Market Overview:

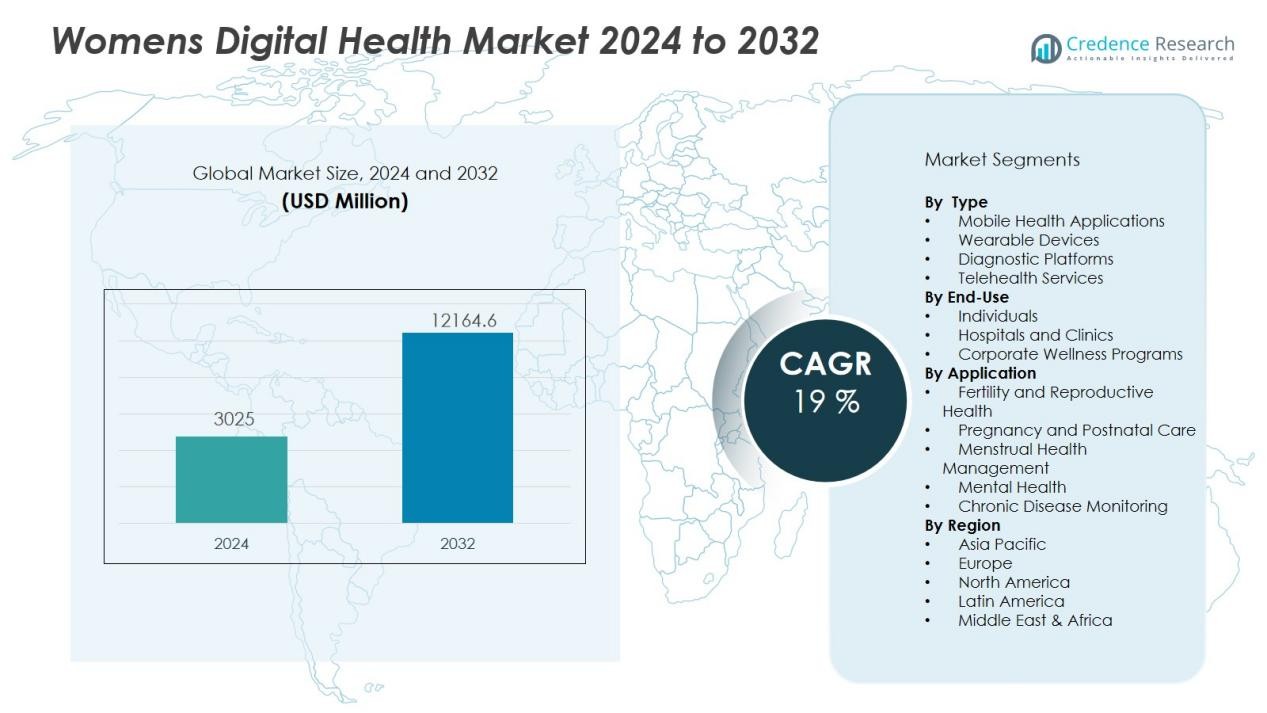

The Womens digital health market size was valued at USD 3025 million in 2024 and is anticipated to reach USD 12164.6 million by 2032, at a CAGR of 19 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Women’s Digital Health Market Size 2024 |

USD 3025 Million |

| Women’s Digital Health Market, CAGR |

19 % |

| Women’s Digital Health Market Size 2032 |

USD 12164.6 Million |

Key market drivers include growing awareness of women’s health issues, increasing adoption of smartphones and digital platforms, and rising investments from both public and private sectors in femtech innovation. The market further benefits from an expanding range of digital health offerings covering fertility, reproductive health, pregnancy care, menstrual tracking, and chronic condition management. Accelerating demand for personalized healthcare, coupled with the increasing prevalence of conditions such as PCOS, endometriosis, and breast cancer, fuels the adoption of digital health solutions among women worldwide.

Regionally, North America dominates the women’s digital health market due to high technology penetration, supportive regulatory policies, and well-established healthcare infrastructure. Europe follows closely, driven by growing femtech investments and government support for digital health adoption. Meanwhile, the Asia-Pacific region is witnessing the fastest growth, supported by increasing internet penetration, rising healthcare expenditure, and expanding awareness of women’s health issues.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The women’s digital health market reached USD 3,025 million in 2024 and is expected to achieve USD 12,164.6 million by 2032, reflecting a robust CAGR of 19%.

- Rising awareness of women’s health issues and increasing demand for personalized healthcare solutions fuel rapid adoption of digital platforms.

- Growth is supported by widespread use of smartphones, digital health applications, and ongoing investments in femtech innovation by public and private sectors.

- Expanding offerings now address fertility, reproductive health, pregnancy care, menstrual tracking, and chronic disease management for women globally.

- Data privacy, cybersecurity concerns, and regulatory complexities challenge providers, requiring robust safeguards and clear compliance strategies.

- North America leads the women’s digital health market, driven by high technology penetration, supportive policies, and strong healthcare infrastructure, with Europe and Asia-Pacific following.

- Disparities in digital access and health literacy, particularly in rural and low-income regions, highlight the need for inclusive solutions and interoperability to support equitable market growth.

Market Drivers:

Rising Awareness and Demand for Personalized Women’s Healthcare Solutions:

The women’s digital health market experiences strong momentum due to greater public awareness of women-specific health challenges and a growing demand for tailored medical solutions. Consumers seek convenient, accessible, and confidential health management tools for issues ranging from menstrual health to chronic diseases. Awareness campaigns and education initiatives drive engagement with digital platforms that empower women to monitor, track, and manage their health proactively. This trend encourages technology developers and healthcare providers to invest in innovative applications that meet the evolving needs of female users.

- For instance, Flo Health’s Flo app supports tracking of over 300 different menstrual and related symptoms across more than 200 million downloads.

Expansion of Digital Infrastructure and Mobile Technology Adoption:

Rapid advancements in digital infrastructure and widespread adoption of smartphones significantly contribute to the women’s digital health market. Mobile health applications and wearable devices offer women seamless access to healthcare services, teleconsultations, and real-time health tracking. It allows users in both urban and rural areas to overcome traditional barriers such as location and availability of specialist care. Reliable internet access and the proliferation of digital devices create a foundation for scalable and user-friendly digital health solutions.

- For instance, the Apple Women’s Health Study preliminary cohort included over 50,000 participants contributing menstrual cycle data via iPhone and Apple Watch.

Supportive Regulatory Environment and Increased Investment in Femtech:

Supportive government regulations and increased funding for femtech startups are critical drivers for the women’s digital health market. Policymakers recognize the need for better access to women’s healthcare and support digital innovation through favorable policies and incentives. Private equity and venture capital investments fuel research and development of advanced digital health products tailored for female health needs. It strengthens the market’s competitive landscape and encourages continued innovation.

Growing Prevalence of Chronic Conditions and Focus on Preventive Care:

The increasing incidence of chronic conditions such as PCOS, endometriosis, and reproductive cancers among women accelerates demand for advanced digital health solutions. Early diagnosis, remote monitoring, and preventive care become priorities, prompting adoption of data-driven platforms. The women’s digital health market responds with sophisticated tools that support disease management, improve health outcomes, and lower healthcare costs. It positions digital health technologies as essential components of modern women’s healthcare strategies.

Market Trends:

Integration of Artificial Intelligence and Data Analytics Transforms Women’s Digital Health Solutions:

The women’s digital health market witnesses a significant transformation through the integration of artificial intelligence and advanced data analytics. AI-powered applications enhance diagnostic accuracy and provide personalized health insights for conditions such as fertility, pregnancy, and chronic disease management. Predictive analytics tools help identify potential health risks and optimize treatment pathways, making preventive care more effective. Technology companies develop smart algorithms that adapt to individual user profiles and deliver real-time, actionable feedback. It enables healthcare providers to tailor recommendations, improve patient engagement, and increase adherence to health plans. Data-driven decision-making improves outcomes and supports the shift toward value-based care within women’s health. The market benefits from continuous investment in AI research and digital platform development.

- For instance, Flo Health’s neural network integration with InData Labs improved irregular cycle prediction accuracy by 54.2% after processing over 450 GB of user data.

Expansion of Telehealth and Remote Monitoring Capabilities Drives Accessibility and Engagement:

A growing emphasis on telehealth and remote monitoring significantly shapes the women’s digital health market, making healthcare more accessible and convenient for women worldwide. Telemedicine platforms enable secure consultations, mental health support, and ongoing care without requiring physical visits to healthcare facilities. The adoption of connected devices, such as wearable trackers and smart diagnostic tools, empowers users to monitor vital signs, reproductive cycles, and chronic conditions from home. It enhances early intervention and fosters continuous engagement between patients and healthcare providers. Companies in the sector focus on developing user-friendly interfaces and integrating multiple health functions into single platforms. The market sees an increase in strategic partnerships among technology firms, healthcare providers, and payers to expand service offerings and reach. This ongoing digitalization helps bridge gaps in women’s healthcare access, especially in underserved regions.

- For instance, ŌURA has sold more than 2.5 million smart rings, now with 59 percent of its users identifying as female.

Market Challenges Analysis:

Data Privacy, Security Concerns, and Regulatory Complexity Hinder Market Advancement:

The women’s digital health market faces significant challenges related to data privacy and cybersecurity risks. Consumers hesitate to share sensitive personal information without strong assurances of confidentiality and robust safeguards. Evolving global regulations, such as GDPR and HIPAA, add layers of complexity to compliance for technology providers. Navigating multiple regulatory frameworks increases operational costs and slows the launch of new products. It requires companies to invest heavily in secure data management and transparent privacy policies. The risk of data breaches and misuse remains a major barrier to user trust and widespread adoption.

Digital Divide, Limited Health Literacy, and Market Fragmentation Affect Accessibility:

Disparities in digital infrastructure and health literacy present ongoing obstacles for the women’s digital health market. Many women in rural or low-income areas lack access to reliable internet or smart devices, limiting their ability to benefit from digital health solutions. Low awareness and understanding of digital health tools further hinder effective adoption. It complicates user onboarding and long-term engagement for technology providers. Fragmentation among digital health platforms and lack of interoperability with traditional healthcare systems create inefficiencies and reduce the impact of digital innovations. The market must address these barriers to achieve equitable and scalable growth.

Market Opportunities:

Personalized Wellness Solutions and Emerging Femtech Applications Expand Market Reach:

The women’s digital health market presents strong opportunities through the development of personalized wellness solutions and innovative femtech applications. Companies leverage AI and big data to deliver tailored care for fertility, pregnancy, menopause, and chronic condition management. Customizable digital platforms empower women to take proactive control of their health, increasing long-term engagement and satisfaction. Growing interest in preventive health and lifestyle management fuels demand for holistic, integrated platforms. It creates space for startups and established players to differentiate their offerings and enter new market segments. Collaboration with healthcare providers and insurers enhances credibility and broadens user adoption.

Global Expansion and Strategic Partnerships Drive Scalability and Innovation:

Opportunities in the women’s digital health market extend to underserved geographies and emerging economies where healthcare access remains limited. Companies can scale their solutions by forming partnerships with local health systems, NGOs, and governments to overcome infrastructural and educational barriers. It allows for more inclusive product development and supports regulatory approval in diverse markets. Strategic alliances with technology companies and research institutions accelerate innovation and improve interoperability of digital health platforms. The focus on global expansion and ecosystem building unlocks new revenue streams and strengthens market resilience against competitive pressures.

Market Segmentation Analysis:

By Type:

The women’s digital health market features a diverse range of digital solutions, including mobile health applications, wearable devices, diagnostic platforms, and telehealth services. Mobile health applications lead this segment, providing convenient access to health tracking, education, and virtual consultations. Wearable devices gain traction for their ability to monitor vital signs, reproductive cycles, and activity levels, offering personalized insights. Diagnostic platforms integrate with digital apps, enabling early detection and timely management of female-specific health conditions. It sees growing adoption of telehealth services, particularly in regions with limited access to traditional care.

- For instance, ŌURA has sold 2.5 million smart rings to date, with members opening the app more than three times daily to track sleep, readiness, and menstrual cycle metrics.

By Application:

Key applications within the women’s digital health market include fertility and reproductive health, pregnancy and postnatal care, menstrual health management, mental health, and chronic disease monitoring. Fertility and reproductive health remain the most prominent application, with digital tools supporting ovulation tracking, IVF planning, and hormonal balance. Pregnancy and postnatal care platforms provide continuous support and education for expecting and new mothers. Solutions for menstrual health management empower women to monitor cycles, symptoms, and related disorders. The market also emphasizes mental health support and management of chronic conditions like PCOS, endometriosis, and breast cancer.

- For instance, Ava’s fertility bracelet achieved a 90% ovulation-prediction accuracy in a 2024 clinical study involving 1,200 participants.

By End-Use:

End-users of women’s digital health solutions include individuals, hospitals and clinics, and corporate wellness programs. Individual users form the largest share, driven by rising health awareness and self-management preferences. Hospitals and clinics adopt digital tools to streamline patient care, improve diagnosis, and enhance patient engagement. Corporate wellness programs incorporate women’s health solutions to promote workforce well-being, reduce absenteeism, and support employee retention. It demonstrates wide-ranging adoption across all end-use categories, underlining its versatility and growth potential.

Segmentations:

By Type:

- Mobile Health Applications

- Wearable Devices

- Diagnostic Platforms

- Telehealth Services

By Application:

- Fertility and Reproductive Health

- Pregnancy and Postnatal Care

- Menstrual Health Management

- Mental Health

- Chronic Disease Monitoring

By End-Use:

- Individuals

- Hospitals and Clinics

- Corporate Wellness Programs

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America :

North America holds a leading position in the women’s digital health market with a market share exceeding 38% in 2024. The region benefits from advanced healthcare infrastructure, high digital literacy, and rapid adoption of innovative technologies. Strong presence of leading femtech companies and active investment from venture capital drive continuous product development. Favorable regulatory frameworks support the introduction of new digital health solutions tailored to women’s needs. The market sees robust demand for telehealth, remote monitoring, and personalized health applications across the United States and Canada. High rates of smartphone usage and widespread health insurance coverage create an environment conducive to digital health expansion. It positions North America as a hub for both innovation and commercial growth in the sector.

Europe:

Europe accounts for a market share near 28% in the women’s digital health market, driven by supportive government initiatives and rising public awareness. Policymakers focus on expanding digital healthcare access and improving gender-specific medical outcomes. The European Union invests in research programs and cross-border collaborations that foster a strong femtech ecosystem. High rates of internet penetration and mobile device usage support widespread adoption of digital health platforms for women. Markets in Western Europe, particularly the UK, Germany, and France, see the highest concentration of femtech startups and funding. Consumer emphasis on preventive health and well-being accelerates demand for digital wellness solutions. It strengthens Europe’s position as a leader in the global digital health transformation for women.

Asia-Pacific :

Asia-Pacific holds a market share close to 22% in the women’s digital health market and demonstrates the fastest growth rate during the forecast period. The region benefits from rapid urbanization, rising disposable incomes, and an expanding base of tech-savvy consumers. Governments in countries such as China, India, and Japan invest heavily in digital health infrastructure and public health campaigns. Increasing internet connectivity and smartphone penetration facilitate access to digital health tools for women across both urban and rural areas. The market sees significant entry of local and international players seeking to capture emerging opportunities. It creates a dynamic landscape marked by strong innovation and competition. Asia-Pacific’s growing focus on women’s health and wellness will play a crucial role in shaping the future trajectory of the global market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

Competitive Analysis:

The women’s digital health market demonstrates high competition, driven by rapid innovation and diverse product offerings. Key players such as HeraMED, Chiaro Technology Ltd., iSono Health, Clue by Biowink, Ava Science, Inc., NURX Inc., Natural Cycles, and Prima-Temp, Inc. invest in advanced technology and data-driven solutions to strengthen their market presence. Companies focus on expanding their product portfolios, enhancing user experience, and securing regulatory approvals to gain a competitive edge. Strategic partnerships and collaborations with healthcare providers, insurers, and research institutions help companies access wider user bases and accelerate innovation cycles. The market rewards firms that prioritize security, personalization, and seamless integration with traditional healthcare systems. It continues to attract new entrants, intensifying the competitive landscape and pushing established brands to evolve rapidly.

Recent Developments:

- In June 2024, marked the soft launch of HeraMED’s HeraCARE maternity solution within the Telstra Health Connected Care Ecosystem.

- In May 2025 brought about a research collaboration where HeraMED joined forces with RMIT University and the Digital Health CRC to enhance maternal health outcomes through AI-enabled predictive care, with a project value of $1.25 million.

- In January 2023, initiated a distribution agreement between iSono Health and Abdul Latif Jameel Health for the ATUSA scanner, broadening its availability across 31 countries in the Global South.

Market Concentration & Characteristics:

The women’s digital health market exhibits moderate to high concentration, with a mix of established healthcare technology companies and a dynamic landscape of specialized femtech startups. Leading players invest heavily in research and product innovation, focusing on data security, regulatory compliance, and user-centric platforms. The market features rapid technology adoption, high customization, and frequent new product launches targeting specific women’s health needs such as fertility, menstrual health, and chronic disease management. It remains characterized by strategic partnerships, mergers, and acquisitions, enabling expansion of product portfolios and geographic reach. Competitive differentiation relies on integration of advanced analytics, seamless user experiences, and scalability, which drive ongoing market evolution.

Report Coverage:

The research report offers an in-depth analysis based on Type, Application, End-Use and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- Developers will enhance personalized wellness tools by using artificial intelligence, improving predictive accuracy and user experience.

- Telehealth platforms will gain deeper integration with wearable sensors and remote diagnostics to boost continuity of care.

- Providers will expand global reach through strategic collaborations with healthcare systems and local organizations in emerging economies.

- Expansion of mental health and perinatal care solutions will support underserved segments and guide holistic women’s wellness.

- Data privacy frameworks will become more robust, enabling it to build trust through encrypted health records and user consent protocols.

- Health insurers and employers will incorporate digital women’s health offerings into workplace wellness and benefits packages.

- Demand for multilingual, culturally sensitive platforms will increase, supporting inclusivity across diverse populations.

- Interoperability between digital health apps and electronic health records will improve, facilitating provider coordination and patient continuity.

- Investment in research around female-specific biomarkers and diagnostic algorithms will accelerate product innovation in femtech.

- Regulatory agencies will streamline approval pathways and support evidence-based digital health interventions tailored for women.