CHAPTER NO. 1 : INTRODUCTION 21

1.1. Report Description 21

Purpose of the Report 21

USP & Key Offerings 21

1.2. Key Benefits for Stakeholders 22

1.3. Target Audience 22

CHAPTER NO. 2 : EXECUTIVE SUMMARY 23

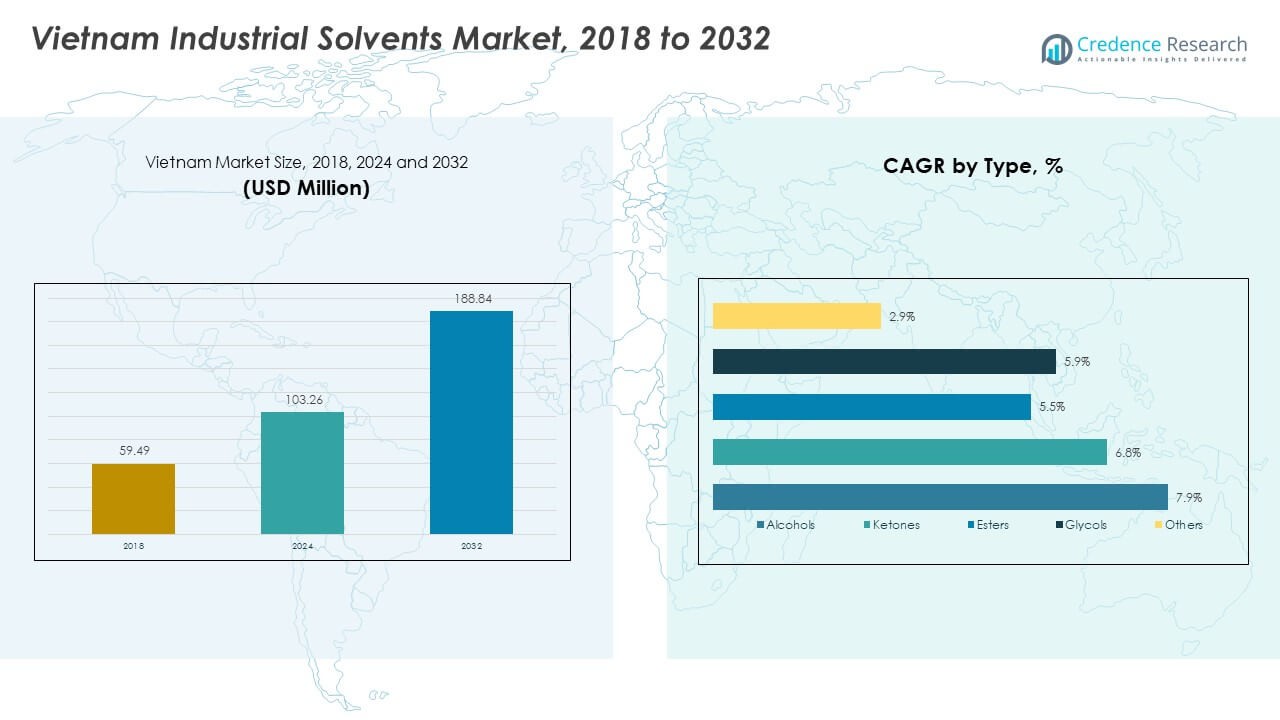

CHAPTER NO. 3 : VIETNAM INDUSTRIAL SOLVENTS MARKET FORCES & INDUSTRY PULSE 25

3.1. Foundations of Change – Market Overview 25

3.2. Catalysts of Expansion – Key Market Drivers 27

3.2.1. Momentum Boosters – Growth Triggers 28

3.2.2. Innovation Fuel – Disruptive Technologies 28

3.3. Headwinds & Crosswinds – Market Restraints 29

3.3.1. Regulatory Tides – Compliance Challenges 30

3.3.2. Economic Frictions – Inflationary Pressures 30

3.4. Untapped Horizons – Growth Potential & Opportunities and Strategic Navigation – Industry Frameworks 31

3.5. Market Equilibrium – Porter’s Five Forces 32

3.6. Ecosystem Dynamics – Value Chain Analysis 34

3.7. Macro Forces – PESTEL Breakdown 36

3.8. Price Trend Analysis 37

3.9. Price Trend by Product Type 38

3.10. Buying Criteria 39

CHAPTER NO. 4 : COMPETITION ANALYSIS 40

4.1. Company Market Share Analysis 40

4.1.1. Vietnam Industrial Solvents Market Company Volume Market Share 40

4.1.2. Vietnam Industrial Solvents Market Company Revenue Market Share 42

4.2. Strategic Developments 44

4.2.1. Acquisitions & Mergers 44

4.2.2. New Product Launch 45

4.2.3. Agreements & Collaborations 46

4.3. Competitive Dashboard 47

4.4. Company Assessment Metrics, 2024 48

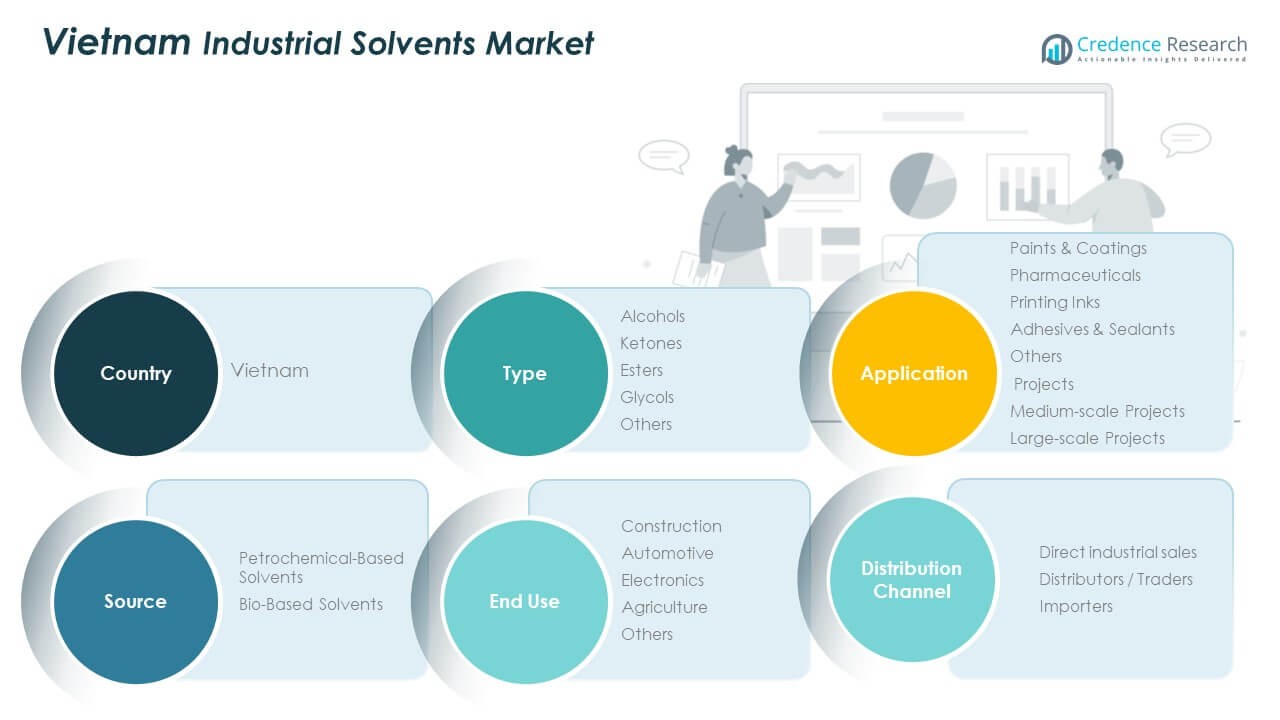

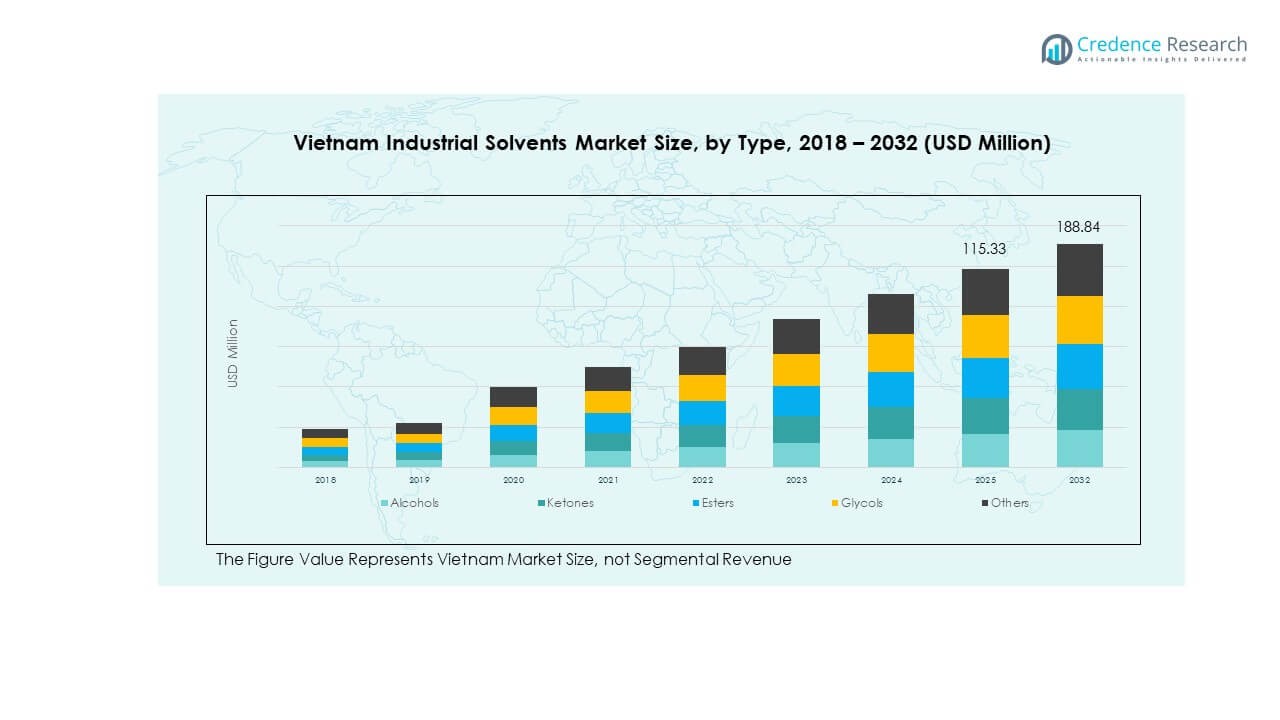

CHAPTER NO. 5 : VIETNAM MARKET ANALYSIS, INSIGHTS & FORECAST, BY TYPE 49

CHAPTER NO. 6 : VIETNAM MARKET ANALYSIS, INSIGHTS & FORECAST, BY APPLICATION 54

CHAPTER NO. 7 : VIETNAM MARKET ANALYSIS, INSIGHTS & FORECAST, BY SOURCE 61

CHAPTER NO. 8 : VIETNAM MARKET ANALYSIS, INSIGHTS & FORECAST, BY END USE 66

CHAPTER NO. 10 : VIETNAM MARKET ANALYSIS, INSIGHTS & FORECAST, BY DISTRIBUTION CHANNEL 71

CHAPTER NO. 11 : COMPANY PROFILE 76

11.1. Kanematsu Vietnam 76

11.2. Top Solvent (Vietnam) Limited 79

11.3. Hai Nguyen Chemicals Company Limited 79

11.4. PLC Chemicals 79

11.5. Northern Industrial Chemicals Joint Stock Company 79

11.6. Hoang Ha Chemical Co., Ltd. 79

11.7. BASF Vietnam Limited 79

11.8. Company 8 79

11.9. Company 9 79

11.10. Company 10 79

List of Figures

FIG NO. 1. Vietnam Industrial Solvents Market Revenue Share, By Type, 2024 & 2032 49

FIG NO. 2. Market Attractiveness Analysis, By Type 50

FIG NO. 3. Incremental Revenue Growth Opportunity by Type, 2024 – 2032 51

FIG NO. 4. Vietnam Industrial Solvents Market Revenue Share, By Application, 2024 & 2032 54

FIG NO. 5. Incremental Revenue Growth Opportunity by Application, 2024 – 2032 55

FIG NO. 6. Incremental Revenue Growth Opportunity by Application, 2024 – 2032 56

FIG NO. 7. Vietnam Industrial Solvents Market Revenue Share, By Source, 2024 & 2032 61

FIG NO. 8. Market Attractiveness Analysis, By Source 62

FIG NO. 9. Incremental Revenue Growth Opportunity by Source, 2024 – 2032 63

FIG NO. 10. Vietnam Industrial Solvents Market Revenue Share, By End Use, 2024 & 2032 66

FIG NO. 11. Market Attractiveness Analysis, By End Use 67

FIG NO. 12. Incremental Revenue Growth Opportunity by End Use, 2024 – 2032 68

FIG NO. 13. Vietnam Industrial Solvents Market Revenue Share, By Distribution Channel, 2024 & 2032 71

FIG NO. 14. Market Attractiveness Analysis, By Distribution Channel 72

FIG NO. 15. Incremental Revenue Growth Opportunity by Distribution Channel, 2024 – 2032 73

List of Tables

TABLE NO. 1. : Vietnam Industrial Solvents Market Revenue, By Type, 2018 – 2024 (USD Million) 52

TABLE NO. 2. : Vietnam Industrial Solvents Market Revenue, By Type, 2025 – 2032 (USD Million) 52

TABLE NO. 3. : Vietnam Industrial Solvents Market Volume, By Type, 2018 – 2024 (Units) 53

TABLE NO. 4. : Vietnam Industrial Solvents Market Volume, By Type, 2025 – 2032 (Units) 53

TABLE NO. 5. : Vietnam Industrial Solvents Market Revenue, By Application, 2018 – 2024 (USD Million) 57

TABLE NO. 6. : Vietnam Industrial Solvents Market Revenue, By Application, 2025 – 2032 (USD Million) 58

TABLE NO. 7. : Vietnam Industrial Solvents Market Volume, By Application, 2018 – 2024 (Units) 59

TABLE NO. 8. : Vietnam Industrial Solvents Market Volume, By Application, 2025 – 2032 (Units) 60

TABLE NO. 9. : Vietnam Industrial Solvents Market Revenue, By Source, 2018 – 2024 (USD Million) 64

TABLE NO. 10. : Vietnam Industrial Solvents Market Revenue, By Source, 2025 – 2032 (USD Million) 64

TABLE NO. 11. : Vietnam Industrial Solvents Market Volume, By Source, 2018 – 2024 (Units) 65

TABLE NO. 12. : Vietnam Industrial Solvents Market Volume, By Source, 2025 – 2032 (Units) 65

TABLE NO. 13. : Vietnam Industrial Solvents Market Revenue, By End Use, 2018 – 2024 (USD Million) 69

TABLE NO. 14. : Vietnam Industrial Solvents Market Revenue, By End Use, 2025 – 2032 (USD Million) 69

TABLE NO. 15. : Vietnam Industrial Solvents Market Volume, By End Use, 2018 – 2024 (Units) 70

TABLE NO. 16. : Vietnam Industrial Solvents Market Volume, By End Use, 2025 – 2032 (Units) 70

TABLE NO. 17. : Vietnam Industrial Solvents Market Revenue, By Distribution Channel, 2018 – 2024 (USD Million) 74

TABLE NO. 18. : Vietnam Industrial Solvents Market Revenue, By Distribution Channel, 2025 – 2032 (USD Million) 74

TABLE NO. 19. : Vietnam Industrial Solvents Market Volume, By Distribution Channel, 2018 – 2024 (Units) 75

TABLE NO. 20. : Vietnam Industrial Solvents Market Volume, By Distribution Channel, 2025 – 2032 (Units) 75