Market Overview

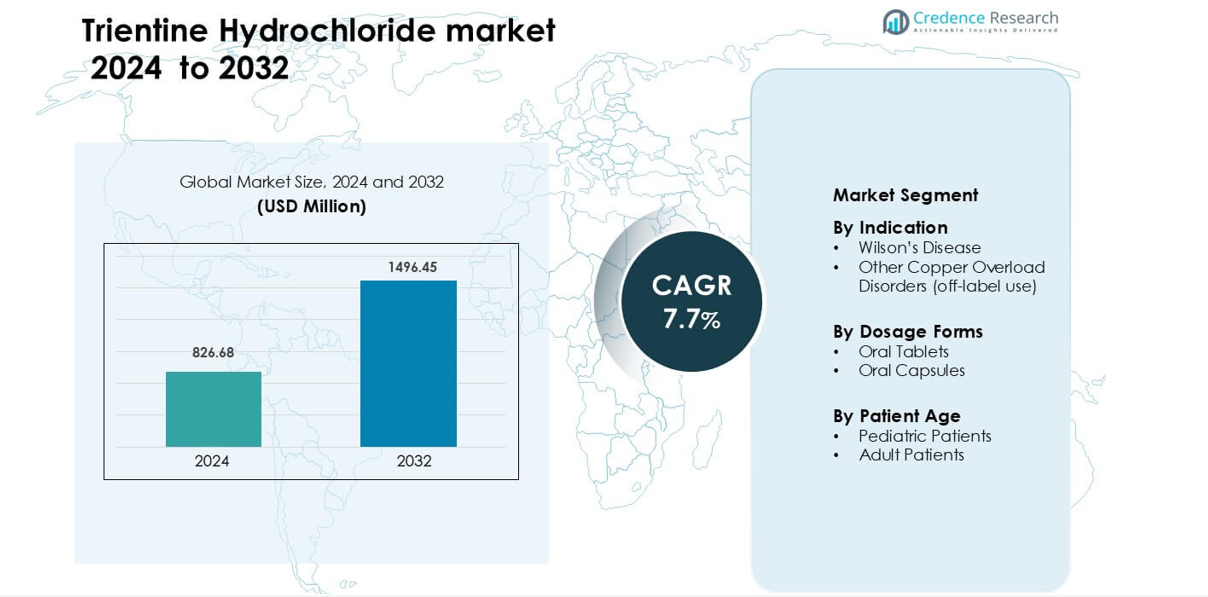

Trientine Hydrochloride market was valued at USD 826.68 million in 2024 and is anticipated to reach USD 1496.45 million by 2032, growing at a CAGR of 7.7 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Trientine Hydrochloride Market Size 2024 |

USD 826.68 million |

| Trientine Hydrochloride Market, CAGR |

7.7% |

| Trientine Hydrochloride Market Size 2032 |

USD 1496.45 million |

North America leads the Trientine Hydrochloride market with 42% share in 2024, driven by strong diagnosis rates, broad insurance coverage, and established rare-disease treatment pathways. Key players such as Curia, Valeant Pharmaceuticals International Inc, Apicore, Green Stone Swiss Co. Ltd, Biophore India Pharmaceuticals Pvt Ltd, SMIQ Pharma, Dasami Lab, Sigma-Aldrich Co. LLC, SGPharma Pvt Ltd, and Apino Pharma shape the competitive landscape through reliable manufacturing, high-purity API supply, and regulatory compliance. These companies focus on consistent production quality, stable global distribution, and formulation improvements to support long-term chelation therapy, reinforcing the region’s leadership in overall market adoption.

Market Insights

- Trientine Hydrochloride market was valued at USD 826.68 million in 2024 and is anticipated to reach USD 1496.45 million by 2032, growing at a CAGR of 7.7 % during the forecast period.

- Demand rises due to growing diagnosis of Wilson’s Disease and strong adoption of safer chelation therapies, with the Wilson’s Disease segment leading with the highest share.

- Key trends include earlier intervention, improved rare-disease screening, and formulation enhancements that support long-term adherence across adult and pediatric groups.

- The competitive landscape is shaped by companies such as Curia, Apicore, Valeant Pharmaceuticals, Biophore India, and Sigma-Aldrich, all focusing on high-purity production and stable global supply.

- North America holds 42% share, followed by Europe at 30% and Asia Pacific at 20%, reflecting strong specialist access and established reimbursement systems supporting Trientine Hydrochloride adoption.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Indication

Wilson’s Disease holds the largest share in 2024 due to its status as the primary approved use for Trientine Hydrochloride. Demand grows as more patients shift from penicillamine because of better tolerance and fewer adverse reactions. Rising diagnosis rates, wider newborn screening programs, and improved clinical guidelines also support this segment. Off-label use for other copper overload disorders expands slowly as physicians adopt chelation therapy for rare metabolic conditions with limited alternative treatments.

- For instance, Orphalan’s CHELATE phase 3 trial of trientine tetrahydrochloride enrolled 53 adults with Wilson disease across 15 centers in nine countries to compare maintenance therapy outcomes with penicillamine.

By Dosage Forms

Oral tablets lead this segment in 2024 because prescribers prefer stable dosing, easier titration, and better patient adherence. Tablet formulations gain traction as manufacturers improve bioavailability and reduce pill burden for long-term therapy. Oral capsules grow at a modest pace and remain useful for patients needing flexible dosing or those with swallowing difficulties. Overall adoption across both formats rises as treatment protocols move toward chronic copper chelation with predictable pharmacokinetics.

- For instance, Orphalan is running a Phase I PK study comparing once-daily dosing (900 mg as 3 × 300 mg tablets) versus their current twice-daily regimen (6 × 150 mg tablets per day).

By Patient Age

Adult patients dominate this segment with a higher share in 2024 because Wilson’s Disease is more often diagnosed during late adolescence or early adulthood. Adults also account for most treatment-experienced cases that transition to Trientine Hydrochloride after intolerance to first-line therapies. Pediatric use grows gradually as early screening programs detect copper metabolism disorders at younger ages. Clinicians increase uptake in children due to improved safety profiles and expanding evidence supporting long-term chelation management.

Key Growth Drivers

Growing Diagnosis and Clinical Awareness of Wilson’s Disease

Greater clinical awareness drives faster detection of Wilson’s Disease across major healthcare systems. Physicians now recognize early neurological and hepatic signs, leading to quicker referrals and standardized diagnostic workups. Wider access to genetic testing and serum ceruloplasmin assessments increases confirmed cases, expanding the pool of patients eligible for Trientine Hydrochloride therapy. Screening programs in schools and pediatric clinics also capture silent cases before organ damage progresses, improving treatment outcomes. As early diagnosis becomes routine, long-term chelation therapy gains importance, increasing reliance on safer, better-tolerated drugs. Hospitals upgrade diagnostic pathways, reducing missed or late-stage cases, which supports sustained adoption of Trientine Hydrochloride as a consistent treatment option across both new and previously untreated patients.

- For instance, in a multicenter Spanish cohort of 153 Wilson’s disease patients followed across 32 hospitals, genetic testing was performed in 56.6% of the cases, and among those tested, 83.9% had detectable ATP7B mutations.

Shift Toward Safer and Tolerable Chelation Therapies

The market experiences strong growth as clinicians move away from penicillamine due to its higher adverse-event burden. Trientine Hydrochloride benefits from this shift because it offers better long-term tolerability and fewer autoimmune reactions, making it a preferred second-line and maintenance therapy. Patients undergoing lifelong chelation respond better when therapy does not cause significant metabolic stress or dermatologic complications. As clinical guidelines emphasize continuous copper control, safer chelators gain more traction across adult and pediatric groups. Pharmaceutical developers support this trend by refining formulations with improved stability and adherence profiles. This steady transition toward patient-friendly therapies strengthens confidence in chronic use and expands the market’s overall treatment base.

- For instance, in a real-world long-term study of 77 Wilson’s Disease patients switched from penicillamine to trientine-2HCl, the mean duration of trientine therapy was 8 years, and only 12 patients (≈ 15.6 %) discontinued due to adverse events — much lower than typical penicillamine drop-out rates.

Regulatory Incentives and Improved Treatment Access

Regulatory frameworks encourage wider access to therapies for rare metabolic disorders through orphan-drug status, accelerated approvals, and expanded reimbursement pathways. These policies reduce financial and administrative barriers for patients requiring lifelong copper chelation. Manufacturers benefit from extended market exclusivity, motivating investment in improved production capacity and quality upgrades. Health authorities also support treatment uniformity through updated clinical guidelines that place Trientine Hydrochloride in key therapy positions. Patient support groups advocate for broader insurance coverage, which further enhances uptake. This combination of regulatory support and policy alignment strengthens market reliability, enabling consistent therapy availability across developed and emerging healthcare systems.

Key Trend and Opportunity

Expansion of Early-Intervention Treatment Models

Healthcare systems increasingly focus on preventive and early-intervention models for managing Wilson’s Disease. Earlier treatment prevents irreversible liver injury and neurological decline, which improves long-term outcomes and increases the duration of therapy. Pediatric screening programs gain traction, identifying cases before progression, leading to earlier introduction of Trientine Hydrochloride. Multidisciplinary care teams also adopt proactive monitoring for carriers and high-risk families, expanding the treated population. As treatment timelines begin earlier in life, lifetime therapy needs grow significantly, reinforcing steady demand for predictable, safe chelation solutions.

- For instance, a genetic screening study in South China tested 38,158 neonates for ATP7B mutations and identified 14 cases of Wilson’s Disease, enabling diagnosis within the first month of life and earlier initiation of chelation.

Rising R&D Activity and Formulation Enhancements

Research efforts intensify around novel drug delivery methods, metabolic monitoring tools, and optimized dosing strategies for copper chelation. Pharmaceutical firms explore formulations with reduced pill burden, enhanced absorption, and improved stability, which increases patient adherence across long treatment cycles. Clinical trials assess combination approaches or sequential therapy models that use Trientine Hydrochloride as a core component. Such advancements refine treatment outcomes and elevate therapy standards, creating additional opportunities for market expansion while improving clinician confidence in the product’s long-term safety profile.

- For instance, scientists have developed liposome-based delivery systems for trientine (TETA) with vectorized liposomes (~ 140–170 nm in size) that achieved up to a 16-fold greater brain uptake in rats compared to free TETA, suggesting a promising strategy to cross the blood-brain-barrier and better target neurological copper deposition.

Growing Access in Emerging Healthcare Markets

Emerging countries strengthen diagnostic infrastructure, invest in genetic testing capabilities, and expand specialist training in hepatology and neurology. These improvements increase detection rates for Wilson’s Disease and raise demand for approved chelation therapies. Governments introduce broader reimbursement models for rare-disease treatments, reducing financial barriers for families. Expanding supply chains and improved drug distribution networks also enhance availability. As awareness and affordability rise, new patient populations gain access to Trientine Hydrochloride, opening significant growth opportunities outside traditional markets.

Key Challenge

Underdiagnosis and Limited Awareness in Low-Resource Regions

Many low-resource regions still lack structured diagnostic protocols and specialist access, causing delayed or missed diagnoses of Wilson’s Disease. Patients often present with advanced symptoms, reducing therapeutic effectiveness and limiting market penetration. Primary care physicians may not recognize early signs, and limited screening infrastructure restricts early detection. These constraints compress the potential treatment window and cap patient numbers eligible for long-term chelation therapy. The resulting geographic imbalance remains a major barrier to global market expansion.

High Dependence on Long-Term Treatment Adherence

Trientine Hydrochloride requires strict adherence to daily dosing schedules to maintain copper control. Missed doses or treatment interruptions can trigger rapid copper accumulation, leading to serious hepatic or neurological complications. High pill burden and lifelong therapy expectations challenge patient commitment, especially in adolescents and young adults. Poor adherence reduces treatment effectiveness and limits real-world outcomes, creating a major barrier for sustained market growth. Strengthening patient education and improving formulation convenience remain essential to overcoming this challenge.

Regional Analysis

North America

North America holds about 42% share of the Trientine Hydrochloride market in 2024, supported by strong diagnostic capacity and widespread specialist access. High clinical awareness, early screening adoption, and established orphan-drug reimbursement drive consistent treatment uptake. The U.S. leads regional demand as most Wilson’s Disease centers follow standardized guidelines favoring safer chelators. Canada contributes steady growth through improved genetic testing availability and reliable reimbursement coverage. Strong advocacy groups and active research networks reinforce North America’s role as the dominant regional market.

Europe

Europe accounts for roughly 30% share of the global market, driven by structured healthcare systems and comprehensive screening protocols. Germany, the U.K., France, and Italy remain the largest adopters, supported by strong reimbursement and uniform treatment guidelines that promote Trientine Hydrochloride use for penicillamine-intolerant patients. High physician awareness and widespread access to metabolic and liver-disease specialists contribute to early diagnosis and long-term therapy adherence. Growing pediatric screening efforts and Europe-wide clinical research strengthen the region’s stable market contribution.

Asia Pacific

Asia Pacific holds close to 20% share and represents the fastest-growing region due to expanding diagnostic infrastructure and improved awareness of copper metabolism disorders. Japan and South Korea lead uptake with advanced clinical systems, while China and Australia show accelerating demand supported by better testing access and specialist training. Many Southeast Asian nations still experience underdiagnosis, but investments in rare-disease programs continue to reduce gaps. Large population size, growing affordability, and rising screening rates position Asia Pacific as a key future growth contributor.

Latin America

Latin America represents about 5% share, supported by improving treatment availability in Brazil, Mexico, Argentina, and Chile. Major urban hospitals continue to adopt better diagnostic pathways, enabling earlier detection of Wilson’s Disease. Although gaps in reimbursement and uneven healthcare access persist, targeted rare-disease funding and improved supply chains enhance uptake. Gradual expansion of genetic testing and specialist training drives steady growth across the region.

Middle East & Africa

Middle East & Africa hold nearly 3% share, reflecting limited screening infrastructure and low awareness in many countries. The Gulf region, especially Saudi Arabia and the UAE, leads adoption because of better specialist access and strong healthcare investment. Several African regions still face challenges in diagnosis and treatment availability. However, rare-disease initiatives, improved import channels, and expanding clinical capabilities help increase adoption slowly, supporting modest but consistent market growth.

Market Segmentations:

By Indication

- Wilson’s Disease

- Other Copper Overload Disorders (off-label use)

By Dosage Forms

- Oral Tablets

- Oral Capsules

By Patient Age

- Pediatric Patients

- Adult Patients

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Trientine Hydrochloride market features a moderately consolidated competitive landscape shaped by active participation from manufacturers, API suppliers, and specialty pharmaceutical companies. Firms focus on maintaining high production quality, regulatory compliance, and consistent global supply to serve long-term Wilson’s Disease therapy needs. Key players strengthen their position by expanding formulation capabilities, enhancing manufacturing purity levels, and securing strategic approvals under orphan-drug pathways. Companies also invest in strengthening distribution networks to improve availability in emerging markets where diagnostic capacity is rising. Research partnerships support ongoing refinement of chelation therapy standards, enabling manufacturers to reinforce clinical acceptance. Competitive differentiation often centers on production reliability, stability enhancements, and adherence-supportive formulations, reflecting the chronic nature of treatment. As screening expands globally, companies enhance capacity planning and regulatory alignment to meet growing therapeutic demand while maintaining consistent product quality.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Curia

- Valeant Pharmaceuticals International Inc

- Apicore

- Green Stone Swiss Co. Ltd

- Biophore India Pharmaceuticals Pvt Ltd

- SMIQ Pharma

- Dasami Lab

- Sigma-Aldrich Co. LLC

- SGPharma Pvt Ltd

- Apino Pharma

Recent Developments

- In 2025 Curia lists Trientine HCl in its Generic APIs / API Catalog and indicates a US DMF regulatory submission on its Trientine HCl product page (site content carries a 2025 copyright). Public Curia materials show Curia as an API developer/manufacturer for Trientine HCl.

- In Nov 2023, Biophore India Pharmaceuticals Pvt Ltd: Biophore presented at CPHI Barcelona (video dated 20 Nov 2023) and lists Trientine Hydrochloride in its product offering with US DMF Available on its CPHI product page.

Report Coverage

The research report offers an in-depth analysis based on Indication, Dosage Forms, Patient Age and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will grow as global diagnosis of Wilson’s Disease increases.

- Earlier screening will expand the eligible patient pool for long-term chelation therapy.

- Improved formulations will reduce pill burden and support stronger treatment adherence.

- Adoption will rise as clinicians continue shifting toward safer alternatives to penicillamine.

- Expansion of pediatric screening programs will increase early-life treatment demand.

- Regulatory incentives will support faster approvals and broader treatment access.

- Emerging markets will see higher uptake as diagnostic infrastructure improves.

- Supply chain upgrades will enhance global availability and reduce treatment gaps.

- Research advancements will refine dosing strategies and strengthen clinical outcomes.

- Growing investment in rare-disease management will reinforce sustained market expansion.