0.03 to 0.2 μ.

Expanding Application in Renewable Energy Infrastructure

Self-Lubricating Bearings Market benefits from renewable energy projects that require durable and low-maintenance parts. Wind turbines and solar tracking systems incorporate these bearings to minimize service needs. It withstands high load variations and harsh environmental conditions, ensuring stable energy output. Engineers prefer designs that operate reliably in remote or offshore sites. Reduced lubricant use supports sustainability objectives in the energy sector. The trend reflects growing investment in reliable components for clean power systems.

Growing Preference for Customized and Application-Specific Designs

Self-Lubricating Bearings Market reflects rising demand for customized solutions tailored to end-user requirements. Industries request bearings engineered for specific load, speed, and temperature profiles. It ensures optimal performance and efficiency in specialized environments. Manufacturers offer varied shapes, coatings, and embedded lubrication technologies to meet diverse needs. The focus on customization strengthens partnerships between suppliers and OEMs. This trend underscores the role of tailored designs in expanding industry adoption.

Market Challenges Analysis

High Production Costs and Complex Manufacturing Requirements

Self-Lubricating Bearings Market faces challenges due to high production costs and advanced manufacturing needs. Specialized materials such as composites, polymers, and alloys demand precision engineering and strict quality control. It increases overall expenses for producers and limits cost competitiveness against conventional bearings. Complex fabrication processes also require investment in technology and skilled labor. Smaller manufacturers struggle to match scale and efficiency of larger players. These barriers restrict wider adoption in cost-sensitive industries and emerging markets.

Performance Limitations in Extreme Operating Conditions

Self-Lubricating Bearings Market encounters constraints in applications with extreme loads or harsh environments. While advanced designs improve durability, certain systems still need external lubrication for optimal reliability. It creates hesitation among industries that prioritize consistent performance in high-risk operations. Aerospace, heavy-duty mining, and marine sectors often demand higher tolerance levels than current designs provide. Failures under intense stress can increase operational risks and maintenance costs. Market growth depends on continued innovation to address these technical performance gaps.

Market Opportunities

Expansion Potential in Emerging Industrial and Automotive Sectors

Self-Lubricating Bearings Market presents opportunities through rising demand in emerging economies and industrial hubs. Rapid urbanization and infrastructure growth create higher need for durable, maintenance-free components. It supports machinery in construction, mining, and manufacturing sectors where operational efficiency is critical. Automotive growth in Asia and Latin America further boosts adoption of reliable bearing solutions. Electric and hybrid vehicle platforms highlight strong potential for integration across drivetrains and auxiliary systems. The expanding footprint of OEMs in these regions strengthens long-term market penetration.

Advancements in Green Technologies and Sustainable Engineering

Self-Lubricating Bearings Market benefits from opportunities linked to sustainability and green technology initiatives. Industries seek solutions that minimize environmental impact and reduce lubricant waste. It enables compliance with stricter global regulations on emissions and material safety. Renewable energy projects such as wind farms and solar trackers create demand for low-maintenance bearings. Research into recyclable composites and eco-friendly materials opens avenues for innovation. The shift toward sustainable design encourages partnerships between bearing producers and environmentally focused industries.

Market Segmentation Analysis:

By Product Type

Self-Lubricating Bearings Market demonstrates strong adoption across diverse product categories. Bushings dominate due to their wide use in automotive, industrial machinery, and heavy equipment. Plain bearings are valued for simple design and cost efficiency in moderate load applications. Thrust bearings serve critical roles in systems requiring support for axial loads, particularly in automotive drivetrains and turbines. Linear bearings find increasing demand in robotics and automation where smooth motion is essential. It extends to niche categories such as sliding bearings, which offer specialized solutions in compact systems. This diversity supports a broad range of industries with performance-focused components.

- For instance, AMES’ SELFOIL® sintered bronze bushings feature a porosity of 20–25 % by volume, retain lubricant oil for maintenance-free use, and operate under loads up to 10 MPa with sliding speeds of 8 m/s, while achieving PV values of 10 MPa·m/s and diameter tolerances as precise as IT5.

By Material

Material selection plays a vital role in determining product suitability and lifecycle. Metallic bearings hold the largest share with durability and adaptability across applications. Bronze-based variants excel in high-load environments such as mining and marine equipment. Iron-based solutions are preferred in cost-sensitive industries where moderate performance suffices. Copper-based bearings offer high conductivity and find niche roles in electrical systems. Aluminium alloys provide lightweight options critical for aerospace and automotive platforms. It also includes other materials such as lead composites, which address specific lubrication requirements under controlled conditions.

- For instance, Valvoline developed its Restore & Protect full synthetic motor oil, which in lab tests removed up to 100 % of engine‑killing deposits after four consecutive oil changes, using a modified Sequence IIIH testing method—demonstrating measurable restoration and protection in internal engine surfaces.

By End User

Self-Lubricating Bearings Market expands across multiple end-user industries with varied requirements. Automotive remains a major consumer, integrating bearings in steering, suspension, and transmission assemblies. Industrial machinery applies these solutions in conveyor systems, pumps, and heavy-duty production equipment. Energy and renewables adopt them in wind turbines and solar tracking systems where maintenance-free operation is essential. Medical devices and robotics rely on precise, low-friction components that ensure smooth, sterile performance. It highlights the growing role of self-lubricating technology in next-generation automation and healthcare systems. Broad applicability strengthens its relevance across both traditional and emerging industries.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Segments:

Based on Product Type:

- Bushings

- Plain bearings

- Thrust bearings

Based on Material:

- Metallic Bearings

- Bronze-based

- Iron-based

Based on End-User:

- Automotive

- Industrial machinery

- Energy & renewables

- Medical devices and robotics

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounts for a significant share of the Self-Lubricating Bearings Market, representing nearly 30% of the global market share. The region benefits from advanced automotive manufacturing, aerospace innovation, and strong industrial machinery demand. It is supported by established OEMs and a focus on adopting maintenance-free technologies. The United States leads the region with heavy investment in aerospace, medical devices, and defense programs that require reliable bearing solutions. Canada contributes through renewable energy projects, particularly in wind power where low-maintenance bearings are essential. Mexico expands the market footprint with its growing automotive production hub. Regional growth remains tied to continuous innovation and a strong emphasis on operational efficiency.

Europe

Europe holds about 28% of the global market share and demonstrates strong adoption across automotive, energy, and industrial sectors. The region’s automotive giants in Germany, France, and Italy integrate self-lubricating bearings into high-performance vehicles. It benefits from strict environmental and safety regulations that drive preference for durable, eco-friendly components. Aerospace programs across the UK, Germany, and France further strengthen demand for advanced bearing solutions. The energy sector, particularly wind and solar, sees rising use of self-lubricating bearings for reducing maintenance in remote projects. Eastern Europe also contributes through growing industrial manufacturing, adding to overall regional momentum. Europe remains a critical innovation hub for advanced materials and bearing designs.

Asia-Pacific

Asia-Pacific leads the Self-Lubricating Bearings Market with about 32% of the global market share, making it the largest regional contributor. The region’s dominance stems from rapid industrialization, infrastructure growth, and automotive production in China, India, Japan, and South Korea. It drives demand across automotive, industrial machinery, and energy applications. China leads with large-scale manufacturing and strong investment in renewable energy projects where reliable bearings are crucial. Japan and South Korea focus on robotics, medical devices, and high-precision equipment using advanced bearing technologies. India expands through its automotive and construction sectors, adopting maintenance-free bearings for cost efficiency. Asia-Pacific continues to represent the fastest-expanding hub due to its scale and manufacturing strength.

Latin America

Latin America contributes around 5% of the global market share with steady adoption across automotive, mining, and energy industries. Brazil leads the region with strong automotive production and renewable energy projects. It integrates self-lubricating bearings into wind turbines and industrial machinery. Mexico supports growth through automotive exports, with rising use of advanced components in vehicle manufacturing. Argentina and Chile demonstrate demand from mining equipment and agricultural machinery requiring durable solutions. It benefits from infrastructure modernization that pushes adoption of reliable, low-maintenance bearings. While smaller in scale, Latin America offers long-term opportunities through regional manufacturing expansion and resource-based industries.

Middle East and Africa

Middle East and Africa account for about 5% of the global market share, reflecting niche but expanding demand. The region integrates self-lubricating bearings into oil and gas operations, heavy-duty equipment, and energy projects. Gulf countries invest in infrastructure development and renewable energy initiatives, boosting adoption of maintenance-free technologies. South Africa contributes with mining equipment and industrial applications where durable bearings are vital. It remains a developing region with opportunities for long-term growth as industries diversify beyond traditional energy. Rising focus on industrial automation and renewable projects is expected to enhance regional penetration.

Key Player Analysis

Competitive Analysis

The Self-Lubricating Bearings Market features include NSK Ltd., GKN Sinter Metals, OILES Corporation, igus GmbH, Daido Metal Co., Ltd., CSB Sliding Bearings, AMES Group, RBC Bearings Incorporated, NTN Corporation, and GGB Bearing Technology. The Self-Lubricating Bearings Market is highly competitive, driven by continuous innovation and performance-focused product development. Companies prioritize advanced materials such as composites, polymers, and sintered metals to enhance durability and reduce maintenance requirements. Strong emphasis is placed on tailoring solutions for automotive, aerospace, industrial machinery, and renewable energy applications. Global manufacturers invest in research and development to improve temperature resistance, load capacity, and friction reduction. Competition also centers on expanding distribution networks and strengthening relationships with OEMs to secure long-term contracts. Sustainability and eco-friendly designs are becoming critical differentiators, with firms aligning product strategies to meet stricter environmental standards.

Recent Developments

- In January 2025, Schaeffler introduced the J20G series of current-insulated bearings which use Insutect A coating. Because they protect against electricity well, these bearings are useful in the rail, wind energy and industrial automation areas.

- In July 2024, AMSOIL INC. launched a new synthetic blend motor oil product line for installers. The latest Synthetic-Blend Motor Oil is available in three viscosities and has more than 50% synthetic content. It offers motorists better performance and protection compared to conventional oils.

- In August 2023, Valvoline introduced a new portfolio of Valvoline 4-stroke Full Synthetic Premium Motor Oil for marine and powersports applications. The product range is designed to withstand the high torque and temperatures encountered in four-stroke ATV/UTV and marine motors.

- In June 2023, Shell and Ducati entered into a collaboration to design and produce a new high-performance oil for the Ducati Panigale with a dry clutch. The product uses Shell’s proprietary PurePlus technology and is developed to protect Ducati engines against wear and tear by reducing friction.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Material, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with higher adoption in electric and hybrid vehicles.

- Demand will rise in renewable energy systems such as wind turbines and solar trackers.

- Aerospace and defense sectors will increasingly rely on maintenance-free bearing solutions.

- Robotics and medical devices will create new opportunities for compact, precise designs.

- Advances in polymer and composite materials will improve performance in harsh environments.

- Industrial automation will boost the need for durable, low-friction components.

- Manufacturers will focus on eco-friendly materials and recyclable bearing solutions.

- Emerging economies will contribute significantly through infrastructure and automotive growth.

- Digital simulation and smart monitoring will enhance product design and reliability.

- Strategic partnerships with OEMs will drive long-term adoption across multiple industries.