Market Overview

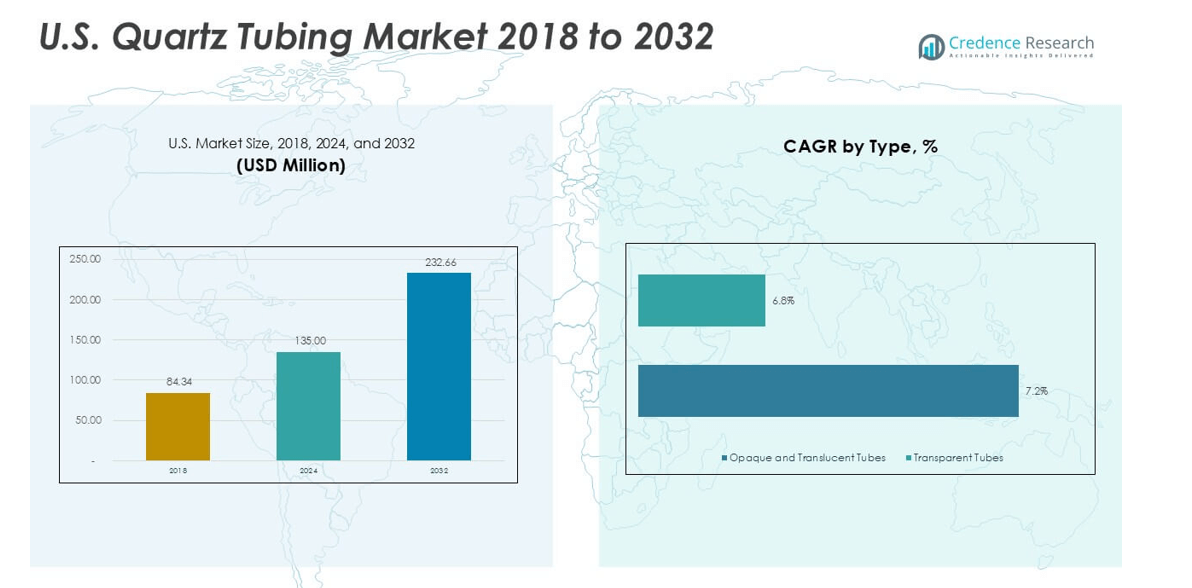

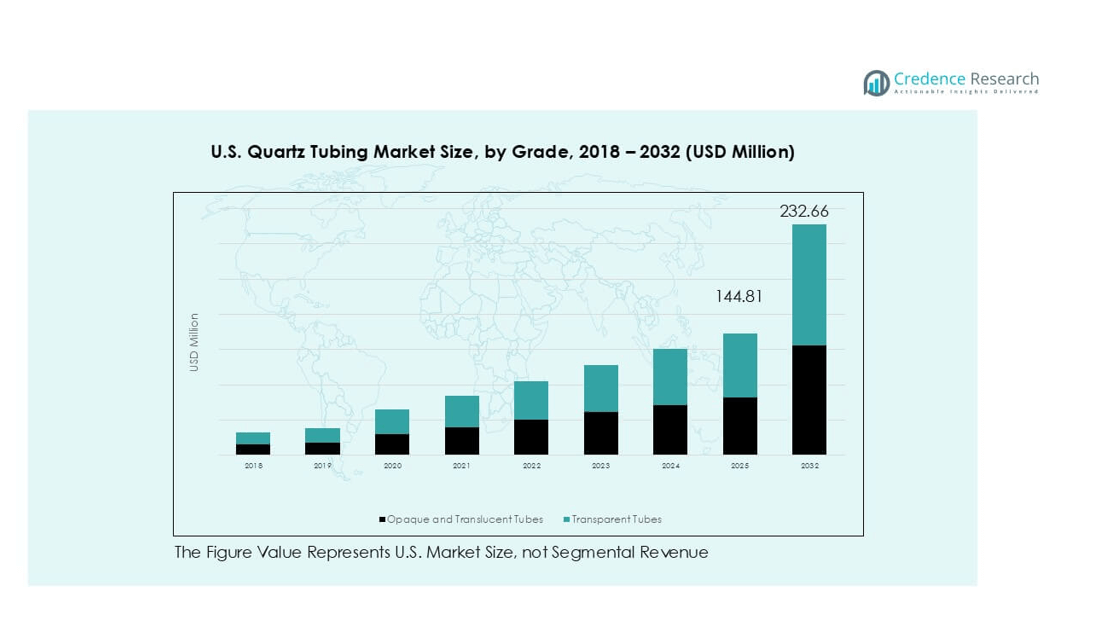

The U.S. Quartz Tubing market size was valued at USD 84.34 million in 2018 to USD 135.00 million in 2024 2024 and is anticipated to reach USD 232.66 million by 2032, at a CAGR of 7.04% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| U.S. Quartz Tubing Market Size 2024 |

USD 135.00 million |

| U.S. Quartz Tubing Market, CAGR |

7.04% |

| U.S. Quartz Tubing Market Size 2032 |

USD 232.66 million |

The U.S. quartz tubing market is led by established global and domestic manufacturers with strong technical capabilities. Key players include Momentive, Heraeus, TOSOH, QSIL, Technical Glass Products, and GM Quartz. These companies compete through high-purity product portfolios, custom fabrication, and reliable supply for semiconductor and industrial customers. Momentive and Heraeus hold strong positions in ultra-high-purity tubing for wafer processing. Regionally, the Western United States leads the market with a 38% share. This dominance reflects concentrated semiconductor fabrication in California, Arizona, and Oregon. The Midwest and Southern regions follow, supported by industrial processing and expanding chip manufacturing ecosystems.

Market Insights

- The U.S. quartz tubing market grew from USD 84.34 million in 2018 to USD 135.00 million in 2024. The market is projected to reach USD 232.66 million by 2032, growing at a CAGR of 7.04% during the forecast period.

- Market growth is driven by strong demand from semiconductor manufacturing. High-purity quartz tubing supports diffusion, oxidation, and thermal processing. Transparent tubes dominate by type with over 60% share due to purity needs.

- Key market trends include rising demand for custom and high-purity tubing. Semiconductor applications hold the largest segment share at nearly 45%. UV and specialty industrial uses also create new opportunities.

- The competitive landscape is moderately consolidated. Major players such as Momentive, Heraeus, and TOSOH focus on purity control, customization, and long-term OEM contracts. Domestic sourcing strengthens competitive positioning.

- Regionally, the Western U.S. leads with about 38% market share, followed by the Midwest at 24%, the South at 22%, and the Northeast at 16%, driven by fabs, industrial bases, and R&D centers.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

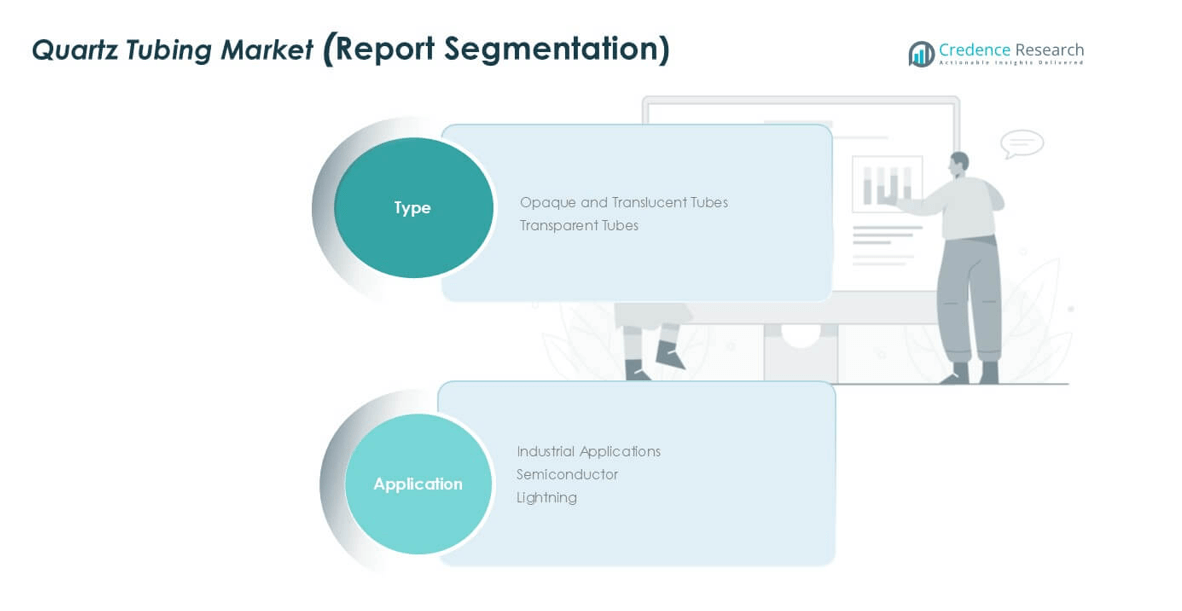

Market Segmentation Analysis:

By Type

The U.S. Quartz Tubing market shows clear dominance by transparent tubes. This sub-segment accounts for over 60% market share. Strong demand comes from semiconductor and high-purity industrial uses. Transparent tubes offer low impurity levels and high thermal stability. These features support critical thermal and chemical processes. Opaque and translucent tubes hold a smaller share. Demand remains steady in insulation-focused applications. However, limited optical clarity restricts broader use. Ongoing chip manufacturing investments continue to favor transparent quartz tubing.

- For instance, Momentive supplies transparent fused-quartz tubes with metal impurities below 1 ppm and thermal expansion near 0.55×10⁻⁶/K, enabling stable operation in oxidation and diffusion tools used in U.S. 300-mm fabs.

By Application

Semiconductor applications represent the dominant segment in the U.S. market. This segment contributes nearly 45% of total demand. Growth is driven by wafer fabrication and diffusion processes. Quartz tubing supports high-temperature and contamination-free operations. Industrial applications follow with moderate share. These include chemical processing and laboratory equipment. Lighting applications hold a smaller portion. LED transition reduces traditional lighting demand. Advanced chip production and fab expansions sustain semiconductor leadership.

- For instance, Heraeus produces semiconductor-grade quartz tubes certified for continuous use above 1,050 °C with hydroxyl content under 10 ppm, supporting clean diffusion and LPCVD steps in U.S.-based wafer fabrication lines.

Key Growth Drivers

Expansion of Semiconductor Manufacturing Capacity

Rising semiconductor fabrication activity is a primary growth driver for the U.S. quartz tubing market. Advanced chip production requires ultra-high-purity quartz tubing for diffusion, oxidation, and LPCVD processes. Quartz tubing withstands temperatures above 1,200 °C while maintaining chemical stability. Ongoing investments in domestic fabs increase steady demand. Federal incentives supporting local semiconductor supply chains further strengthen this trend. Quartz tubing remains essential in wafer processing due to low contamination risk. As node sizes shrink, tolerance limits tighten, increasing reliance on premium quartz products. Equipment replacement cycles also add recurring demand. This driver remains long term due to strategic chip manufacturing priorities.

- For instance, Momentive supplies semiconductor-grade quartz tubes with certified Fe, Al, and Na impurities below 1 ppm and continuous-use ratings up to 1,200 °C, supporting oxidation and LPCVD tools in U.S. 300-mm wafer fabs.

Growth in High-Temperature Industrial Processing

Industrial processing applications continue to drive quartz tubing demand across the U.S. market. Industries such as chemicals, pharmaceuticals, and advanced materials rely on quartz for thermal resistance. Quartz tubing supports processes involving corrosive gases and rapid thermal cycling. Compared with metal alternatives, quartz offers superior purity and longer service life. Adoption rises in pilot plants and precision manufacturing lines. Demand also grows from laboratory-scale reactors and analytical equipment. As manufacturers seek higher efficiency and reduced downtime, quartz tubing adoption expands. Process optimization and safety compliance further reinforce this driver across industrial sectors.

- For instance, Heraeus manufactures industrial fused-silica tubes with thermal expansion near 0.55 × 10⁻⁶/K and verified resistance to repeated heat-quench cycles from above 1,000 °C, enabling stable use in chemical reactors and high-temperature process lines.

Rising Use in Advanced Lighting and UV Systems

Quartz tubing plays a critical role in specialized lighting and ultraviolet systems. These include UV disinfection, curing, and medical lighting equipment. Quartz enables high UV transmission and thermal durability. Growing adoption of UV-based sterilization systems supports market growth. Healthcare facilities and water treatment plants increase UV installations. Industrial curing applications also expand in electronics and coatings. While general lighting demand slows, niche UV and specialty lighting offset declines. Regulatory focus on hygiene and surface sterilization further supports adoption. This driver benefits from increasing awareness of non-chemical disinfection solutions.

Key Trends & Opportunities

Increasing Demand for High-Purity and Custom Quartz Tubes

A key trend is the shift toward high-purity and application-specific quartz tubing. Semiconductor and research users demand tighter impurity limits. Custom diameters, wall thicknesses, and surface finishes gain importance. Manufacturers invest in precision forming and advanced purification methods. This trend creates opportunities for value-added products. Customized tubing improves process yields and equipment compatibility. Suppliers offering engineering support gain competitive advantage. As applications diversify, tailored quartz solutions unlock new revenue streams. This trend favors suppliers with advanced manufacturing capabilities.

- For instance, Momentive produces custom semiconductor quartz tubes with metal impurities below 1 ppm and diameter tolerances held within ±0.1 mm, supporting oxidation and LPCVD tools used in U.S. wafer fabs.

Opportunities from Domestic Supply Chain Localization

Supply chain localization presents a strong opportunity for U.S. quartz tubing suppliers. End users seek reliable domestic sources to reduce import dependence. Shorter lead times improve operational resilience. Local production also supports compliance with government procurement requirements. This shift encourages capacity expansion and technology upgrades. Partnerships with equipment OEMs strengthen long-term contracts. Domestic sourcing aligns with broader industrial policy goals. Suppliers that scale efficiently can capture stable demand. Localization also improves quality control and customer collaboration.

- For instance, Heraeus operates U.S.-based quartz manufacturing lines that supply fused-silica tubing rated for continuous use above 1,100 °C, enabling faster delivery and tighter process control for domestic semiconductor and industrial customers.

Key Challenges

High Production Costs and Energy Intensity

High production costs remain a key challenge in the U.S. quartz tubing market. Quartz melting and forming require energy-intensive furnaces. Electricity and fuel price volatility affects margins. Maintaining ultra-high purity adds further cost pressure. Specialized equipment and skilled labor increase capital intensity. Smaller manufacturers face barriers to scale. Cost competitiveness against imported products remains difficult. Passing costs to customers proves challenging in price-sensitive segments. This challenge limits rapid capacity expansion and pressures profitability.

Technical Complexity and Quality Consistency Risks

Maintaining consistent quality presents another major challenge. Quartz tubing applications demand strict dimensional and purity tolerances. Minor defects can cause equipment failure or yield loss. Process control requires advanced monitoring and expertise. Scrap rates increase when specifications tighten. Scaling production without compromising quality is difficult. Customer audits and qualification cycles extend sales timelines. Any quality deviation risks long-term supplier relationships. This challenge increases operational risk and demands continuous investment in process control systems.

Regional Analysis

Western United States

The Western United States holds the largest share of the U.S. quartz tubing market. The region accounts for about 38% of total demand. Strong semiconductor manufacturing drives regional dominance. California, Arizona, and Oregon host advanced wafer fabrication plants. These facilities require high-purity quartz tubing for diffusion and oxidation processes. Continuous fab upgrades sustain replacement demand. Research institutions and specialty lighting manufacturers add further volume. Proximity to technology hubs supports faster supplier collaboration. High capital investment levels reinforce stable long-term consumption across semiconductor-focused applications.

Midwestern United States

The Midwest represents nearly 24% of the U.S. quartz tubing market. Demand comes mainly from industrial processing and laboratory equipment. Chemical manufacturing and materials research drive steady usage. States such as Ohio, Michigan, and Illinois support advanced manufacturing clusters. Quartz tubing serves high-temperature reactors and analytical systems. Automotive R&D labs also contribute incremental demand. The region benefits from strong industrial infrastructure. Moderate semiconductor activity provides additional support. Stable industrial output ensures consistent consumption levels across multiple end-use segments.

Southern United States

The Southern region accounts for approximately 22% market share. Growth is supported by expanding semiconductor fabs in Texas and Arizona’s neighboring supply chains. Chemical processing and pharmaceutical manufacturing also contribute. Quartz tubing supports corrosion-resistant and high-temperature operations. The region benefits from lower operating costs and business-friendly policies. Industrial investments continue to rise across the Gulf Coast. Demand from UV disinfection systems grows in municipal facilities. These factors strengthen the South’s role as a fast-growing consumption center.

Northeastern United States

The Northeast holds close to 16% of the U.S. quartz tubing market. Demand is driven by research laboratories and specialty industrial users. Universities and federal research centers require precision quartz components. Semiconductor activity remains limited but stable. Medical device and UV system manufacturers support niche demand. Higher operating costs constrain large-scale production. However, strong R&D spending sustains consistent consumption. The region focuses on high-value, low-volume applications. This structure supports stable but slower market expansion.

Market Segmentations:

By Type

- Opaque and Translucent Tubes

- Transparent Tubes

By Application

- Industrial Applications

- Semiconductor

- Lighting

By Geography

- Western United States

- Midwestern United States

- Southern United States

- Northeastern United States

Competitive Landscape

The U.S. quartz tubing market features a moderately consolidated competitive landscape. Global suppliers and specialized domestic manufacturers compete on purity, dimensional accuracy, and supply reliability. Leading players such as Momentive, Heraeus, and TOSOH leverage advanced melting and purification technologies. These companies serve semiconductor and high-end industrial customers. Mid-sized firms focus on custom tubing and faster lead times. Competition centers on long-term supply contracts with equipment OEMs. Continuous investment in process automation strengthens quality consistency. Domestic production capacity gains importance due to supply chain localization. Strategic partnerships and product customization remain key differentiation factors.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Momentive

- Heraeus

- QSIL

- TOSOH

- Fudong Lighting

- Aoxin Quartz

- Sentro Tech

- Anderman Ceramics

- GM Quartz

- Technical Glass Products Inc.

Recent Developments

- In Jan 2025, Heraeus combined high-performance materials units into Heraeus Covantics to expand its technology leadership in high-purity quartz and fused silica products.

- In Nov 2024, Momentive Technologies promoted two long-serving executives into global quartz and ceramics leadership roles, strengthening its quartz business focus

Report Coverage

The research report offers an in-depth analysis based on Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Semiconductor fabrication expansion will continue to drive sustained quartz tubing demand.

- High-purity and defect-free tubing requirements will tighten across advanced process nodes.

- Transparent quartz tubes will maintain dominance due to semiconductor and UV applications.

- Domestic manufacturing capacity will expand to support supply chain resilience.

- Custom tube dimensions and engineered solutions will gain stronger customer preference.

- Energy-efficient melting and forming technologies will see higher adoption.

- Industrial processing demand will remain stable across chemicals and laboratories.

- UV disinfection and specialty lighting applications will support niche growth.

- Quality consistency and traceability will become critical supplier selection criteria.

- Strategic partnerships with equipment manufacturers will shape long-term market positioning.