Soft Covering Flooring Market Overview:

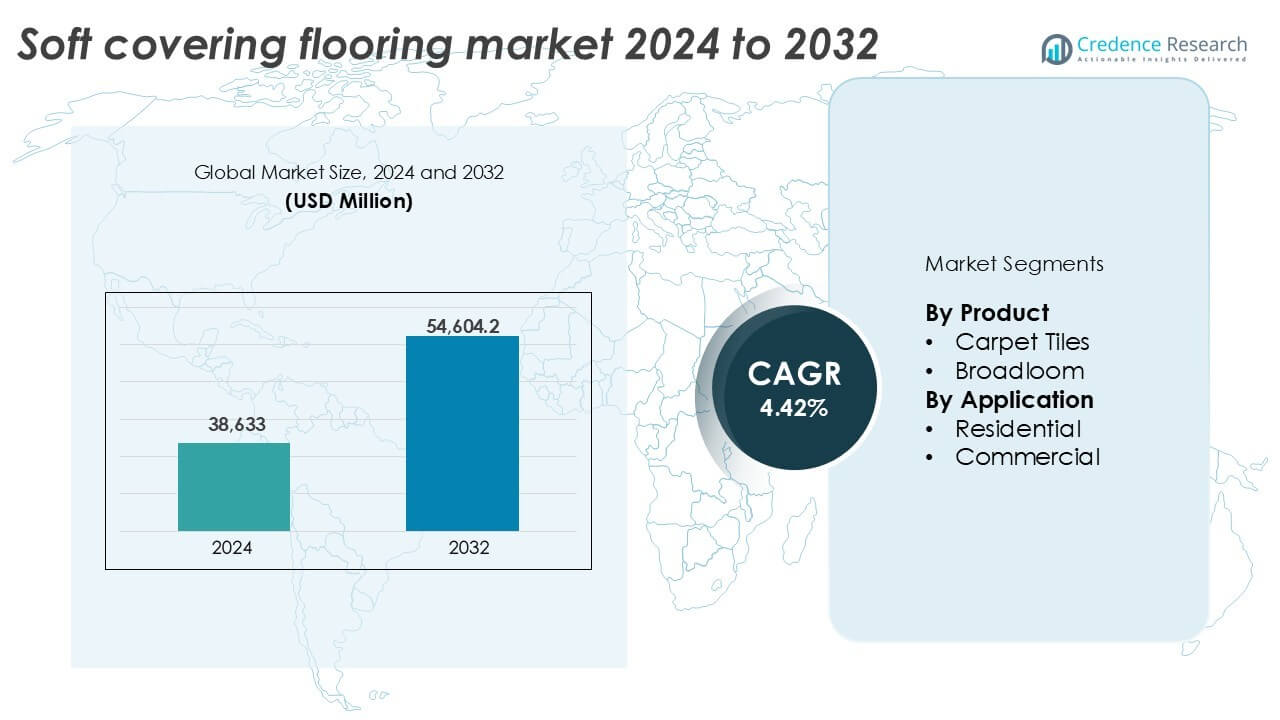

The soft covering flooring market size was valued at USD 38,633 million in 2024 and is anticipated to reach USD 54,604.2 million by 2032, at a CAGR of 4.42% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Soft Covering Flooring Market Size 2024 |

USD 38,633 million |

| Soft Covering Flooring Market, CAGR |

4.42% |

| Soft Covering Flooring Market Size 2032 |

USD 54,604.2 million |

Soft Covering Flooring Market Insights

- Growing residential construction and renovation activities, especially in emerging economies, continue to drive product demand due to comfort, noise insulation, and design flexibility.

- Carpet tiles dominate the product segment with over 55% share, supported by rising adoption in commercial interiors for easy maintenance and modularity.

- Asia-Pacific leads the market with a 31% share, followed by North America at 29% and Europe at 27%, driven by real estate expansion, infrastructure projects, and modernization programs.

- Market growth is challenged by rising raw material and transportation costs, along with increasing competition from hard surface alternatives like luxury vinyl tiles and wood flooring.

Soft Covering Flooring Market Segmentation Analysis:

By Product

The carpet tiles segment holds the dominant share in the soft covering flooring market, accounting for over 55% in 2024. This dominance is driven by growing demand for modular, easy-to-install flooring solutions in high-traffic commercial spaces. Carpet tiles offer greater design flexibility, ease of replacement, and lower installation waste. Their popularity has surged in office buildings, educational institutions, and public infrastructure projects. Broadloom carpets remain in demand for luxury and residential use, but their market share is steadily declining due to higher maintenance needs and installation complexity.

- For instance, Mohawk Industries produces carpet tiles alongside broadloom and hard flooring products from over 43,000 employees worldwide, supporting high‑traffic commercial projects.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Application

The residential segment leads the market with a share exceeding 60% in 2024, supported by rising home renovation trends and growing demand for noise insulation. Soft coverings are preferred for bedrooms, living rooms, and children’s spaces due to comfort and aesthetic appeal. Urban housing expansion and increased disposable income further support this segment’s dominance. However, the commercial segment is growing steadily with increased adoption in hospitality, corporate offices, and healthcare, where durable, modular, and easy-to-maintain carpet tiles are in high demand.

- For instance, Interface’s FLOR modular carpet tiles are marketed for residential living spaces with customizable patterns

Key Growth Drivers

Rising Residential Construction and Home Renovation Activities

The soft covering flooring market benefits from sustained growth in residential construction and remodeling projects. Urbanization across developing economies and demand for affordable housing have triggered new residential developments. In mature markets, increased homeowner investment in interior upgrades drives demand for flooring replacement, especially in bedrooms and living areas where soft materials are preferred. Growing adoption of carpets and carpet tiles for comfort, noise insulation, and thermal benefits boosts market growth. Moreover, design trends favoring warm textures and cozy aesthetics further support this segment. Governments supporting housing schemes, along with post-pandemic emphasis on home improvement, also fuel sales of soft flooring products.

- For instance, flexible modular carpet tiles comprised about 60 percent of the modular carpet tile market unit share in 2024, reflecting growing use in commercial offices and renovation projects, although broadloom carpet remains the dominant type in the overall global carpet market.

Growing Commercial Sector Investments

Commercial buildings increasingly favor soft covering flooring for offices, hospitality, healthcare, and education sectors. Carpet tiles dominate due to their modularity, ease of installation, and low maintenance. Global expansion of coworking spaces, corporate campuses, and hospitality refurbishments enhances flooring demand. Healthcare and senior living facilities prefer soft coverings for slip resistance and underfoot comfort. Sustainable commercial development, especially in green-certified buildings, encourages the use of recyclable and low-VOC carpet materials. The expanding infrastructure in emerging economies further contributes to demand from hotels, shopping centers, and institutional buildings. The need for acoustic control and improved indoor ambiance reinforces usage in open-plan layouts.

- For instance, Tarkett’s DESSO SoundMaster carpet tile improves impact sound insulation by about 8 dB, aiding acoustics in open‑plan offices.

Technological Advancements in Carpet Manufacturing

Innovations in fiber technology and manufacturing processes play a critical role in boosting market growth. Manufacturers now offer stain-resistant, antimicrobial, and water-repellent carpets tailored for high-traffic areas. Modular tile innovations with improved backing systems enhance durability and replacement ease. Eco-friendly production methods using recycled PET bottles and bio-based fibers attract sustainability-conscious buyers. Digital dyeing techniques allow intricate designs with minimal water usage, supporting green compliance. Smart carpets integrated with sensors are emerging in commercial interiors to monitor footfall and space usage. These advancements help manufacturers address performance gaps and expand into newer applications, adding to product differentiation and consumer interest.

Key Trends & Opportunities

Rising Preference for Sustainable and Recyclable Materials

Environmental concerns drive strong interest in sustainable flooring solutions. Consumers and businesses seek carpets made from recycled content, such as nylon and PET bottles, along with recyclable backing systems. Manufacturers focus on closed-loop production systems and certifications like Cradle-to-Cradle, Green Label Plus, and LEED credits. Demand for low-emission, non-toxic carpets is high, especially in schools, healthcare, and homes with children. Companies offering take-back programs and modular carpet designs that minimize waste gain competitive advantage. As green building regulations become stricter across Europe, North America, and parts of Asia-Pacific, suppliers that offer certified eco-friendly products have the opportunity to capture long-term contracts.

- For instance, Interface’s ReEntry program collects used carpet tiles and reuses, recycles, or recovers materials to reduce landfill waste.

Expansion of Online and Omnichannel Retail Strategies

The soft covering flooring market is seeing a strong shift toward digital and omnichannel sales strategies. E-commerce platforms, virtual room visualizers, and remote consultation tools have improved buyer confidence in online carpet purchases. Direct-to-consumer brands offer customization, sample deliveries, and simplified installation guidance. Large retailers are also integrating AI-based design tools to help users visualize flooring outcomes. The convenience of browsing, ordering, and scheduling installation online appeals to younger homeowners. In commercial segments, digital procurement platforms simplify bulk orders and repeat purchases. This trend presents significant opportunity for brands to scale faster and reach wider geographies with lower operational costs.

Key Challenges

Competition from Hard Surface Flooring Alternatives

The increasing popularity of hard surface flooring materials such as luxury vinyl tiles (LVT), engineered wood, and ceramic tiles presents a major challenge. These materials offer durability, water resistance, and aesthetic variety, which appeal to both residential and commercial buyers. LVT in particular mimics the texture of wood or stone while offering easier maintenance and lower lifecycle costs. Many property owners now favor hard surfaces in high-traffic and wet areas like kitchens, hallways, and bathrooms. This shift erodes the market share of soft coverings, especially broadloom carpets, limiting growth in certain segments. Overcoming this trend requires targeted innovation and repositioning.

Rising Raw Material and Transportation Costs

Volatile prices of raw materials such as nylon, polypropylene, and polyurethane foams impact production margins. Global supply chain disruptions and high freight costs further strain operations, especially for imported carpet tiles and materials. In regions where carpets are not locally manufactured, price fluctuations affect both retailers and end users. Manufacturers face cost pressures while trying to maintain competitive pricing and comply with environmental regulations. This challenge is particularly significant for small and mid-sized enterprises. Balancing affordability with quality and sustainability remains a persistent issue in achieving scalable market growth across diverse geographies.

Regional Analysis

North America

North America accounted for nearly 29% of the global soft covering flooring market share in 2024. The region benefits from high demand across residential renovations and commercial office refurbishments. The U.S. drives most of the revenue, with strong uptake of carpet tiles in corporate interiors and hospitality spaces. Homeowners favor broadloom carpets in bedrooms and living rooms for insulation and comfort. Sustainability awareness and LEED-certified projects also fuel demand for recyclable carpet products. Canada shows similar trends, supported by a growing housing market and public infrastructure upgrades. Innovation and omnichannel distribution enhance competitive advantage across key players.

Europe

Europe held approximately 27% of the market share in 2024, supported by strong consumer preference for design-focused and eco-labeled carpet products. Germany, the UK, and France lead demand, driven by housing modernization and commercial retrofits. Stringent regulations promoting indoor air quality and environmental compliance increase demand for low-VOC, recyclable flooring. Modular carpet tiles dominate in corporate and educational buildings, while broadloom remains popular in high-end residential spaces. EU-backed green building mandates further promote sustainable product adoption. Manufacturers also benefit from consumer awareness around health, comfort, and thermal performance. Regional innovation in materials and dyeing technologies strengthens competitiveness.

Asia-Pacific

Asia-Pacific represented the largest share at 31% in 2024, with robust growth across residential and commercial segments. China and India lead in volume demand, driven by rising urbanization, middle-class expansion, and infrastructure investments. Commercial real estate, including office spaces, hospitality, and healthcare facilities, boosts carpet tile adoption. Japan and South Korea favor high-tech, antimicrobial carpet solutions for compact urban housing. Regional manufacturers expand capacity and adopt automation to meet domestic and export demand. Growing e-commerce, rising home improvement spending, and favorable government housing policies further support the region’s leadership in the global soft covering flooring market.

Latin America

Latin America contributed around 7% of the global market share in 2024, with Brazil and Mexico as key contributors. The region shows growing demand for soft covering flooring in mid-range residential units and hospitality refurbishments. Cost-effective broadloom carpets remain popular in residential housing. However, carpet tile adoption is increasing in commercial offices and educational institutions due to ease of installation and maintenance. Economic recovery, urban development, and real estate investments drive demand despite import dependency for some raw materials. Suppliers are gradually shifting toward local production and offering modular, stain-resistant options to meet evolving consumer expectations.

Middle East & Africa (MEA)

The MEA region held a 6% market share in 2024, with growth concentrated in the Gulf Cooperation Council (GCC) countries and South Africa. The hospitality sector, driven by tourism and luxury developments in the UAE and Saudi Arabia, fuels demand for premium carpet flooring. Commercial offices and retail spaces adopt modular carpet tiles for acoustic control and aesthetic value. In residential areas, carpets remain limited to high-income segments due to climatic conditions and cultural preferences. The market faces challenges from hard flooring dominance, but modernization efforts in healthcare, education, and urban housing projects open new opportunities.

Soft Covering Flooring Market Segmentations:

By Product

By Application

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the soft covering flooring market is characterized by the presence of several global and regional players competing on design innovation, sustainability, and product performance. Leading companies such as Mohawk Industries, Shaw Industries, and Tarkett hold significant market share due to their wide distribution networks and extensive product portfolios. These players focus on modular carpet tiles, eco-friendly materials, and digital manufacturing technologies to meet evolving customer preferences. European firms like Forbo and Gerflor emphasize sustainable production and recyclable flooring solutions. Interface Inc. continues to lead in carbon-neutral carpet offerings for commercial applications. Mergers, acquisitions, and strategic partnerships remain key tactics to expand geographic presence and product capabilities. Regional firms increasingly target niche markets with customized offerings and localized supply chains. Innovation in antimicrobial, water-repellent, and low-VOC carpets enhances competitive positioning, while omnichannel sales strategies support market expansion. Intense competition drives continuous product development and pricing pressure across segments.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Dow (U.S.)

- Arkema S.A. (France)

- Beaulieu International Group (Belgium)

- Shaw Industries Group Inc. (U.S.)

- Interface Inc. (U.S.)

- Tarkett (France)

- Sika India Pvt. Ltd. (Switzerland)

- Ashland Inc. (U.S.)

- Gerflor (France)

- Forbo Management SA (Switzerland)

- BASF SE (Germany)

- Fosroc Inc. (U.K.)

- Mohawk Industries, Inc. (U.S.)

Recent Developments

- In 2024, Forbo Flooring Systems announced the launch of its new Surestep Balance range, specifically designed for dementia-friendly environments. This safety flooring complies with Health and Safety Executive (HSE) standards and features eight subtle color options with a minimalist matte finish.

- In 2023, Shaw Industries announced a partnership with Encina to develop a groundbreaking carpet waste recycling program. This collaboration aimed to convert post-consumer carpet waste into valuable products, significantly reducing landfill contributions. Using Encina’s advanced technology, the initiative focused on transforming discarded carpets into sustainable materials for various applications.

Report Coverage

The research report offers an in-depth analysis based on Product, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for modular carpet tiles will rise due to ease of installation and design flexibility.

- Residential renovations will continue driving soft flooring adoption in urban housing.

- Commercial offices and hospitality sectors will increase use of acoustic-friendly soft coverings.

- Sustainable and recyclable carpet materials will gain stronger market traction.

- Technological innovations will enhance stain resistance, durability, and antimicrobial features.

- E-commerce and virtual design tools will expand online flooring sales channels.

- Asia-Pacific will maintain dominance with strong construction and infrastructure growth.

- European demand will focus on eco-label certified and low-VOC carpet products.

- Competitive pressure will push manufacturers to optimize cost and expand product variety.

- Rising preference for hybrid flooring designs may create new growth avenues.