Market Overview:

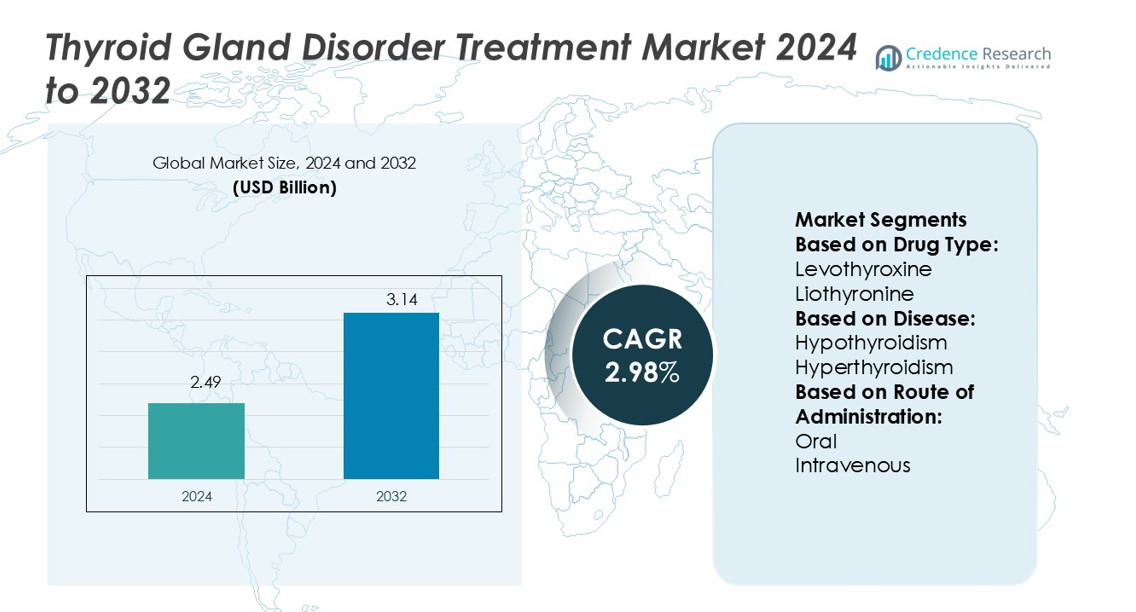

Thyroid Gland Disorder Treatment Market size was valued USD 2.49 billion in 2024 and is anticipated to reach USD 3.14 billion by 2032, at a CAGR of 2.98% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Thyroid Gland Disorder Treatment Market Size 2024 |

USD 2.49 billion |

| Thyroid Gland Disorder Treatment Market, CAGR |

2.98% |

| Thyroid Gland Disorder Treatment Market Size 2032 |

USD 3.14 billion |

The Thyroid Gland Disorder Treatment Market is shaped by key players such as Novartis AG, Glenmark Pharmaceuticals Ltd., Sun Pharmaceutical Industries Limited, Pfizer Inc., Abbott Laboratories, Merck & Co., Inc., Mylan N.V., AbbVie Inc., Aspen Pharmacare Holdings Limited, and Lannett Company, Inc. These companies focus on expanding their product portfolios through innovative formulations, generics production, and strategic collaborations to strengthen global reach. North America leads the market with a 34% share, supported by advanced healthcare infrastructure, strong adoption of hormone replacement therapies, and high diagnostic awareness. The region’s leadership is reinforced by favorable reimbursement policies and robust R&D investments from multinational pharmaceutical companies.

Market Insights

- The Thyroid Gland Disorder Treatment Market was valued at USD 2.49 billion in 2024 and is projected to reach USD 3.14 billion by 2032, growing at a CAGR of 2.98%.

- Market growth is driven by rising prevalence of hypothyroidism, strong adoption of hormone replacement therapies, and expanding diagnostic capabilities supporting early detection.

- Trends include the development of novel formulations such as liquid and soft gel levothyroxine, along with a growing shift toward personalized medicine and improved drug delivery systems.

- Competitive dynamics are shaped by leading players including Novartis, Pfizer, Merck, Abbott, and Glenmark, while generics manufacturers strengthen affordability and expand access globally.

- North America dominates with 34% share, followed by Europe at 29% and Asia-Pacific at 23%; by disease, hypothyroidism holds the largest share due to high patient dependence on lifelong hormone therapy, reinforcing demand for levothyroxine as the leading drug type.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Drug Type

Levothyroxine dominates the thyroid gland disorder treatment market, holding the largest share due to its status as the standard therapy for hypothyroidism. The drug’s consistent effectiveness in restoring normal thyroid hormone levels and its wide availability support its dominance. Liothyronine serves as an alternative for patients requiring faster action, while propylthiouracil and imidazole-based compounds are primarily used in hyperthyroidism cases. Beta-blockers remain essential in managing related symptoms such as palpitations and tremors. However, levothyroxine’s proven safety, affordability, and established clinical guidelines maintain its leadership within this segment.

- For instance, Full dose escalation results from the Phase 1 TRIgnite-1 study demonstrated that ISB 2001 achieved target. The dose-escalation study tested dose levels up to 2700 µg/kg.

By Disease

Hypothyroidism represents the dominant disease segment, accounting for the largest market share. This dominance stems from the high global prevalence of underactive thyroid conditions, especially in aging populations and iodine-deficient regions. Patients with hypothyroidism rely on long-term hormone replacement therapy, which sustains strong and recurring demand. Hyperthyroidism, while significant, remains smaller in share due to lower patient incidence and a broader range of treatment options including surgery and radioactive iodine therapy. Rising diagnostic awareness and routine thyroid function testing further reinforce the growth of hypothyroidism-focused treatments.

- For instance, Sun Pharma typically invests between 6-8% of its global revenues annually in R&D, maintaining a team of more than 3,000 scientists who work on hormones, novel formulations, and drug delivery systems.

By Route of Administration

Oral administration leads this segment with the highest share, supported by ease of use, patient compliance, and availability of standardized tablets and capsules. Levothyroxine and other thyroid drugs are primarily prescribed in oral form, making it the most accessible route for chronic management. Intravenous administration, though limited, plays a critical role in severe thyroid emergencies such as myxedema coma or thyroid storm, where rapid hormone delivery is vital. Other routes remain marginal. The convenience, affordability, and long-term suitability of oral formulations drive their dominance in thyroid treatment practices worldwide.

Market Overview

Rising Prevalence of Thyroid Disorders

The increasing incidence of hypothyroidism and hyperthyroidism globally drives demand for thyroid gland treatments. Sedentary lifestyles, iodine deficiency, and autoimmune conditions such as Hashimoto’s thyroiditis contribute to rising case numbers. With hypothyroidism affecting a significant share of middle-aged and elderly populations, long-term reliance on hormone replacement therapy remains strong. Expanding diagnostic capabilities and screening programs across developed and developing markets further increase the identified patient pool. This growing prevalence directly supports sustained demand for both synthetic hormone therapies and adjunct treatment solutions.

- For instance, the Abbott Alinity i TRAb CMIA (thyroid-stimulating hormone receptor antibody assay) shows repeatability CVs of 4.07%, 1.56%, and 0.71% at TRAb concentrations of 3.0, 10.0, and 30.0 IU/L respectively; within-laboratory imprecision CVs are 4.07%, 1.90%, and 0.71% at the same levels.

Advancements in Diagnostic Technologies

Improved diagnostic techniques significantly enhance early detection and treatment of thyroid disorders. Advanced imaging tools, high-sensitivity TSH assays, and molecular diagnostics allow for precise evaluation of thyroid function. These technologies enable timely treatment decisions, minimizing complications from delayed diagnosis. In addition, growing use of genetic and biomarker testing supports targeted therapy approaches in thyroid cancers. Hospitals and clinics increasingly adopt these innovations, boosting patient confidence and expanding treatment uptake. As accessibility to advanced diagnostics rises, the overall treatment market gains momentum.

- For instance, Merck Indonesia Thyroid RAISE program trained over 5,000 healthcare professionals in thyroid screening; conducted more than 27,000 TSH tests with a conversion yield of ~5,200 detected thyroid disorder cases.

Government and Healthcare Initiatives

Public health programs promoting iodine supplementation and thyroid screening campaigns strongly support market expansion. Governments and healthcare organizations are actively investing in awareness drives, particularly in regions with high iodine deficiency. National health insurance schemes in several countries now cover thyroid medications, improving affordability for patients. In addition, training programs for primary care providers strengthen early diagnosis and treatment adherence. Combined with increasing global investments in healthcare infrastructure, these initiatives widen access to thyroid gland treatments and stimulate long-term market growth.

Key Trends & Opportunities

Shift Toward Personalized Medicine

The adoption of personalized treatment strategies creates new opportunities in thyroid care. Tailored dosing of levothyroxine, genetic-based therapy adjustments, and precision medicine approaches enhance treatment outcomes. Pharmaceutical companies are focusing on developing formulations with improved bioavailability and patient-specific adaptability. This trend reduces variability in treatment response and improves quality of life for patients. Growing integration of digital health platforms and wearable monitoring tools also supports patient-centered management, paving the way for customized therapies as a major growth avenue.

- For instance, Mylan levothyroxine sodium the study aimed to demonstrate the bioequivalence of Mylan 300 µg levothyroxine sodium tablets to a reference product.The study involved 36 healthy adult volunteers.

Development of Novel Drug Formulations

Emerging drug formulations provide opportunities for market differentiation and patient convenience. Liquid levothyroxine, soft gel capsules, and combination therapies address absorption challenges seen in traditional tablets. These alternatives improve compliance among patients with gastrointestinal disorders or poor drug uptake. In addition, research into sustained-release formulations aims to reduce dosing frequency, enhancing long-term adherence. Pharmaceutical firms investing in innovation around improved delivery systems stand to capture larger shares of the expanding patient base, positioning novel therapies as key market growth opportunities.

- For instance, Lannett received FDA first‐cycle approval for its ANDA for Mycophenolate Mofetil for Oral Suspension the drug has a concentration of 200 mg/mL and is in the form of a powder for oral suspension

Key Challenges

Adverse Effects and Treatment Limitations

Despite their effectiveness, thyroid medications face challenges from side effects and limited efficacy in certain patients. Levothyroxine therapy, while widely used, may cause cardiovascular complications, bone density loss, or over-treatment issues if mismanaged. Similarly, anti-thyroid drugs like propylthiouracil carry risks of liver toxicity. These safety concerns often result in patient non-compliance and demand for alternative therapies. Manufacturers must address these limitations through improved formulations and monitoring protocols to reduce adverse outcomes and maintain patient trust in treatment regimens.

High Dependence on Long-Term Therapy

Thyroid disorders, especially hypothyroidism, typically require lifelong treatment, which poses challenges for patient adherence. Daily dosing of levothyroxine demands consistent compliance, and interruptions often lead to serious health complications. This dependence increases treatment costs and burdens healthcare systems in regions with large patient populations. Non-compliance, whether due to forgetfulness, side effects, or financial barriers, remains a critical issue. Addressing this challenge requires innovation in sustained-release therapies, patient education, and healthcare support systems to ensure continuity and long-term treatment success.

Regional Analysis

North America

North America leads the thyroid gland treatment market with a 34% share, driven by high disease prevalence, advanced healthcare infrastructure, and widespread adoption of hormone replacement therapies. The U.S. dominates within the region due to strong pharmaceutical availability, advanced diagnostic technologies, and significant patient awareness. Favorable reimbursement policies and government-backed screening programs further support market penetration. Canada also contributes significantly, aided by public health initiatives targeting iodine deficiency and early thyroid disorder detection. Continuous R&D investments by leading pharmaceutical companies reinforce North America’s position as the largest revenue-generating regional market.

Europe

Europe holds a 29% market share, supported by established healthcare systems, increasing screening rates, and government-led awareness programs. Countries such as Germany, the U.K., and France account for the largest shares, with rising thyroid cancer cases and high diagnosis rates fueling treatment demand. Expanding use of advanced diagnostic technologies and improved access to levothyroxine drive adoption across the region. Strong presence of multinational pharmaceutical companies and collaborations with healthcare providers enhance drug availability. In addition, aging populations and rising prevalence of hypothyroidism further strengthen Europe’s position in the thyroid gland treatment market.

Asia-Pacific

Asia-Pacific accounts for 23% of the thyroid gland treatment market and is the fastest-growing region. Rising prevalence of iodine deficiency disorders, rapid urbanization, and expanding healthcare access are major drivers. China and India lead due to their large populations, growing awareness of thyroid health, and expanding diagnostic infrastructure. Increasing government efforts to address iodine deficiency, coupled with growing availability of affordable generic drugs, improve treatment access. The region also benefits from expanding private healthcare facilities and rising medical tourism, positioning Asia-Pacific as a key growth hub for thyroid treatment solutions over the forecast period.

Latin America

Latin America represents 8% of the global thyroid gland treatment market, with Brazil and Mexico as the leading contributors. Growing healthcare investments, increased awareness of thyroid disorders, and improving diagnostic capabilities drive market expansion. Public health campaigns addressing iodine deficiency and rising incidence of hypothyroidism among aging populations further support demand. However, limited healthcare infrastructure in rural areas and lower affordability of branded drugs pose challenges. Expanding pharmaceutical distribution networks and the availability of cost-effective generic drugs are expected to improve treatment access, boosting the region’s market growth in the coming years.

Middle East & Africa

The Middle East & Africa region holds a 6% share of the thyroid gland treatment market, driven primarily by urban centers with advanced healthcare facilities. Gulf countries such as Saudi Arabia and the UAE lead the region due to higher healthcare spending and improved access to diagnostics. However, much of Africa faces challenges including limited awareness, inadequate healthcare infrastructure, and affordability issues. Growing government initiatives for iodine supplementation and international collaborations to improve healthcare access are gradually expanding the patient pool, offering long-term growth potential for thyroid treatments in this emerging region.

Market Segmentations:

By Drug Type:

- Levothyroxine

- Liothyronine

By Disease:

- Hypothyroidism

- Hyperthyroidism

By Route of Administration:

By Geography

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Competitive Landscape

The Thyroid Gland Disorder Treatment Market features players including Novartis AG, Glenmark Pharmaceuticals Ltd., Sun Pharmaceutical Industries Limited, Pfizer Inc., Abbott Laboratories, Merck & Co., Inc., Mylan N.V., AbbVie Inc., Aspen Pharmacare Holdings Limited, and Lannett Company, Inc. The thyroid gland treatment market is characterized by intense competition, with companies focusing on innovation, affordability, and accessibility to strengthen their positions. The market is witnessing growing investments in research and development aimed at improving drug formulations, including liquid and soft gel alternatives to enhance absorption and patient adherence. Expansion of generic drugs has also intensified competition by offering cost-effective options, particularly in developing regions. In addition, strategies such as mergers, acquisitions, and regional partnerships are widely adopted to broaden product portfolios and distribution networks. This competitive environment continues to drive advancements in treatment solutions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Novartis AG

- Glenmark Pharmaceuticals Ltd.

- Sun Pharmaceutical Industries Limited

- Pfizer Inc.

- Abbott Laboratories

- Merck & Co., Inc.

- Mylan N.V.

- AbbVie Inc.

- Aspen Pharmacare Holdings Limited

- Lannett Company, Inc.

Recent Developments

- In January 2025, Health Canada issued comprehensive update on biotin interference risks in thyroid function tests, emphasizing mandatory 7-day cessation protocols after documented clinical cases of false results leading to patient mismanagement.

- In October 2024, GE HealthCare took a leading role in Thera4Care, an initiative to revolutionize cancer care through theranostics. This personalized approach integrates imaging diagnostics and targeted therapeutics, using molecular imaging to visualize tumors and deliver radioactive drugs.

- In August 2024, Illumina’s TruSight Oncology (TSO) Comprehensive test secured FDA approval, marking a milestone as the pan-cancer companion diagnostic claims and the first distributable comprehensive genomic profiling IVD kit.

- In December 2023, Aspen Pharmacare Holdings Limited’s subsidiary, Aspen Global Incorporated, finalized agreements with Sandoz AG to acquire its Chinese business. This strategic move aligned with Aspen’s strategic goal of expanding its presence in China by leveraging Sandoz’s established portfolio, infrastructure, and experienced team for future growth in the region

Report Coverage

The research report offers an in-depth analysis based on Drug Type, Disease, Route of Administration and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with rising prevalence of hypothyroidism and hyperthyroidism worldwide.

- Demand for hormone replacement therapies will remain strong due to lifelong treatment needs.

- Development of novel drug formulations will improve patient compliance and treatment outcomes.

- Personalized medicine approaches will gain traction with genetic and biomarker-based therapies.

- Digital health tools will support remote monitoring and dose adjustments for better management.

- Emerging economies will offer high growth potential with expanding healthcare access and awareness.

- Generics will continue to drive affordability and improve accessibility in developing regions.

- Strategic collaborations between pharmaceutical firms and healthcare providers will strengthen distribution.

- Government initiatives and public health programs will support early diagnosis and treatment adoption.

- Innovation in sustained-release and alternative delivery routes will reduce dosing challenges.