Market Overview:

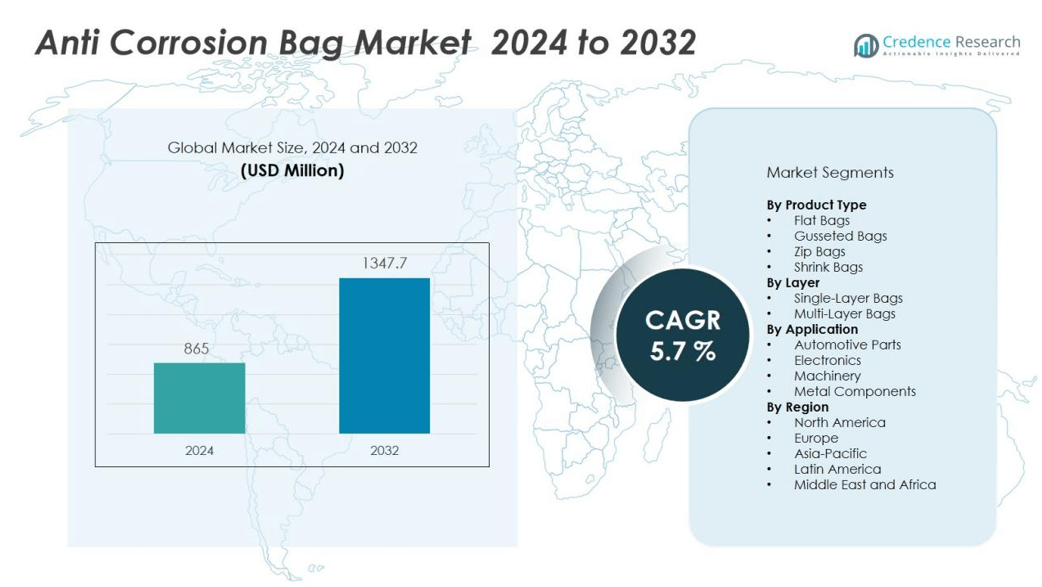

The anti corrosion bag market size was valued at USD 865 million in 2024 and is anticipated to reach USD 1347.7 million by 2032, at a CAGR of 5.7 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Anti-Corrosion Bag Market Size 2024 |

USD 865 million |

| Anti-Corrosion Bag Market, CAGR |

5.7% |

| Anti-Corrosion Bag Market Size 2032 |

USD 1347.7 million |

Key drivers supporting the anti-corrosion bag market include heightened awareness of material loss due to corrosion and stricter quality standards in end-user industries. Manufacturers are prioritizing cost-effective protection solutions to minimize product recalls, warranty claims, and reputational damage. The push for sustainable and recyclable packaging also fosters product innovation, with companies developing eco-friendly anti-corrosion bags that meet regulatory requirements and environmental targets. The ongoing digitalization of inventory management and logistics encourages more businesses to adopt advanced packaging with smart indicators, further elevating market growth.

Asia Pacific holds the largest share of the anti-corrosion bag market, driven by manufacturing activity in China, India, Japan, and South Korea. Key regional players include Gulmohar Pack-Tech India Pvt. Ltd., Northern Technologies International Corporation (NTIC), Smurfit Kappa, H L Saw Mill, NEFAB Group, and Acme Packaging. The region benefits from strong exports of automotive parts, electronics, and industrial machinery that require corrosion protection during transit. North America follows, led by the United States in technology and supply chain modernization. Europe maintains steady demand, supported by environmental regulations and a mature industrial base. Latin America and the Middle East & Africa show growth through rising industrialization and export quality focus.

Market Insights:

- The anti corrosion bag market reached USD 865 million in 2024 and will hit USD 1,347.7 million by 2032.

- Rising quality standards and strict compliance in automotive, electronics, and heavy machinery drive market demand.

- Sustainable and recyclable packaging solutions foster continuous product innovation and meet environmental targets.

- Asia Pacific leads with 47% share, benefiting from manufacturing hubs and strong exports in China, India, Japan, and South Korea.

- North America holds 28% share, with the United States excelling in technology adoption and advanced logistics systems.

- The market faces challenges from diverse industry needs, regulatory standards, and fluctuating raw material costs.

- Key players like Gulmohar Pack-Tech India Pvt. Ltd., NTIC, Smurfit Kappa, H L Saw Mill, NEFAB Group, and Acme Packaging drive innovation and supply chain reliability.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Stringent Quality Requirements Across Industrial Sectors:

The anti corrosion bag market benefits from rising quality standards in critical industries such as automotive, electronics, aerospace, and heavy machinery. Companies in these sectors prioritize corrosion prevention to avoid equipment failure, operational delays, and costly warranty claims. Regulatory bodies enforce strict compliance related to product integrity and safety, driving organizations to invest in advanced packaging solutions. It helps companies protect high-value components from moisture and oxidation during storage and shipment. End users seek reliable packaging to reduce downtime and extend product lifespan. Frequent product recalls and negative brand exposure due to corrosion incidents reinforce the demand for effective protection. These factors continue to shape procurement decisions across the value chain.

- For instance, in aerospace and sensitive applications, ProAmpac’s ProActive Intelligence Moisture Protect (MP-1000) flexible packaging technology, powered by Aptar CSP’s Activ-Polymer platform, eliminates the need for desiccant sachets while offering a high moisture-adsorbing capacity, and has been shown to extend product shelf life and lower internal package moisture to as little as 100ppm depending on product requirements.

Increasing Globalization of Supply Chains and Export Activity:

The growth of international trade and extended global supply chains drives the need for anti corrosion packaging solutions. Exporters and logistics companies require dependable products to safeguard goods during transit, particularly across varying climatic conditions. The anti corrosion bag market responds with innovative barrier technologies designed for long-haul storage and cross-border shipments. It delivers value by reducing the risk of financial loss from corrosion-related damage. The rise of e-commerce and aftermarket parts distribution further amplifies the demand for specialized protective packaging. End users value the ability to maintain product quality across long distances. This trend supports market growth in both developed and emerging economies.

- For instance, Rust-X VCI film utilizes patented moisture passivation technology and, in combined system applications, has been certified to protect steel components from corrosion for up to 10 years as validated by TL 8135-0043 and the German Razor Blade Test, providing long-term reliability for exporters and OEMs.

Ongoing Innovation in Material Science and Sustainable Packaging:

Continuous advances in material technology support the adoption of high-performance, multi-layer anti corrosion bags. Manufacturers focus on developing bags with superior moisture barrier, vapor phase corrosion inhibitor (VCI), and mechanical strength properties. The anti corrosion bag market witnesses the introduction of recyclable and biodegradable films, aligning with global sustainability goals. Companies address regulatory mandates by offering eco-friendly alternatives without sacrificing protection. It provides customers with packaging options that balance environmental responsibility and product safety. Innovations in smart packaging, such as integrated corrosion indicators, further elevate product value.

Heightened Cost Pressures and Emphasis on Operational Efficiency:

Companies aim to minimize total ownership costs through effective corrosion prevention strategies. The anti corrosion bag market addresses cost challenges by offering solutions that reduce maintenance, product returns, and warranty expenses. Firms focus on operational efficiency by streamlining packaging processes and lowering manual intervention. It allows manufacturers to improve asset utilization and reduce waste. The trend toward automation and digital inventory control increases demand for standardized, easy-to-integrate packaging. Growing awareness of hidden costs associated with corrosion reinforces the shift toward proactive protection. This approach supports both profitability and long-term customer satisfaction.

Market Trends:

Adoption of Eco-Friendly and High-Performance Packaging Solutions:

Sustainability drives a key trend in the anti corrosion bag market, with manufacturers and end users seeking eco-friendly alternatives to traditional packaging. Companies invest in developing recyclable, biodegradable, and compostable films to meet rising environmental regulations and customer expectations. The integration of vapor phase corrosion inhibitors (VCI) with environmentally safe carriers enables effective protection while supporting corporate sustainability goals. The market sees growth in the use of plant-based materials and reduced plastic content, allowing businesses to align packaging strategies with global green initiatives. It also leads to increased research and collaboration across the supply chain for innovative, compliant solutions. This shift toward sustainable materials continues to transform product portfolios and marketing strategies across major regions.

- For instance, Cortec’s EcoCorr® Film, produced in their Croatian biofilms plant, is certified industrially compostable to TÜV Austria standards and will fully disintegrate within 2–3 months in a commercial composting environment, protecting both ferrous and non-ferrous metals from corrosion while minimizing plastic pollution.

Integration of Smart Technologies and Customization Capabilities:

Advancements in packaging technology create new opportunities for the anti corrosion bag market, with a focus on smart features and tailored solutions. Companies adopt packaging embedded with sensors, corrosion indicators, and QR codes, providing real-time monitoring and improved traceability throughout storage and transit. Customization capabilities allow manufacturers to address specific industry needs, such as different metal types, dimensions, and protection durations. It increases customer confidence by offering more visibility into product condition and enhancing quality assurance programs. The trend toward digitalization of supply chains further supports the adoption of smart packaging. These developments drive market differentiation and long-term customer relationships.

- For instance, SICK sensors are deployed in packaging to deliver real-time tracking of location, temperature, and humidity quality parameters in supply chains, with some systems capable of generating over 1,000 real-time data points per shipment, strengthening visibility and risk reduction.

Market Challenges Analysis:

Complexity in Meeting Diverse Industry Requirements and Regulatory Standards:

The anti corrosion bag market faces significant challenges in addressing diverse requirements across multiple industries. Each sector demands specific protection levels, compatibility with different materials, and adherence to unique regulatory standards. Manufacturers must develop products that perform consistently in varied environmental conditions while ensuring compliance with safety and quality certifications. It requires ongoing investment in research, testing, and customization, which increases production complexity and time-to-market. Companies risk product rejection or limited adoption if solutions fail to meet customer specifications. These complexities slow market penetration and increase operational costs for suppliers.

Pressure from Raw Material Costs and Sustainable Packaging Expectations:

Fluctuating prices of raw materials, such as specialty polymers and additives, present a persistent challenge for the anti corrosion bag market. Rising input costs affect profit margins and force manufacturers to optimize sourcing strategies or transfer expenses to customers. It becomes more difficult to balance cost control with the development of sustainable packaging that meets performance and regulatory standards. Companies must innovate without compromising on affordability or environmental impact. The pressure to achieve both economic efficiency and eco-friendly solutions increases competition and requires strategic investments across the value chain.

Market Opportunities:

Expansion into Emerging Markets and Export-Oriented Industries:

The anti corrosion bag market holds significant opportunities in emerging markets where rapid industrialization and infrastructure growth create strong demand for corrosion prevention solutions. Countries in Asia Pacific, Latin America, and the Middle East & Africa are expanding their manufacturing bases and export activities. It benefits from rising investments in sectors such as automotive, electronics, and heavy machinery, which require reliable packaging for safe international transit. Local players can partner with global suppliers to introduce advanced anti corrosion technologies. Governments promoting export competitiveness further stimulate demand for high-quality packaging. These factors provide a strong foundation for market entry and long-term growth.

Product Innovation Aligned with Sustainability and Smart Packaging Trends:

Opportunities for product innovation are expanding in the anti corrosion bag market as end users seek advanced and sustainable solutions. Manufacturers can differentiate by developing recyclable, biodegradable, or reusable bags that address environmental regulations without sacrificing performance. It can leverage new materials, such as plant-based films or multi-layer composites, to meet both protection and sustainability targets. The integration of smart features, such as real-time corrosion indicators or RFID tracking, creates added value for supply chain management. Companies investing in R&D and technology partnerships will capture evolving customer needs. This innovation-driven approach positions market leaders for greater brand loyalty and global reach.

Market Segmentation Analysis:

By Product Type:

The anti corrosion bag market offers a diverse range of products including flat bags, gusseted bags, zip bags, and shrink bags. Flat bags lead segment demand due to their widespread use in industrial packaging and ease of application for various components. Gusseted and shrink bags cater to larger machinery and parts requiring complete enclosure. Zip bags provide added convenience for frequent access and resealing. Each product type addresses specific user needs in manufacturing, storage, and export activities.

- For instance, VCI2000 resealable zipper bags from Intertape Polymer Group offer 24 months of long-term corrosion protection for metal components that need regular inspection, enabled by their reusable and tamper-evident design.

By Layer:

The market segments by layer into single-layer and multi-layer bags. Multi-layer bags dominate due to their enhanced barrier properties against moisture and atmospheric gases. It finds strong acceptance in environments with high humidity or for products destined for long-distance shipping. Single-layer options remain popular for low-risk applications or shorter storage cycles. Manufacturers focus on advancing film technology to offer tailored performance for both segments.

By Application:

The anti corrosion bag market serves applications such as automotive parts, electronics, machinery, and metal components. Automotive and machinery segments contribute the largest revenue share due to high export volumes and sensitivity to corrosion damage. Electronics manufacturers rely on specialized bags to safeguard sensitive circuits and assemblies. The market’s application diversity supports stable growth and drives continuous product development across industries.

- For instance, Toyota’s plant in Cambridge, Ontario, uses PPG’s Enviro-Prime EPIC 200X electrocoat, achieving a reduction of 3,500 metric tons of CO2 emissions per year, saving 5.6 million kWh of energy, and reducing coating usage by 0.6kg per vehicle—all while delivering enhanced corrosion protection.

Segmentations:

By Product Type:

- Flat Bags

- Gusseted Bags

- Zip Bags

- Shrink Bags

By Layer:

- Single-Layer Bags

- Multi-Layer Bags

By Application:

- Automotive Parts

- Electronics

- Machinery

- Metal Components

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Asia Pacific:

Asia Pacific holds 47% share of the anti corrosion bag market, reflecting strong demand from the region’s automotive, electronics, and industrial manufacturing sectors. It benefits from large-scale production hubs in China, India, Japan, and South Korea, where exporters require advanced packaging to protect goods during transit. Local manufacturers prioritize corrosion prevention to reduce operational losses and support high-volume international shipments. Government incentives, investment in infrastructure, and a growing focus on quality control accelerate market growth. Rapid industrialization and the presence of global supply chains sustain high adoption rates. Key regional suppliers continue to invest in innovation and product customization for diverse end-user requirements.

North America:

North America accounts for 28% share of the anti corrosion bag market, with the United States leading the region in technological advancements and adoption of new packaging standards. It is characterized by a mature manufacturing sector and extensive export activities involving aerospace, automotive, and industrial equipment. Businesses focus on maintaining product integrity and compliance with strict regulatory requirements during storage and logistics. Research and development investments drive the introduction of next-generation barrier materials and sustainable alternatives. The region’s well-established distribution networks and high consumer awareness contribute to consistent demand. Strategic partnerships between suppliers and end users further reinforce market stability.

Europe:

Europe secures 19% share of the anti corrosion bag market, driven by robust regulatory frameworks and a mature industrial base. The region emphasizes environmental responsibility and product quality, pushing manufacturers to adopt sustainable packaging solutions. Key markets such as Germany, France, and the United Kingdom play central roles in innovation and export-oriented production. It witnesses steady demand from automotive, machinery, and electronics sectors, which require advanced corrosion protection. Regional suppliers compete on technical expertise and the ability to meet stringent certification standards. Public and private sector initiatives encourage ongoing improvements in packaging safety and efficiency.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Gulmohar Pack-Tech India Pvt. Ltd.;

- Northern Technologies International Corporation (NTIC);

- Smurfit Kappa;

- H L Saw Mill;

- NEFAB Group;

- Acme Packaging;

- Modi Polyfab Pvt Ltd.;

- Pontus Pack Private Limited;

- Metpro Group;

- AGM Container Controls, Inc.;

Competitive Analysis:

The anti corrosion bag market features a mix of global leaders and regional specialists focused on technological advancement and customization. Key players include Gulmohar Pack-Tech India Pvt. Ltd., Northern Technologies International Corporation (NTIC), Smurfit Kappa, H L Saw Mill, NEFAB Group, and Acme Packaging. It exhibits competitive intensity driven by constant innovation in material science, product design, and environmental compliance. Leading companies invest in research and development to deliver high-performance, sustainable solutions that address diverse customer needs. Strategic partnerships, mergers, and global distribution networks support market expansion and brand recognition. Companies compete on the basis of product quality, cost-effectiveness, and the ability to deliver tailored protection for specialized applications. The market remains dynamic, encouraging players to differentiate through innovation, customer service, and regulatory compliance.

Recent Developments:

- In September 2023, Smurfit Kappa and WestRock announced a definitive agreement to combine both companies into Smurfit WestRock, a $34 billion global leader in sustainable packaging.

- In July 2025, Nefab Group acquired Plasticos Flome, a Valencia-based company specializing in sustainable thermoforming and injection molding, further expanding Nefab’s portfolio of packaging solutions centered on sustainability and innovation.

Market Concentration & Characteristics:

The anti corrosion bag market shows moderate concentration, with several global and regional players holding significant shares. It features a diverse competitive landscape where companies compete on product innovation, quality, and compliance with environmental standards. Large players invest in research and development to introduce advanced materials and eco-friendly solutions, while regional firms focus on cost efficiency and local market requirements. The market serves a wide range of industries, including automotive, electronics, and heavy machinery, driving continuous demand for specialized packaging. Rapid industrialization in Asia Pacific and ongoing technological advancements influence market dynamics. The need for customized, high-performance solutions shapes purchasing decisions and supports ongoing competition among key suppliers.

Report Coverage:

The research report offers an in-depth analysis based on Product Type, Layer, Application and Region.It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Adoption of bio-based and recyclable materials will strengthen product appeal and align with sustainability mandates.

- Smart packaging features such as corrosion indicators and RFID tags will improve traceability and quality assurance.

- Collaboration between packaging manufacturers and end users will drive tailored solutions for specific industrial needs.

- Regional expansion into emerging markets will unlock new revenue streams and diversify customer portfolios.

- Focus on lightweight and space-efficient designs will reduce logistics costs and simplify handling.

- Integration of barrier technologies will bolster performance in high-humidity and long-duration storage environments.

- Digital inventory management systems will reinforce demand for packaging with enhanced compatibility and standardization.

- Demand from aftermarket parts sectors will increase need for reliable protection during transit and storage.

- Environmental regulations will accelerate innovation in sustainable anti corrosion bag offerings.

- Investment in R&D will enable development of multi-functional packaging that meets both technical and eco-friendly criteria.