Market Overview

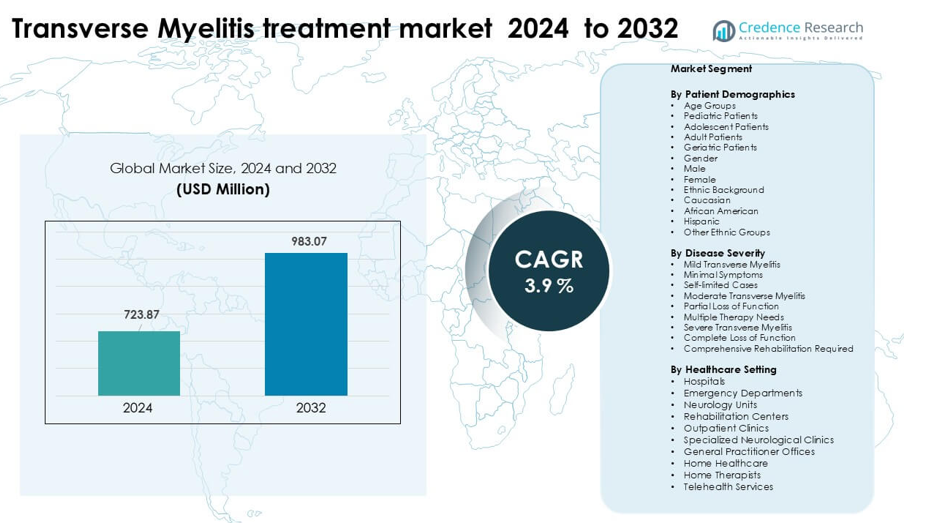

Transverse Myelitis treatment market was valued at USD 723.87 million in 2024 and is anticipated to reach USD 723.87 million by 2032, growing at a CAGR of 3.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Transverse Myelitis treatment market Size 2024 |

USD 723.87 million |

| Transverse Myelitis treatment market, CAGR |

3.9% |

| Transverse Myelitis treatment market Size 2032 |

USD 723.87 million |

North America led the transverse myelitis treatment market in 2024 with about 41% share, driven by strong access to advanced immunotherapies, high diagnostic rates, and broad insurance coverage. Key companies shaping the competitive space include Pfizer, B. Braun Melsungen AG, Johnson & Johnson, GSK, Amgen, Fresenius Kabi AG, Bayer AG, Bristol-Myers Squibb, Haemonetics Corporation, and Medtronic. These firms expanded offerings across corticosteroids, plasma-exchange devices, monoclonal antibodies, and supportive neurological care. Their focus on clinical research, wider treatment availability, and strong hospital partnerships supported dominance in regions with mature healthcare systems, while emerging markets saw steady adoption through expanding neurology care infrastructure.

Market Insights

- The transverse myelitis treatment market reached USD 723.87 million in 2024 and is projected to hit USD 983.07 million by 2032, expanding at a 3.9 % CAGR.

- Growth is driven by rising autoimmune disorders, faster neurological diagnostics, and wider use of corticosteroids, plasma-exchange systems, and biologics that improve acute recovery outcomes.

- Key trends include increasing adoption of monoclonal antibodies, higher investment in MRI-guided monitoring, and expanding clinical trials focused on targeted immunomodulation for both acute and recurrent cases.

- Competition features Pfizer, Johnson & Johnson, GSK, Amgen, B. Braun Melsungen AG, Fresenius Kabi AG, Bayer AG, Bristol-Myers Squibb, Haemonetics Corporation, and Medtronic, with firms expanding product portfolios and hospital partnerships.

- North America held the leading 41% share in 2024, supported by strong reimbursement and advanced neurology care, while corticosteroid therapy maintained the dominant segment share due to broad first-line adoption across global treatment centers.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Patient Demographics

Adult patients held the dominant share with about 46% in 2024. Adults showed the highest treatment demand because they report more autoimmune triggers, post-infection inflammation, and neurological complications that require timely diagnosis and structured therapy. Pediatric and adolescent groups saw steady growth due to rising awareness and early MRI screening, while geriatric patients required more intensive care because of comorbidities. Female patients continued to represent a higher clinical load compared to male patients, and Caucasian and African American groups reported higher incidence rates, driving their stronger treatment uptake.

- For instance, in a U.S. study of neuromyelitis optica spectrum disorder (NMOSD), researchers found that the prevalence among adults aged 35–64 reached above 9.5 per 100,000, whereas prevalence in pediatric age groups (under 14) was only about 1.7 per 100,000.

By Disease Severity

Moderate transverse myelitis led the segment in 2024 with nearly 49% share. These patients often experience partial loss of function and need multiple therapy inputs, including corticosteroids, plasma exchange, and physical rehabilitation. Mild cases remained stable due to self-limited progression and low intervention needs, while severe transverse myelitis cases required long-term rehabilitation and advanced neurological management. Increased clinical reporting, broader MRI access, and strengthened referral pathways supported the dominance of moderate cases because clinicians prioritized faster intervention to prevent progression toward severe disability.

- For instance, in a global clinical‑record analysis of neuromyelitis optica spectrum disorder (NMOSD) relapses, among 520 relapses classified as “moderate,” only 69 (13%) achieved full recovery, compared to 264 out of 522 (51%) in the “mild” category.

By Healthcare Setting

Hospitals dominated the segment with about 54% share in 2024. Hospitals remained the primary care hub as most patients present through emergency departments or neurology units for rapid clinical evaluation, imaging, and acute treatment. Rehabilitation centers showed expanding use due to long-term physical therapy needs, while outpatient clinics and specialized neurological centers gained traction for follow-up care. Home healthcare and telehealth services grew steadily as supportive care options, but hospitals continued to lead because they offer multidisciplinary teams, advanced diagnostics, and immediate treatment protocols essential for acute transverse myelitis management.

Key Growth Drivers

Rising Autoimmune and Post-Infectious Cases

Growing autoimmune disorders and post-infectious complications continue to drive the global demand for transverse myelitis treatment. More adults and young patients experience immune-mediated spinal cord inflammation linked to viral infections, post-vaccination responses, and systemic autoimmune diseases. Increased diagnostic accuracy through rapid MRI and antibody testing contributes to higher case identification, which pushes healthcare systems to strengthen treatment pathways. Hospitals report more admissions for acute neurological symptoms, creating strong demand for corticosteroids, plasma exchange, and immunotherapies. As more countries introduce structured neurology referral systems, early diagnosis improves, and this expands the overall treatment volume across both public and private facilities.

- For instance, a retrospective cohort analysis of over 960,000 SARS‑CoV-2 patients found that those infected had a 1.46-fold higher hazard of developing acute transverse myelitis (ATM) within one year compared to non-infected individuals indicating a real‑world linkage between COVID‑19 infection and increased TM burden.

Advancements in Neurological Imaging and Diagnostics

Better imaging access enhances early detection and treatment success, making diagnostics a major growth driver. High-resolution MRI, CSF analysis, and autoimmune biomarker panels now help clinicians identify inflammation patterns faster. Neurology units rely on rapid imaging to differentiate transverse myelitis from related disorders such as MS or NMOSD, which improves treatment precision. Many hospitals have invested in AI-assisted MRI interpretation, enabling faster triage and reduced diagnostic delays. Screening programs in pediatric and adult neurology have also expanded, raising case identification rates. Improved imaging infrastructure in emerging markets strengthens adoption of evidence-based treatment protocols and boosts overall market growth.

- For instance, modern AQP4‑IgG cell‑based assays (CBAs) have shown sensitivity between 90–94% and specificity up to 100%, substantially improving diagnostic accuracy in NMOSD over older ELISA or immunofluorescence methods.

Expansion of Rehabilitation and Long-Term Care Services

Rehabilitation centers and specialized therapy units play a growing role in market expansion. Many transverse myelitis patients require long-term mobility support, gait training, and strength recovery, pushing demand for physiotherapy, occupational therapy, and assistive technologies. Hospitals refer moderate and severe patients to structured rehab programs to prevent muscle loss and improve functional outcomes. Home-based therapy and tele-rehabilitation also grow as cost-effective options, increasing access for patients in remote regions. Rising awareness of rehabilitation benefits among families and caregivers encourages early therapy enrollment. This growing ecosystem of rehabilitation services supports sustained treatment demand across age groups.

Key Trend & Opportunity

Growth of Telehealth-Enabled Neurology Care

Telehealth adoption creates major opportunities for follow-up care and remote management of transverse myelitis patients. Digital neurology consultations help patients monitor symptoms, manage medications, and adjust therapy plans without frequent hospital visits. Rehabilitation providers now use virtual platforms to deliver guided physiotherapy sessions, widening access for rural and mobility-restricted patients. The rise of digital health programs also allows better continuity of care after hospital discharge. Remote monitoring devices, digital exercise tools, and AI-based symptom tracking support ongoing management and reduce relapse risks. As countries expand telemedicine reimbursement, providers can scale neurological care more efficiently.

- For instance, in a rural inpatient teleneurology program in the U.S., 138 out of 251 patients (about 55%) received exclusively remote neurology consults via a team of eight off-site neurologists, with only 4 patients (1.6%) needing transfer for higher‑level care.

Increasing Development of Novel Immunotherapies

Research in immunology and neuroinflammation drives opportunities for advanced treatment options. Pharmaceutical companies focus on developing monoclonal antibodies, precision immunotherapies, and targeted anti-inflammatory agents for autoimmune-related spinal cord disorders. Clinical trials for biologics and cell-based therapies offer potential improvements in recovery time and long-term functional outcomes. Hospitals and academic institutes collaborate on early-stage research to understand immune pathways that trigger transverse myelitis. Growing investment in neurology R&D encourages the launch of innovative therapies with fewer side effects. As more regulators approve advanced treatments, the market gains strong momentum across major regions.

- For instance, inebilizumab, a humanized anti‑CD19 monoclonal antibody, was tested in a phase II/III N‑MOmentum trial with 174 treated participants; only 12% of them had an NMOSD attack, versus 39% in the placebo arm.

Key Challenge

Delayed Diagnosis and Limited Specialist Access

Many patients face delayed diagnosis due to limited awareness and restricted access to neurology specialists, especially in low-resource regions. Early symptoms often mimic other neurological conditions, causing late referrals and treatment delays. Rural hospitals may lack MRI equipment, antibody tests, or trained neurologists, which reduces early detection rates. Late diagnosis increases severity, raises hospitalization costs, and complicates rehabilitation outcomes. Healthcare systems must improve referral pathways and expand specialist availability to reduce diagnostic gaps. Without stronger screening infrastructure and physician training, treatment effectiveness remains inconsistent across regions.

High Long-Term Treatment and Rehabilitation Costs

Transverse myelitis often requires prolonged and costly care, creating a significant challenge for patients and healthcare systems. Acute treatment may involve immunotherapies, plasma exchange, and intensive hospitalization, followed by months or years of rehabilitation. Many families struggle with the economic burden of therapy, mobility aids, home modifications, and caregiver support. Insurance coverage remains uneven, especially for long-term physiotherapy and psychological support. These financial pressures delay therapy enrollment and reduce adherence to treatment plans. Expanding affordable rehabilitation programs and improving reimbursement policies are essential to address this barrier.

Regional Analysis

North America

North America held the dominant share of about 41% in 2024 due to strong neurological care infrastructure, wide insurance coverage, and early adoption of MRI and immunotherapy. Hospitals and neurology units manage a high volume of autoimmune and post-infectious transverse myelitis cases, supported by rapid diagnostic workflows. The U.S. leads the region with advanced specialty centers and expanded rehabilitation programs, while Canada shows steady demand through universal healthcare systems. Growing tele-neurology networks and structured referral pathways continue to improve early detection and long-term care, reinforcing the region’s leading position.

Europe

Europe accounted for nearly 29% share in 2024, driven by strong public healthcare systems and high access to specialized neurological care across major countries such as Germany, France, and the U.K. Widespread use of high-resolution MRI and immunomodulatory therapies supports early treatment. Rehabilitation units maintain consistent demand due to structured post-acute therapy programs. Eastern Europe shows rising diagnosis rates as hospitals upgrade imaging tools and expand neurology capacity. Growing clinical research collaborations and government-supported neurology initiatives strengthen the region’s overall treatment ecosystem.

Asia Pacific

Asia Pacific captured about 22% share in 2024, supported by expanding hospital networks, increased MRI availability, and rising awareness of autoimmune neurological conditions. China, Japan, and India remain major contributors due to large patient populations and rapid healthcare modernization. Rehabilitation centers and physiotherapy chains continue to grow, improving long-term care access. Telehealth and remote neurology consultations gain traction in urban and semi-urban areas, improving follow-up treatment. As governments invest in neurology infrastructure and specialist training, early diagnosis rates rise and regional market penetration strengthens.

Latin America

Latin America held nearly 5% share in 2024, with demand driven by growing neurology capacity in Brazil, Mexico, and Argentina. Many patients still face diagnostic delays due to limited MRI access in rural areas, but tertiary hospitals in major cities provide advanced treatment and immunotherapies. Rehabilitation services expand as awareness increases and private therapy centers grow. Telemedicine adoption improves follow-up care and symptom monitoring. Strengthening public healthcare programs and increased investment in neurology training continue to support gradual market growth across the region.

Middle East & Africa

The Middle East & Africa accounted for about 3% share in 2024, reflecting uneven access to neurological care across countries. Gulf nations such as the UAE and Saudi Arabia lead regional demand due to advanced hospitals, strong imaging infrastructure, and greater uptake of immunotherapies. In contrast, many African nations experience delays in diagnosis and limited rehabilitation availability. International aid programs and private hospital expansions improve access slowly. Growing investment in digital health, cross-border treatment partnerships, and neurology workforce development support steady but gradual market improvement.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Market Segmentations:

By Patient Demographics

- Age Groups

- Pediatric Patients

- Adolescent Patients

- Adult Patients

- Geriatric Patients

- Gender

- Male

- Female

- Ethnic Background

- Caucasian

- African American

- Hispanic

- Other Ethnic Groups

By Disease Severity

- Mild Transverse Myelitis

- Minimal Symptoms

- Self-limited Cases

- Moderate Transverse Myelitis

- Partial Loss of Function

- Multiple Therapy Needs

- Severe Transverse Myelitis

- Complete Loss of Function

- Comprehensive Rehabilitation Required

By Healthcare Setting

- Hospitals

- Emergency Departments

- Neurology Units

- Rehabilitation Centers

- Outpatient Clinics

- Specialized Neurological Clinics

- General Practitioner Offices

- Home Healthcare

- Home Therapists

- Telehealth Services

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape in the transverse myelitis treatment market features major healthcare firms such as Pfizer, B. Braun Melsungen AG, Johnson & Johnson, GSK, Amgen, Fresenius Kabi AG, Bayer AG, Bristol-Myers Squibb, Haemonetics Corporation, and Medtronic. These companies expanded portfolios through advanced immunotherapies, plasma-exchange systems, corticosteroid formulations, and biologics that support faster recovery and relapse control. Competitive focus stayed strong on developing therapies that reduce inflammation and prevent long-term neurological damage. Firms invested in clinical trials for targeted monoclonal antibodies and next-generation steroid protocols to improve outcomes in acute and chronic cases. Partnerships with neurology centers and research institutes increased access to novel pipeline drugs. Market participants strengthened diagnostic integration with MRI-guided monitoring tools, allowing treatment alignment with disease progression. Overall competition intensified as companies enhanced global distribution, expanded reimbursement coverage, and improved patient-support programs to gain a wider share in the transverse myelitis treatment market.

Key Player Analysis

- Pfizer

- Braun Melsungen AG

- Johnson & Johnson

- GSK

- Amgen

- Fresenius Kabi AG

- Bayer AG

- Bristol-Myers Squibb

- Haemonetics Corporation

- Medtronic

Recent Developments

- In October 2025, Bristol-Myers Squibb Bristol-Myers Squibb presented Phase 1 Breakfree-1 data on its CD19 NEX-T CAR-T cell therapy BMS-986353 in three severe autoimmune diseases at ACR Convergence 2025. The trial showed deep B-cell depletion, signs of immune “reset,” and most patients remaining off chronic immunosuppressants, strengthening a pipeline that could support future immune-reset approaches for neuro-inflammatory disorders related to transverse myelitis treatment needs.

- In February 2025, B. Braun Melsungen AG continues to be identified in 2024–2025 apheresis/therapeutic-plasma-exchange market reports and on its product pages as a key supplier of apheresis / plasmapheresis systems and disposables. As therapeutic plasma exchange (TPE) and apheresis are standard escalation treatments for steroid-refractory TM, B. Braun’s ongoing product activity and presence in apheresis market analyses is a market development that affects TM treatment capacity and hospital purchasing decisions.

- In April 2024, Medtronic obtained FDA approval for its Inceptiv closed-loop rechargeable spinal cord stimulator for chronic pain, the company’s first SCS device with real-time biologic sensing. Advanced SCS systems like Inceptiv are relevant to transverse myelitis care because spinal cord stimulation has shown benefit in case reports for TM-related neuropathic pain and functional deficits, expanding neuromodulation options within the transverse myelitis treatment market.

Report Coverage

The research report offers an in-depth analysis based on Patient Demographics, Disease Severity, Healthcare Setting and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for advanced immunotherapies will rise as targeted treatments gain wider approval.

- Biologics will expand use due to stronger relapse control and better long-term outcomes.

- MRI-based monitoring will become standard for guiding personalized treatment plans.

- Plasma-exchange systems will see higher adoption in acute and severe episodes.

- Clinical trials will accelerate development of next-generation monoclonal antibodies.

- Digital tools will support faster diagnosis and improve patient-tracking accuracy.

- Hospitals will increase investment in neurology units to manage autoimmune cases.

- Emerging markets will adopt modern therapies as healthcare access improves.

- Companies will strengthen collaborations with research institutes for pipeline growth.

- Reimbursement coverage will expand as payers recognize long-term recovery benefits.