Market Overview:

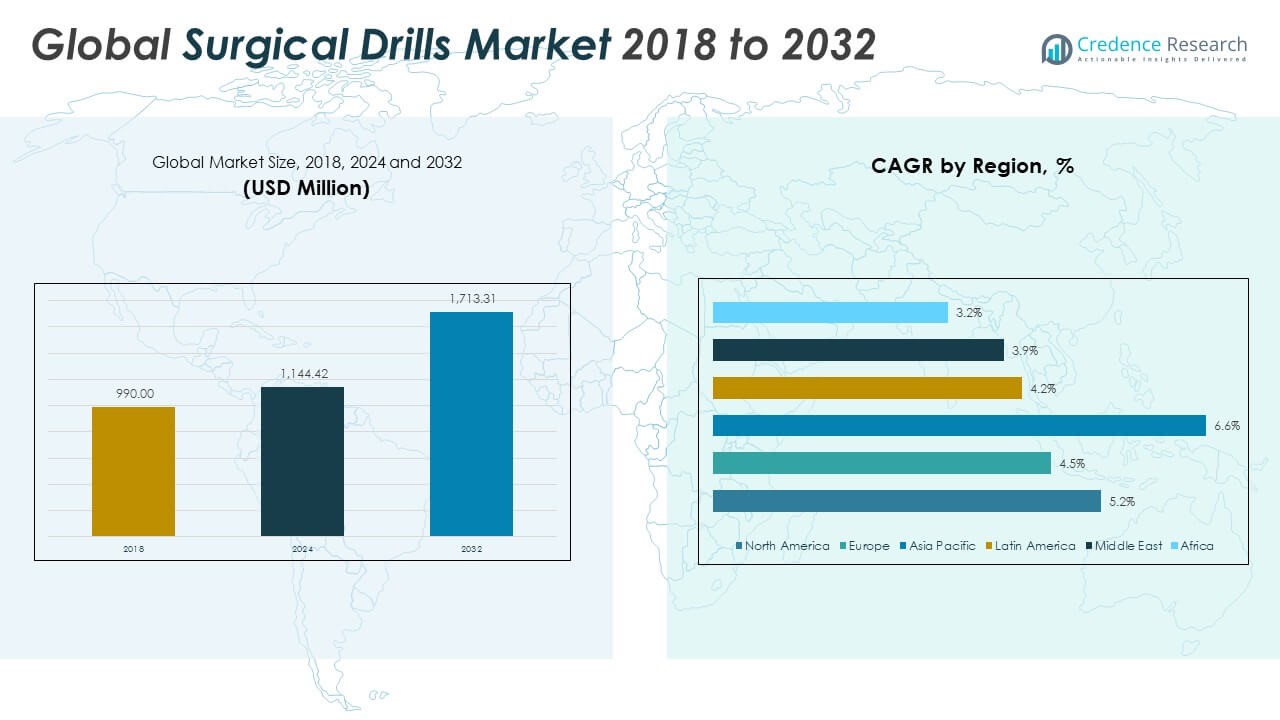

The Global Surgical Drills Market size was valued at USD 990.00 million in 2018 to USD 1,144.42 million in 2024 and is anticipated to reach USD 1,713.31 million by 2032, at a CAGR of 5.21% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Surgical Drills Market Size 2024 |

USD 1,144.42 million |

| Surgical Drills Market, CAGR |

5.21% |

| Surgical Drills Market Size 2032 |

USD 1,713.31 million |

The primary driver of the surgical drills market is the growing global burden of chronic conditions, trauma, and degenerative diseases that often necessitate surgical intervention. An aging global population, particularly in North America, Europe, and parts of Asia, is contributing to a surge in orthopedic procedures such as hip and knee replacements, spinal surgeries, and dental implants. Technological advancements in surgical drills—including the adoption of cordless, smart, and robotic-compatible models—are significantly improving operating room efficiency and surgical accuracy. Moreover, the trend toward minimally invasive surgery is increasing demand for compact and high-precision drills that offer enhanced control and reduced patient recovery time. Government investments in healthcare infrastructure and medical device innovation, especially in emerging economies, are also playing a critical role in supporting market expansion.

Regionally, North America dominates the global surgical drills market, accounting for the largest share due to its well-established healthcare infrastructure, advanced surgical technology adoption, and high volume of surgical procedures. Europe follows closely, driven by supportive regulatory frameworks and an aging population demanding orthopedic and neurological care. The Asia Pacific region, however, is emerging as the fastest-growing market, spurred by rapid urbanization, rising healthcare expenditure, and a growing medical tourism industry in countries like China, India, and South Korea. Latin America and the Middle East & Africa regions are experiencing moderate growth, largely supported by gradual improvements in healthcare access and increasing awareness about advanced surgical solutions. Together, these regional dynamics reflect a steadily evolving market landscape shaped by demographic trends, medical innovation, and regional healthcare investments.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Global Surgical Drills Market grew from USD 990.00 million in 2018 to USD 1,144.42 million in 2024 and is projected to reach USD 1,713.31 million by 2032, at a CAGR of 5.21%.

- The increasing number of trauma cases, degenerative diseases, and orthopedic conditions among the aging population is significantly driving demand for surgical drills worldwide.

- Surgeons are shifting toward compact, cordless, and robotic-compatible drills to support minimally invasive techniques that reduce recovery time and improve outcomes.

- Smart drills, battery-powered systems, and single-use components are enhancing device efficiency, safety, and performance in high-precision surgical environments.

- Rapid healthcare infrastructure development in Asia Pacific and Latin America is creating strong demand, supported by government investment and higher patient volumes.

- High costs of advanced drills and ongoing maintenance limit adoption in budget-constrained healthcare systems, especially in developing countries.

- North America holds the largest market share due to high surgical volumes and advanced technology adoption, while Asia Pacific emerges as the fastest-growing region.

Market Drivers:

Growing Surgical Procedure Volume Due to Aging Population and Trauma Cases:

The rising number of surgical procedures worldwide is a significant driver of the Global Surgical Drills Market. Increasing incidences of trauma, sports injuries, road accidents, and age-related orthopedic conditions are contributing to a surge in demand for surgical interventions. The expanding geriatric population, particularly in developed nations, faces a higher risk of fractures, joint degeneration, and spinal disorders, all of which require precision surgical tools. It is prompting hospitals and surgical centers to invest in efficient and safe drilling equipment. The demand is especially strong in orthopedics and neurosurgery, where accuracy and control are critical. With healthcare providers focusing on enhancing surgical outcomes, surgical drills have become a standard requirement in both elective and emergency procedures.

- For instance, Stryker’s System 8 power tools are widely used in orthopedic and trauma procedures, with the product line specifically designed for enhanced ergonomics, reliability, and precision. The System 8 family includes saws and rotary drills developed in collaboration with orthopedic surgeons, featuring improved grip, neutral wrist positioning, and advanced materials to prevent sticking and slipping during procedures.

Rising Demand for Minimally Invasive and Robotic-Assisted Surgeries:

Minimally invasive procedures are gaining traction due to shorter recovery times, less postoperative pain, and reduced hospital stays. This trend is pushing manufacturers to develop smaller, more accurate, and ergonomically designed surgical drills. The Global Surgical Drills Market is responding to this demand by integrating advanced features such as high-torque, cordless operation and compatibility with robotic systems. It enables surgeons to perform complex procedures with greater precision while maintaining a minimally invasive approach. Robotic-assisted surgeries, particularly in neurology and orthopedics, require highly specialized drills that provide control over speed and depth. This shift is influencing purchasing decisions across surgical departments and healthcare facilities globally.

- For instance, DePuy Synthes (Johnson & Johnson) launched the UNIUM™ System for small bone, sports medicine, spine, and thorax procedures. The UNIUM System is 19% lighter, 26% smaller, and 18% more powerful than its predecessors. It features modular handpieces and a high-capacity Li-ion battery with over 1,000 use-and-charging cycles, supporting aseptic transfer and reducing sterilization needs.

Technological Advancements Enhancing Device Functionality and Efficiency:

Continuous improvements in surgical drill design and functionality are fueling market growth. Innovations include battery-powered systems, smart drills with integrated feedback mechanisms, and systems designed for single-use to improve hygiene and reduce cross-contamination. The Global Surgical Drills Market is benefitting from increased investments in R&D aimed at creating safer and more user-friendly devices. It supports the need for accuracy and reliability in high-stakes surgical environments. Hospitals are adopting these innovations to improve operating room efficiency, reduce manual fatigue, and shorten overall procedure time. New developments in material science and electronics are also contributing to the durability and adaptability of modern surgical drills.

Expansion of Healthcare Infrastructure and Procedural Capabilities in Emerging Markets:

The rapid development of healthcare infrastructure in emerging economies is boosting the demand for surgical equipment. Governments and private entities are investing heavily in building hospitals, equipping operating rooms, and training medical personnel. The Global Surgical Drills Market is expanding in regions like Asia Pacific and Latin America, where patient volumes are high and access to advanced care is improving. It aligns with the increasing emphasis on universal healthcare and improved surgical care access. Manufacturers are entering these markets through partnerships, local distribution networks, and cost-effective product lines. This regional expansion is playing a key role in supporting the market’s long-term growth trajectory.

Market Trends:

Increased Adoption of Disposable and Single-Use Surgical Drill Components:

Hospitals and surgical centers are increasingly prioritizing infection control, which is leading to higher adoption of disposable and single-use surgical drill components. These products help reduce the risk of cross-contamination, improve operational efficiency, and eliminate the need for complex sterilization procedures. The Global Surgical Drills Market is witnessing a shift toward pre-sterilized, ready-to-use drill kits that support high surgical turnover and meet strict hygiene standards. It is helping healthcare providers reduce labor costs and meet regulatory compliance with ease. Disposable drills are particularly gaining acceptance in outpatient settings and ambulatory surgical centers. Manufacturers are responding by developing compact, affordable, and reliable disposable solutions tailored for high-volume procedures.

- For instance, Medtronic’s Midas Rex™ MR8™ system includes electric high-speed drills designed for use with disposable dissecting tools. The MR8 motors operate at selectable speeds up to 75,000 rpm and are compatible with a range of attachments for various surgical procedures.

Growing Preference for Ergonomically Designed and Lightweight Devices:

Surgeons increasingly prefer ergonomically optimized surgical drills that minimize fatigue and enhance control during lengthy procedures. This trend is influencing design innovation, with manufacturers focusing on reduced weight, improved handgrip contours, and better balance in drill bodies. The Global Surgical Drills Market is responding with products that enhance user comfort without compromising torque or precision. It supports both safety and procedural efficiency, especially in specialties like orthopedic trauma and spine surgery. Surgeons are also demanding customizable speed settings and intuitive controls for greater precision. These ergonomic advances are becoming critical for product differentiation and market competitiveness.

- For example, Zimmer Biomet’s X Series Power System is engineered to be lightweight and ergonomic, with modular attachments for various orthopedic procedures. The system offers real-time power status, streamlined battery charging, and is designed for easy sterilization, meeting hospital cleaning requirements.

Integration of Connectivity and Data-Driven Capabilities in Drills:

The demand for smarter surgical tools is encouraging the integration of connectivity features in surgical drills. Bluetooth-enabled or digitally controlled drills are enabling real-time data capture, usage tracking, and performance analytics. The Global Surgical Drills Market is gradually adopting such features to support preventive maintenance, improve inventory control, and enhance post-procedure reporting. It aligns with the broader healthcare trend of digital transformation and intelligent operating room systems. These capabilities are also proving useful in training environments, allowing surgical teams to analyze performance and refine techniques. Data integration is emerging as a key value addition in high-end drill models.

Increased Customization and Specialty-Specific Drill Variants:

Healthcare facilities are seeking surgical drills tailored to the unique demands of specific procedures and specialties. This trend is leading to the development of drill models with specialty-specific features, such as micro-drills for neurosurgery or high-speed bone drills for maxillofacial applications. The Global Surgical Drills Market is evolving to provide modular systems that allow quick adaptation based on clinical needs. It is enabling surgeons to work with tools that match the precision requirements of each procedure type. Manufacturers are offering kits with interchangeable attachments and heads to support versatile usage. Customization is becoming a critical factor in procurement decisions for both large hospitals and specialty clinics.

Market Challenges Analysis:

High Cost of Advanced Surgical Drills and Limited Access in Low-Income Regions:

The cost of technologically advanced surgical drills poses a significant barrier to adoption, particularly in low- and middle-income countries. Premium features such as smart sensors, battery-powered functionality, and robotic compatibility elevate the overall price of these devices. The Global Surgical Drills Market faces constraints in price-sensitive markets where budget limitations restrict procurement of next-generation equipment. It is especially challenging for public hospitals and smaller healthcare centers that lack the resources to invest in high-end tools. The expense associated with regular maintenance, replacement parts, and training further compounds the issue. These financial challenges slow down market penetration and limit the availability of modern drills in underserved regions.

Stringent Regulatory Requirements and Product Approval Delays:

Medical device regulations vary significantly across regions, requiring manufacturers to meet a complex set of safety and quality standards before product launch. Navigating these regulatory landscapes often leads to delays in product approvals and extended time-to-market. The Global Surgical Drills Market must comply with certifications such as FDA clearance, CE marking, and other country-specific protocols, each demanding detailed clinical validation and documentation. It places a burden on manufacturers, especially smaller players, who must allocate significant resources for compliance. Regulatory hurdles also impact innovation cycles, slowing down the introduction of upgraded models. In a highly competitive market, these delays can limit a company’s ability to respond swiftly to evolving clinical needs.

Market Opportunities:

Expansion of Ambulatory Surgical Centers and Outpatient Procedures:

The growing shift toward outpatient and same-day surgeries is creating new demand for portable, efficient, and easy-to-use surgical drills. Ambulatory surgical centers are increasing in number due to their cost-effectiveness and faster patient turnover. The Global Surgical Drills Market can capitalize on this trend by offering compact, cordless, and disposable drill systems tailored for high-frequency, short-duration procedures. It aligns well with the operational needs of these facilities that prioritize mobility, sterilization ease, and procedural speed. Manufacturers have an opportunity to design targeted solutions that address workflow efficiency in non-hospital surgical settings. This expansion supports higher volume sales and greater product customization potential.

Rising Demand in Emerging Healthcare Markets:

Emerging economies are making significant investments in healthcare infrastructure, medical training, and surgical capacity. The Global Surgical Drills Market has strong growth potential in countries across Asia Pacific, Latin America, and the Middle East where surgical volumes are rising. It can leverage localized manufacturing, public-private partnerships, and cost-effective product lines to address regional needs. Demand for orthopedic, dental, and trauma surgeries continues to grow alongside urbanization and better healthcare access. Manufacturers who adapt their distribution models and pricing strategies for these markets can build lasting competitive advantages. This geographic expansion provides a critical pathway for long-term market sustainability.

Market Segmentation Analysis:

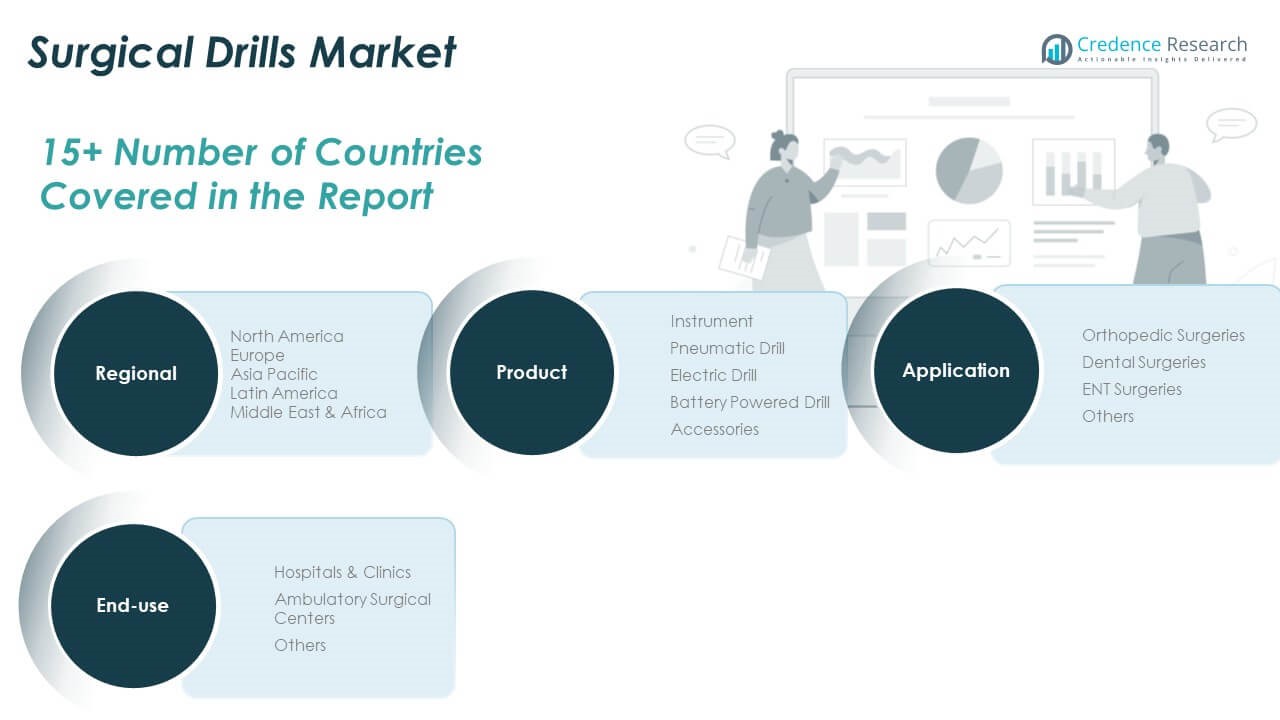

By Product

The Global Surgical Drills Market is categorized into instruments and accessories. Within instruments, battery-powered drills are witnessing growing demand due to their portability, ease of use, and cordless functionality. Electric drills remain widely used for their precision and reliability in complex procedures. Pneumatic drills, though older in design, are still utilized in high-volume surgical environments for their robustness. Accessories—including drill bits, heads, and sterilization trays—contribute significantly to recurring revenue and enhance the functionality of core systems.

- For instance, B. Braun’s Aesculap® Acculan 4 Mini is a battery-driven power system used in orthopedics and traumatology, featuring a titanium housing, a wide range of attachments, and a proven EC motor for reliability and long life.

By Application

The market spans applications such as orthopedic surgeries, dental surgeries, ENT surgeries, and others. Orthopedic surgeries hold the largest share, driven by a global rise in trauma cases, joint replacements, and spinal interventions. Dental surgeries are expanding steadily due to growing awareness of oral health and increasing demand for implants and maxillofacial procedures. ENT surgeries represent a niche but stable segment, with technological integration supporting minimally invasive procedures. Other applications include neurosurgery and veterinary use.

- For instance, NSK Nakanishi is a leading manufacturer of surgical drills for dental procedures. The Surgic Pro2 micromotor system, launched in 2025, features wireless connectivity, intuitive controls, and is designed for precision in dental implant placement. The Osseo 100+ device provides implant stability measurements, optimizing treatment protocols and outcomes.

By End-use

End-use segments include hospitals & clinics, ambulatory surgical centers, and others. Hospitals & clinics dominate the market, backed by comprehensive infrastructure, high patient volumes, and access to advanced surgical technologies. Ambulatory surgical centers are growing rapidly, fueled by demand for same-day surgeries and cost-effective care. It supports a shift in healthcare delivery, emphasizing efficiency and patient convenience across surgical services.

Segmentation:

By Product

- Instrument

- Pneumatic Drill

- Electric Drill

- Battery Powered Drill

- Accessories

By Application

- Orthopedic Surgeries

- Dental Surgeries

- ENT Surgeries

- Others

By End-use

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America Surgical Drills Market size was valued at USD 365.21 million in 2018 to USD 417.13 million in 2024 and is anticipated to reach USD 623.65 million by 2032, at a CAGR of 5.2% during the forecast period. North America holds the largest share of the Global Surgical Drills Market, accounting for over 36% of global revenue. It benefits from a well-established healthcare system, high surgical volumes, and rapid adoption of advanced surgical technologies. The presence of major market players and continuous innovation in drill design contribute to sustained demand. Hospitals in the U.S. and Canada are increasingly investing in battery-powered and robotic-compatible devices to improve procedural outcomes. It also reflects high awareness among medical professionals and favorable reimbursement policies.

Europe

The Europe Surgical Drills Market size was valued at USD 284.63 million in 2018 to USD 317.32 million in 2024 and is anticipated to reach USD 451.03 million by 2032, at a CAGR of 4.5% during the forecast period. Europe represents around 28% of the Global Surgical Drills Market, supported by robust public healthcare systems and a growing elderly population. Countries like Germany, France, and the UK are leading adopters of orthopedic and dental surgical drills. The market benefits from strict regulatory standards, which ensure product quality and patient safety. It also shows strong uptake of minimally invasive procedures, increasing the need for compact, high-precision tools. Regional manufacturers and distributors are expanding their portfolios to meet evolving surgical demands.

Asia Pacific

The Asia Pacific Surgical Drills Market size was valued at USD 218.79 million in 2018 to USD 265.33 million in 2024 and is anticipated to reach USD 442.55 million by 2032, at a CAGR of 6.6% during the forecast period. Asia Pacific is the fastest-growing region in the Global Surgical Drills Market, accounting for over 23% of global share in 2024. Rapid urbanization, increasing healthcare expenditure, and the growth of medical tourism are fueling demand. Countries such as China, India, Japan, and South Korea are investing in surgical infrastructure and expanding procedural capabilities. It is attracting global players seeking to tap into high-volume markets with localized product strategies. Government efforts to improve access to advanced surgical care are further supporting growth.

Latin America

The Latin America Surgical Drills Market size was valued at USD 57.32 million in 2018 to USD 65.56 million in 2024 and is anticipated to reach USD 90.41 million by 2032, at a CAGR of 4.2% during the forecast period. Latin America holds approximately 6% of the Global Surgical Drills Market, with Brazil and Mexico leading regional demand. The market is gradually expanding due to increased healthcare investments and rising awareness of advanced surgical tools. Private hospitals are upgrading surgical suites with modern equipment, including electric and battery-powered drills. It remains price-sensitive, driving the need for cost-effective solutions. International companies are forming distribution partnerships to strengthen market presence.

Middle East

The Middle East Surgical Drills Market size was valued at USD 38.51 million in 2018 to USD 41.76 million in 2024 and is anticipated to reach USD 56.55 million by 2032, at a CAGR of 3.9% during the forecast period. The Middle East accounts for a modest share of the Global Surgical Drills Market, supported by healthcare modernization initiatives across the GCC. Countries such as the UAE and Saudi Arabia are investing in surgical infrastructure to meet rising demand for orthopedic and dental procedures. It reflects increasing demand from both public and private healthcare institutions. Regional hospitals are adopting advanced surgical tools to improve care quality and attract medical tourists. However, slower adoption in less developed areas limits full regional potential.

Africa

The Africa Surgical Drills Market size was valued at USD 25.54 million in 2018 to USD 37.31 million in 2024 and is anticipated to reach USD 49.12 million by 2032, at a CAGR of 3.2% during the forecast period. Africa represents the smallest share of the Global Surgical Drills Market, with limited access to advanced surgical technologies across many countries. Growth is driven by gradual improvements in healthcare infrastructure, particularly in South Africa and Egypt. Public health programs and international aid are helping expand surgical capabilities. It remains a challenging market due to budget constraints and shortage of trained medical professionals. Local demand is rising, but affordability and supply chain limitations continue to hinder widespread adoption.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Arthrex, Inc.

- Braun SE

- Medtronic

- Johnson & Johnson Services, Inc.

- Stryker

- Apothecaries Sundries Manufacturing Co.

- ConMed Corporation

- 3M

- MicroAire

- Zimmer Biomet

Competitive Analysis:

The Global Surgical Drills Market is moderately consolidated, with a mix of established multinational players and regional manufacturers competing on innovation, pricing, and product reliability. Leading companies such as Stryker, Medtronic, Johnson & Johnson, and B. Braun SE dominate the market through broad product portfolios, strong distribution networks, and consistent investments in R&D. It sees active participation from specialized firms like Arthrex, ConMed Corporation, and MicroAire, which focus on ergonomic and procedure-specific solutions. Competitive dynamics are influenced by rapid advancements in battery-powered and smart drills, pushing companies to differentiate through performance, safety, and ease of use. Strategic mergers, acquisitions, and product launches are common growth tactics. Emerging players in Asia and Latin America are gaining ground with cost-effective alternatives, creating pressure on global brands to localize offerings. The market rewards innovation, clinical effectiveness, and regulatory compliance, with companies aligning portfolios to meet the rising demand for minimally invasive and robotic-assisted procedures.

Recent Developments:

- In June 2025, Arthrex, Inc. launched the Synergy Power™ system, a new battery-powered instrument suite designed for a wide range of orthopedic procedures including sports medicine, arthroplasty, trauma, and distal extremities. The system features two ergonomic handpieces—a dual trigger rotary drill with a unique twist mechanism for rapid attachment changes, and a sagittal saw with an open hub for easy cleaning. The Synergy Power system utilizes 13.2V sterilizable lithium-ion batteries and is manufactured in the United States.

- In June 2025, Johnson & Johnson also introduced the ETHICON™ 4000 Stapler, which will be integrated into future robotic systems.

- In June 2025, Medtronic announced a strategic partnership with IRCAD North America, a leading surgical training and innovation center. The collaboration will integrate Medtronic’s advanced surgical technologies, including the Hugo™ robotic-assisted surgery system and AiBLE™ smart ecosystem, into IRCAD’s curriculum for hands-on training in minimally invasive and robotic-assisted procedures. This partnership aims to accelerate surgical innovation and enhance clinical education for thousands of surgeons annually.

- In April 2025, Johnson & Johnson MedTech launched the DUALTO™ Energy System, an integrated surgical platform that combines multiple energy modalities for use in both open and minimally invasive surgeries. The DUALTO system is designed for compatibility with the company’s OTTAVA™ Robotic Surgical System and features digital device management through the Polyphonic™ Fleet software application. The system received FDA 510(k) clearance and was showcased at the 2025 Association of periOperative Registered Nurses Global Surgical Conference.

- In February 2025, ConMed Corporation launched the HydroSeal™ Silicone Cannula, engineered to enhance maneuverability and instrument handling during arthroscopic procedures. The HydroSeal™ features a flexible design, low-profile distal flange, and double dam for effective fluid management, complementing ConMed’s powered surgical instruments portfolio.

Market Concentration & Characteristics:

The Global Surgical Drills Market demonstrates moderate to high market concentration, with a few dominant players holding a significant share of global revenues. It is characterized by continuous technological innovation, stringent regulatory standards, and strong brand loyalty among healthcare providers. Leading manufacturers compete by offering advanced features such as battery operation, ergonomic designs, and robotic integration. The market favors companies with strong distribution networks, after-sales support, and compliance with regional certifications. Product differentiation, clinical reliability, and pricing flexibility define competitive success. Entry barriers remain high due to complex regulatory approvals and the need for clinical validation. It is also shaped by growing demand for minimally invasive procedures and outpatient surgeries, driving the adoption of compact and high-performance devices.

Report Coverage:

The research report offers an in-depth analysis based on product, application, and end-use. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising global surgical volumes will continue to drive demand for high-precision surgical drills across specialties.

- Battery-powered and cordless drills will gain further market share due to their portability and efficiency.

- Integration with robotic and image-guided systems will enhance drill accuracy and support complex procedures.

- Emerging markets in Asia Pacific and Latin America will offer strong growth potential through healthcare infrastructure expansion.

- Single-use and disposable drill components will see increased adoption to support infection control measures.

- Customized, specialty-specific drill systems will cater to the growing demand for personalized surgical tools.

- Ongoing R&D investment will fuel innovation in lightweight materials and user-centric design.

- Strategic mergers and acquisitions will intensify as companies seek to expand product portfolios and global reach.

- Regulatory harmonization efforts may streamline product approvals and accelerate market entry.

- Digital connectivity and data-driven features will redefine performance monitoring and enhance surgical workflow efficiency.