Market Overview

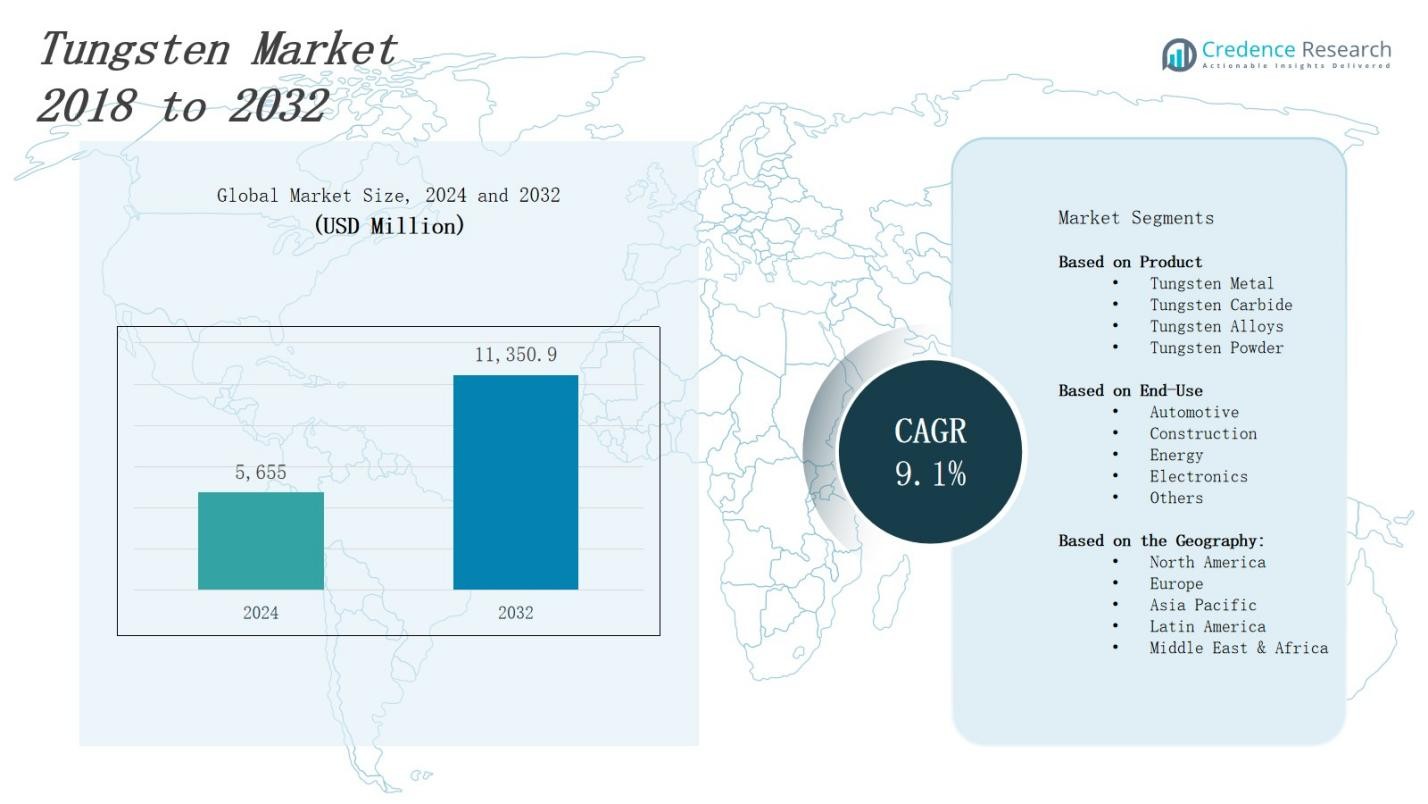

The tungsten market is projected to grow from USD 5,655 million in 2024 to USD 11,350.9 million by 2032, expanding at a CAGR of 9.1%.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Tungsten Market Size 2024 |

USD 5,655 Million |

| Tungsten Market, CAGR |

9.1% |

| Tungsten Market Size 2032 |

USD 11,350.9 Million |

The tungsten market grows driven by rising demand from the automotive, aerospace, and electronics industries, where tungsten’s high melting point and durability are critical. Increasing adoption in cutting tools and wear-resistant applications fuels market expansion. Technological advancements in powder metallurgy and tungsten alloys enhance performance and cost efficiency. Growth in construction and energy sectors further supports demand. Trends include the development of eco-friendly and sustainable tungsten extraction methods and recycling initiatives to address supply constraints. Additionally, manufacturers focus on producing specialized tungsten products for emerging applications such as 3D printing and advanced electronics, reinforcing market growth.

The tungsten market shows strong geographical diversity, with Asia-Pacific leading at 55%, followed by Europe at 20%, North America at 15%, and the Rest of the World at 10%. Asia-Pacific dominates due to vast reserves and industrial growth, while Europe and North America focus on advanced manufacturing and sustainability. Key players driving the market include CMOC Group Ltd., Sandvik AB, Kennametal Inc., Plansee SE, China Tungsten & Hightech Materials Co. Ltd., and Masan High-Tech Materials Corporation. These companies leverage innovation and strategic partnerships to maintain global competitiveness.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The tungsten market is projected to grow from USD 5,655 million in 2024 to USD 11,350.9 million by 2032, expanding at a CAGR of 9.1%.

- Rising demand from automotive, aerospace, and electronics industries drives market growth, leveraging tungsten’s high melting point and durability.

- Technological advancements in powder metallurgy and tungsten alloys enhance performance and cost efficiency, supporting wider application.

- Sustainability trends encourage eco-friendly extraction methods and recycling initiatives to mitigate supply constraints.

- Asia-Pacific leads with 55% market share, followed by Europe (20%), North America (15%), and Rest of the World (10%), reflecting diverse regional demand and production capacities.

- Supply chain constraints and geopolitical risks create vulnerabilities, requiring efforts to diversify sources and manage regulatory hurdles.

- High production costs and stringent environmental regulations challenge market expansion, necessitating investment in cleaner technologies and operational efficiencies.

Market Drivers

Rising Demand in Automotive and Aerospace Industries

The tungsten market benefits from increasing demand in automotive and aerospace sectors due to tungsten’s superior heat resistance and strength. It plays a crucial role in manufacturing cutting tools, electrical contacts, and aerospace components that require high durability under extreme conditions. Growth in lightweight and fuel-efficient vehicle production boosts tungsten consumption for engine parts and wear-resistant tools. Expanding aerospace activities worldwide also drive demand for tungsten-based alloys, strengthening market growth.

Expansion in Electronics and Electrical Applications

The tungsten market grows due to its essential use in electronics, particularly in semiconductors, filaments, and electrical contacts. It offers excellent conductivity and high melting points, making it ideal for various electronic components. The rise in consumer electronics, IoT devices, and industrial automation fuels tungsten consumption. It supports development of miniaturized and high-performance electronic products, maintaining steady market demand across multiple regions globally.

- For instance, Kennametal, a major manufacturer of tungsten-based materials, supplies tungsten carbide powders used in manufacturing high-performance cutting tools and electrical components critical to industrial automation systems.

Advancements in Manufacturing and Powder Metallurgy

Technological progress in powder metallurgy and alloy production strengthens the tungsten market by improving product quality and reducing costs. These advancements enable the production of complex tungsten components with enhanced performance characteristics. Manufacturers increasingly adopt advanced fabrication techniques to meet stringent industry standards. It allows tungsten to penetrate new applications, including 3D printing and specialized tooling, which broadens its usage across diverse industries.

- For instance, American Elements has developed advanced tungsten silver alloys using nanostructuring techniques, which improve conductivity and high-temperature resistance, enabling components for electronics and aerospace applications with superior performance.

Sustainability and Recycling Initiatives

The tungsten market responds to supply challenges by increasing focus on recycling and sustainable extraction methods. It reduces dependence on primary mining, conserves resources, and lowers environmental impact. Companies invest in recovering tungsten from scrap and spent products to ensure steady supply and cost efficiency. Efforts to develop eco-friendly processing techniques reinforce the market’s long-term viability and support circular economy principles, sustaining growth opportunities worldwide.

Market Trends

Increased Adoption of Advanced Tungsten Alloys for Industrial Applications

The tungsten market shows a strong trend toward the development and adoption of advanced tungsten alloys with enhanced mechanical and thermal properties. It meets the growing industrial demand for materials that withstand high temperatures and wear in sectors like aerospace, defense, and automotive manufacturing. Research focuses on improving alloy strength and corrosion resistance, which expands tungsten’s applicability. Manufacturers prioritize innovation to deliver high-performance solutions that address evolving technical challenges across industries.

Growth in Sustainable Practices and Circular Economy Integration

The tungsten market experiences a rising emphasis on sustainability, encouraging the integration of circular economy principles throughout the supply chain. It drives increased recycling efforts and the use of secondary tungsten sources to minimize environmental impact and resource depletion. Companies adopt efficient recovery technologies to reclaim tungsten from industrial scrap and end-of-life products. This trend supports cost reduction and supply security, making tungsten production more environmentally responsible and economically viable over the long term.

- For instance, Sumitomo Electric Group has pioneered tungsten recycling since the 1980s using chemical processes to convert scrap into tungsten trioxide, operating recycling centers in Japan, the U.S., and globally to ensure supply stability and environmental conservation.

Expansion of Tungsten Applications in Emerging Technologies

The tungsten market diversifies with expanding use in emerging technologies such as additive manufacturing, electronics, and renewable energy. It supports 3D printing of complex, high-strength components, enabling rapid prototyping and customized production. Tungsten’s excellent thermal and electrical properties make it ideal for semiconductors, microelectronics, and solar energy devices. This trend reflects the material’s critical role in driving innovation and performance improvement in cutting-edge technological sectors worldwide.

- For instance, Tungsten is a prime material for plasma-facing components in fusion reactors, where Powder Bed Fusion Electron Beam (PBF-EB) technology produces crack-free, high-purity tungsten parts that withstand extreme temperatures.

Strategic Collaborations and Investments to Enhance Market Position

The tungsten market witnesses increased strategic partnerships, mergers, and investments among key players to strengthen product portfolios and expand global reach. It accelerates research and development initiatives, focusing on new tungsten-based materials and applications. Collaborations between mining companies, manufacturers, and technology firms improve supply chain efficiency and innovation capacity. This approach positions companies to respond effectively to market demands and competitive pressures while fostering sustainable growth.

Market Challenges Analysis

Supply Chain Constraints and Geopolitical Risks Impacting Market Stability

The tungsten market faces significant challenges due to supply chain constraints and geopolitical risks concentrated in key producing regions. It depends heavily on a few countries, which creates vulnerability to export restrictions, trade disputes, and political instability. These factors disrupt the steady flow of raw materials, causing price volatility and uncertainty for manufacturers. Efforts to diversify supply sources and develop alternative extraction sites encounter regulatory hurdles and high capital requirements, limiting rapid mitigation of these risks. Market participants must manage these uncertainties to maintain production continuity and meet demand.

High Production Costs and Environmental Regulations Limit Growth Potential

The tungsten market struggles with high production costs driven by energy-intensive mining and processing operations. It faces increasing pressure from stringent environmental regulations targeting emissions, waste management, and land rehabilitation. Compliance costs raise barriers for smaller producers and challenge the economic viability of new projects. Technological improvements partially alleviate these issues but require substantial investment and time to implement. The combination of rising operational expenses and regulatory burdens slows capacity expansion and constrains market growth in several regions globally.

Market Opportunities

Expanding Demand in High-Tech and Emerging Industrial Sectors

The tungsten market presents significant opportunities driven by growing demand from high-tech industries such as aerospace, electronics, and renewable energy. It plays a vital role in manufacturing advanced components that require exceptional heat resistance and durability. Growth in electric vehicle production and development of 5G infrastructure further increase tungsten’s applications. Emerging sectors like additive manufacturing also offer new avenues for tungsten use, enabling customized and lightweight parts. Capitalizing on these trends can unlock substantial market potential and foster innovation.

Advancement in Recycling Technologies and Sustainable Resource Management

The tungsten market benefits from opportunities created by advancements in recycling technologies and sustainable resource management practices. It supports recovery of tungsten from scrap and end-of-life products, reducing reliance on primary sources and lowering environmental impact. Innovations in efficient recycling methods improve material yield and cost-effectiveness, encouraging wider adoption. Companies that invest in circular economy initiatives can enhance supply chain resilience and meet growing regulatory requirements. These efforts provide a strategic advantage and contribute to long-term market sustainability.

Market Segmentation Analysis:

By Product

The tungsten market segments into tungsten metal, tungsten carbide, tungsten alloys, and tungsten powder, each serving distinct industrial needs. Tungsten carbide dominates due to its exceptional hardness and wear resistance, driving demand in cutting tools and machining applications. Tungsten metal supports electrical and lighting industries with its high melting point and conductivity. Tungsten alloys find use in aerospace and defense sectors for their strength and durability. Tungsten powder supplies raw material for various manufacturing processes, maintaining steady demand across segments.

- For instance, Accusharp Cutting Tools Pvt Ltd specializes in customized tungsten carbide metal cutting tools, using advanced equipment to ensure accuracy and a strong logistics network that supports diverse manufacturing sectors with fast delivery and tailored solutions.

By End-Use

The tungsten market divides across automotive, construction, energy, electronics, and other end-use industries, reflecting its broad application scope. It sees substantial demand from the automotive sector, driven by the need for durable engine parts and cutting tools. The construction industry utilizes tungsten in heavy machinery and wear-resistant components. Energy applications include tungsten use in power generation and renewable technologies. Electronics rely on tungsten for semiconductors and electrical contacts. Other industries, such as aerospace and medical, contribute to diversified market growth.

- For instance, W Resources Plc develops tungsten alloys for automotive tooling, skid plates, and chassis weights that provide durable protection and balance in compact volumes.

Segments:

Based on Product

- Tungsten Metal

- Tungsten Carbide

- Tungsten Alloys

- Tungsten Powder

Based on End-Use

- Automotive

- Construction

- Energy

- Electronics

- Others

Based on the Geography:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis

Asia-Pacific

Asia-Pacific leads the tungsten market with a dominant share of 55%. It benefits from abundant tungsten reserves and strong mining activities in countries like China, which controls a significant portion of global production. Growing industrialization, rapid urbanization, and expanding automotive and electronics sectors fuel regional demand. Investments in infrastructure and technological advancements further drive tungsten consumption. The region’s emphasis on manufacturing and export-oriented economies sustains steady growth. It also focuses on developing recycling capabilities to enhance resource efficiency and supply security.

Europe

Europe accounts for 20% of the tungsten market, supported by advanced manufacturing industries and stringent regulatory frameworks promoting sustainable resource use. It demands tungsten primarily for aerospace, automotive, and electronics applications. The presence of established companies specializing in tungsten alloys and powder metallurgy boosts market development. Europe prioritizes innovation in high-performance materials and recycling technologies to reduce dependency on imports. It faces challenges from limited domestic tungsten reserves but offsets this through efficient supply chain management and imports.

North America

North America holds 15% of the tungsten market share, driven by strong industrial bases in the United States and Canada. The region focuses on aerospace, defense, and energy sectors where tungsten’s high durability and thermal resistance are critical. Increasing investments in advanced manufacturing and additive technologies expand tungsten applications. It emphasizes sustainability and recycling programs to ensure steady tungsten supply amid fluctuating raw material availability. The market benefits from government initiatives supporting critical minerals and material innovation.

Rest of the World

The Rest of the World region captures 10% of the tungsten market share, including Latin America, the Middle East, and Africa. Emerging economies in these areas experience growing demand due to expanding automotive, construction, and electronics industries. Limited tungsten production capacity drives reliance on imports from major suppliers. The region invests in mining exploration and processing infrastructure to develop local tungsten resources. It also shows growing interest in recycling and sustainable practices to address supply challenges and environmental concerns.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Kennametal Inc.

- Sandvik AB

- Plansee SE

- China Tungsten & Hightech Materials Co. Ltd.

- CMOC Group Ltd.

- Global Tungsten & Powders Corp.

- Masan High-Tech Materials Corporation

- Umicore N.V.

- Xiamen Tungsten Co. Ltd.

- Chongyi Zhangyuan Tungsten Co. Ltd.

- IMC International Metalworking Companies B.V.

Competitive Analysis

The tungsten market remains highly competitive, driven by a mix of established global players and emerging regional companies. It demands continuous innovation in product quality, alloy development, and sustainable practices to maintain market position. Leading companies focus on expanding production capacities, enhancing recycling technologies, and forming strategic partnerships to secure raw material supply. Market participants invest in research to develop advanced tungsten applications for aerospace, automotive, and electronics industries. Price volatility and supply chain disruptions challenge competitive dynamics, pushing firms to diversify sourcing and improve operational efficiency. It rewards companies that balance cost management with technological advancement while complying with environmental regulations. Overall, the tungsten market emphasizes strategic collaboration and innovation to capture growth opportunities and address evolving industry demands.

Recent Developments

- On May 14, 2024, MHT and MMC announced an agreement for MMC to acquire all shares of H.C. Starck Holding GmbH, a leading producer of tungsten products.

- In December 2023, Sandvik Group finalized the acquisition of Buffalo Tungsten, Inc., a major producer of tungsten metal and carbide powder in North America.

- In February 2025, Spearmint Resources completed the acquisition of the Sisson North Tungsten Project in New Brunswick, Canada.

- On June 27, 2025, United States Antimony announced the acquisition of the Fostung Tungsten Property located in Ontario, Canada.

Market Concentration & Characteristics

The tungsten market exhibits a moderately concentrated structure dominated by key players controlling significant production and supply capacities. It relies heavily on a few major producers, primarily located in Asia-Pacific, which influences pricing and availability worldwide. The market features a blend of upstream mining companies and downstream manufacturers specializing in tungsten powders, alloys, and finished products. It demands continuous innovation to meet evolving industry requirements in aerospace, automotive, and electronics sectors. Competitive dynamics emphasize technological advancements, sustainable practices, and strategic partnerships to secure raw material access. Barriers to entry remain high due to capital-intensive extraction processes and strict environmental regulations. It rewards companies that balance cost management with quality improvement and supply chain resilience. Overall, the tungsten market maintains stable growth driven by demand diversification and increasing adoption of recycled materials to mitigate supply risks.

Report Coverage

The research report offers an in-depth analysis based on Product, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The tungsten market will expand due to rising demand from automotive and aerospace industries.

- It will benefit from growing applications in electronics and renewable energy sectors.

- Manufacturers will adopt advanced powder metallurgy to improve tungsten product performance.

- Recycling and sustainable extraction methods will gain prominence to secure supply chains.

- Emerging technologies like 3D printing will create new opportunities for tungsten use.

- Regional markets, especially in Asia-Pacific, will continue to dominate production and consumption.

- Companies will increase investments in research and development for innovative tungsten alloys.

- Environmental regulations will drive the adoption of cleaner and more efficient production techniques.

- Strategic partnerships and collaborations will strengthen market competitiveness.

- Supply chain diversification will remain a critical focus to reduce geopolitical risks.