Market Overview:

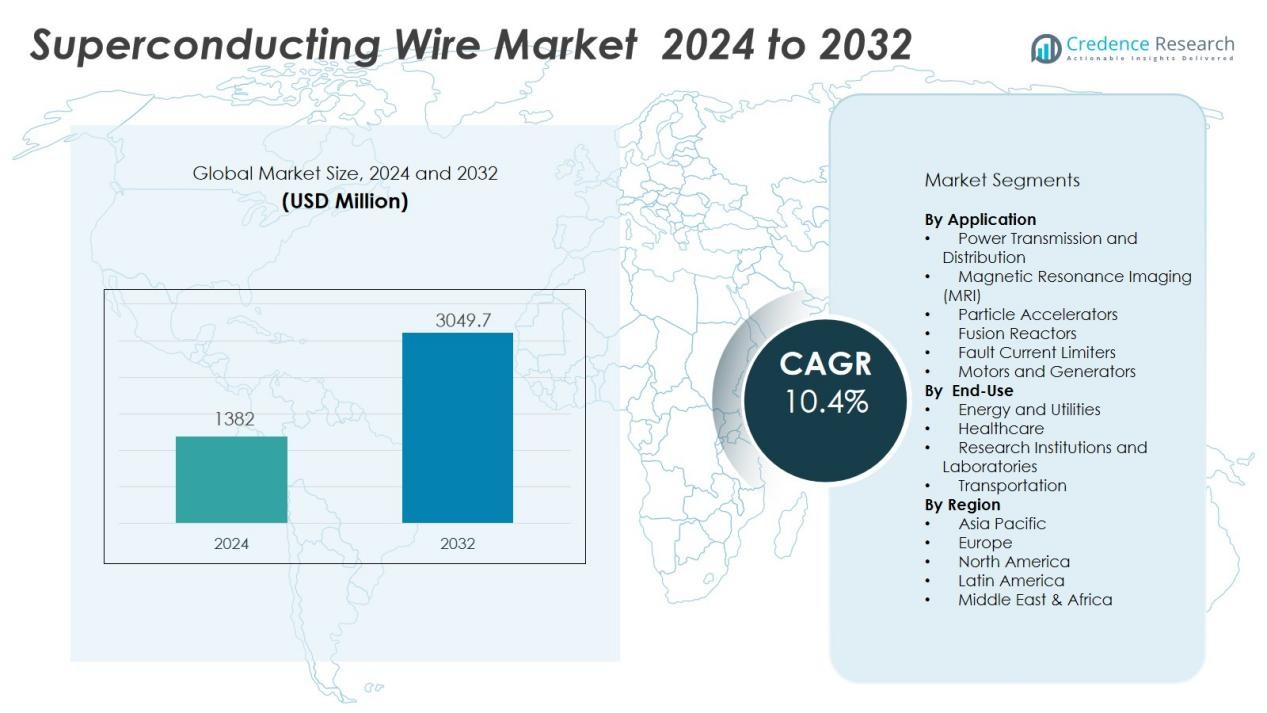

The Superconducting Wire Market size was valued at USD 1382 million in 2024 and is anticipated to reach USD 3049.7 million by 2032, at a CAGR of 10.4 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Superconducting Wire Market Size 2024 |

USD 1382 Million |

| Superconducting Wire Market , CAGR |

10.4 % |

| Superconducting Wire Market Size 2032 |

USD 3049.7 Million |

Key market drivers include increasing investments in upgrading national power grids, accelerating adoption of magnetic resonance imaging (MRI) in the healthcare sector, and expanding research initiatives in particle accelerators and fusion energy. The unique properties of superconducting wires—such as zero electrical resistance and high current-carrying capacity—enable transformative improvements in power transmission efficiency, compact medical devices, and high-performance industrial systems. Government funding and public-private partnerships are further supporting technology commercialization and deployment, especially in projects targeting grid modernization and clean energy.

Regionally, North America leads the superconducting wire market due to established research institutions, significant healthcare infrastructure, and strong federal support for advanced energy projects. Asia-Pacific is rapidly emerging as a growth center, with China, Japan, and South Korea investing heavily in smart grids and scientific research. Europe remains a key market, driven by cross-border power projects and collaborative research programs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The superconducting wire market reached USD 1,382 million in 2024 and is projected to hit USD 3,049.7 million by 2032, supported by a CAGR of 10.4% from 2024 to 2032.

- Strong investments in national power grid upgrades and grid modernization drive steady demand, leveraging superconducting wires for efficiency and low-loss energy transmission.

- Healthcare advances, particularly in MRI technology, continue to spur market growth as hospitals and imaging centers require high-performance superconducting wires for precise diagnostics.

- Expanding research in particle accelerators, fusion reactors, and advanced laboratories increases the need for reliable, high-capacity superconducting wire solutions.

- The shift to clean energy and electric mobility creates new opportunities, with superconducting wires supporting compact renewable energy generators and advanced electric propulsion systems.

- High production costs and complex manufacturing processes remain major challenges, limiting widespread adoption and encouraging ongoing R&D for more cost-effective solutions.

- North America leads the global market with a 37.5% share, while Asia-Pacific rapidly gains ground at 29.2% and Europe holds 25.1%, each region shaped by its own policy support, infrastructure, and research focus.

Market Drivers:

Expansion of Power Infrastructure and Grid Modernization Initiatives:

The superconducting wire market benefits from rising investments in power infrastructure upgrades and grid modernization projects worldwide. Governments and utilities seek advanced solutions to address growing energy demand, minimize transmission losses, and enhance grid reliability. Superconducting wires offer near-zero resistance, which enables highly efficient power transmission across long distances and supports compact substation designs. The market leverages these properties to deliver substantial cost savings and environmental benefits, making it a preferred choice for next-generation electrical networks.

- For instance, ComEs in Chicago integrated AMC’s Resilient Electric Grid (REG) system, which uses high-temperature superconductor cables capable of conducting up to 200 times the electrical current of copper wire of similar size and delivering 62 MVA at 12 kV, significantly increasing grid reliability and performance.

Growth in Advanced Healthcare and Diagnostic Technologies:

Healthcare applications, particularly magnetic resonance imaging (MRI), drive demand for superconducting wires due to their essential role in enabling high-field magnets. Hospitals and imaging centers require more precise and efficient diagnostic tools, and MRI systems using superconducting wires offer superior image quality and operational efficiency. The superconducting wire market capitalizes on these requirements, supporting both upgrades of existing installations and deployment of new MRI systems. Growing healthcare infrastructure in emerging economies further amplifies this trend.

- For instance, Siemens Healthineers incorporated DryCool technology in their latest MRI systems, reducing helium requirements from 1,500 liters to less than 1 liter per machine, and established a facility in the UK to manufacture these low-helium superconducting magnets, which will enable access to advanced MRIs for many more patients globally.

Rising Investments in Scientific Research and Particle Accelerators:

The superconducting wire market responds to increasing investments in large-scale scientific projects, including particle accelerators, fusion reactors, and research laboratories. Superconducting magnets form a core component of these advanced facilities, requiring reliable and high-performance wire solutions. It gains momentum from government and institutional funding, which supports the ongoing expansion of research capabilities. International collaborations further stimulate demand for superconducting wire technologies.

Emergence of Clean Energy and Electric Mobility Applications:

The shift toward clean energy and electrification of transport creates new opportunities for the superconducting wire market. Renewable energy projects, including wind and fusion power, rely on superconducting wires for compact generators and efficient energy transfer. It also finds application in electric propulsion systems, enabling lighter and more powerful electric vehicles, trains, and ships. Ongoing innovation in these sectors accelerates the adoption of superconducting wire solutions globally.

Market Trends:

Technological Advancements in High-Temperature Superconductors and Wire Manufacturing Processes:

The superconducting wire market is witnessing a shift toward high-temperature superconductors (HTS), which offer improved performance at elevated temperatures and reduced cooling requirements. Companies invest in refining manufacturing processes to enhance critical current density, mechanical flexibility, and reliability of HTS wires. Continuous progress in material science supports the development of second-generation HTS wires, such as REBCO and BSCCO, which address challenges of scalability and cost-effectiveness. Manufacturers collaborate with research institutes to streamline production methods and accelerate commercialization of advanced wire solutions. It gains momentum from end users seeking efficient and compact products for energy, healthcare, and industrial applications. This trend supports the expansion of the market into new segments requiring higher operational efficiency and reduced infrastructure footprints.

- For instance, in 2024, University at Buffalo researchers fabricated REBCO-based superconducting wires with a record-breaking critical current density of 190 megaamps per square centimeter (MA/cm²) and a pinning force of 6.4 teranewtons per cubic meter (TN/m³) at 4.2 kelvin, vastly surpassing the performance of previous generations and opening avenues for higher efficiency in energy and fusion applications.

Integration of Superconducting Wires in Renewable Energy, Mobility, and Smart Grid Applications:

The superconducting wire market expands its footprint in sectors driving global sustainability goals, including renewable energy, electric mobility, and digitalized smart grids. Wind turbines, fusion energy pilots, and large-scale energy storage systems utilize superconducting wires for their ability to handle high currents and enable compact system designs. It benefits from ongoing electrification of rail, marine, and urban transport, where superconducting wire technology supports lightweight and efficient propulsion systems. Smart grid projects incorporate superconducting cables to boost transmission capacity and enhance grid stability. Industry stakeholders focus on strategic alliances and demonstration projects to showcase the practical benefits of superconducting wire integration. This trend accelerates the market’s relevance across industries adopting advanced power management and zero-emission initiatives.

- For instance, GE successfully completed trials of its Hydrogenie 1.7-MW low-temperature superconducting (LTS) wind generator, while the EU’s SUPRAPOWER project has demonstrated superconducting generator technology scalable up to 10 MW for offshore wind turbines.

Market Challenges Analysis:

High Production Costs and Complex Manufacturing Processes Limit Widespread Adoption:

The superconducting wire market faces significant challenges related to the high cost of raw materials, complex fabrication techniques, and the need for specialized equipment. Manufacturing processes for both low- and high-temperature superconducting wires require precise control over composition, structure, and purity, which drives up costs. The use of rare earth elements and advanced ceramics further strains production budgets. Limited scalability and low yield rates in current manufacturing lines hinder price reductions, making it difficult for many potential customers to justify investments in superconducting wire systems. These barriers slow the adoption of superconducting wires in commercial and utility-scale applications. Market participants continue to seek cost-effective production methods and material alternatives to address these obstacles.

Stringent Cooling Requirements and Technical Barriers to Commercial Deployment:

Maintaining the ultra-low temperatures necessary for optimal superconducting performance presents another challenge for the superconducting wire market. Most applications require sophisticated cryogenic systems that add operational complexity and ongoing maintenance costs. Equipment reliability, system integration, and the risk of quenching—where a superconductor reverts to a normal conducting state—raise further technical hurdles. Compatibility with existing infrastructure remains limited, particularly in retrofitting conventional power grids or industrial equipment. It must address these engineering challenges to enable broader deployment beyond niche applications. Collaboration among material scientists, equipment manufacturers, and end users will be essential for overcoming these technical and operational barriers.

Market Opportunities:

Integration of Superconducting Wires in Renewable Energy and Smart Grid Infrastructure

Expanding renewable energy deployment and modernization of electric grids create strong opportunities for the superconducting wire market. It can enable highly efficient, high-capacity transmission lines that minimize energy loss and support large-scale integration of wind and solar power into national grids. Superconducting fault current limiters, cables, and storage systems improve grid resilience and reliability while meeting stricter sustainability targets. Governments and utilities prioritize advanced power technologies for urban infrastructure upgrades and rural electrification programs. Strategic investments in smart grid pilot projects demonstrate the potential for superconducting wires to optimize grid operations. Industry stakeholders benefit from partnerships and demonstration sites that validate operational efficiency and cost savings.

Growing Adoption in Advanced Healthcare, Transportation, and Research Applications

The superconducting wire market will capture further opportunities from rising demand for advanced medical imaging, electric mobility, and scientific research. Hospitals and diagnostic centers seek next-generation MRI and NMR systems with higher field strengths and operational efficiency, fueling steady wire demand. Electric vehicle manufacturers and rail operators explore superconducting propulsion and energy storage for lighter, more powerful, and energy-efficient designs. Scientific research, including particle accelerators and fusion energy projects, continues to require high-performance superconducting wire solutions. Industry players expanding their presence in these segments can diversify revenue streams and accelerate technology commercialization.

Market Segmentation Analysis:

By Application:

The superconducting wire market serves a range of critical applications, with power transmission and distribution standing out as a primary segment. Utilities integrate superconducting wires into smart grids and high-capacity power lines to enhance energy efficiency and minimize losses. Magnetic resonance imaging (MRI) represents another major application, where hospitals and diagnostic centers rely on superconducting wires for high-field magnets and superior imaging quality. Particle accelerators and fusion reactors drive demand from the scientific research community, with superconducting wires enabling powerful magnetic fields essential for experimentation and innovation. The market also finds use in fault current limiters, motors, and generators that require high current density and low resistance to support demanding operational environments.

- For instance, over 50,000 of MRI scanners installed worldwide use superconducting magnets, and approximately 4,000 metric tons of niobium-titanium superconducting wire are consumed by MRI manufacturing each year.

By End-Use:

The superconducting wire market addresses diverse end-use sectors. The energy and utilities segment leads in adoption, leveraging superconducting wires to modernize grids and support renewable energy integration. Healthcare follows, where growing demand for advanced MRI systems continues to fuel investments. Research institutions and laboratories represent another core end user, implementing superconducting technology in accelerators, fusion projects, and quantum computing platforms. Transportation is an emerging end-use sector, where the focus is on electric propulsion for railways, marine, and future mobility solutions. The market benefits from tailored product offerings to meet the performance and regulatory needs of each end-use industry.

- For instance, American Electric Power deployed 200 meters of Southwire Triax high-temperature superconducting (HTS) cable at the Bixby Station in Ohio, reliably delivering more than 50 MW of load to approximately 8,600 customers since 2006.

Segmentations:

By Application:

- Power Transmission and Distribution

- Magnetic Resonance Imaging (MRI)

- Particle Accelerators

- Fusion Reactors

- Fault Current Limiters

- Motors and Generators

By End-Use:

- Energy and Utilities

- Healthcare

- Research Institutions and Laboratories

- Transportation

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America :

North America holds a leading share in the superconducting wire market, accounting for 37.5% of total revenue in 2024. The region benefits from federal funding programs, a high concentration of research institutions, and established players advancing superconducting technology. The United States drives demand with large-scale power grid modernization projects, expansion of MRI and NMR installations, and continued investment in scientific research infrastructure. Canada supports market growth through partnerships in clean energy and transportation electrification. The presence of advanced manufacturing capabilities and collaborative public-private initiatives accelerates commercialization and deployment of superconducting wire products. North America’s focus on energy efficiency and resilient infrastructure ensures sustained demand from utilities, healthcare, and research sectors.

Asia-Pacific :

Asia-Pacific holds a 29.2% revenue share in the superconducting wire market and demonstrates the fastest growth trajectory globally. China, Japan, and South Korea lead regional activity, with ambitious national programs in smart grid development, renewable energy integration, and fusion research. Major government investments target local manufacturing, driving innovation in high-temperature superconductors and cost-effective production techniques. It captures demand from rapid urbanization, large-scale healthcare investments, and the build-out of transportation electrification projects. Regional manufacturers increasingly supply international projects, boosting the global competitiveness of Asia-Pacific suppliers. Strong collaboration between universities, research institutes, and technology providers propels technical advances and market penetration.

Europe :

Europe secures a 25.1% share of the superconducting wire market, building on its tradition of scientific excellence and integrated infrastructure. The region features high-profile collaborations such as the European Organization for Nuclear Research (CERN) and multinational grid interconnection projects that require advanced superconducting solutions. Leading economies including Germany, France, and the United Kingdom support the sector through funding for quantum technologies, particle physics, and medical imaging. It benefits from an established network of academic and commercial partnerships that foster knowledge transfer and supply chain development. The European Union’s emphasis on sustainable energy and grid resilience further fuels the adoption of superconducting wires in utility and industrial applications.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- LS Cable and System

- MagForce

- Siemens

- KMel Robotics

- Zhejiang University

- Hitachi

- Shenyang Yuanda Industrial

- Taiwan Semiconductor Manufacturing Company

- Superconductor Technologies

- Western Superconducting Technologies

- Nexans

Competitive Analysis:

The superconducting wire market features strong competition among established multinational corporations and emerging innovators. Major players such as LS Cable and System, Siemens, Hitachi, MagForce, and Taiwan Semiconductor Manufacturing Company invest heavily in research and development to advance wire performance and reduce production costs. It sees dynamic participation from specialized firms like KMel Robotics and Shenyang Yuanda Industrial, as well as leading academic contributors including Zhejiang University. These companies focus on expanding their global footprint, securing patents, and building strategic alliances to strengthen their market positions. The landscape demands ongoing innovation in high-temperature superconductors and improved scalability to address the needs of energy, healthcare, and research sectors. Industry leaders drive progress through continuous product launches and close collaboration with technology partners, research institutions, and end users.

Recent Developments:

- In July 2025, LS Cable & System launched Korea’s first high-flex industrial USB cable, engineered to withstand over 1 million repetitive movements and targeted at the industrial automation sector.

- In June 2025, Siemens Digital Industries Software released a significant update to its NX and NX X platforms, introducing the “AI Copilot,” an AI-powered natural language interface that accelerates CAD learning and design productivity.

- In September 2024, Hitachi completed the acquisition of MA micro automation GmbH to expand its automation and robotics solutions in advanced manufacturing.

Market Concentration & Characteristics:

The superconducting wire market features moderate concentration, with several global leaders and niche innovators driving competition. It presents high entry barriers due to complex technology, significant capital requirements, and the need for advanced manufacturing expertise. Leading companies invest in research and development to enhance product performance and lower costs, while smaller firms often specialize in customized solutions or specific end-use sectors. Strategic alliances, licensing agreements, and joint ventures are common, supporting rapid technological advancement and market expansion. The market is characterized by strict quality standards, long development cycles, and close collaboration between manufacturers, research institutions, and end users to address evolving application demands.

Report Coverage:

The research report offers an in-depth analysis based on Application, End-Use and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Expansion of smart grid initiatives propels demand for superconducting cables and fault current limiters.

- Healthcare operators deploy higher‑field MRI and NMR systems using advanced superconducting wire solutions.

- Research facilities and fusion energy projects adopt superconducting magnets at larger scale.

- Manufacturers develop cost‑effective high‑temperature superconductors with improved mechanical flexibility and performance.

- Transport electrification gains momentum, with superconducting propulsion systems emerging for rail, marine, and EV applications.

- Renewable energy developers integrate superconducting generators and compact energy storage systems.

- Industry partnerships and public‑private projects validate pilot deployments and accelerate commercial adoption.

- Supply chains move toward vertically integrated production models to reduce lead times and control material quality.

- Regulatory bodies support grid modernization and green energy initiatives, creating funding opportunities for deployment.

- Industry convergence with digital monitoring, cryogenic management systems, and AI‑based diagnostics increases operational reliability.