Market Overview:

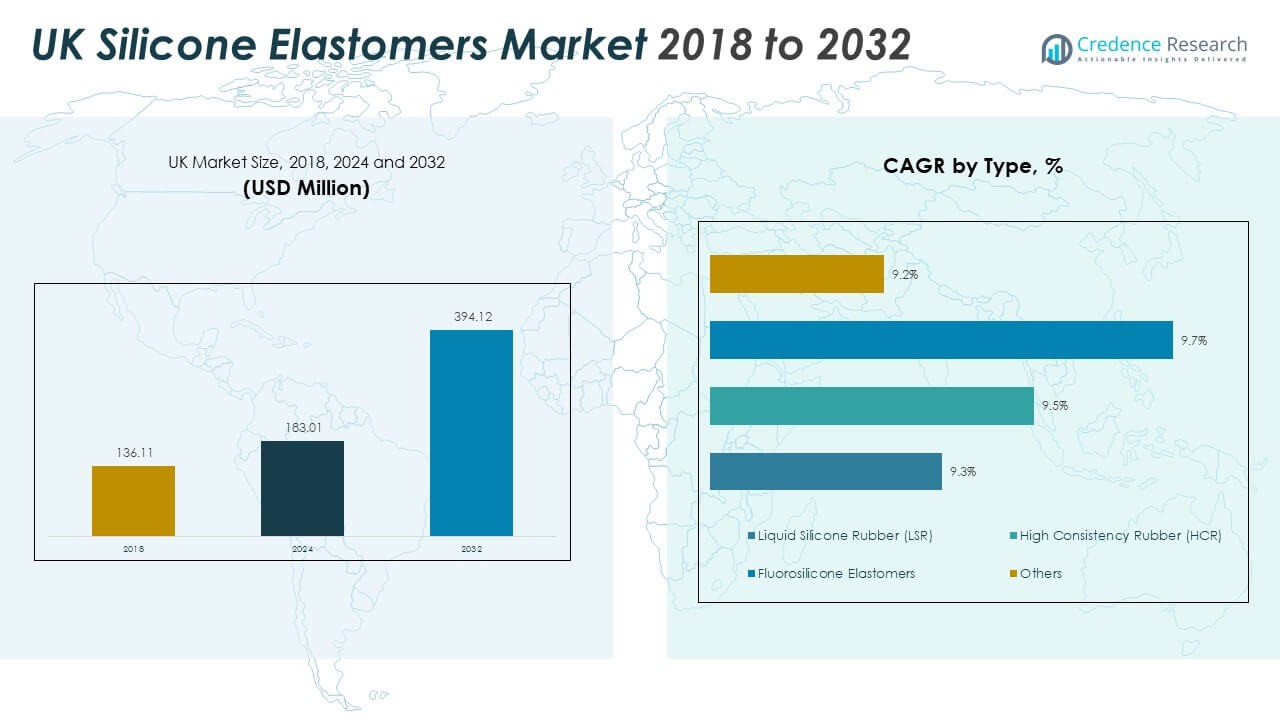

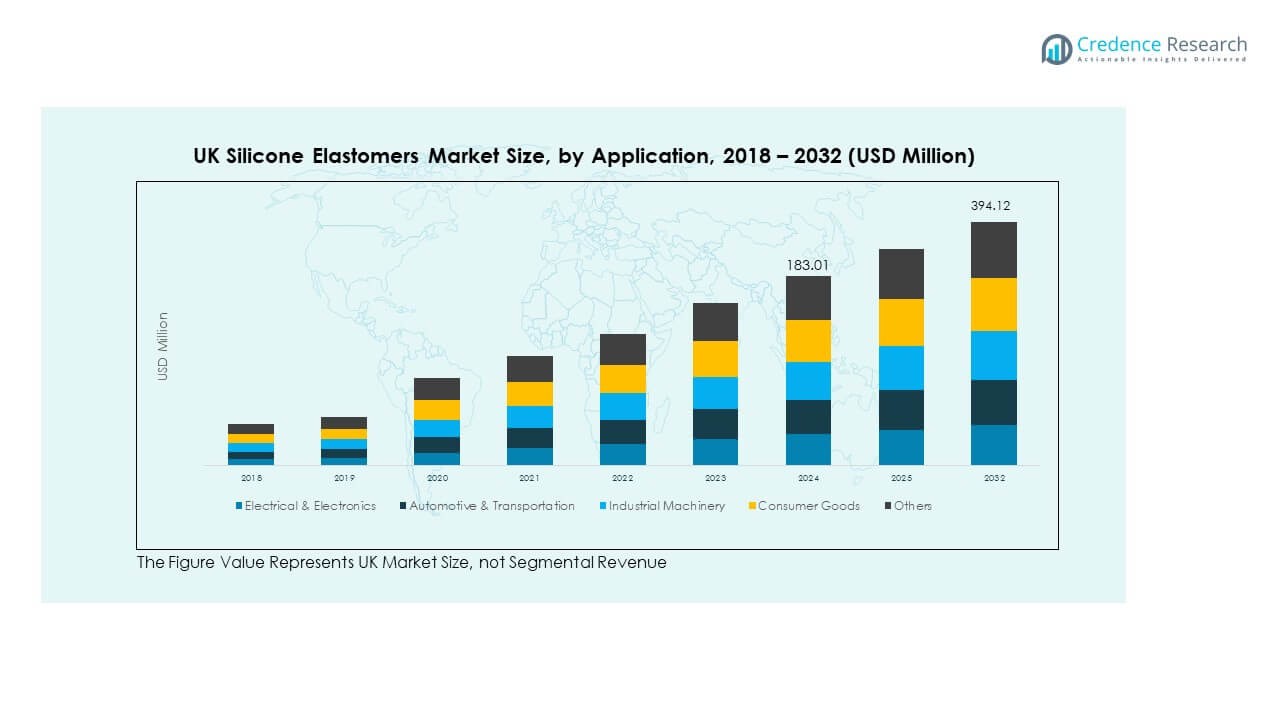

The UK Silicone Elastomers Market size was valued at USD 136.11 million in 2018 to USD 183.01 million in 2024 and is anticipated to reach USD 394.12 million by 2032, at a CAGR of 10.06% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| UK Silicone Elastomers Market Size 2024 |

USD 183.01 Million |

| UK Silicone Elastomers Market, CAGR |

10.06% |

| UK Silicone Elastomers Market Size 2032 |

USD 394.12 Million |

The market is driven by rising adoption in automotive and healthcare sectors due to silicone elastomers’ excellent thermal stability, chemical resistance, and biocompatibility. Automotive manufacturers use silicone materials in gaskets, seals, and insulation for electric vehicles and hybrid systems. Healthcare applications such as catheters, prosthetics, and tubing benefit from their flexibility and sterilization capability. Increasing investment in renewable energy, electronics manufacturing, and sustainable materials further accelerates demand. The market continues to evolve through R&D initiatives focused on performance enhancement and eco-friendly product development.

Regionally, England dominates the UK Silicone Elastomers Market due to its strong manufacturing base and advanced healthcare and automotive industries. Scotland is emerging as a fast-growing region supported by renewable energy expansion and polymer innovation initiatives. Wales and Northern Ireland contribute through industrial and construction-based applications. Strategic R&D investments and the presence of leading producers across southern England enhance innovation capabilities. Regional integration of production facilities and supply chains ensures efficient distribution and material accessibility across the country.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The UK Silicone Elastomers Market was valued at USD 136.11 million in 2018, reached USD 183.01 million in 2024, and is projected to achieve USD 394.12 million by 2032, expanding at a CAGR of 10.06% during the forecast period.

- England holds 58% of the market share, driven by a strong automotive and healthcare base; Scotland follows with 23% due to renewable energy projects, while Wales and Northern Ireland together account for 19%, supported by industrial and construction applications.

- Scotland stands out as the fastest-growing region with a 23% share, supported by investments in renewable infrastructure, offshore wind projects, and advancements in polymer innovation.

- The electrical & electronics segment leads with 28% share, benefiting from increased demand for high-performance insulating materials in energy and communication systems.

- The automotive & transportation segment holds 25% share, driven by expanding electric vehicle production and growing need for reliable, heat-resistant silicone components.

Market Drivers

Rising Demand from Automotive and Transportation Industries

The automotive sector significantly drives the UK Silicone Elastomers Market due to rising adoption in engine gaskets, seals, and connectors. Manufacturers rely on silicone elastomers for their ability to withstand temperatures above 200°C and resist chemical degradation. The material’s flexibility supports lightweight designs and extends component lifespan. Electric vehicle makers use silicone elastomers for battery pack insulation and thermal management systems. Growing EV production across the UK strengthens demand for high-performance materials. OEMs are investing in advanced formulations to enhance durability and safety. It continues to gain traction across both passenger and commercial vehicle segments.

- For instance, in April 2025, Freudenberg Sealing Technologies introduced a new elastomer sealing material for electric vehicle battery cells that prevents electrolyte leakage and maintains shape under temperature fluctuations up to 60 °C, enhancing safety and performance in e-mobility applications.

Growing Use in Healthcare and Medical Applications

Expanding healthcare manufacturing is a major driver of the UK Silicone Elastomers Market. Medical-grade silicones are increasingly applied in prosthetics, catheters, and respiratory devices due to their biocompatibility and sterility. Manufacturers use high-purity grades suitable for long-term implantation and contact applications. Rising healthcare expenditure and aging populations are encouraging hospitals to adopt reliable medical devices. The material’s ability to maintain integrity under sterilization cycles boosts its suitability for clinical use. Silicone tubing and seals ensure efficient drug delivery and fluid management systems. It supports medical innovation by improving patient safety and product reliability.

Expansion in Electrical and Electronics Manufacturing

Silicone elastomers are becoming essential in electrical insulation, cable sheathing, and sensor encapsulation. The UK’s electronics sector increasingly adopts silicone materials for flexible, heat-resistant, and flame-retardant applications. Rapid growth in renewable energy and telecommunications enhances the need for durable insulating materials. Silicone’s superior dielectric strength ensures safety in high-voltage systems. Manufacturers are focusing on thermally conductive variants for heat dissipation in compact electronic assemblies. Industrial automation and smart devices are accelerating product adoption. The UK Silicone Elastomers Market benefits from strong domestic R&D and advanced electronics production infrastructure.

- For instance, Momentive Performance Materials’ SilCool™ family of thermal management silicone compounds provides high thermal conductivity, thin bond lines, and low thermal resistance, ensuring efficient heat dissipation and protection of sensitive components in high-performance electronic applications.

Increased Focus on Sustainable and High-Performance Materials

Sustainability is reshaping the demand landscape of silicone elastomers. Companies are developing eco-efficient production technologies to minimize emissions and waste. The integration of bio-based feedstocks supports low-carbon material innovation. Manufacturers are improving recycling processes for silicone waste recovery. Green construction projects in the UK rely on silicone sealants and coatings to enhance energy efficiency. High-performance elastomers extend component life, reducing replacement frequency and environmental footprint. It aligns with the country’s sustainability commitments and circular economy goals. This shift enhances competitiveness and long-term material resilience.

Market Trends

Adoption of Advanced Liquid Silicone Rubber Technologies

The increasing use of liquid silicone rubber (LSR) highlights a key trend in the UK Silicone Elastomers Market. LSR supports precision molding, high throughput, and reduced waste in automated manufacturing. Medical and electronics industries prefer LSR for its purity and reproducibility. New injection molding systems enable faster curing and consistent quality. Companies are integrating LSR into wearable electronics and microcomponents due to its flexibility. Advanced formulations with enhanced mechanical and thermal stability are under development. It ensures consistent performance across critical applications and supports miniaturization in next-generation products.

- For example, Dow Inc. launched the SILASTIC™ MS-5002 Moldable Silicone in 2022. The grade features very low mold-fouling and supports much higher throughput for optical injection-molded parts.

Growing Integration in Renewable Energy and Infrastructure Projects

Infrastructure modernization and renewable energy development are creating steady demand for silicone elastomers. The material is used in sealing, bonding, and insulation for solar and wind installations. Its resistance to UV radiation, moisture, and extreme temperatures ensures durability in harsh outdoor environments. Renewable infrastructure projects increasingly depend on high-performance silicones for energy-efficient construction. Manufacturers are tailoring formulations for long-term resistance and structural stability. The trend aligns with the UK’s green energy targets and sustainability commitments. It reinforces silicone’s role in enhancing operational reliability and reducing maintenance costs.

Increasing Innovation in High-Temperature and Fluorosilicone Grades

A surge in innovation around high-temperature elastomers is shaping market direction. Fluorosilicone grades are gaining attention for aerospace, defense, and industrial machinery applications. Their chemical resistance to oils, fuels, and solvents enables superior durability. Manufacturers are introducing compounds that function efficiently in extreme conditions up to 250°C. Demand for heat-resistant materials in turbine seals, gaskets, and electrical systems is rising. The trend supports the evolution of high-performance industrial equipment. It encourages continuous product differentiation and R&D investments in the UK Silicone Elastomers Market.

Digital Transformation and Smart Manufacturing Expansion

Digitalization of manufacturing processes is influencing material adoption and production efficiency. Companies are using predictive analytics and automated systems to enhance elastomer compounding and molding accuracy. Smart factories integrate real-time quality monitoring and energy optimization. 3D printing of silicone parts is emerging for customized prototypes and low-volume production. AI-driven process control helps maintain consistent product characteristics. Manufacturers are also adopting digital twins to improve performance testing. It promotes agile manufacturing and supports faster innovation cycles across industries.

- For instance, Arburg’s GESTICA control system, presented at the K 2025 trade fair, features a robust industrial panel with an extended user interface and smart assistance functions for intuitive operation and adaptive process control, supporting digital transformation in injection molding processes.

Market Challenges Analysis

Volatility in Raw Material Prices and Supply Chain Disruptions

The UK Silicone Elastomers Market faces challenges due to fluctuations in raw material availability. Polysiloxane and silicon metal price volatility impacts production stability. Supply constraints from global producers create cost pressure for local manufacturers. Rising logistics costs and trade delays further strain margins. Dependence on imported feedstock exposes the market to geopolitical and economic uncertainties. Companies are seeking domestic sourcing alternatives and process optimization to maintain competitiveness. Balancing quality control with cost efficiency remains difficult under uncertain global supply dynamics. It affects production planning and long-term investment strategies.

Stringent Environmental Regulations and Processing Complexity

Environmental and safety regulations increase compliance obligations for silicone producers. Manufacturers must reduce emissions from curing and compounding processes. Waste disposal and recycling present technical difficulties due to the cross-linked nature of silicone polymers. Meeting REACH and environmental standards demands costly technological upgrades. Complex processing steps raise energy consumption and operational expenses. Small and mid-scale firms face barriers in adopting sustainable manufacturing practices. Regulatory scrutiny around chemical compositions requires frequent formulation adjustments. It limits flexibility and increases R&D costs for producers in this market.

Market Opportunities

Expansion in Electric Vehicles and Energy Storage Applications

Rapid growth of electric mobility offers strong opportunities for the UK Silicone Elastomers Market. EV battery insulation, cable protection, and heat management systems require high-performance silicones. Manufacturers are developing grades optimized for thermal conductivity and flame retardance. Expanding charging infrastructure across the UK supports further adoption. Companies focusing on lightweight and durable materials benefit from this demand surge. It strengthens collaboration between elastomer producers and automotive OEMs. Growing energy storage projects also enhance material relevance in power modules and sealing systems.

Rising Adoption in Consumer Electronics and Smart Devices

The increasing demand for compact, durable electronics drives opportunities for silicone elastomer applications. The material ensures flexibility and environmental resistance in wearables and handheld devices. Growth in home automation, 5G, and IoT expands usage scope. Manufacturers are designing transparent and conductive silicone grades for touch-sensitive and optical components. Partnerships with electronic component suppliers encourage new product innovations. It supports long-term market expansion through integration with digital consumer technologies. Continuous innovation in miniaturization and durability is reinforcing silicone’s role in modern devices.

Market Segmentation Analysis

By Type

Liquid Silicone Rubber (LSR) dominates the UK Silicone Elastomers Market due to its superior purity, flowability, and suitability for automated injection molding. High Consistency Rubber (HCR) follows, preferred for its mechanical strength and use in industrial seals and gaskets. Fluorosilicone Elastomers are widely used in aerospace and automotive sectors for fuel and oil resistance. The “Others” segment includes specialty grades used in niche medical and electronics applications. Each type addresses specific mechanical and thermal requirements across industries, enabling material versatility.

- For instance, Momentive’s Silopren™ LSR 4640 is a medical-grade liquid silicone rubber compliant with USP Class VI and ISO 10993 standards. It supports injection molding for healthcare applications and retains its mechanical properties after ethylene oxide, steam, and gamma sterilization, as confirmed by Momentive’s official product data.

By Application

Electrical & Electronics lead application adoption due to expanding smart device manufacturing and renewable energy systems. Automotive & Transportation ranks next, driven by EV growth and lightweight material demand. Industrial Machinery increasingly relies on silicones for seals, tubing, and connectors under high stress. Consumer Goods use silicone for cookware, personal care, and home appliances due to safety and durability. Construction benefits from weather-resistant sealants and coatings, supporting energy-efficient structures. The “Others” segment covers medical and aerospace uses where high precision and stability are vital.

- For instance, Wacker Chemie AG’s ELASTOSIL® silicone dampening pads are designed for industrial and machinery applications, delivering verified vibration and noise reduction performance. These products are supported by quality certifications and European supply standards, demonstrating their reliability in demanding mechanical environments.

Segmentation

By Type

- Liquid Silicone Rubber (LSR)

- High Consistency Rubber (HCR)

- Fluorosilicone Elastomers

- Others

By Application

- Electrical & Electronics

- Automotive & Transportation

- Industrial MachineryConsumer Goods

- Construction

- Others

Regional Analysis

England Leading the Market with Strong Industrial and Manufacturing Base

England dominates the UK Silicone Elastomers Market with a market share of 58%. Its leadership stems from a well-established automotive, electronics, and healthcare manufacturing ecosystem. The region hosts several global silicone producers and research centers that focus on innovation in liquid silicone rubber and high-consistency rubber grades. Demand is driven by medical device manufacturing clusters and advanced automotive component production. Major players have expanded their facilities across the Midlands and southern England to meet growing application needs. Strong export capabilities and a skilled workforce sustain England’s position. It remains the key contributor to national output due to industrial diversity and robust infrastructure.

Scotland Emerging as a High-Growth Region with Renewable Energy Expansion

Scotland accounts for 23% of the UK market share, supported by its growing renewable energy and infrastructure projects. The material’s use in sealing, insulation, and electrical applications aligns with the region’s clean energy goals. Local industries are integrating silicone elastomers into offshore wind installations and power transmission systems. Investments in construction and equipment manufacturing are enhancing local demand. R&D initiatives in polymer engineering also contribute to regional innovation. Scotland’s industrial clusters near Aberdeen and Glasgow promote technological advancements in silicone-based solutions. It shows significant potential for growth in sustainable applications and high-performance materials.

Wales and Northern Ireland Supporting Niche Industrial Applications

Wales and Northern Ireland collectively represent 19% of the UK market share, focusing on niche industrial, construction, and transportation applications. Wales benefits from ongoing manufacturing investments in automotive components and industrial machinery. Northern Ireland’s chemical and aerospace sectors are increasing the use of high-temperature silicone materials. Both regions support small to medium enterprises involved in customized elastomer processing. Growing construction activities and renewable installations further drive silicone demand. Government support for advanced material production encourages local competitiveness. It strengthens regional contributions to the national silicone elastomer supply chain.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Dow Inc.

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- China National Bluestar (Group) Co., Ltd.

- Stockwell Elastomerics

- Specialty Silicone Products, Inc.

Competitive Analysis

The UK Silicone Elastomers Market features strong competition among global and domestic players focusing on innovation, product quality, and industry specialization. Key companies such as Wacker Chemie AG, Momentive Performance Materials, Dow Silicones UK Ltd., Elkem ASA, and Shin-Etsu Chemical Co. Ltd. lead through extensive product portfolios and R&D investments. Local manufacturers cater to customized demands in automotive, medical, and electronics applications. Companies are adopting sustainable production technologies to align with environmental regulations. Strategic mergers, facility upgrades, and partnerships enhance their competitiveness and market presence. It remains a dynamic market where material innovation and application diversification define long-term leadership.

Recent Developments

- In September 2025, Safic-Alcan announced the expansion of its partnership with Momentive to distribute silicone elastomers more broadly across Europe, particularly strengthening its portfolio in France and Eastern Europe. This partnership is designed to accelerate innovation in the market and provide customers with wider access to Momentive’s advanced silicone elastomer solutions, reflecting a strong commitment to performance, safety, and sustainability in regional supply chains.

- In June 2025, WACKER introduced a new silicone elastomer product specifically aimed at the power grid and e-mobility sectors, which it showcased at the K 2025 trade fair held in Germany from October 8 to 15. This product is engineered to provide highly reliable insulation for components in these critical applications, reinforcing WACKER’s innovation leadership in the European silicone elastomers market and catering to the rising demand for advanced materials in both energy infrastructure and electric mobility.

Report Coverage

The research report offers an in-depth analysis based on Type and Application. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The UK Silicone Elastomers Market will witness growing adoption in electric vehicle manufacturing due to superior thermal insulation and sealing properties.

- Increased demand for medical-grade silicone products will drive advancements in biocompatible elastomer formulations.

- Expanding renewable energy infrastructure will strengthen silicone applications in wind, solar, and grid components.

- Technological innovation in liquid silicone rubber processing will improve efficiency and reduce production time.

- Rising investment in sustainable and recyclable silicone materials will enhance environmental compliance.

- Integration of silicone elastomers in consumer electronics will support miniaturization and durability of next-generation devices.

- Growth in industrial automation will create opportunities for high-performance silicone parts and connectors.

- Regional R&D collaborations will encourage the development of specialty elastomers with higher temperature stability.

- Increasing focus on domestic manufacturing will reduce supply chain dependence and enhance market resilience.

- The UK Silicone Elastomers Market will remain competitive, driven by product innovation, capacity expansion, and strategic partnerships across industries.